cedfe9917ab18be158428ed550e33bb3.ppt

- Количество слайдов: 42

Texas Agricultural Forum Waco, Texas January 21, 2004 New Trade Negotiations: What’s at Stake For Texas Agriculture? Parr Rosson Center for North American Studies Department of Agricultural Economics Texas A&M University C NAS

Texas Agricultural Forum Waco, Texas January 21, 2004 New Trade Negotiations: What’s at Stake For Texas Agriculture? Parr Rosson Center for North American Studies Department of Agricultural Economics Texas A&M University C NAS

What’s at Stake? l Market Access l Secure Sources of Raw Materials & Inputs l Gains & Losses to Trade l Adjustment for Some Sectors

What’s at Stake? l Market Access l Secure Sources of Raw Materials & Inputs l Gains & Losses to Trade l Adjustment for Some Sectors

U. S. Trade Negotiations l GATT 1947 -94 l US/Israel 1985 l Uruguay Round 1986 -93 (GATT) l Canada 1989 l NAFTA 1994 (Year 10) l Doha Round 2000 -05? (WTO) l 3 Regionals Completed in 2002/03 l 6 Regionals Pending

U. S. Trade Negotiations l GATT 1947 -94 l US/Israel 1985 l Uruguay Round 1986 -93 (GATT) l Canada 1989 l NAFTA 1994 (Year 10) l Doha Round 2000 -05? (WTO) l 3 Regionals Completed in 2002/03 l 6 Regionals Pending

CUSTA, ‘ 89 NAFTA ‘ 94 CAFTA ‘ 05 Jordan ‘ 03 Bahrain Israel ‘ 85 Morocco ‘ 06 Chile ‘ 04 FTAA ‘ 06 Singapore ‘ 03 Southern African Customs Union ‘ 06 U. S. Trade Agreements Australia ‘ 05

CUSTA, ‘ 89 NAFTA ‘ 94 CAFTA ‘ 05 Jordan ‘ 03 Bahrain Israel ‘ 85 Morocco ‘ 06 Chile ‘ 04 FTAA ‘ 06 Singapore ‘ 03 Southern African Customs Union ‘ 06 U. S. Trade Agreements Australia ‘ 05

U. S. Agricultural Trade, 1970 -2003 E $70 Billion Dollars Imports Exports $60 $50 Trade Surplus Exports $40 $30 $20 Imports $10 $0 1970 72 74 76 78 80 82 84 86 88 90 92 94 96 98 2000 2003 E

U. S. Agricultural Trade, 1970 -2003 E $70 Billion Dollars Imports Exports $60 $50 Trade Surplus Exports $40 $30 $20 Imports $10 $0 1970 72 74 76 78 80 82 84 86 88 90 92 94 96 98 2000 2003 E

US Agricultural Trade with NAFTA Billion US Dollars US Exports $20 US Imports NAFTA Became Effective $15 $9 $8 $16$16 $15 $13 $12 $12 $11 $10 Trade Balance $14$14 $13$13 $9 $9 $8 $7 $6 $5 $2 $2 $2 $0 $1 -$0 $0 $0 -$5 1990 -92 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 $0

US Agricultural Trade with NAFTA Billion US Dollars US Exports $20 US Imports NAFTA Became Effective $15 $9 $8 $16$16 $15 $13 $12 $12 $11 $10 Trade Balance $14$14 $13$13 $9 $9 $8 $7 $6 $5 $2 $2 $2 $0 $1 -$0 $0 $0 -$5 1990 -92 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 $0

World Trade Organization “Doha Development Agenda” Attempt to Restart is Underway l ‘Common Sense’ Letter, 1/12/04 l Export Subsidies, Trade Distorting Policies & Cotton/Cotton Textiles l Retaining Protection of the Peace Clause Important for U. S. Agriculture & Open Markets l

