81b01e121cc5613db24d488066d527a8.ppt

- Количество слайдов: 40

XBRL Adoption by Tax Administrations Eric E. Cohen Chair, XBRL US; Co-founder, XBRL; Chief Architect, XBRL GL eric. e. cohen@us. pwc. com

What is XBRL? A consortium An archival format XBRL A transfer syntax Supply chains working to develop XML for business reports A standardised way to design XML Standards (Not a specific XML standard) Specification: syntax and semantics of taxonomies and instances Optimized for Business Reporting

XBRL GL Fills the GAPS between GAAPS On e wa y Tax Regulators Investors Creditors Lende Website rs Aggregators Intra system 2 way XBRL BUSINESS REPORTING ERP Detail Suppliers G/L Packages On e wa y Detail to summary CRM XBRL GL Journal Taxonomy Transaction Creation Accounting recognition/ (e-)Business classification • Orders Customers • A/P • A/R X 12, UN/CEFACT Forum, UBL, HR-XML, ACORD, • Delivery MISMO, and other XML INITIATIVES 2 -way

Why are Tax Authorities Looking at XBRL? § EFiling, e. Government and other efforts § Representing current e. Filing in friendlier face § Financial statements and information § Same payload useful for many purposes, comparable § Note: different jurisdictions and the “books” § Universal audit trail § From transactions through the business reporting supply chain § Other business information § XBRL: Summarized, aggregated, filtered, (sorted) § XBRL GL: Underlying detail

XML and Other Reusable Formats Attributes of “standard” formats XML HTML Variable length fields Yes No field size limitations ASCII Fixed CSV Excel DBF EDI Yes No Yes Yes Yes No No Yes Extensible Yes * No No * * No Includes context or field names (“rip and read”) Yes No No No Yes No Cross-platform, nonproprietary, “universal” Yes Yes No No Yes Validation of files Yes No No No * * No Groups collaborating on definition and interoperability Yes No No No Yes Selective digital signatures Yes * No No No Selective encryption Yes * No No No Standard Office import/export Yes Yes Yes No Not verbose, smaller file sizes * * * * Note: PDF is a very popular document exchange format, but is primarily designed for human, and not computer, consumption. Likewise, TIF, GIF, JPG, BMP and other binary graphics formats. Note 2: UNICODE is an “update” to ASCII more useful in the international context. weakness workaround strength

One Framework § One format § Optimized for business reporting information § Attributes of business reporting information § Needs of business reporting information § Lowering preparation/compliance burden § Smoother collection of data of all kinds § Reduction of things published to reconcile and track § More common adoption by software developers § Web Services

XBRL § § Internationally Developed Royalty-free Optimized for business reporting Entirely XML-family based § XML, XML Namespaces, XML Schema, XLink § Holistic § One family, one framework, collaborative, compromise for greater common good § Interoperability - validation, comparison across data sources

Oxymoron: Customizable Standards § Standardized Customization § X - Extensibility § Greater community gets commonality § Local community gets flexibility, customization § A new world that brings customization and compromise together § Standards § Standardized customization § “Bread trail” from customization to standards

