59f6547d19f6de24769773a5d3835a08.ppt

- Количество слайдов: 27

WIPO Asia Sub-Regional on the Use of IP by SME Support Institutions for the Promotion of Competitiveness of SMEs in the Food Processing Sector Lahore, Pakistan, June 5 and 6, 2007 Guriqbal Singh Jaiya Director SMEs Division, WIPO

Intellectual Property Audits 1. 2. 3. 4. 5. 6. 7. Intellectual Property What is an IP audit Why do an IP audit When should an IP audit be done Who should do an IP audit How should an IP audit be done After an IP audit

1. Intellectual Property Rights n Innovative products/processes n Patents or utility models n Cultural, artistic and literary works n Copyright and related designs n Creative designs n Industrial design rights n Distinctive signs n Trademark, Collective mark n Microchips n n Goods of a given quality due to its geographical origin Confidential business information n Layout-designs or topographies of integrated circuits. Geographical indications n Trade secrets n

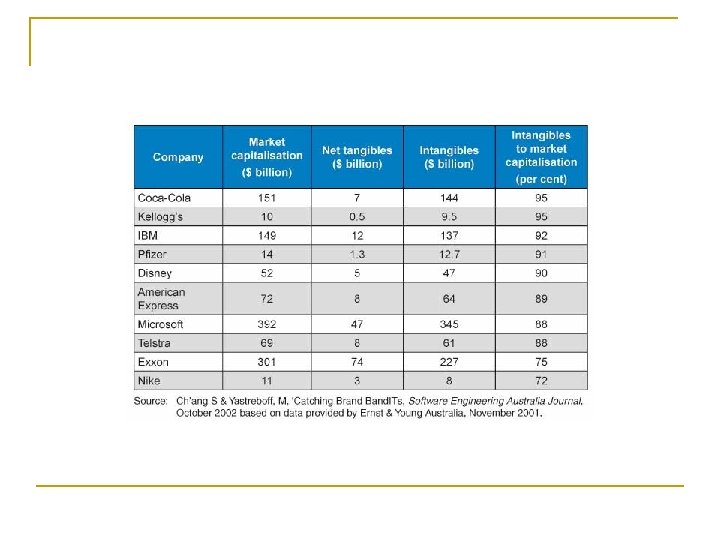

Knowledge Economy intangible Assets 20% tangible Assets 80% tangible Assets 20% intangible Assets 80%

2. What is IP Audit? n n In the knowledge economy intangibles have taken center stage Like tangible assets IP has to be identified, protected and maintained to q q n maximize their value and minimize the potential for third party abuse prevent inadvertent loss ensure freedom to operate IP audit is a review involving the identification of the IP owned, used or acquired by a business, its management, maintenance, exploitation and enforcement

3. Why do an IP audit n n Enables a company to identify its IP assets Make decisions with respect to those assets; q q q whether rights have been or should be acquired for them, whether they are or should be maintained, how best they could be exploited, are there any redundancies, threats to those rights, infringements of others rights etc. .

Importance of IP Assets n n n The overall importance of IP assets to the business will have a bearing on the audit. Where IP assets are relatively unimportant to the nature of the business as a whole, it might be sufficient merely to confirm that registered IP rights are in good standing and are held in the name of the company. Where the company’s principal assets are IP, it may be necessary to conduct a more thorough assessment of the company’s IP portfolio and IP based activities.

4. When to do an IP audit n n n General purpose IP Audit; Event driven IP audit; Limited purpose focused audits

General Purpose IP Audit n n Before establishing a new company. q It is always important for a start-up company to be aware of intangible assets it owns or needs to protect. When a business is considering implementing new policies, standards, or procedures relating to IP. When a business is considering implementing a new marketing approach or direction, or is planning a major reorganization of the company. When a new person becomes responsible for IP management

Event Driven IP Audit n n n An “event driven” IP audit is often called IP due diligence when done to assess the value and risk of a target company’s IP assets. IP due diligence is a part of a comprehensive due diligence audit that is done to assess the financial, commercial and legal risks linked to a target company’s IP portfolio, typically before it is bought or invested in. It can provide detailed information that may affect the price or other key elements of a proposed transaction or even aborting the further consideration of the proposed transaction.

