Lecture_7_The_U_S_Financial_Crisis.ppt

- Количество слайдов: 31

The U. S. Financial Crisis Causes and Responses

The U. S. Financial Crisis Causes and Responses

The Crisis 2008 • March 24 - Bear Stern Take Over - Founded in 1923, 15, 000 employees - purchased by J. P. Morgan for $2/share, one year earlier Bear Stern had been $133/share. • July 11 - Indy Mac Bank Fails - Take over by Federal Government cost $4 billion • September 15 - Lehman Brothers Bankruptcy - Founded in 1850, 26, 000 employees - Survived Great Depression, Occupied three floors of World Trade Center • September 15 – Merrill Lynch Take Over - Founded in 1914, 60, 000 employees - Bank of America pressured by Federal Bank Regulators into purchasing

The Crisis 2008 • March 24 - Bear Stern Take Over - Founded in 1923, 15, 000 employees - purchased by J. P. Morgan for $2/share, one year earlier Bear Stern had been $133/share. • July 11 - Indy Mac Bank Fails - Take over by Federal Government cost $4 billion • September 15 - Lehman Brothers Bankruptcy - Founded in 1850, 26, 000 employees - Survived Great Depression, Occupied three floors of World Trade Center • September 15 – Merrill Lynch Take Over - Founded in 1914, 60, 000 employees - Bank of America pressured by Federal Bank Regulators into purchasing

The Crisis 2008 • September 16 – AIG Bailout - Founded 1949, over 100, 000 employees and $113 billion in sales. - Central Bank Loans $85 Billion to keep AIG solvent • September 25 – Washing Mutual Bank Fails - $300 billion in assets, 43, 000 employees - Take over buy federal government and sold • October 12 – Wachovia Bank take over - Over 100, 000 employees, $800 billion in assets - Reported a $9 billion loss in 2 nd quarter 2008 - Government forces sale to Wells Fargo Bank • December 29 – General Motors Acceptance Corp. Bailout - Founded in 1920, almost 20, 000 employees - U. S. Treasury Injects $5 Billion Dollars, eventually even more.

The Crisis 2008 • September 16 – AIG Bailout - Founded 1949, over 100, 000 employees and $113 billion in sales. - Central Bank Loans $85 Billion to keep AIG solvent • September 25 – Washing Mutual Bank Fails - $300 billion in assets, 43, 000 employees - Take over buy federal government and sold • October 12 – Wachovia Bank take over - Over 100, 000 employees, $800 billion in assets - Reported a $9 billion loss in 2 nd quarter 2008 - Government forces sale to Wells Fargo Bank • December 29 – General Motors Acceptance Corp. Bailout - Founded in 1920, almost 20, 000 employees - U. S. Treasury Injects $5 Billion Dollars, eventually even more.

The Crisis 2008 • By March 2009 the U. S. stock market value was back to 1997 levels. • By September 2009 six million workers had lost their jobs throughout U. S. economy.

The Crisis 2008 • By March 2009 the U. S. stock market value was back to 1997 levels. • By September 2009 six million workers had lost their jobs throughout U. S. economy.

Causes • • Worldwide Surplus Savings U. S. Homeownership policy U. S. Psychology of Rising House Prices Lax Mortgage Standards – No skin in game – No Regulatory oversight • • Securitization Failure of Rating Agencies Credit Default Swaps Financial Market Deregulation

Causes • • Worldwide Surplus Savings U. S. Homeownership policy U. S. Psychology of Rising House Prices Lax Mortgage Standards – No skin in game – No Regulatory oversight • • Securitization Failure of Rating Agencies Credit Default Swaps Financial Market Deregulation

Glut of World Savings • China, Japan, Germany economies total trade surplus was about $750 billion in 2007. • $750 billion of saving flowing to the ROW looking for a the best return. • U. S. Economy was Borrowing about $750 Billion • Best Return = Best Risk Adjusted Return • Housing Bubble not restricted to U. S. (see, for example, Spain)