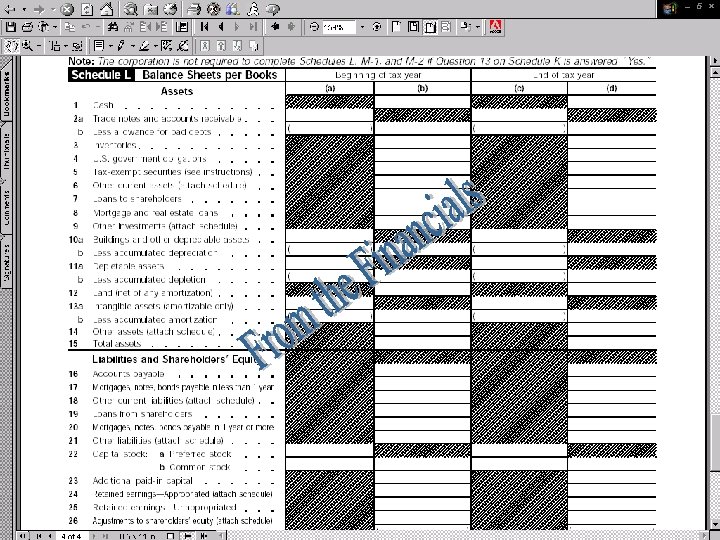

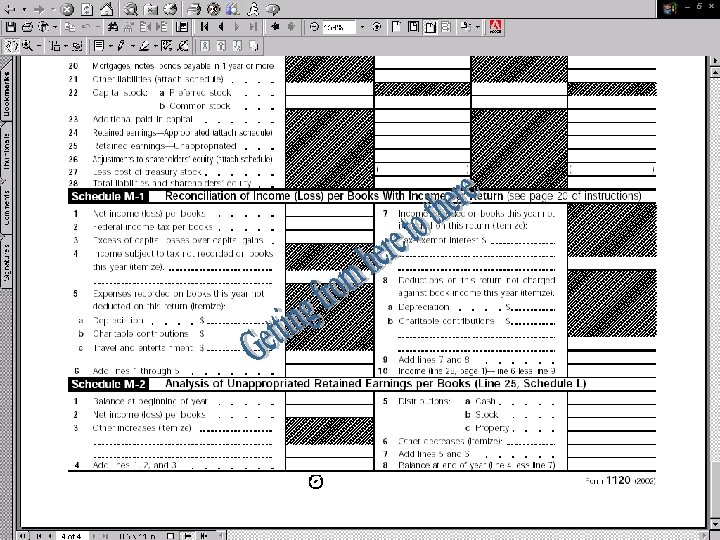

XBRL § Post processed reporting § Financial statements § US § IFRS § German § Japan § Many other countries § Bank call reports, tax forms, other formats § Detail (XBRL GL) § Entries, agents, resources, documents § Universal audit trail § Who is using the same version of the same accounting system as 1999?

Reporting Ledger Database Operations Ledger Reporting Ledger Database Operations Reporting Operations Ledger Database Consolidated Management GAAP Statutory

<>

Customer, vendor, employee KEY Core Saxon Business Multicurrency

Invoice, voucher info Inventory, Value. Reporting KEY Core Saxon Business Multicurrency

Congress Treasury Tax Policy Analysts Regulator filing format Guidance Checklists Practitioner Aids CLIENT Organizer Regulations News Instructions Filing formats Reference Integrated Non-integrated Outsources ASP Trading Partners Lenders Other Regulators The Market Service Regulator Service Extranet Software developers 3 rd Parties Regulator

Tax Regulators Involved in XBRL

Australian Tax Office § ATO recently joined the XBRL Consortium § Considering XBRL 2. 1 as the standard for electronic filings § Phased implementation: § Activity Statements (12 M filings annually) § Phase I scheduled for the end of 2003 § Anticipated benefits: § Time and cost savings § Enhanced information processing

Canada Revenue Agency § Active member of XBRL Canada § Presentation to follow § (Slide from last meeting attached - was CCRA)

Canadian Value Proposition CCRA XML Exchange/Transformation Employers Tax VAT GST Excise New and Legacy Systems Internally XML Exchange/Transformation CCRA Taxonomies Corp. Tax T 2 Externally STF BI/DS Individ. Tax T 4 T 2 Benefits GST Others XML Exchange/Transformation CCRA XBRL Taxonomy snapshot XBRL Chart of Accounts (GAAP) Instance Document Other Gov’ts Other Gov’t Depts TBD Other Levels of Gov’ts TBD Externally

§ Workgroup \"XBRL Taxonomie Steuern\" (Taxonomy for Tax Filing)")

German Tax Agency (Oberfinanzdirektion München) § Workgroup "XBRL Taxonomie Steuern" (Taxonomy for Tax Filing) § XBRL Deutschland e. V. workgroup establishing XBRL as a standard for electronic tax filing in Germany. § The workgroup's agenda comprises: § Development of a taxonomy (or expansion of the existing taxonomy German. AP) in order to render all pertinent data § Processing and operating (data delivery workflow, assurance, certifying data quality) § Information exchange with international workgroups and other jurisdictions focusing on this issue § Back end processing still an issue § Staffing § Staffed by Oberfinanzdirektion München (tax authority), DATEV, and software providers. § Date of last update: May 27, 2003 - see http: //www. ofd. bayern. de/ofdmuenchen/

