8b4b0fbcf22d3bd4501df5653943cc58.ppt

- Количество слайдов: 119

Welcome to the 2015 Healthcare Seminar! Hosted by:

THE SHIFTING REIMBURSEMENT LANDSCAPE Karen Meador, MD, MBA Managing Director BDO Center for Health Care Excellence and Innovation 214 -259 -1477 kmeador@bdo. com May 1, 2015 Healthcare Symposium: Preparing for the Future of Healthcare San Antonio, TX

3 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION OVERVIEW OF PRESENTATION Ø The Underlying Factors: Cost and Quality Ø The Early Evidence of the Shift to Value-Based Payments Ø Preparation and Risk Reduction

THE UNDERLYING FACTORS: COST AND QUALITY

5 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION U. S. HEALTHCARE EXPENDITURES $2. 9 Trillion in 2013 ($9, 225 person) 17. 4% of GDP since 2009 Spending projected to increase at 5. 7% per year (1. 1% faster than GDP growth) through 2023. In 2023, spending is likely to reach $5. 2 Trillion (19. 3% GDP). www. cms. gov

6 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION DISTRIBUTION OF HEALTHCARE EXPENDITURES ~5% of population responsible for 50% of spending ~50% of population accounts for just 3% of spending Agency for Healthcare Research and Quality analysis of 2009 Medical Expenditure Panel Survey

7 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION PAYERS OF HEALTHCARE EXPENDITURES 2013 (in billions) $312 11% $586 20% $106 4% $339 12% $449 15% $962 33% www. cms. gov and Hartman M et al. National Health Spending in 2013. Health Affairs. 34 No. 1 (2015)

8 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION RECIPIENTS OF HEALTHCARE EXPENDITURES 2013 (in billions) Hospital Physician Other Professional Services Dental $936. 9 (32%) $271. 1 (9%) Health, Residential, Personal care Home Health Nursing & CCRC Prescription DME $586. 7 (20%) OTC Government Admin Government Public Health Net Cost Health Insurance Investment www. cms. gov and Hartman M et al. National Health Spending in 2013. Health Affairs. 34 No. 1 (2015)

9 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION DISTRIBUTION OF PREMIUMS 2014 Relative to average premium rates for employer-provided health benefits 20% 16% 15% $16, 834 <$13, 46 20% >$20, 20 7 20% 13% 1 16% 17% 16% $6, 025 11% 20% >$7, 230 Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 2004 -2014

10 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION SHARE OF HEALTHCARE PREMIUMS By Employer and Employee for Family Plan, 2004 v 2014 $16, 834 $12, 011 $9, 950 $7, 289 $4, 823 $2, 661 81% increase Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 2004 -2014

11 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION U. S. HEALTHCARE QUALITY In 1999, The Institute of Medicine reported that as many 98, 000 people per year die in hospitals from preventable errors. In 2013, Patient Safety America (in Houston) estimated that as many as 440, 000 preventable adverse events occur annually in hospitals. To err is human. Institute of Medicine. November 1999. James J. A new evidence-based estimate…Journal of Patient Safety: September 2013. 9(3).

12 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION U. S. HEALTHCARE QUALITY Commonwealth Fund Surveys and Analyses indicate US is 11 th out of 11 Mahon M. Us health system ranks last. . . The Commonwealth Fund. June 16 2014

13 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION U. S. HEALTHCARE QUALITY These negative rankings have been challenged. American Enterprise Institute: Remove fatal injuries and US ranking goes to first. CONCORD Cancer Survival in Five Continents: US first for breast, prostate, and colon cancers. Researchers at U Penn: Low life expectancy in US not likely due to health care system. Perception remains that quality is too low and cost is too high. The myth of Americans’ poor life expectancy. Forbes. Nov 2011. Coleman MP et al. CONCORD… Lancet. Aug 2008 Ohsfeldt R and Schneider J. The business of health… American Enterprise institute. 2006. Preston S and Ho J. Low life expectancy in the US… PSC Working Papers. July 2009.

14 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION U. S. HEALTHCARE IS UNDERGOING A PARADIGM SHIFT KEY HEALTH CARE MARKET TRENDS Rising Costs and Suboptimal Quality Regulatory Reform Aging Population & Chronic Disease Burden Reduced Number of Hospitals DATA & TECHNOLOGY ü Value-based reimbursement to providers ü Emphasis on chronic care management ü Shift to lower-cost care settings ü Increased M&A among providers and payers www. cms. gov and Hartman M et al. National Health Spending in 2013. Health Affairs. 34 No. 1 (2015)

THE EARLY EVIDENCE OF THE SHIFT TO VALUE

16 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION HOSPITAL INPATIENT QUALITY REPORTING (HOSPITAL IQR) Mandated by section 501 b of the Medicare Prescription Drug, Improvement, and Modernization Act (MMA) of 2003 Initially, the MMA reduced by 0. 4% the annual market basket update for hospitals that failed to report metrics. Deficit Reduction Act of 2005 increased the penalty to 2%. The quality of care data is available to consumers at www. hospitalcompare. hhs. gov www. cms. gov