Glut of World Savings • China, Japan, Germany economies total trade surplus was about $750 billion in 2007. • $750 billion of saving flowing to the ROW looking for a the best return. • U. S. Economy was Borrowing about $750 Billion • Best Return = Best Risk Adjusted Return • Housing Bubble not restricted to U. S. (see, for example, Spain)

U. S. Homeownership Culture/Policy • Federal Housing Administration – Established 1934, borrower pays small insurance premium and FHA insures lender will receive 100% repayment. • Fannie Mae – Government Sponsored Enterprise. Established 1938 to support Mortgage Market. Bought 30 year mortgages, high Loan to value , middle class mortgages. Financed Fannie Mae Bond, implicitly backed by federal government.

U. S. Homeownership Culture/Policy • Federal Housing Administration – Established 1934, borrower pays small insurance premium and FHA insures lender will receive 100% repayment. • Fannie Mae – Government Sponsored Enterprise. Established 1938 to support Mortgage Market. Bought 30 year mortgages, high Loan to value , middle class mortgages. Financed Fannie Mae Bond, implicitly backed by federal government.

U. S. Homeownership Culture/Policy • Government National Mortgage Association • Established in 1968 to : – To sell and guarantee bonds backed by special FHA and special mortgages to veterans. - The Original Mortgage Backed Security.

U. S. Homeownership Culture/Policy • Government National Mortgage Association • Established in 1968 to : – To sell and guarantee bonds backed by special FHA and special mortgages to veterans. - The Original Mortgage Backed Security.

U. S. Homeownership Culture/Policy • Freddie Mac – Another Government Sponsored Enterprise. Established 1970 to support Mortgage Market. • Compete directly with private market. Bought and resold conventional mortgages. • Purpose was to add liquidity to the market.

U. S. Homeownership Culture/Policy • Freddie Mac – Another Government Sponsored Enterprise. Established 1970 to support Mortgage Market. • Compete directly with private market. Bought and resold conventional mortgages. • Purpose was to add liquidity to the market.

U. S. Homeownership Culture/Policy • Home Mortgage Interest Deduction • Anyone borrowing to buy a home can subtract the interest payments from their reported income, reporting lower taxable income and thereby paying less tax. • The large the loan the bigger the tax break! • With progressive income tax, higher income get a bigger break.

U. S. Homeownership Culture/Policy • Home Mortgage Interest Deduction • Anyone borrowing to buy a home can subtract the interest payments from their reported income, reporting lower taxable income and thereby paying less tax. • The large the loan the bigger the tax break! • With progressive income tax, higher income get a bigger break.

U. S. Psychology of Rising House Prices • “We’ve never had a decline in house prices on a nationwide basis. So, what I think what is more likely is that house prices will slow, maybe stabilize, might slow consumption spending a bit. I don’t think it’s going to drive the economy too far from its full employment path, though. ” » Ben Bernanke, Federal Reserve Chairman, » CNBC, July 1, 2005. »

U. S. Psychology of Rising House Prices • “We’ve never had a decline in house prices on a nationwide basis. So, what I think what is more likely is that house prices will slow, maybe stabilize, might slow consumption spending a bit. I don’t think it’s going to drive the economy too far from its full employment path, though. ” » Ben Bernanke, Federal Reserve Chairman, » CNBC, July 1, 2005. »

2001 Q 1 2001 Q 2 2001 Q 3 2001 Q 4 2002 Q 1 2002 Q 2 2002 Q 3 2002 Q 4 2003 Q 1 2003 Q 2 2003 Q 3 2003 Q 4 2004 Q 1 2004 Q 2 2004 Q 3 2004 Q 4 2005 Q 1 2005 Q 2 2005 Q 3 2005 Q 4 2006 Q 1 2006 Q 2 2006 Q 3 2006 Q 4 2007 Q 1 2007 Q 2 2007 Q 3 2007 Q 4 2008 Q 1 2008 Q 2 2008 Q 3 2008 Q 4 2009 Q 1 2009 Q 2 2009 Q 3 2009 Q 4 2010 Q 1 2010 Q 2 2010 Q 3 2010 Q 4 2011 Q 1 2011 Q 2 2011 Q 3 2011 Q 4 2012 Q 1 2012 Q 2 Federal Housing Agency House Price Index 15. 00% -10. 00% HPI % Change Over Previous 4 Quarters 10. 00% 5. 00% 0. 00% -5. 00% HPI % Change Over Previous 4 Quarters