Japan - National Tax Agency § What: Portion of Electronic Tax Filing, i. e. Financial Statements § Crucial Project for XBRL Japan § NTA will nominate/endorse any XML-based FS submission if it proves to work § Currently only XBRL is on NTA’s radar screen. § Large Scale Project § Impact on virtually all companies § When: NTA plans to make tools available in November 2003, to go live in March, 2004 (corporate tax filing for the year 2003). § How: Based on the latest XBRL Specification § Based on XBRL Japan’s “sample” Taxonomy § Effect: XBRL-enabled accounting software products emerging. § When actually started, it will accelerate adoption at large scale. § Updated news as of Dec-03 as follows:

§ § § Their “e-tax” project is positioned as a part of implementation of e-government plan (“e-Japan”) using digital signature. Adoption of XBRL is admitted as a one of acceptable formats for the financial statements attached to filing information. The financial statements received in XBRL format are to be printed in paper to validate the contents. Direct linking to the agency’s internal system is considered difficult at this point. This system is giving clear priorities on interface to taxpayers. Implementation of STP in NTA is left unfulfilled. Filers create tax returns in XML format in this system, and adoption of XBRL is admitted for some documents in accompanying materials (corporate financial statements, business summary report, etc. ) Verification of numerical consistency and accuracy, between tax returns in XML and attached financial statements in XBRL, is not available yet in a systematic way. The NTA should perform those procedures in manual fashion in the meanwhile. The reason of selecting Nagoya as the first jurisdiction to launch e-tax system: 1) it has 10% of the nation wide tax revenue and 2) it has well-assorted kinds of taxpayers. NTA has a system to perform complex validation, analysis and statistical work, called “KSK system” (a back office system). Software application for creating tax return will be distributed to taxpayers in a CD-ROM. NTA can issue certificates of tax payment (electronic certificate of tax payment) to taxpayers, however NTA cannot show those certificates to a third party since law prohibits it. Certificates are only seeable within local government agency. When a taxpayer presents a tax return to the NTA, he also prepares a copy of the return. The NTA affixes a reception stamp on the copy for the taxpayer; however, it only proves that the NTA has received his/her return, not that the copy is identical to the submitted return. On the e-tax system, the NTA returns e-mail that says they received a return. < Upcoming schedule > § February 2, 2004 – e-tax filing for income tax and consumption tax filing (for personal business) will be available § § § for the taxpayers in the jurisdiction of Nagoya Regional Taxation Bureau (including the prefecture of Gifu, Shizuoka, Aichi and Mie). March 22, 2004 – other than the tax filing listed above, e-tax filing for corporate tax, consumption tax (corporate), tax payment for all tax items and some of the submission process for tax applications and notifications will be available for the taxpayers in the jurisdiction of Nagoya Regional Taxation Bureau. June 1, 2004 – all e-tax procedures started in Nagoya jurisdiction will be available throughout the country. From September 2004 – e-tax filings for other submission processes for tax applications and notifications will be available for the taxpayers nationwide.

Netherlands § Dutch Tax and Customs Administration § Mandate for e. Filing by 1/2005 § Corporate tax: >90% in XML § Portal access for 100% of corporate tax users § Today § Corporate tax: 1% today in XML § Personal tax, based on simple XML: 90% § Customs: 80% using an EDI model § Options § Offline filing based on standard e. Media Jul-2004 § Online web-based forms starting Feb-2004 § Considering XBRL § Government initiative to reduce compliance burden § XBRL can be catalyst for reducing costs

§UK Inland Revenue § § § Electronic filing processes Persuasive business case Office of e-envoy 2004 optional filings All compliance software vendors in place § Also evaluating role within audit and VAT

Other XBRL International Members § Irish Revenue § Inland Revenue Authority of Singapore § Inland Revenue Department of New Zealand § Encouraging development and adoption § Collaborating on financial statement and other taxonomy development § Collaborating on common issues regarding security, audit and other issues - WIN-WIN

Information TAX INSTRUCTIONS Paper Support FINANCIAL STATEMENT TAX FORM Corporate Data feeds direct access or extracts Operational Data

