9a9e4dd360c661c8214243ca38bab253.ppt

- Количество слайдов: 21

The Costs of Production § Outline: – Study how firm’s decisions regarding prices and quantities depend on the market conditions they face – Firm’s costs are a key determinant of its production (supply curve) and its pricing decisions – Firm’s objective therefore is to maximize its profits – Profits= TR-TC

The Costs of Production § Outline: – Study how firm’s decisions regarding prices and quantities depend on the market conditions they face – Firm’s costs are a key determinant of its production (supply curve) and its pricing decisions – Firm’s objective therefore is to maximize its profits – Profits= TR-TC

The Costs of Production § TR= Total Revenue= Px. Q § Total Revenue is the amount a firm receives from the sale of its output § Total cost is the amount a firm pays to buy the units of production § Economist’s interpretation of total cost includes the opportunity cost of production as well

The Costs of Production § TR= Total Revenue= Px. Q § Total Revenue is the amount a firm receives from the sale of its output § Total cost is the amount a firm pays to buy the units of production § Economist’s interpretation of total cost includes the opportunity cost of production as well

The Costs of Production § A firm’s opportunity costs can be obvious at times and not so obvious at other times § Explicit costs are input costs that require an outlay of money by the firm § Implicit costs are input costs that do not require an outlay of money by the firm

The Costs of Production § A firm’s opportunity costs can be obvious at times and not so obvious at other times § Explicit costs are input costs that require an outlay of money by the firm § Implicit costs are input costs that do not require an outlay of money by the firm

Economic Costs Versus Accounting Costs § Accountants measure explicit costs (as it involves money flows) § Economists use both explicit costs (wages, rent, cost of raw material) and implicit costs (foregone income) to arrive at the total cost of production § The cost of capital is an opportunity cost due to the foregone interest on savings (implicit cost)

Economic Costs Versus Accounting Costs § Accountants measure explicit costs (as it involves money flows) § Economists use both explicit costs (wages, rent, cost of raw material) and implicit costs (foregone income) to arrive at the total cost of production § The cost of capital is an opportunity cost due to the foregone interest on savings (implicit cost)

Economic Profit Versus Accounting Profit § Economic profit is the TR minus TC, including both explicit and implicit costs § Accounting profit is the TR minus total explicit cost § Therefore, economic profit is smaller than accounting profit

Economic Profit Versus Accounting Profit § Economic profit is the TR minus TC, including both explicit and implicit costs § Accounting profit is the TR minus total explicit cost § Therefore, economic profit is smaller than accounting profit

Economic Profit Versus Accounting Profit Economic profit TR Accounting profit Implicit Costs OC Explicit costs Economist’s view TR Explicit costs Accountant's view

Economic Profit Versus Accounting Profit Economic profit TR Accounting profit Implicit Costs OC Explicit costs Economist’s view TR Explicit costs Accountant's view

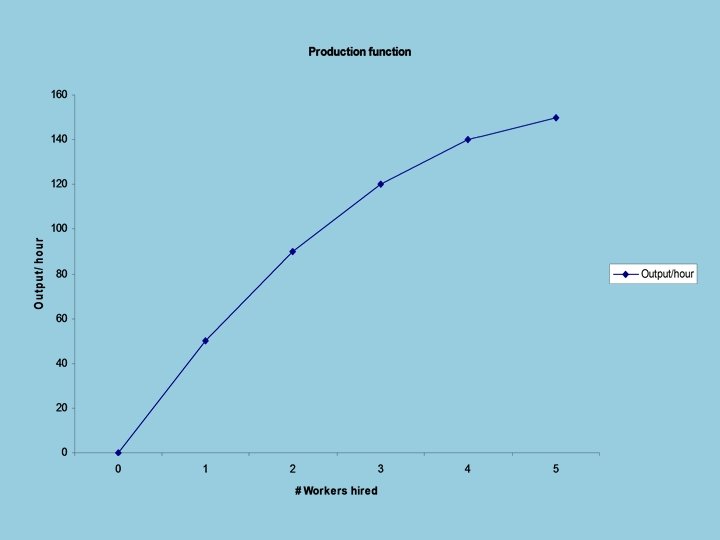

Production and Costs § What is the link between a firm’s production process and its total cost? – Fixed size of the firm – Labor is the only variable input – Decisions in the SR (# of labor to hire and quantity of output to produce) § Production function is the relationship between the quantity of inputs used to make a good and the quantity of output of the good