World Trade Organization “Doha Development Agenda” Attempt to Restart is Underway l ‘Common Sense’ Letter, 1/12/04 l Export Subsidies, Trade Distorting Policies & Cotton/Cotton Textiles l Retaining Protection of the Peace Clause Important for U. S. Agriculture & Open Markets l

Market Access

Market Access

Tariff of Abominations, 1828 Smoot-Hawley Tariff, 1930 Morrill Act, 1861 Generalized System of Preferences, 1968 WTO, 1995 Fordney-Mc. Cumber Tariff, 1922 GATT, 1947

Tariff of Abominations, 1828 Smoot-Hawley Tariff, 1930 Morrill Act, 1861 Generalized System of Preferences, 1968 WTO, 1995 Fordney-Mc. Cumber Tariff, 1922 GATT, 1947

World Average Agricultural Tariffs, 2000 Percent 140 Bound Average World Average 115 120 85 100 80 62% 55 60 40 30 40 25 12 20 s d te h or t N U ni A m er St a te ic a U ni on Eu ro pe a n er ic a A m h So ut ra l en t C C ar ib be an A m er ic Is la nd h So ut a s A sia 0

World Average Agricultural Tariffs, 2000 Percent 140 Bound Average World Average 115 120 85 100 80 62% 55 60 40 30 40 25 12 20 s d te h or t N U ni A m er St a te ic a U ni on Eu ro pe a n er ic a A m h So ut ra l en t C C ar ib be an A m er ic Is la nd h So ut a s A sia 0

Bound Tariffs for Selected Products Percent 100 86 86 86 80 55 54 60 50 46 40 39 40 25 50 25 39 37 42 23 19 18 20 0 Total South America Source: ERS/USDA Grains Grain Products Central America Feed Caribbean Islands Oilseeds North America

Bound Tariffs for Selected Products Percent 100 86 86 86 80 55 54 60 50 46 40 39 40 25 50 25 39 37 42 23 19 18 20 0 Total South America Source: ERS/USDA Grains Grain Products Central America Feed Caribbean Islands Oilseeds North America

Bound Tariffs for Selected Products Percent 100 91 88 86 90 90 87 85 80 80 68 55 60 40 68 49 48 43 43 41 41 43 34 21 20 0 Live Animals South America Source: ERS/USDA Meat Fresh Meat Frozen Meat Prepared Central America Caribbean Islands Dairy North America

Bound Tariffs for Selected Products Percent 100 91 88 86 90 90 87 85 80 80 68 55 60 40 68 49 48 43 43 41 41 43 34 21 20 0 Live Animals South America Source: ERS/USDA Meat Fresh Meat Frozen Meat Prepared Central America Caribbean Islands Dairy North America

New Agreements

New Agreements

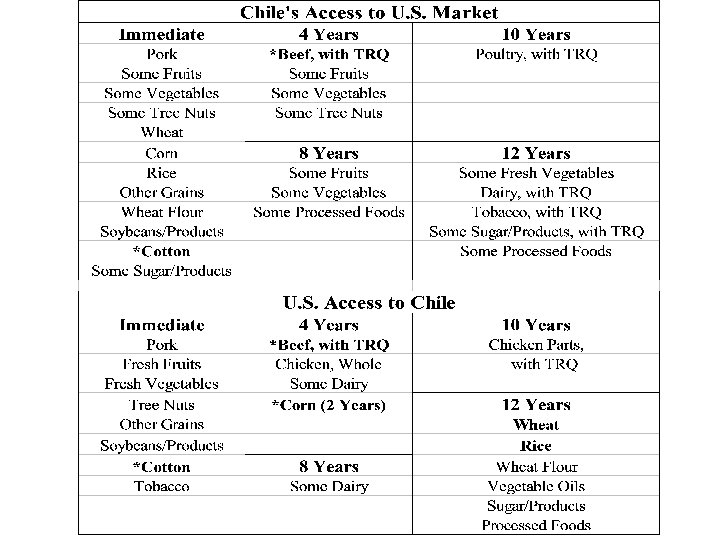

Chile Effective January 1, 2004 l Tariffs Eliminated Immediately, or Over 4, 8, 10 or 12 Years l Chile’s Price Band System on Wheat, Vegetable Oils, & Sugar Eliminated l U. S. Receives Preferential Access Compared to Canada & European Union l U. S. Export Impacts Small (18 -52%) l U. S. Import Impacts Small (6 -14%) l