")

17 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION HOSPITAL OUTPATIENT QUALITY REPORTING (OQR) PROGRAM Mandated by the Tax Relief and Health Care Act of 2006 Hospitals are subject to a 2 percentage point reduction in the annual payment update (APU) under the Outpatient Prospective Payment System (OPPS) if reporting requirements are not met. Approximately 30 quality metrics covering: www. cms. gov Process of care Imaging efficiency patterns Care transitions ED throughput efficiency Use of Health Information Technology (HIT) care coordination Patient safety and volume

")

18 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION PHYSICIAN QUALITY REPORTING SYSTEM (PQRS) Began in 2007 as PQRI with incentives that continued through 2014 to encourage quality metric reporting regarding Medicare FFS part B services. Now penalties of 1. 5% in 2015 if metrics were not reported in 2013; going to 2% in 2016 if not reported in 2014. 51% participation in 2015 with 470, 000 physicians receiving 1. 5% penalty. www. cms. go v

19 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION MEDICARE AND MEDICAID EHR INCENTIVE PROGRAM Began in 2011 with incentive payments up to $43, 720 for Medicare and $63, 750 for Medicaid Stage 1: data capture and sharing Stage 2: advanced clinical processes Stage 3 coming 2017: improved outcomes; reduced complexity Proposed rule released in March 2015 https: //www. federalregister. gov/articles/2015/03/30 /2015 -06685/medicare-and-medicaid-programselectronic-health-record-incentive-program-stage-3#h -14 www. cms. gov

20 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION READMISSION REDUCTION PROGRAM Established by Section 3025 of the ACA Began with discharges in October 2012 Hospitals penalized with reduced payments for all DRGs if 30 day readmissions exceed risk-adjusted anticipated levels for Initially acute MI, heart failure, and pneumonia. In 2015, COPD and THA/TKA. Penalty has increased from 1% in 2013 to 3% in 2015. www. cms. gov

")

21 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION HOSPITAL VALUE BASED PURCHASING (VBP) www. cms. gov Authorized by section 3001(a) of the ACA Uses data from Hospital Inpatient Quality Reporting Program. Began in 2013 with 12 clinical process measures and 8 patient experience measures from HCAPS In 2014, 30 day outcome mortality measures added (AMI, HF, PN) For 2015, PSI-90, CLABSI, MSBP For 2016, CAUTI and surgical site infection

")

22 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION HOSPITAL VALUE BASED PURCHASING (VBP) Shifting emphasis from process measures to outcomes 2015 Clinical Process of Care Patient Experience of Care Efficiency Outcomes www. cms. gov 2016 2017 20% 30% 10% 25% 40% 5% 25% 45%

")

23 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION HOSPITAL VALUE BASED PURCHASING (VBP) Increasing redistribution of payments from lowest performers to highest performers Fiscal Year 2013 2014 2015 2016 2017 www. cms. gov Percent Reduction 1 1. 25 1. 75 2

")

24 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION HOSPITAL VALUE BASED PURCHASING (VBP) 2015 Payment Adjustment factors https: //www. cms. gov/Medicare/Quality-Initiatives-Patient-Assessment-Instruments/hospital-value-based-purchasing/index. html? redirect=/hospital-value-based-purchasing/ www. cms. gov 3089 hospitals 1375 receive penalties up to -1. 24% 1714 receive bonus up to 2. 09%

25 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION CENTER FOR MEDICARE AND MEDICAID INNOVATION (CMMI) Established by section 3021 of the ACA Purpose: Testing new payment and service delivery models Evaluating results and advancing best practices Engaging a broad range of stakeholders to develop additional models for testing Innovation Models: ACOs including Pioneer and Advanced Payment ACOs Bundled Payments Primary care transformation Medicaid and CHIP initiatives Dual-eligible initiatives Speeding adoption of best practices New payment methodologies www. cms. gov

26 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION CENTER FOR MEDICARE AND MEDICAID INNOVATION (CMMI) 15 innovation models being run by state of TX 659 facility level innovation models http: //innovation. cms. gov/initiatives/map/index. html#model=

")

27 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION MEDICARE SHARED SAVINGS PROGRAM (MSSP) AND PIONEER ACCOUNTABLE CARE ORGANIZATIONS Established by section 3022 of the ACA; began in 2012 Participation through Accountable Care Organizations (ACO) Providers coming together to serve fee-for-service Medicare MSSP shared savings/losses % share Cap Participants beneficiaries track 1 year 1 -2 year 3 track 2 all 3 years shared savings only savings and losses 52. 50% 60% 7. 5% 10% 401 3 Pioneer ACO 32 → 19 year 1 savings and losses 60% 10% Seton Health Alliance and Plus (THR and Texas Specialty year 2 savings and losses 70% 15% Physicians) were Pioneer ACOs in TX but have dropped out year 3 savings and losses up to 100% • Seton has gone on to form an ACO with private 15% payers www. cms. gov