Production and Costs § What is the link between a firm’s production process and its total cost? – Fixed size of the firm – Labor is the only variable input – Decisions in the SR (# of labor to hire and quantity of output to produce) § Production function is the relationship between the quantity of inputs used to make a good and the quantity of output of the good

Production and Costs § Marginal product is the increase in output that arises from an additional unit of input § Diminishing marginal product is the property whereby the marginal product of an input declines as the quantity of the input increases § The slope of the production function is given as the change in output for an additional input of labor. § Slope of the production function measures the marginal product of input

Production and Costs § Marginal product is the increase in output that arises from an additional unit of input § Diminishing marginal product is the property whereby the marginal product of an input declines as the quantity of the input increases § The slope of the production function is given as the change in output for an additional input of labor. § Slope of the production function measures the marginal product of input

Production and Costs # workers 0 1 2 3 4 5 Output /hour 0 50 90 120 140 150 Wage=$10/ worker MP of L Cost of factory 30 50 30 40 30 30 30 20 30 10 30 Cost of workers 0 10 20 30 40 50 TC of inputs 30 40 50 60 70 80

Production and Costs # workers 0 1 2 3 4 5 Output /hour 0 50 90 120 140 150 Wage=$10/ worker MP of L Cost of factory 30 50 30 40 30 30 30 20 30 10 30 Cost of workers 0 10 20 30 40 50 TC of inputs 30 40 50 60 70 80

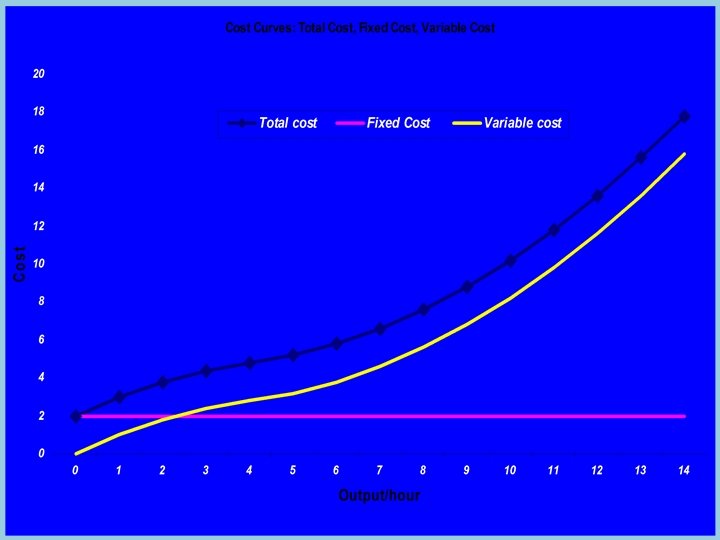

Production Function and Total Cost § § § Total cost curve shows the relationship between the quantity of output produced and the total cost of production Production function gets flatter as the amount of input increases (diminishing Marginal Product) Total cost curve gets steeper as the amount produced rises (production cost of a marginal unit of output increases)

Production Function and Total Cost § § § Total cost curve shows the relationship between the quantity of output produced and the total cost of production Production function gets flatter as the amount of input increases (diminishing Marginal Product) Total cost curve gets steeper as the amount produced rises (production cost of a marginal unit of output increases)