Streamlined Processing XBRL for Financial Statements XBRL G/L Common Audit Trail Processes Business Operations XBRL for Business Event Reporting Internal Financial Reporting External Financial Reporting XBRL for Audit Schedules XBRL for Tax Filings Trading Partners CFO’s Investment and Lending Analysis Financial Publishers and Data Aggregators Companies Participants XBRL for Regulatory Filings Auditors Software Vendors Investors Regulators/Stock exchanges

The architecture of XBRL Taxonomy Labels Instance Document Reference Definition Concept Presentation Fact Calculation Formulae Context Entity Period Segment Unit CWA Scenario Precision

Why XBRL? XBRL adds to XML: § Multi dimensional data Definitions AKA Liquid Assets contexts § Mathematical relationships between concepts § Flexibility about how to References Presentation GAAS I. 2. (a) USSGL 1100. 00 Cash & Cash Equivalents XBRL Item present items to users § Aliases and other definition relationships § Links to authoritative literature and guidance § Financial reporting vocabularies (taxonomies) Reporting apps need these even when using XML. Calculations Formulas Cash = Currency + Deposits Cash ≥ 0 Contexts USD FY 2003 Budgeted

How XBRL Compares to Proprietary XML Attributes of formats XBRL Proprietary XML Uses W 3 C standards for XML and related technologies Yes Holistic framework (can, of course, have non-XBRL framework) Yes * Documented and proven agreement on syntax and semantics of schema design and instance design Yes No Groups collaborating on definition and interoperability Yes No Agreed upon tools for extensibility Yes * Software vendor community developing tools that help with specifics of syntax Yes * Reuse of IP Yes * weakness workaround strength

Why XBRL Linkbases Over “Standard” XML Schema Attributes of formats XBRL Schema alone * Yes Human readable labels provided in various languages and for specific purposes as part of deliverable Yes No Guidance on hierarchy and presentation order for applications Yes No Guidance on hierarchy and (sub-)totals for applications Yes No Standardized rules for extensibility of all of the hierarchies Yes No Standard tools for identifying relationships across taxonomies, such as “Same-as” relationships Yes No Standard tools for relating concepts to underlying authoritative literature and explanatory guidance Yes No Prescribes and limits XML Schema for business reporting Yes No A single hierarchy using complex. Types makes it easy to see that hierarchy with standard tools like XML Spy weakness workaround strength

Why XBRL for XML Reporting Standard? § Community developed concepts with communication of meaning, support, requirements § Advantages to development community, users § Greater picture § More than just efficiencies as point-to-point, single use filing § Greater integration with internal systems § Filing § Definition, validation (PRE-validation) § Extensibility § Internal and then external sharing

XML Without Agreement … § XML is “selfdefining? ” § Sure, this looks simple:

… is just SYNTAX § But how “self-defining” is this? § To a computer (XML parser), they are the same. § The tags (element names) provide no semantic knowledge to the program. § NEED TO COMMUNICATE MEANING - across languages enter XBRL!

Some Options § Ignore/disallow XBRL altogether § XBRL as an option for filers § Required statutory accounts in local XBRL format as payload § XBRL based standards for one or more tax filings § Mandate that XBRL be used for some or all reporting § XBRL as an INTERNAL efficiency tool § Compliance, audit, reporting to outsiders share common language, tools § Cooperate and collaborate for more global XBRL adoption and usage § Reduce everyone’s costs

Representative XBRL-enabled Products § Shipping § § § Oracle FSG People. Soft SAP my. SAP financials Hyperion Microsoft Business Solutions Navision, Axapta Creative Solutions (et al. ) § Caseware § About to ship § Microsoft Office 2003 Add-in

XBRL Outreach § XBRL in general § Interoperability pledge § Other efforts § XBRL GL and audit/continuous audit community § XBRL GL and electronic efforts § XBRL and Tax XML § We have common needs, interests and all fit in the Business Reporting Supply Chain § Not just technical needs § Future development issues - including security/Digi. Sig

XBRL Issues § XBRL is NOT point-to-point, proprietary schemas § Ease of development and fast implementation § Familiarity § XBRL GL is MORE than tax authority needs § Familiarity with Schemas and complex. Type relationships § XBRL Specification 2. 1 and complex. Types § Incentives § Others

81b01e121cc5613db24d488066d527a8.ppt