28 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION MEDICARE SHARED SAVINGS PROGRAM: RESULTS 7. 3 M beneficiaries as of January 2015 Year 1 58 of the 243 initial MSSP’s earned a bonus ($705 M in savings leading to $315 M in bonuses). One shared in losses ($10 M loss with $4 M penalty). 30 of 33 quality measures improved. www. cms. gov

29 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION PIONEER ACO RESULTS 620, 000 beneficiaries as of January 2015 Year 1 Saved Medicare $117 per participating beneficiary per year and a total of $118 million the first year. And savings was similar between ACOs that have dropped out versus those that have remained. Year 2 Saved Medicare $96 M and 11 earned bonuses totaling $68 M. 3 generated losses. 28 of 33 quality measures improved. Mc. Williams JM et al. Performance differences in year 1 of pioneer ACOs. JAMA. April 15, 2015 www. cms. gov

Mandated")

30 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION VALUE PAYMENT MODIFIER (VPM) Mandated by section 3007 of ACA Adjusts payments based on quality and cost metrics 2015: Physicians in groups of 100 or more Eligible Professionals (EPs) based on 2013 performance. 2016: Physicians in groups of 10 or more EPs based on 2014 performance. 2017: all Physicians including those participating in Shared Savings, ACOs, and Comprehensive Primary Care Initiative. 2018: extended to non-physician EPs. www. cms. gov

Performance")

31 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION VALUE PAYMENT MODIFIER (VPM) Performance Metrics in 2013 impacting payment in 2015: 14 Process measures; examples: Follow-up after hospitalization for mental illness Spirometry testing to confirm COPD Lipid profile within 3 months of starting lipid lowering med 3 Outcome measures: Composite of acute prevention: PN, UTI, dehydration Composite of chronic prevention: DM, COPD, HF All cause readmission Cost Total per capita cost Per capita cost for each of COPD, HF, CAD, and DM www. cms. gov

VPM")

32 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION VALUE PAYMENT MODIFIER (VPM) VPM adjustment for 2015 Physician groups could have elected Quality Tiering by Oct 15, 2013. 127 groups elected tiering. No groups earned the 2 x% upward adjustment based on high quality and low cost. 14 groups get an upward adjustment of 1 x%. 11 groups get downward adjustment of -0. 5 -1%. For those who did not report got an automatic 1% penalty. The x “adjustment factor” above is based on the available funds from the groups that had a downward adjustment. www. cms. gov

VPM")

33 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION VALUE PAYMENT MODIFIER (VPM) VPM adjustment for 2015 For 2015 the adjustment factor is 4. 89 increasing payments by 4. 89% to the 14 groups that earned 1 x%. CMS: “We also anticipate that we would propose to increase the amount of payment at risk for the Value Modifier as we gain additional experience with the methodologies used to assess the quality of care, and the cost of care, furnished by physicians and groups of physicians. ” www. cms. gov.

VPM")

34 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION VALUE PAYMENT MODIFIER (VPM) VPM adjustment for 2016 In 2016 (based on 2014) data the downward adjustment goes to 2%. It’s too late to change your payment status for 2016. In 2017, all physicians impacted and quality tiering becomes mandatory! www. cms. gov.

Coming")

35 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION VALUE PAYMENT MODIFIER (VPM) Coming in 2017 To avoid the downward adjustment of 2% in 2017 (for groups up to 9) or 4% for groups of 10 or more: Option 1 Participate in Group Practice Reporting Option (GPRO): Qualified PQRS registry HER Web interface for those with 25+ EPs Consumer Assessment of Health Providers and Systems (CAHPS) for PQRS survey (mandatory for groups with 100+ EPs) **Must register on cms. gov between April 1 and June 30, 2015. www. cms. gov

Coming")

36 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION VALUE PAYMENT MODIFIER (VPM) Coming in 2017 (cont’d) To avoid the downward adjustment of 2% in 2017 (for groups up to 9) or 4% for groups of 10 or more: Option 2 At least 50% of group participates in PQRS as individuals Medicare Part B Claims Qualified PQRS registry EHR Qualified Clinical Data Registry www. cms. gov

37 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION PENALTIES FOR HOSPITAL ACQUIRED INFECTIONS (HAI) Introduced by Section 3008 of the ACA 35% of score is composite safety measure with 8 indicators from AHRQ. 65% of score from 2 HAI measures from data reported to the National Healthcare Safety Network and the CDC’s online infection reporting system. Beginning in 2015, 1% of payments subtracted from hospitals with the highest quartile rates of HAIs. 724 hospitals penalized in 2015. Mc. Kinney M. Hospital-acquired conditions mean Medicare penalties…Modern Healthcare. Dec 18, 2014. www. cms. gov

38 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION MEDICARE SHIFTING TO A FOCUS ON VALUE Goal to have 50% of all Medicare payments and 90% of fee-for-service Medicare tied to value by 2018 Develop and test new payment models. Encourage greater integration, coordination among providers, and attention to population health. Accelerate availability of EHR information and interoperability. ACA established Patient-Centered Outcomes Research Institute with goals of research findings being disseminated in part through EHRs. Medicare website allows consumers to compare data on costs and quality. Burwell S. Setting value-based payment goals… NEJM. January 26, 2015. Japsen B. White House plans to shift Medicare… Forbes. January 26, 2015.