=TFC+TVC Fixed Costs (TFC)") Measures of Cost § § § § Total Cost (TC) =TFC+TVC Fixed Costs (TFC) are costs that do not vary with the quantity of output (Q) produced Variable Costs (TVC) are costs that do vary with the quantity of output produced Average Cost (ATC) = TC/Q Average Fixed Cost (AFC)= TFC/Q Average Variable Cost (AVC)= TVC/Q Marginal cost (MC)= change in TC/change in Q MC is the increase in total cost that arises from an extra unit of production

Measures of Cost § § § § Total Cost (TC) =TFC+TVC Fixed Costs (TFC) are costs that do not vary with the quantity of output (Q) produced Variable Costs (TVC) are costs that do vary with the quantity of output produced Average Cost (ATC) = TC/Q Average Fixed Cost (AFC)= TFC/Q Average Variable Cost (AVC)= TVC/Q Marginal cost (MC)= change in TC/change in Q MC is the increase in total cost that arises from an extra unit of production

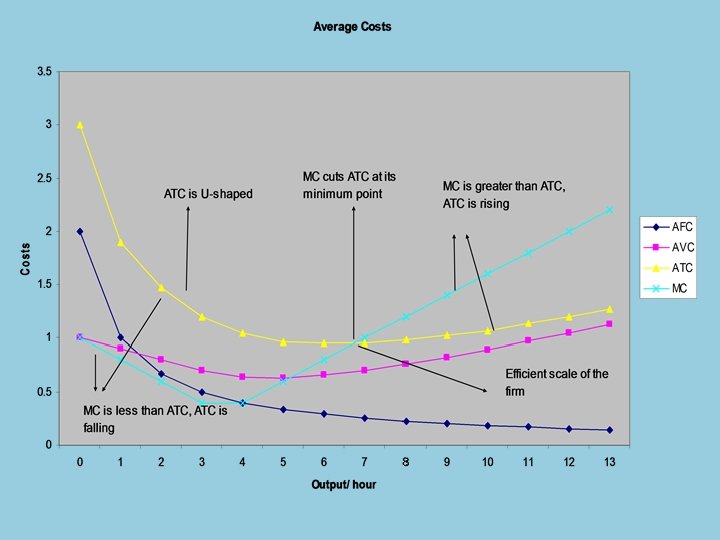

Production and Costs § Cost of production has an impact on the firm’s production decisions – Cost of producing a typical unit of output (ATC) – Cost of producing an additional unit of output (MC) § Cost curves and their shapes – X-axis measures the quantity produced – Y-axis measures the cost of production

Production and Costs § Cost of production has an impact on the firm’s production decisions – Cost of producing a typical unit of output (ATC) – Cost of producing an additional unit of output (MC) § Cost curves and their shapes – X-axis measures the quantity produced – Y-axis measures the cost of production

Q/hour TC FC VC AFC AVC ATC MC 0 2. 00 0. 00 - - - 1 3. 00 2. 00 1. 00 3. 00 1. 00 2 3. 80 2. 00 1. 80 1. 00 0. 90 1. 90 0. 80 3 4. 40 2. 00 2. 40 0. 67 0. 80 1. 47 0. 60 4 4. 80 2. 00 2. 80 0. 50 0. 70 1. 20 0. 40 5 5. 20 2. 00 3. 20 0. 40 0. 64 1. 04 0. 40 6 5. 80 2. 00 3. 80 0. 33 0. 63 0. 96 0. 60 7 6. 60 2. 00 4. 60 0. 29 0. 66 0. 95 0. 80 8 7. 60 2. 00 5. 60 0. 25 0. 70 0. 95 1. 00 9 8. 80 2. 00 6. 80 0. 22 0. 76 0. 98 1. 20 10 10. 20 2. 00 8. 20 0. 82 1. 02 1. 40 11 11. 80 2. 00 9. 80 0. 18 0. 89 1. 07 1. 60 12 13. 60 2. 00 11. 60 0. 17 0. 97 1. 14 1. 80 13 15. 60 2. 00 13. 60 0. 15 1. 05 1. 20 2. 00 14 17. 80 2. 00 15. 80 0. 14 1. 13 1. 27 2. 20

