cb04239449e33e7bd065a67f80a3af98.ppt

- Количество слайдов: 47

The Key Questions of Corporate Finance

The Key Questions of Corporate Finance

Investment Policy") (Real) Investment Policy

(Real) Investment Policy

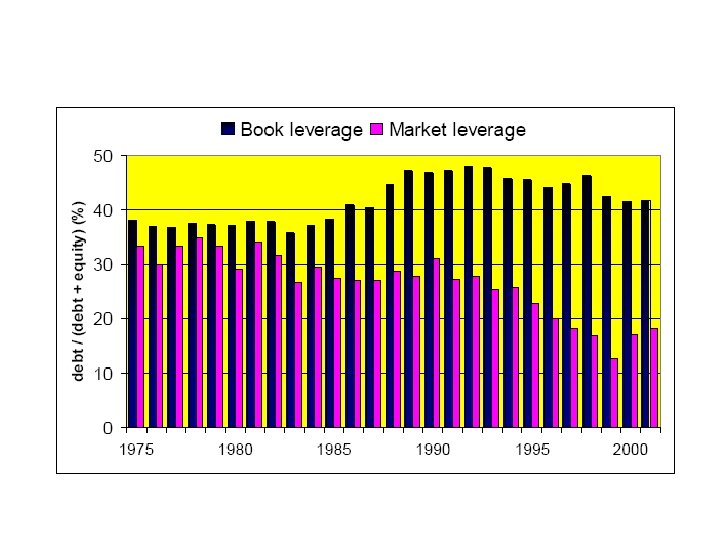

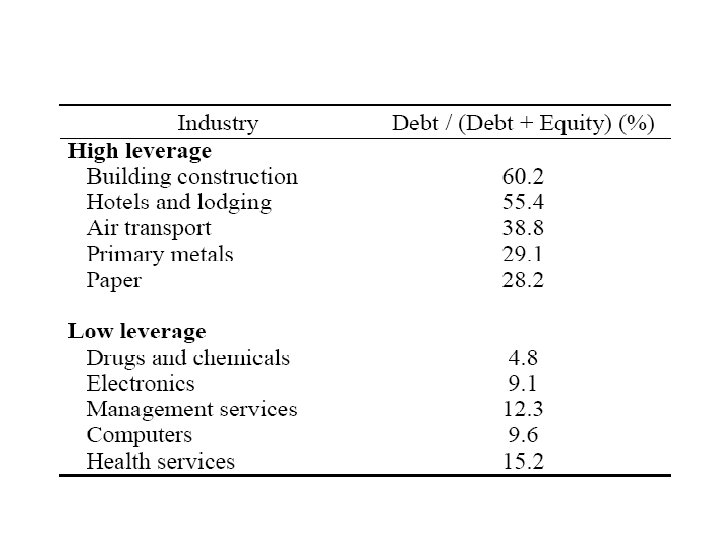

Capital structure, International 1991

Capital structure, International 1991

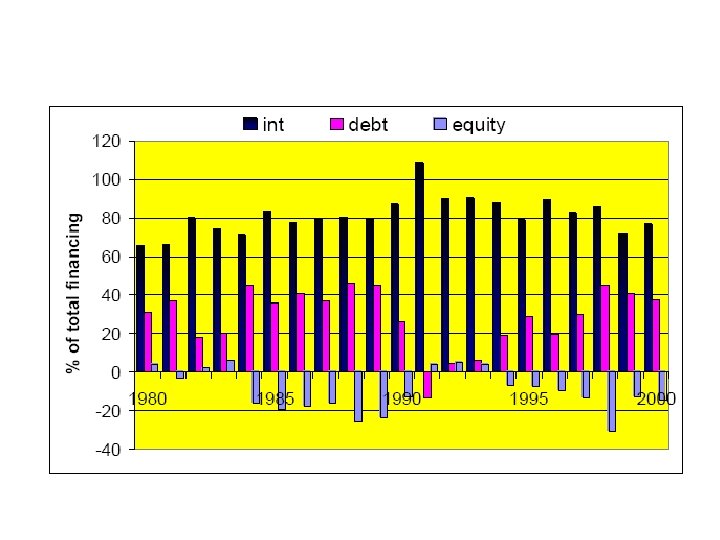

Sources of Funds: International 1990 -94

Sources of Funds: International 1990 -94

M-M’s “Irrelevance” Theorem

M-M’s “Irrelevance” Theorem

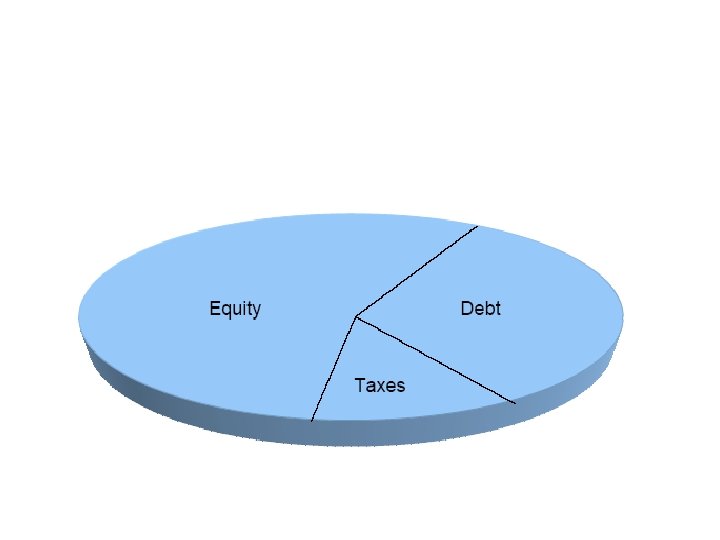

*") MM Theorem: Proof 1 (pie theory)*

MM Theorem: Proof 1 (pie theory)*

