Theme 5. Fundamentals of theory of supply and demand

Theme 5. Fundamentals of theory of supply and demand

1. Demand. Factors determining the demand

1. Demand. Factors determining the demand

Demand Expresses the law of demand: the inverse relationship between price and buys many goods, a gradual decrease in demand for a given product or service. The higher price and a clear tendency to its growth, the lower the amount of goods and services will be purchased by consumers. If the price of a good increases, the volume of sales of the product, according to the fall in demand is reduced.

Demand Expresses the law of demand: the inverse relationship between price and buys many goods, a gradual decrease in demand for a given product or service. The higher price and a clear tendency to its growth, the lower the amount of goods and services will be purchased by consumers. If the price of a good increases, the volume of sales of the product, according to the fall in demand is reduced.

Demand curve If the price of a good rises from point B to point A, then the volume sales declines. The direction of the axes schedule changes to the opposite, if the price fall away from point A to point B. demand corresponds to a certain value of two variables prices and sales

Demand curve If the price of a good rises from point B to point A, then the volume sales declines. The direction of the axes schedule changes to the opposite, if the price fall away from point A to point B. demand corresponds to a certain value of two variables prices and sales

Non-price factors: income customers, their subjective tastes, fashion, consumer goods, etc. What then happens to the demand curve? The answer is simple: change non-price factors and demand causes the configuration change, the slope of the demand curve, expressing the change in the quantity of goods sold for the same price is not changing.

Non-price factors: income customers, their subjective tastes, fashion, consumer goods, etc. What then happens to the demand curve? The answer is simple: change non-price factors and demand causes the configuration change, the slope of the demand curve, expressing the change in the quantity of goods sold for the same price is not changing.

In Figure 4. dashed line shows its increase in demand under the influence of non-price factors. Increased demand - shift the entire curve to the right and up, which means an increase in sales of the product for the same, do not change, the price. In Figure 5. shows the decrease in demand: the dotted demand curve shifted to the left and down.

In Figure 4. dashed line shows its increase in demand under the influence of non-price factors. Increased demand - shift the entire curve to the right and up, which means an increase in sales of the product for the same, do not change, the price. In Figure 5. shows the decrease in demand: the dotted demand curve shifted to the left and down.

2. Supply. The law of supply

2. Supply. The law of supply

The supply of goods on the market Prices and sales of goods vary unidirectional: if the price rises, the market will come to sell more goods. And vice versa. The level of prices of products offered depends revenue, profit. Higher than they are, the faster growing market supply of goods, and vice versa. Market supply of goods makes sense only if it is confirmed to meet the price.

The supply of goods on the market Prices and sales of goods vary unidirectional: if the price rises, the market will come to sell more goods. And vice versa. The level of prices of products offered depends revenue, profit. Higher than they are, the faster growing market supply of goods, and vice versa. Market supply of goods makes sense only if it is confirmed to meet the price.

Supply curve Point A in the supply curve shows a higher level of price P 1 and the increased volume of goods Q 1, offered for sale at market. Point B on the curve proposal shows changes: decrease prices to P 2, which corresponding reduction offered for sale goods Q 2.

Supply curve Point A in the supply curve shows a higher level of price P 1 and the increased volume of goods Q 1, offered for sale at market. Point B on the curve proposal shows changes: decrease prices to P 2, which corresponding reduction offered for sale goods Q 2.

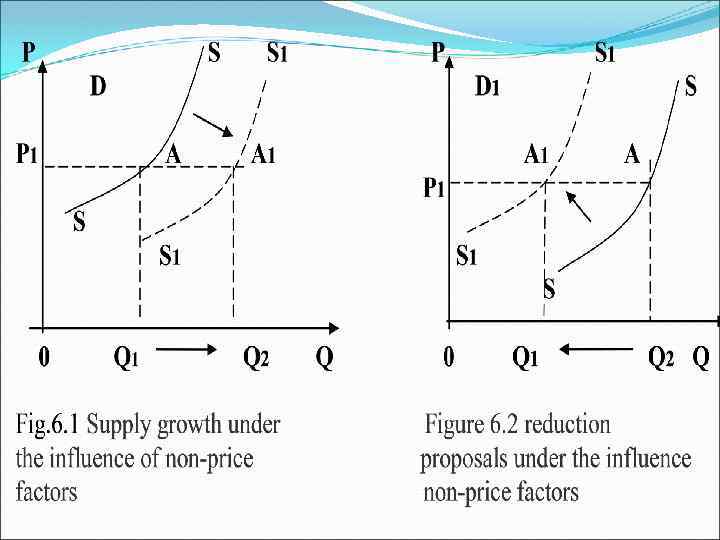

For non-price factors of market supply include: The level Tax policy of of the state technology The prices of resources Subjective The expectations number of of the sellers producers