2001 Q 1 2001 Q 2 2001 Q 3 2001 Q 4 2002 Q 1 2002 Q 2 2002 Q 3 2002 Q 4 2003 Q 1 2003 Q 2 2003 Q 3 2003 Q 4 2004 Q 1 2004 Q 2 2004 Q 3 2004 Q 4 2005 Q 1 2005 Q 2 2005 Q 3 2005 Q 4 2006 Q 1 2006 Q 2 2006 Q 3 2006 Q 4 2007 Q 1 2007 Q 2 2007 Q 3 2007 Q 4 2008 Q 1 2008 Q 2 2008 Q 3 2008 Q 4 2009 Q 1 2009 Q 2 2009 Q 3 2009 Q 4 2010 Q 1 2010 Q 2 2010 Q 3 2010 Q 4 2011 Q 1 2011 Q 2 2011 Q 3 2011 Q 4 2012 Q 1 2012 Q 2 Federal Housing Agency House Price Index 15. 00% -10. 00% HPI % Change Over Previous 4 Quarters 10. 00% 5. 00% 0. 00% -5. 00% HPI % Change Over Previous 4 Quarters

Weakening Mortgage Lending Standards • The Community Reinvestment Act, 1977 – Intended to encourage depository institutions to help meet the credit needs of low- and moderate-income neighborhoods…… – Political pressure on banks increased in the 1990’ and early 2000’s. Regulators told banks that much higher LTVs was an appropriate way to meet their CRA obligations. –

Weakening Mortgage Lending Standards • The Community Reinvestment Act, 1977 – Intended to encourage depository institutions to help meet the credit needs of low- and moderate-income neighborhoods…… – Political pressure on banks increased in the 1990’ and early 2000’s. Regulators told banks that much higher LTVs was an appropriate way to meet their CRA obligations. –

Private Mortgage Originators • Banks could meet their CRA obligations by buying high-risk, nontraditional mortgages from what were essentially private contracting firms that in many cases produced deceptive mortgage documents. • With the boom times in housing, easy lending standards spread. As long as house prices were rising any loan could be repaid by selling the house. • No incentive to consider risk of default!

Private Mortgage Originators • Banks could meet their CRA obligations by buying high-risk, nontraditional mortgages from what were essentially private contracting firms that in many cases produced deceptive mortgage documents. • With the boom times in housing, easy lending standards spread. As long as house prices were rising any loan could be repaid by selling the house. • No incentive to consider risk of default!

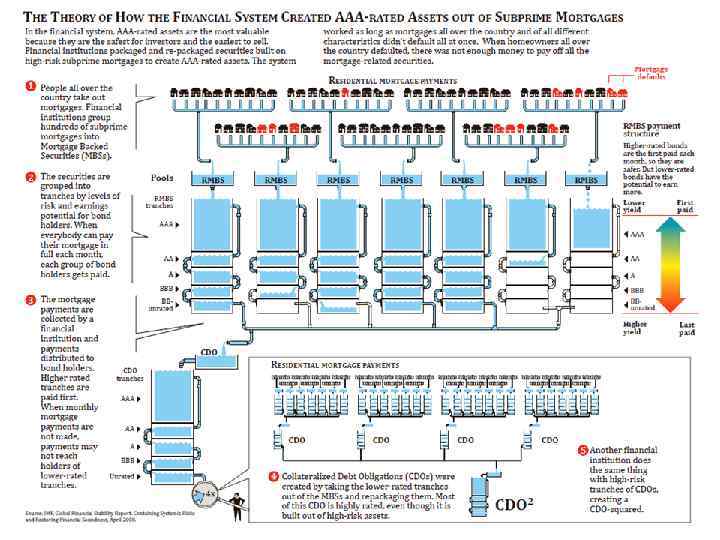

Securitization The Mortgage Backed Security Securitization allows homeowners access to enormous amounts of additional funding and thereby makes homeownership more affordable. It also can diversify housing risk among different types of lenders.

