4a229dc9001db59bcb12926fdcfd6aa8.ppt

- Количество слайдов: 22

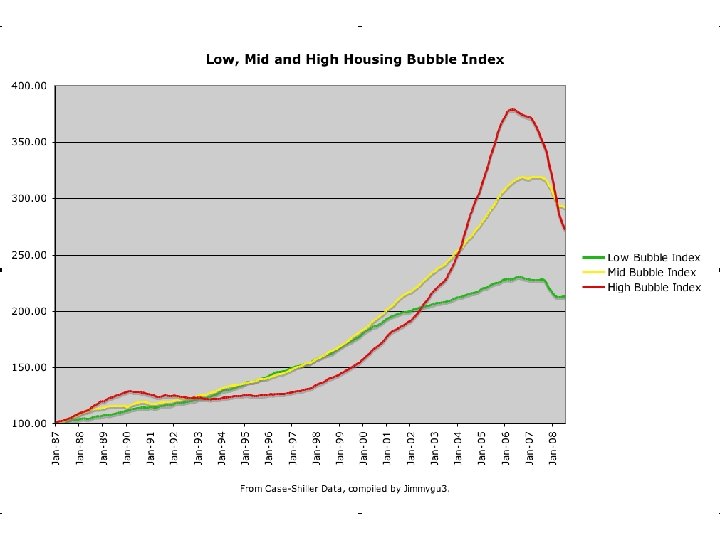

The Housing Market Crash 2006 What happened?

The Housing Market Crash 2006 What happened?

GROUP/MARKET B House Original Asking Price Period 1 Sale Price Period 3 Sale Price Period 7 Sale Price Period 8 Sale Price Selling price More or Less Seller #1 $345, 000 $600, 000 $520, 000 $510, 000 More Seller #2 $352, 000 $1, 000 $700, 000 $372, 000 More

GROUP/MARKET B House Original Asking Price Period 1 Sale Price Period 3 Sale Price Period 7 Sale Price Period 8 Sale Price Selling price More or Less Seller #1 $345, 000 $600, 000 $520, 000 $510, 000 More Seller #2 $352, 000 $1, 000 $700, 000 $372, 000 More

GROUP/MARKET B 2 Homes/Sellers 4 Buyers

GROUP/MARKET B 2 Homes/Sellers 4 Buyers

GROUP/MARKET A House Original Asking Price Selling price More or Less Period 1 Sale Price Period 3 Sale Price Period 7 Sale Price Period 8 Sale Price Seller #1 $345, 000 No Sale $330, 000 $291, 000 No Sale Less Seller #2 $352, 000 $300, 000 No Sale $322, 000 $100, 000 Less Seller #3 $343, 000 No Sale Less Seller #4 $348, 000 $305, 000 $55, 000 $315, 000 $338, 000 Less

GROUP/MARKET A House Original Asking Price Selling price More or Less Period 1 Sale Price Period 3 Sale Price Period 7 Sale Price Period 8 Sale Price Seller #1 $345, 000 No Sale $330, 000 $291, 000 No Sale Less Seller #2 $352, 000 $300, 000 No Sale $322, 000 $100, 000 Less Seller #3 $343, 000 No Sale Less Seller #4 $348, 000 $305, 000 $55, 000 $315, 000 $338, 000 Less

GROUP/MARKET A 4 Homes/Sellers 2 Buyers

GROUP/MARKET A 4 Homes/Sellers 2 Buyers

Many sellers Few Buyers Many Buyers Few Sellers Prices GO DOWN GO UP

Many sellers Few Buyers Many Buyers Few Sellers Prices GO DOWN GO UP

The Mortgage What does the mortgage lender do? 1. Check credit score 2. Check your income 3. Check your savings

The Mortgage What does the mortgage lender do? 1. Check credit score 2. Check your income 3. Check your savings

CREDIT SCORE 1. Do you pay your bills on time? 2. How much debt do you have?