Event driven IP Audit n n n Before entering into a financial transaction involving IP Buying or selling a division, product line Licensing Bankruptcy IP disputes Outsourcing

Limited purpose focused audits n n Personnel turnover q Before a major personnel turnover of in-house R&D or marketing staff, especially if they are disgruntled employees. Foreign IP filings q Before a company takes up an aggressive program of filing IP applications in other countries for entering a new market abroad or expanding overseas through off-shoring/outsourcing. Before having an Internet presence q helps it to identify the needs of e-commerce and registration of appropriate domain names, etc. Significant changes in IP law and practice

")

5. Who should perform an IP Audit? n n Company personnel (in-house counsel, management) Outside counsel who have experience with such audits in the particular industry, in IP management issues

6. How to do an IP Audit? n n n Define an audit plan Define a schedule for the audit Define responsibilities among the audit team

An Audit Plan n n Prepare a check list modified for the type and size of the company’s business, IP laws, purpose and desired outcome of the audit Include a list of the documents to be reviewed q license agreements, distribution agreements, government contracts, employee and consultant agreements, journal articles, published papers, competitive analysis documents, marketing files, patents, lab notebooks, assignments… The specific areas of the business to be covered Define the personnel to be interviewed q Attorneys, Brand managers/marketing, those responsible for websites, R & D Personnel (employment agreements and policies), Graphic designers Prepare questionnaire

Auditing agreements n Licensing agreements: Assignment agreements: . Employment and independent Contractor agreements Joint venture agreements: Government contracts Technology transfer, or know how, or technical assistance agreements Design and development agreements Settlement agreements Franchise agreements Royalty agreements Marketing agreements n Distribution/Distributorship agreements n n n n n

Intellectual Property Rights n Innovative products/processes n Patents or utility models n Cultural, artistic and literary works n Copyright and related designs n Creative designs n Industrial design rights n Distinctive signs n Trademark, Collective mark n Microchips n Layout-designs n Goods of a given quality due to its geographical origin Confidential business information n Geographical indications n Trade secrets n

7. After an IP audit n Catalog of IP assets q Have rights been acquired, if not should they be (cost benefit analysis), if they have been acquired are they been properly maintained q Ownership issues; does the company own these assets? Are there infringement issues (license/design around)? has title not been properly assigned by employees/consultants q Strategic issues; are these assets being properly managed and exploited within the strategic objectives of the company. Are there restrictions to their use

Strategic issues n n After an IP audit, the management matches its newly established inventory of IP assets to its strategic business objectives. A possible technique is to divide: n n n Techniques, innovations, and ideas that are essential to your products and services, and to the markets your company has decided to serve Intellectual assets of real potential but not to your company Assets’ that seem, on balance, to have no great value to your company or to anyone else

Business strategy formulation n n How would the assets that have been identified as essential to the business of the company be better utilized in marketing its goods and services in the relevant markets How would the assets with potential be used What would one do with the other `assets’ The results of the IP audit may add a new dimension to its strategy discussions and may lead to new business strategies

From IP audit to IP asset management n The audit team could evolve into a permanent IP asset management team overseen by a senior executive and charged with managing the knowledge portfolio. The team could be composed of managers from various disciplines who understand the firm’s intellectual assets.

Create an IP culture – Respect for IP. Training on IP best practices for all staff. Training programs to include content on IP asset management. n Review the existence and adequacy of IP asset management policies, procedures and practices within a company and verify that they are effectively communicated to all the employees. n

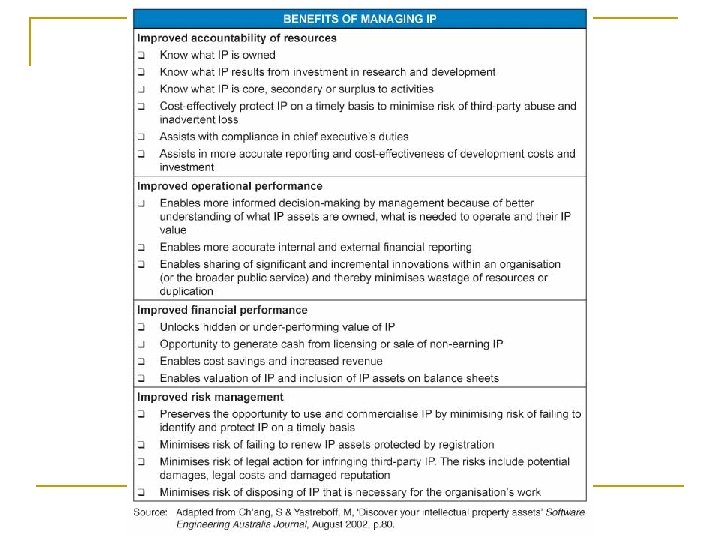

Building value through IP management n IP asset creation. n Reducing costs of third-party IP claims. n Building value from product markets using IP assets. n Creating non-core revenue streams. n Creating additional revenue through core business licensing. n Reducing costs of unused IP assets. n Receiving tax deductions for IP asset donations.

n Reducing new product development costs n Evaluating the IP assets of an acquisition or investment target (due diligence). n Assessing business direction and strength. n Discovering unclaimed business opportunities. n Discovering business expansion opportunities

Consequences of not managing IP assets n n n Failing to protect assets Infringing others assets duplication of efforts to redevelop existing needs loss of potential benefits (revenue, reputation, industry development) from failing to commercialize low moral and stifle innovation

59f6547d19f6de24769773a5d3835a08.ppt