Securitization The Mortgage Backed Security Securitization allows homeowners access to enormous amounts of additional funding and thereby makes homeownership more affordable. It also can diversify housing risk among different types of lenders.

Collateralized Debt Obligations The CDO: Mortgaged Backed Securities that were combined, repackaged and then divided up in ways that were supposed to diversify away much of the risk. Recall: “We have never had a decline in house prices on a nationwide basis. ” Bernanke

Collateralized Debt Obligations The CDO: Mortgaged Backed Securities that were combined, repackaged and then divided up in ways that were supposed to diversify away much of the risk. Recall: “We have never had a decline in house prices on a nationwide basis. ” Bernanke

Credit Default Swap • An insurance contract purchased by the holder of a debt instrument for protection against the debt instrument defaulting. • One caveat: It was possible and legal to but Credit Default Swap insurance even if you did not hold the debt instrument! Pure gambling. • AIG was very big provider of this “insurance. ”

Credit Default Swap • An insurance contract purchased by the holder of a debt instrument for protection against the debt instrument defaulting. • One caveat: It was possible and legal to but Credit Default Swap insurance even if you did not hold the debt instrument! Pure gambling. • AIG was very big provider of this “insurance. ”

The Big Three Credit Rating Agencies • Moody’s, S & P, Fitch (95% of Market) • Nationally Recognized Statistical Rating Organizations (NRSRO) by U. S. SEC. • These three gave AAA ratings to mortgaged backed CDO’s

The Big Three Credit Rating Agencies • Moody’s, S & P, Fitch (95% of Market) • Nationally Recognized Statistical Rating Organizations (NRSRO) by U. S. SEC. • These three gave AAA ratings to mortgaged backed CDO’s

Federal Reserve Response • Discount Rate Reductions • Traditional Open Market Operations – Buying U. S Treasuries – inject liquidity – Lower Fed Funds Rate – Cut 10 times from 2007 to end of 2008 – Lowers borrowing cost for banks

Federal Reserve Response • Discount Rate Reductions • Traditional Open Market Operations – Buying U. S Treasuries – inject liquidity – Lower Fed Funds Rate – Cut 10 times from 2007 to end of 2008 – Lowers borrowing cost for banks

Federal Reserve Response • Swap lines with foreign central banks – Fed swapped dollars foreign currency. Allowed foreign central banks to provide Dollar Liquidity where needed. – Program lasted through December 2010 – Currency exchange at specific rate with agreement to swap back at same rate at later date. – Overnight, one week, One month, Three month – Total reached over $500 billion dollars • -

Federal Reserve Response • Swap lines with foreign central banks – Fed swapped dollars foreign currency. Allowed foreign central banks to provide Dollar Liquidity where needed. – Program lasted through December 2010 – Currency exchange at specific rate with agreement to swap back at same rate at later date. – Overnight, one week, One month, Three month – Total reached over $500 billion dollars • -

Federal Reserve Response • Term Securities Lending Facility – Everybody wanted to hold U. S. Treasury Bonds – Treasury prices rise, interest rates fall – The Fed lent U. S. Treasury Bonds for 30 day periods in exchange for a wide range of collateral assets (mostly mortgage backed securities). – Up to $200 billion lent out – March 2008 to February 2010

Federal Reserve Response • Term Securities Lending Facility – Everybody wanted to hold U. S. Treasury Bonds – Treasury prices rise, interest rates fall – The Fed lent U. S. Treasury Bonds for 30 day periods in exchange for a wide range of collateral assets (mostly mortgage backed securities). – Up to $200 billion lent out – March 2008 to February 2010

Federal Reserve Response • Primary Dealer Credit Facility • For a few large primary dealers: Citibank, Goldman Sachs, Morgan Stanly etc. • Mostly, the primary dealers traded mortgage backed securities in exchange for Treasury bonds. • March 2008 to February 2010 • Allowed by Section 13(3) of the Federal Reserve Act