39 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION MEDICARE SHIFTING TO A FOCUS ON VALUE The Sustainable Growth Rate (SGR) “Doc-fix” includes greater emphasis on payment for value Merit-based payment incentive system (MIPS) coming in 2020 Will consolidate current incentive programs including PQRS 4 categories of metrics: Resource use / efficiency EHR use Quality Clinical improvement activities Up to 9% of pay will be at risk Wynne B. Health Affairs Blog. April 14, 2015

40 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION MEDICARE SHIFTING TO A FOCUS ON VALUE Fiscal year 2016 IPPS Proposed Rule Hospitals that are meaningful users of EHRs and report quality through IQR data get a 1. 1% increase in their operating rates 2. 7% market basket update -0. 8% multi-factor productivity and ACA adjustment -0. 8% recoupment by American Taxpayer Relief Act of 2012 1. 1% Others will experience a decline in rates -(0. 5 x 2. 7%) if not meaningful use compliant -(0. 25 x 2. 7%) if not participating in IQR Overall, a 0. 3% increase in IPPS payments is expected. www. cms. gov

41 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION COMMERCIAL PAYERS ALSO SHIFTING TO VALUE United Health Initiated value-based contracting in 2012. Claims it has saved 1 -6% by value based initiatives. Plans to increase valued based payments to doctors and hospitals by 20% in 2015 to $43 Billion and to $65 B by 2018. Aetna Claims 8 -15% savings first year in transition to ACO model and $1, 600 per member over 3 years. Predicts increased value-based spend to triple from 2013 -2017. Humana Claims full accountability (per member per month payment) reduces Medicare costs by 22% compared with no$43 B exit… Forbes. Jan 23, 2015. provider Japsen B. United. Health’s Funk M. Humana’s approach to value-based reimbursement. Jan 24, 2014. incentives. 2013 Aetna Investor Conference. Dec 12, 2013.

PREPARATION AND RISK REDUCTION

43 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION RECOGNIZE THAT FEE-FOR-SERVICE IS DIMINISHING BOTH THROUGH CMS AND COMMERCIAL PAYERS While it might have previously seemed financially favorable for small practices to accept the reimbursement cuts rather than make substantial capital investments to upgrade EMR and reporting systems, the penalties will soon be too great for this to continue to work.

44 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION RECOGNIZE THAT FEE-FOR-SERVICE IS DIMINISHING BOTH THROUGH CMS AND COMMERCIAL PAYERS If you are going to participate with third party payers, you are going to have to participate in value-based payment systems.

45 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION EVALUATE YOUR OPTIONS Identify programs that are mandatory or that result in penalties for non-participation. Identify optional programs for which the organization or provider may qualify. Compare the costs of compliance and potential risks with the revenue lost by not participating. Develop a plan for maximizing revenue and margins in the current and projected regulatory and payer environment. If fully prepared for risk, a health system may benefit from launching its own Medicare Advantage plan.

46 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION UNDERSTAND YOUR COSTS OF CARE Map out the costs of each component of an episode of care Identify the average costs per patient in various categories This information will be particularly beneficial in: Identifying opportunities for savings Negotiating bundled payment scenarios Medicare Share Savings Plan and ACOs Launching a Medicare Advantage plan

47 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION MAKE SURE YOUR PHYSICIANS AND STAFF ARE INFORMED AND PREPARED Engage physicians, other clinicians, and staff throughout the process, beginning before the hospital or physician group makes changes to processes and compensation.

48 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION PROVIDE APPROPRIATE INCENTIVES FOR PHYSICIANS AND STAFF Develop compensation systems that link income to individual and team performance on the same quality metrics used by the payers. Ensure that physicians and staff understand the metrics on which they are evaluated and that they have guidance on how to improve those metrics and their income.

49 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION DEVELOP OR IMPROVE QUALITY DATA CAPTURE AND REPORTING Consider having an internal audit done to assess the completeness and accuracy of your reporting and the opportunities for improvement in metrics.

50 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION DEVELOP EFFICIENCIES AND LOWER COST CARE SETTINGS From hospitals to clinics and community settings Emphasis on reducing ER use, unnecessary hospitalizations, and readmissions. Payments increasingly less about location and more about the outcomes.