") MM Theorem: Proof 2 (market efficiency)

MM Theorem: Proof 2 (market efficiency)

") MM Theorem: Proof 2 (market efficiency)

MM Theorem: Proof 2 (market efficiency)

MM Theorem: Example

MM Theorem: Example

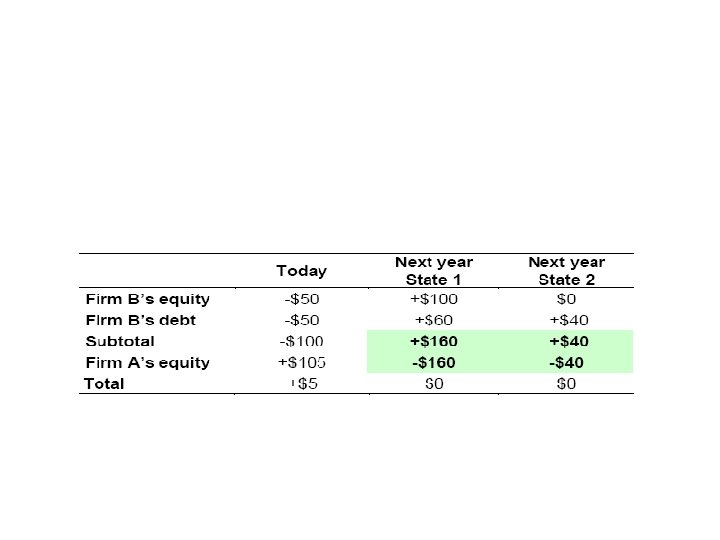

MM Theorem: Proof 3

MM Theorem: Proof 3

MM Theorem: Proof 3

MM Theorem: Proof 3

The Curse of M-M

The Curse of M-M

Using M-M Sensibly

Using M-M Sensibly

WACC Fallacy: “Debt is Better Because Debt Is Cheaper Than Equity. ”

WACC Fallacy: “Debt is Better Because Debt Is Cheaper Than Equity. ”

") WACC Fallacy (cont. )

WACC Fallacy (cont. )

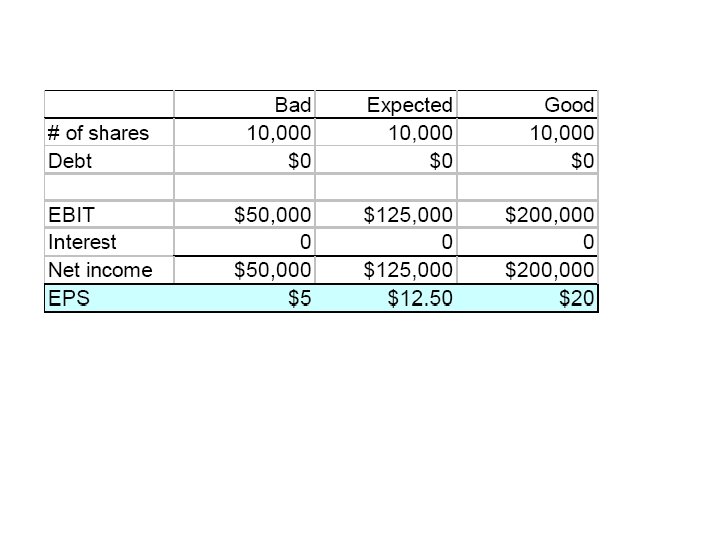

EPS Fallacy: “Debt is Better When It Makes EPS Go Up. ”