Federal Reserve Response • Primary Dealer Credit Facility • For a few large primary dealers: Citibank, Goldman Sachs, Morgan Stanly etc. • Mostly, the primary dealers traded mortgage backed securities in exchange for Treasury bonds. • March 2008 to February 2010 • Allowed by Section 13(3) of the Federal Reserve Act

Federal Reserve Response • Term Auction Facility – To get liquidity to over 7000 commercial banks – Banks bid on borrowing each week. – Fix amount of funds available each week – Anonymous highest bidders (interest rates) get funds – Assign collateral to the Fed. (Current illiquid assets with little current marketability. ) – December 2007 until March 2010

Federal Reserve Response • Term Auction Facility – To get liquidity to over 7000 commercial banks – Banks bid on borrowing each week. – Fix amount of funds available each week – Anonymous highest bidders (interest rates) get funds – Assign collateral to the Fed. (Current illiquid assets with little current marketability. ) – December 2007 until March 2010

Federal Reserve Response • Asset Backed Commercial Paper Money Market Mutual Fund Liquidity Facility (AMLF) • Banks use “money market” to make 30 -day loans to businesses, who borrow using Accounts Receivable as collateral. This market freezes up as people pull money out of Money Market Mutual Funds. Fed lends money for banks to purchase 30 day loans re-liquifying the market. • September 2008 to February 2010

Federal Reserve Response • Asset Backed Commercial Paper Money Market Mutual Fund Liquidity Facility (AMLF) • Banks use “money market” to make 30 -day loans to businesses, who borrow using Accounts Receivable as collateral. This market freezes up as people pull money out of Money Market Mutual Funds. Fed lends money for banks to purchase 30 day loans re-liquifying the market. • September 2008 to February 2010

Federal Reserve Response • Money Market Investor Funding Facility • Goal to provide liquidity to U. S. money market mutual funds allowing institutions to honor withdrawals. • October 2008 to October 2009

Federal Reserve Response • Money Market Investor Funding Facility • Goal to provide liquidity to U. S. money market mutual funds allowing institutions to honor withdrawals. • October 2008 to October 2009

Federal Reserve Response • QE 1 - Purchase of Long Term Debt • Purchase $1. 25 trillion of GSE debt and Long Term Treasury Bonds. Goal : to reduce long term rates in Housing market. • QE 2 – Additional purchase of long term Treasuries. • QE 1 – November 2008 to March 2009 • QE 2 – November 2010 to June 2011

Federal Reserve Response • QE 1 - Purchase of Long Term Debt • Purchase $1. 25 trillion of GSE debt and Long Term Treasury Bonds. Goal : to reduce long term rates in Housing market. • QE 2 – Additional purchase of long term Treasuries. • QE 1 – November 2008 to March 2009 • QE 2 – November 2010 to June 2011

Quantitative Easing: Increase Bank") Federal Reserve Response • Chairman Bernanke Makes a Distinction: 1) Quantitative Easing: Increase Bank Reserves 2) Credit Easing: Ease credit in specific area of market

Federal Reserve Response • Chairman Bernanke Makes a Distinction: 1) Quantitative Easing: Increase Bank Reserves 2) Credit Easing: Ease credit in specific area of market

U. S. Treasury Response • Troubled Asset Relief Fund –October 2008 • Congress authorized the Treasury Department to use up to $700 billion to stabilize financial markets • By Oct. 2, 2010 it had committed $470 billion to hundreds of banks, to A. I. G. , to the car industry, and to help homeowners.

U. S. Treasury Response • Troubled Asset Relief Fund –October 2008 • Congress authorized the Treasury Department to use up to $700 billion to stabilize financial markets • By Oct. 2, 2010 it had committed $470 billion to hundreds of banks, to A. I. G. , to the car industry, and to help homeowners.

• quick deal, the short-term • gain—without proper consideration of longterm consequences

• quick deal, the short-term • gain—without proper consideration of longterm consequences