CREDIT SCORE 1. Do you pay your bills on time? 2. How much debt do you have?

INCOME DO YOU MAKE ENOUGH MONEY EACH MONTH TO MAKE THE MONTHLY INSTALLMENT PAYMENT?

INCOME DO YOU MAKE ENOUGH MONEY EACH MONTH TO MAKE THE MONTHLY INSTALLMENT PAYMENT?

SAVINGS DO YOU HAVE ENOUGH MONEY TO MAKE A DOWN PAYMENT AND PAY FOR OTHER COSTS RELATED TO BUYING A HOUSE?

SAVINGS DO YOU HAVE ENOUGH MONEY TO MAKE A DOWN PAYMENT AND PAY FOR OTHER COSTS RELATED TO BUYING A HOUSE?

Purchase Price $380, 000

Purchase Price $380, 000

BUYER #1 • Credit Score 755 • Income $150, 000 • Savings $85, 000 (20% down payment)

BUYER #1 • Credit Score 755 • Income $150, 000 • Savings $85, 000 (20% down payment)

BUYER #2 • Credit Score 590 • Income $50, 000 • Savings $5, 000 (0% down payment)

BUYER #2 • Credit Score 590 • Income $50, 000 • Savings $5, 000 (0% down payment)

BUYER #3 • Credit Score 725 • Income $100, 000 • Savings $40, 000 (10% down payment)

BUYER #3 • Credit Score 725 • Income $100, 000 • Savings $40, 000 (10% down payment)

BUYER #4 • Credit Score 655 • Income $85, 000 • Savings $10, 000 (2% down payment)

BUYER #4 • Credit Score 655 • Income $85, 000 • Savings $10, 000 (2% down payment)

WHY SHOULD A LENDER BE CAREFUL WHEN LENDING MONEY FOR MORTGAGES? • In a “normal” market banks only make money if the borrower pays the money back. • It costs banks a lot of money to foreclose on a home.

WHY SHOULD A LENDER BE CAREFUL WHEN LENDING MONEY FOR MORTGAGES? • In a “normal” market banks only make money if the borrower pays the money back. • It costs banks a lot of money to foreclose on a home.

HOW DOES THE LENDER BENEFIT FROM LENDING THIS MONEY TO YOU? • Principal loan amount $380, 000 • Interest paid over 30 years: $354, 32. 20 • Total payments $734, 321. 20

HOW DOES THE LENDER BENEFIT FROM LENDING THIS MONEY TO YOU? • Principal loan amount $380, 000 • Interest paid over 30 years: $354, 32. 20 • Total payments $734, 321. 20

NINA Loans “No income/No asset” verification If the banks are now willing to lend money without verifying income and assets, how many borrowers will be approved for a loan? What does that do to the housing market?

NINA Loans “No income/No asset” verification If the banks are now willing to lend money without verifying income and assets, how many borrowers will be approved for a loan? What does that do to the housing market?

Why would a lender be willing to lend without looking at all the relevant information? The mistaken belief that home prices would never go down. Lender A found a way to sell the mortgages and still make money.

Why would a lender be willing to lend without looking at all the relevant information? The mistaken belief that home prices would never go down. Lender A found a way to sell the mortgages and still make money.

HOW? LENDER 1 loans money to 10 people to buy homes. Lender makes money on fees charged to the buyers. LENDER 2 offers to buy all of LENDER 1’s MORTGAGE LOANS. LENDER 1 does not care if those 10 people can actually pay back the loans.

HOW? LENDER 1 loans money to 10 people to buy homes. Lender makes money on fees charged to the buyers. LENDER 2 offers to buy all of LENDER 1’s MORTGAGE LOANS. LENDER 1 does not care if those 10 people can actually pay back the loans.

WHY? Wall Street created a market for mortgages that could not survive. Government made it easier for banks to loan more money. People bought homes they could not afford.

WHY? Wall Street created a market for mortgages that could not survive. Government made it easier for banks to loan more money. People bought homes they could not afford.