51 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION PROVIDE CARE MANAGEMENT FOR PATIENTS WITH CHRONIC DISEASE Has been shown to have an ROI as high as 3. 8* Patients with 2 or more chronic conditions are eligible for Medicare Chronic Care Management Services Must provide access to care management 24/7 and meet several criteria including minimum of 20 minutes per month of clinical time Payment to physician of about $40/per patient per month Subject to patient deductible and coinsurance * Mattke S et al. Do workplace wellness programs save employers money? RAND Research Brief; 2014.

SUMMARY

53 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION SUMMARY U. S. healthcare expenditures at $2. 9 Trillion and expected to grow at 5. 7% per year, exceeding GDP by 1. 1%. Perception that quality is deficient relative to costs. CMS and commercial payers are shifting from fee-for-service to payment models based on quality, efficiency, & outcome metrics. Providers that prepare for the new payment models with a focus on improving quality, containing costs, and having reporting mechanisms that clearly document quality processes and outcomes may actually experience revenue growth.

54 BDO | CENTER FOR HEALTHCARE EXCELLENCE & INNOVATION SUMMARY Providers that fail to prepare and do not meet or report metrics may be unsustainable. Achieving efficiencies in care and compliance with reporting requirements may be easier for larger systems so that M&A activity is likely to increase.

BDO IS THE BRAND NAME FOR BDO USA, LLP, A U. S. PROFESSIONAL SERVICES FIRM PROVIDING ASSURANCE, TAX, FINANCIAL ADVISORY AND CONSULTING SERVICES TO A WIDE RANGE OF PUBLICLY TRADED AND PRIVATELY HELD COMPANIES. FOR MORE THAN 100 YEARS, BDO HAS PROVIDED QUALITY SERVICE THROUGH THE ACTIVE INVOLVEMENT OF EXPERIENCED AND COMMITTED PROFESSIONALS. THE FIRM SERVES CLIENTS THROUGH 58 OFFICES AND MORE THAN 400 INDEPENDENT ALLIANCE FIRM LOCATIONS NATIONWIDE. AS AN INDEPENDENT MEMBER FIRM OF BDO INTERNATIONAL LIMITED, BDO SERVES MULTINATIONAL CLIENTS THROUGH A GLOBAL NETWORK OF 1, 328 OFFICES IN 152 COUNTRIES. BDO USA, LLP, A DELAWARE LIMITED LIABILITY PARTNERSHIP, IS THE U. S. MEMBER OF BDO INTERNATIONAL LIMITED, A UK COMPANY LIMITED BY GUARANTEE, AND FORMS PART OF THE INTERNATIONAL BDO NETWORK OF INDEPENDENT MEMBER FIRMS. BDO IS THE BRAND NAME FOR THE BDO NETWORK AND FOR EACH OF THE BDO MEMBER FIRMS. WWW. BDO. COM

ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Venson Wallin, Jr. CPA Managing Director, BDO USA, LLP 804 -614 -1188 vwallin@bdo. com BDO USA, LLP, a Delaware limited liability partnership, is the U. S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international BDO network of independent member firms. BDO is the brand name for the BDO network and for each of the BDO Member Firms.

What is ICD-10? Diagnostic coding system implemented by the World Health Organization in 1993 Broken down into clinical modification (CM) set and procedural coding system (PCS) Currently scheduled to be adopted on October 1, 2015 ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 57

How does ICD-10 compare to ICD-9? More granularity in ICD-10, which provides for more clarity in documenting diagnoses and treatments of patients Significant increase in coding ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 58

Activity, milking an animal • Y 93. K 2 ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 59

ICD-10 Delay Timeline CMS Announcement August 24, 2012 October 1, 2013 October 1, 2014 October 1, 2015 Congress’ SGR patch March 31, 2014 ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 60

conducts periodic ICD-10")

How Prepared is the Industry? Workgroup for Electronic Data Interchange (WEDI) conducts periodic ICD-10 readiness surveys and reports results back to HHS in its advisory role under HIPAA Latest results are from survey conducted in August, 2014, and released in September, 2014 ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 61

The WEDI results of the August, 2014 readiness")

How Prepared is the Industry? (continued) The WEDI results of the August, 2014 readiness survey indicate the following (keeping in mind that the deadline was October 1, 2015 at the time of the survey): • Less than 10% of vendors were halfway or less complete with product development, 33% were three-quarters complete, and 40% were fully complete • 67% of vendors indicated their product is already available, but 25%+ indicated their product would not be available until 2015 or responded “unknown” • 25% of health plans less than complete with their impact assessment • 25% of health plans had not started internal testing • 25%+ of health plans did not expect to start external testing until 2015 • Only 50% of providers had completed their impact assessment • 67% of providers had not started external testing ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 62

What about ICD-11? Not as significant a jump from ICD-10 to ICD-11 as from ICD-9 to ICD-10 Scheduled for release in 2017 (after delay from 2015), but not fully implemented until 2020 or after • Use by U. S. for reimbursement purposes requires modifications ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 63