For non-price factors of market supply include: The level Tax policy of of the state technology The prices of resources Subjective The expectations number of of the sellers producers

3. The interaction of supply and demand. Market equilibrium

3. The interaction of supply and demand. Market equilibrium

Equilibrium market price - the price at which this product for each market there is no surplus or deficit. It is installed as a result of the equilibrium of supply and demand as the cash equivalent of a fixed amount of goods. Supply and demand are balanced under the influence of the competitive environment of the market, so that the price is referred to as the competitive market equilibrium.

Equilibrium market price - the price at which this product for each market there is no surplus or deficit. It is installed as a result of the equilibrium of supply and demand as the cash equivalent of a fixed amount of goods. Supply and demand are balanced under the influence of the competitive environment of the market, so that the price is referred to as the competitive market equilibrium.

is the price, balancing supply and") Market equilibrium The intersection of demand supply (E) is the price, balancing supply and demand. Characterizes the equilibrium price point that there is supply and demand, as opposed market forces are balanced. The equilibrium price means that goods produced as long as required to customers.

Market equilibrium The intersection of demand supply (E) is the price, balancing supply and demand. Characterizes the equilibrium price point that there is supply and demand, as opposed market forces are balanced. The equilibrium price means that goods produced as long as required to customers.

3. Elasticity and its types

3. Elasticity and its types

The term "elasticity" is used to measure the relations of mutually variable price and quantity, or volume, sales of goods.

The term "elasticity" is used to measure the relations of mutually variable price and quantity, or volume, sales of goods.

Different price elasticity of demand • demand is elastic, when a slight increase in sales price increases • the demand has unit elasticity, when 1% change price is 1% change of sales of goods • demand is inelastic, if very substantial reduction of price sales varies slightly • demand is infinitely elastic, when you change only one price at which consumers buy goods • demand is perfectly inelastic, when consumers purchase a fixed number of goods, regardless of its price

Different price elasticity of demand • demand is elastic, when a slight increase in sales price increases • the demand has unit elasticity, when 1% change price is 1% change of sales of goods • demand is inelastic, if very substantial reduction of price sales varies slightly • demand is infinitely elastic, when you change only one price at which consumers buy goods • demand is perfectly inelastic, when consumers purchase a fixed number of goods, regardless of its price

Each option presented in Figure 8 has a coefficient of elasticity: ratio is less than one inelastic demand the elasticity of demand when the 1% decrease in price causes an increase in sales of more than 1%, the coefficient of elasticity is greater than one the unit elasticity coefficient is a unit elasticity of supply

Each option presented in Figure 8 has a coefficient of elasticity: ratio is less than one inelastic demand the elasticity of demand when the 1% decrease in price causes an increase in sales of more than 1%, the coefficient of elasticity is greater than one the unit elasticity coefficient is a unit elasticity of supply

Elasticity of demand

Elasticity of demand

Elasticity of supply

Elasticity of supply

4. The theory of consumer behavior

4. The theory of consumer behavior

Consumer behavior - the formation of consumers' demand for various goods and services, which determines the development of production and supply in the market. Consumer behavior is due to income people who distribute them according to your view of the possible usefulness and profitability, purchased goods.

Consumer behavior - the formation of consumers' demand for various goods and services, which determines the development of production and supply in the market. Consumer behavior is due to income people who distribute them according to your view of the possible usefulness and profitability, purchased goods.

In the modern theory of consumer choice assumes that The cash income of the consumer is limited The prices do not depend on the amount of goods purchased by individual households All buyers are perfectly marginal utility of products consumers seek to maximize the overall utility

In the modern theory of consumer choice assumes that The cash income of the consumer is limited The prices do not depend on the amount of goods purchased by individual households All buyers are perfectly marginal utility of products consumers seek to maximize the overall utility

Consumer choice is based on the following assumptions • Multiple types of consumption • unsaturation • transitivity • substitution • diminishing marginal utility

Consumer choice is based on the following assumptions • Multiple types of consumption • unsaturation • transitivity • substitution • diminishing marginal utility