EPS Fallacy: “Debt is Better When It Makes EPS Go Up. ”

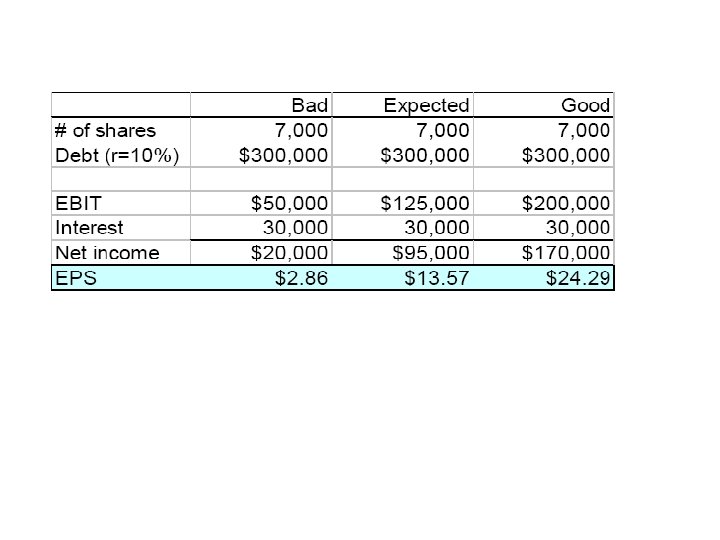

") EPS Fallacy (cont. )

EPS Fallacy (cont. )

Leverage, returns, and risk

Leverage, returns, and risk

Leverage, returns, and risk

Leverage, returns, and risk

Leverage and beta

Leverage and beta

Leverage and required returns

Leverage and required returns

Example

Example

Win-Win Fallacy: “Debt Is Better Because Some Investors Prefer Debt to Equity. ”

Win-Win Fallacy: “Debt Is Better Because Some Investors Prefer Debt to Equity. ”

Practical Implications

Practical Implications

Debt Tax Shield

Debt Tax Shield

Example In 2000, Microsoft had sales of $23 billion, earnings before taxes of $14. 3 billion, and net income of $9. 4 billion. Microsoft paid $4. 9 billion in taxes, had a market value of $423 billion, and had no long-term debt outstanding. Bill Gates is thinking about a recapitalization, issuing $50 billion in long-term debt (rd = 7%) and repurchasing $50 billion in stock. How would this transaction affect Microsoft’s after-tax cash flows and shareholder wealth?

Example In 2000, Microsoft had sales of $23 billion, earnings before taxes of $14. 3 billion, and net income of $9. 4 billion. Microsoft paid $4. 9 billion in taxes, had a market value of $423 billion, and had no long-term debt outstanding. Bill Gates is thinking about a recapitalization, issuing $50 billion in long-term debt (rd = 7%) and repurchasing $50 billion in stock. How would this transaction affect Microsoft’s after-tax cash flows and shareholder wealth?

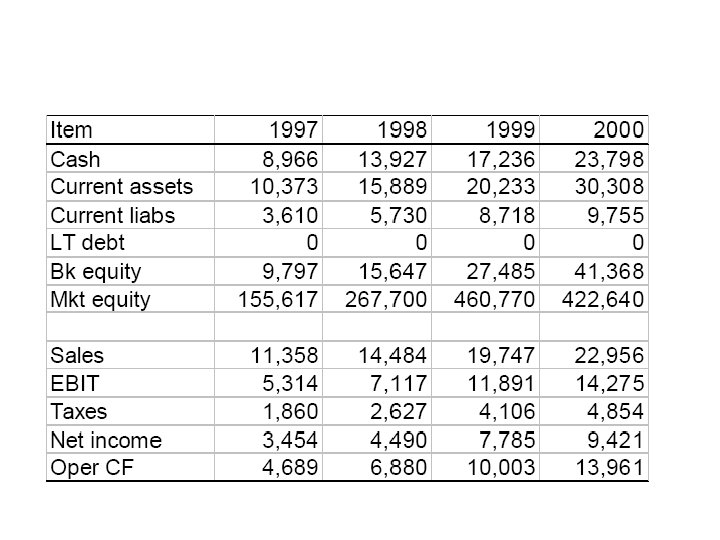

") Microsoft, 2000 ($ millions)

Microsoft, 2000 ($ millions)

Tax savings of debt

Tax savings of debt