Activity, walking an animal • Y 93. K 1 ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 64

CODER STAFFING ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 65

Supply and Demand Playing a Significant Role 0 CD-1 ualified I or q Demand f coders Today October 1, 2014 Supply (avail ability) of qu alified ICD-10 coders ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 66 October 1, 2015

How are Health Systems Identifying Qualified ICD 10 Coders? Hiring directly Subcontracting with a national agency Subcontracting with an off-shore agency Sending candidates to community colleges for training ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 67

Emerging Issue: Availability of ICD-9 Coders With initial go-live date of October 1, 2013, and then delayed date of October 1, 2014, focus had been on getting everyone trained in ICD-10 With the go-live date pushed out until October 1, 2015, there is a knowledge gap emerging as ICD-9 coders leave the health system and new coders are not trained in ICD-9 In 2014, AHIMA estimated over 25, 000 students in associate and baccalaureate health information management programs were in limbo as they had trained exclusively in ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 68

What Areas Should Coders Focus On? Ensuring education is sufficient to code effectively – knowledge of anatomy and physiology Continue to practice ICD-10 coding – use it or lose it Increase engagement with physicians to strengthen relationships which will facilitate coding transition Analyze health system data to identify high-risk areas for documentation and coding inaccuracies ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 69

Activity, piano playing • Y 93. J 1 Activity, drum and other percussion instrument playing • Y 93. J 2 Activity, string instrument playing • Y 93, J 3 Activity, winds and brass instrument playing • Y 93. J 4 ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 70

CDI ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 71

How much can a CDI program really help you prepare for ICD-10? • Assisting (v. training) with Physician Adoption – reducing the noise associated with physician documentation training – Clinical Documentation Specialist or Clinical Documentation “Compliance” Specialist – query forms • Clinician and Coder Cooperation To Flatten Learning Curve – DRG/query reconciliation ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 72

Activity, computer keyboarding • Y 93. C 1 ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 73

TESTING ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 74

Testing requires a multi-stage approach throughout the implementation Unit testing • Testing of code to check design of the unit within the program Integration testing • Testing of integration and interfaces of program components within the overall program System testing • Testing to confirm program has met business requirements documentation and that it works with other related hardware/software User acceptance testing • Testing to enable real world users to check that the program fulfills their needs End-to-end testing • Testing that mimics a real world application, including interacting with databases, network communications, and other hardware/software – Does this operationally work the way it should on a day-to-day basis? ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 75

Who, What and Whens of Testing Who do you test with? • Yourself • Vendors • Payers/Providers • Clearinghouses What do you test? • Entire revenue cycle (registration to claims flow) • Unique hospital-specific services • Mapping software • Claims submission (with those payers/clearinghouses ICD-10 ready and those who will not be) • Management reports When do you test? • ASAP! ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 76

What are the Challenges of Testing? Scheduling • Competing internal priorities • Readiness of testing partners • Competing interests/parties at testing partners Dedicated testing environments Test data • Create your own test cases • Utilize vendor who utilizes your own claims data to create test population ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 77

Struck by basketball, initial encounter • W 21. 05 XA ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 78

DELAY-GENERATED ADDITIONAL IMPLEMENTATION EXPENSES ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 79

Additional Implementation Costs From the Delay May Be Quite Significant CMS estimated that the delay could cost an additional $1 to $6 Billion Examples of additional costs include the following: • Dual coding – decision as to either maintain dual coding for another year or stop and restart at a later date • Updates to training as new skills will not be applied for an extended period of time • IT costs associated with maintaining legacy systems that were scheduled to be updated/replaced – new software versions/patches ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 80

• Extension of")

Additional Implementation Costs From the Delay May Be Quite Significant (continued) • Extension of contract employees hired specifically for the implementation/transition period • Renegotiation/modification of payer/provider contracts that incorporated ICD-10 language beginning in 2014 • Loss of momentum and diversion of resources to other projects ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 81

Activity, bungee jumping • Y 93. 34 ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 82

SUMMARY ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 83

Six Months Out – What Do You Do? • Challenge adequacy and knowledge level of internal ICD-10 certified coders • Challenge adequacy and knowledge level of internal ICD-9 certified coders • Identify source of additional coders as needed • Conduct coding exercises for coders to maintain training • Determine status of dual-coding program and plan on how to proceed over the coming year ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 84

• Challenge effectiveness of Clinical")

Six Months Out – What Do You Do? (continued) • Challenge effectiveness of Clinical Documentation Improvement program • Conduct exercises for physicians to maintain any ICD-10 training already provided, or provide initial training • Develop Clinical Documentation Improvement strategies for taking advantage of ICD-10, such as enhanced clinical transparency ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 85

• Prepare/update the full internal")

Six Months Out – What Do You Do? (continued) • Prepare/update the full internal and external ICD-10 testing timeline • Stratify your testing partners so that high volume, high dollar partners critical to your operations are focused on initially • Decide how test case data will be generated • Conduct regular updates with partners to monitor their progress towards testing • Determine adequacy of hardware for dedicated testing environment ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 86