Q/hour TC FC VC AFC AVC ATC MC 0 2. 00 0. 00 - - - 1 3. 00 2. 00 1. 00 3. 00 1. 00 2 3. 80 2. 00 1. 80 1. 00 0. 90 1. 90 0. 80 3 4. 40 2. 00 2. 40 0. 67 0. 80 1. 47 0. 60 4 4. 80 2. 00 2. 80 0. 50 0. 70 1. 20 0. 40 5 5. 20 2. 00 3. 20 0. 40 0. 64 1. 04 0. 40 6 5. 80 2. 00 3. 80 0. 33 0. 63 0. 96 0. 60 7 6. 60 2. 00 4. 60 0. 29 0. 66 0. 95 0. 80 8 7. 60 2. 00 5. 60 0. 25 0. 70 0. 95 1. 00 9 8. 80 2. 00 6. 80 0. 22 0. 76 0. 98 1. 20 10 10. 20 2. 00 8. 20 0. 82 1. 02 1. 40 11 11. 80 2. 00 9. 80 0. 18 0. 89 1. 07 1. 60 12 13. 60 2. 00 11. 60 0. 17 0. 97 1. 14 1. 80 13 15. 60 2. 00 13. 60 0. 15 1. 05 1. 20 2. 00 14 17. 80 2. 00 15. 80 0. 14 1. 13 1. 27 2. 20

Typical Cost Curves § A firm’s cost curves exhibit the following common features: – MC eventually rises with the quantity of output – ATC is U-shaped – MC curve crosses the ATC at the minimum of ATC § MC initially falls with increase in output but eventually rises as output increasesdiminishing marginal product

Typical Cost Curves § A firm’s cost curves exhibit the following common features: – MC eventually rises with the quantity of output – ATC is U-shaped – MC curve crosses the ATC at the minimum of ATC § MC initially falls with increase in output but eventually rises as output increasesdiminishing marginal product

Typical Cost Curves § § § AFC declines as output increases but AVC increases as output increases- explains ATC’s U-shape The bottom of the U-shape occurs at the quantity that minimizes ATC. This quantity of output is called the efficient scale of the firm MC

Typical Cost Curves § § § AFC declines as output increases but AVC increases as output increases- explains ATC’s U-shape The bottom of the U-shape occurs at the quantity that minimizes ATC. This quantity of output is called the efficient scale of the firm MC

Typical Cost Curves § § The combination of increasing and then decreasing MP also make the AVC Ushaped Both MC and AVC fall initially before rising with increase in output

Typical Cost Curves § § The combination of increasing and then decreasing MP also make the AVC Ushaped Both MC and AVC fall initially before rising with increase in output

LR and SR costs § § In the SR the firm has to continue on the same cost curve chosen in the past In the LR the firm can choose to move to a different cost curve as FC become variable

LR and SR costs § § In the SR the firm has to continue on the same cost curve chosen in the past In the LR the firm can choose to move to a different cost curve as FC become variable

Economies of scale § Economies of scale is the property whereby LR ATC falls as the quantity of output increases – Specialization leads to higher output/worker and lower ATC/unit of output § Diseconomies of scale is the property whereby LR ATC rises as the quantity of output increases – Coordination problems § Constant returns to scale is the property whereby LR ATC remains constant as the quantity of output changes

Economies of scale § Economies of scale is the property whereby LR ATC falls as the quantity of output increases – Specialization leads to higher output/worker and lower ATC/unit of output § Diseconomies of scale is the property whereby LR ATC rises as the quantity of output increases – Coordination problems § Constant returns to scale is the property whereby LR ATC remains constant as the quantity of output changes