• Consider need for updates")

Six Months Out – What Do You Do? (continued) • Consider need for updates to training given time delay since last training period • Quantify need and budget for maintaining legacy system updates/patches to bridge the delay gap • Identify need for extension of contract employees dedicated to implementation and corresponding cost • Identify specific ICD-10 language contained in current managed care contracts and the need for amendment/renegotiation ICD-10: The Alarm Clock is Ticking and No Snooze Button in Sight Page 87

2015 Healthcare Seminar

Negotiating Your Managed Care Contract: The Top Ten Mistakes to Avoid Edgar C. Morrison, Jr. Jackson Walker, LLP jmorrison@jw. com 210 -978 -7780

# 1 Mistake: Signing the Contract without Review

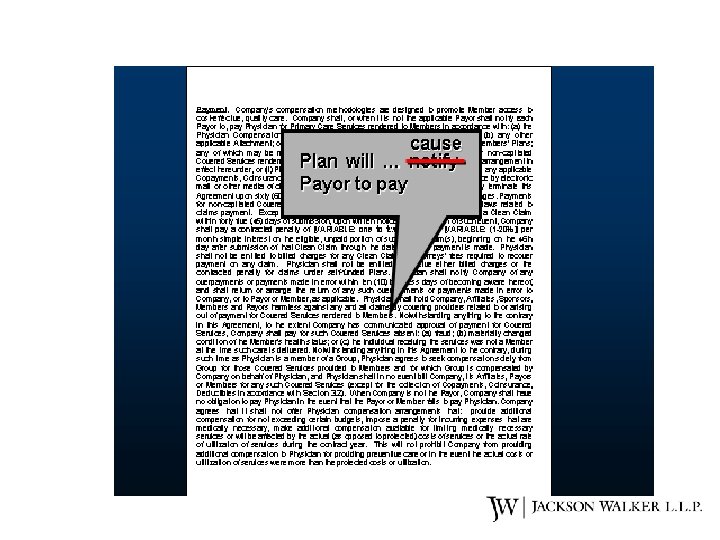

# 2: Payment Clause • “Provider is entitled to receive…” • “Provider will accept payment of claim or penalty…if required by law” • “If Plan is not payor, Plan will notify payor to pay” • “If Plan is not payor, Plan has no obligation to pay” • “Company shall pay, or when it is not the applicable Payor shall cause each Payor to pay, Group for Services rendered to Members in accordance with the fee schedule attached as Exhibit A.

# 3: Fee Schedule “Provider will be paid 115% of the Company San Antonio area usual and customary fee schedule amount” Questions: • Can Fee Exhibit be changed/updated by Payor? • Are fees subject to Administrative Guides, Policies, Procedures, Manuals “as amended from time to time”? • Can Payor change by electronic notice? • Is notice only given for material changes?

When is a Fee Schedule Not a Fee Schedule? • Definition of “fee schedule” is an amount that changes from time to time, e. g. , “ 110% of Company Market Fee Schedule” • Payor won’t tell you about routine fee schedule changes • Change can be posted on the website which constitutes notice from the date of posting

Fee Schedule Tips • Read the Fee Schedule! • Attach specific fee schedule with $$ amounts • Limit Plan’s ability to amend without consent • Avoid “usual and customary” or other vague terms • At least quarterly, compare remittances with fee schedule

Sample Fee Schedule Specialist Physician Group Services and Compensation Schedule CPT Codes Description Fee Schedule 90658 Influenza immunization $5. 17 90703 Tetanus Toxoid $1. 80 90732 Pneumovax $12. 86 90780 IV infusion therapy, 1 hour $40. 93 90781 IV infusion, additional hour $20. 46 90782 Injection (IM, SQ) $4. 10 90784 Injection (IV) $17. 73 93000 Electrocardiogram, complete (EKG) $27. 46 96400 Chemotherapy, (SC)/(IM) $5. 11 96408 Chemotherapy, IV push $35. 47

# 4: Applicability of Texas Prompt Pay Laws • Payment within 30/45 days of receipt of clean claim • From due date to 45 th day pay 50% of difference between contract rate and billed charge • From 45 th -91 st day after due – pay full billed charge • After 91 st day also pay 18% interest • Can recover attorneys’ fees and costs

• “Applies only to fully-insured")

Prompt Pay Amendments (Examples of Language Used by Plans) • “Applies only to fully-insured plans” • “Does not apply to self-funded plans” • “Applies only when Company is the Payor” • Provider wants state law to apply and should not negate application of state law. The clause should say: “Applies to those claims to which the state law applies. ”

Prompt Pay: ERISA v. State Law • ERISA preempts certain state laws • Not intended to override state’s regulation of insurance • Effect on Prompt Pay laws: Texas Courts divided on the issue

U. S.")

Recent Texas Prompt Pay Cases • Blue Cross vs. Methodist Hospitals (2015) U. S. D. C. N. Dist. Tex. —Prompt Pay laws do not apply to insurers acting only as third party administrators • Aetna v. Methodist Hospitals (2015) U. S. D. C. N. Dist. Tex. —ERISA does not preempt Prompt Pay laws against third party administrators

# 5: Amendments to the Contract • Can be made without notice, and no opportunity to object • They automatically become part of the agreement • Or provider has 30 days to object • If you object – you terminate the contract • Many ways for Plan to change contract are not found in the amendment clause

Suggested Amendment Language Amendments This Agreement constitutes the entire understanding of the Parties hereto and no changes, amendments or alterations shall be effective unless signed by both Parties. Notwithstanding the foregoing, at Company’s discretion, Company may amend this Agreement to comply with applicable law or regulation, or any order or directive of any governmental agency, without the consent of Facility.

# 6: Adding New Products Provider will provide Covered services under the following types of Coverage Plans: • Plan HMO • Plan POS • Plan PPO • Plan may add to or delete from this list upon written notice.

Adding New Products “Company reserves the right to introduce new Plans during the course of this Agreement and to designate Group and Participating Group Providers as Participating Providers in such Plans. Group agrees that Participating Group Providers will provide Covered Services to Members of such Plans where so designated under compensation arrangements determined by Company. ”

# 7: Audit and Overpayment • State law: Plan should pay claim timely, has 180 days to complete audit and 30 days to pay additional amounts due. Cannot recoup refund until appeals exhausted. • Overpayment requests must be within 180 days of receipt of claim. Cannot collect for 45 days after notice. • Exceptions for fraud

Audit Tips • Do not allow offset from current payments unless all appeals exhausted • Payor must reimburse provider copying costs for medical records • Company must disclose specific nature and purpose of audit

# 8: Arbitration Clause Common Arbitration Language: • Waives the right to a trial by jury • May waive your right to legal damages • May limit power of arbitrator (what he can consider) • Waives your right to appeal decision • May waive right to have discovery on company

New Plan Arbitration Clauses • • Waives your right to file a class action Waives your ability to consolidate claims Requires you pay arbitration fee (or split) Can't terminate contract without arbitration

Waiver of Damages • “Company’s liability to Provider is limited to the amount paid to Provider in prior 12 months. ” • Company is not liable for several types of damages for any action, inaction, tortious conduct, or delay by Company.

Catch 22: Loss of Right To Arbitrate • Not filing timely notices for review, not exhausting internal remedies that Plan controls • Not seeking first and second level reviews within time periods • Limits on time allowed to initiate arbitration

Arbitration Clause Tips • • • Preserve right to discovery against Plan Preserve right to costs and attorneys’ fees Preserve right to consolidate claims No limitation of damages No limitations on arbitrator’s authority Arbitration not required to terminate contract

# 9: Indemnity Clauses • Shifts legal burden by contract • “Provider is responsible for all care and nothing Plan does affects Provider’s obligation, Provider will indemnify Plan for same. ” • Can require one party to pay other parties’ damages, costs, or legal fees to third party • Malpractice Policies Usually Do Not Cover Contractual Indemnity

Indemnity Clause Tips • Just say NO! • Or limited to fees: amounts paid to provider on behalf of other providers • Or limited to claims “to the extent covered by applicable insurance” • Or exclude claims partly the fault of payor or patient

when given by Plan")

# 10: Verification and Authorization Texas Law • Verification (coverage) when given by Plan cannot be retroactively denied for 30 days • Preauthorization (medical necessity) when given cannot be retroactively denied or reduce payment • Unless misrepresentation or services not provided

Top Ten Mistakes 10. 9. 8. 7. 6. 5. 4. 3. 2. 1. Verification and Authorization Indemnity Clauses Arbitration Clause Audit and Overpayments Adding New Products Amendments Prompt Pay Fee Schedule Payment Clause Signing without Review

Negotiating Your Managed Care Contract: The Top Ten Mistakes to Avoid Edgar C. Morrison, Jr. Jackson Walker, LLP jmorrison@jw. com 210 -978 -7780

2015 Healthcare Seminar

The Urge to Merge: A Panel Discussion of Mergers and Acquisitions in Healthcare Moderator: Jeannie Frazier, CFO Partner, Aventine Hill Partners, Inc. Jeannie. frazier@aventinehillinc. com or at (210) 745 -4200 Panelists: Stephanie Chandler, Partner and Chair – San Antonio Corporate & Securities Practice Group, Jackson Walker, L. L. P. schandler@jw. com or at (210) 978 -7704 Patrick Pilch, MBA, Managing Director, BDO USA, LLP ppilch@bdo. com or at (212) 885 -8006 Clay Jett, Market President, Bank SNB clayjett@banksnb. com or at (210) 271 -8291

Thank you for attending the 2015 Healthcare Seminar! Hosted by:

8b4b0fbcf22d3bd4501df5653943cc58.ppt