Chile Effective January 1, 2004 l Tariffs Eliminated Immediately, or Over 4, 8, 10 or 12 Years l Chile’s Price Band System on Wheat, Vegetable Oils, & Sugar Eliminated l U. S. Receives Preferential Access Compared to Canada & European Union l U. S. Export Impacts Small (18 -52%) l U. S. Import Impacts Small (6 -14%) l

U. S. -Chile Agricultural Trade, 1990 - 2002 $1, 500 Billion U. S. Dollars $1, 154 $910 $1, 000 $751 $500 $481 $63 $445 $72 $495 $94 $457 $109 $543 $103 $745 $1, 027 $1, 023 $784 $547 $169 $126 $135 $152 $116 $98 $111 $0 -$500 -$348 -$378 -$418 -$374 -$401 -$441 -$625 -$619 -$648 -$758 -$1, 000 -$910 -$924 U. S. Exports U. S. Imports Balance -$1, 043 -$1, 500 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

U. S. -Chile Agricultural Trade, 1990 - 2002 $1, 500 Billion U. S. Dollars $1, 154 $910 $1, 000 $751 $500 $481 $63 $445 $72 $495 $94 $457 $109 $543 $103 $745 $1, 027 $1, 023 $784 $547 $169 $126 $135 $152 $116 $98 $111 $0 -$500 -$348 -$378 -$418 -$374 -$401 -$441 -$625 -$619 -$648 -$758 -$1, 000 -$910 -$924 U. S. Exports U. S. Imports Balance -$1, 043 -$1, 500 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

U. S. Agricultural Exports to Chile, 2002 Total: $111. 1 Million Food Preps 9. 0% Animal Feed 6. 6% Rice 6. 1% Cotton 4. 2% Saps/Thickeners 3. 2% Seeds 3. 2% Corn 3. 0% $10. 0 $7. 3 Wheat 16. 3% $18. 1 $6. 8 $4. 7 $3. 6 $3. 5 $3. 3 $19. 9 $33. 9 Other 30. 5% Corn Gluten 17. 9%

U. S. Agricultural Exports to Chile, 2002 Total: $111. 1 Million Food Preps 9. 0% Animal Feed 6. 6% Rice 6. 1% Cotton 4. 2% Saps/Thickeners 3. 2% Seeds 3. 2% Corn 3. 0% $10. 0 $7. 3 Wheat 16. 3% $18. 1 $6. 8 $4. 7 $3. 6 $3. 5 $3. 3 $19. 9 $33. 9 Other 30. 5% Corn Gluten 17. 9%

U. S. Agricultural Imports from Chile, 2002 Total: $1, 154 Million Grape Wines 11. 9% Stone Fruit 9. 4% Corn 7. 1% $108. 7 $136. 9 $82. 2 Avocados 7. 1% Fruit Juices 4. 8% Apples/Pears 4. 6% Kiwi/Berries 3. 4% $81. 5 $464. 1 $55. 5 Grapes 40. 2% $52. 8 $39. 3 $132. 6 Other 11. 5%

U. S. Agricultural Imports from Chile, 2002 Total: $1, 154 Million Grape Wines 11. 9% Stone Fruit 9. 4% Corn 7. 1% $108. 7 $136. 9 $82. 2 Avocados 7. 1% Fruit Juices 4. 8% Apples/Pears 4. 6% Kiwi/Berries 3. 4% $81. 5 $464. 1 $55. 5 Grapes 40. 2% $52. 8 $39. 3 $132. 6 Other 11. 5%

Central America Free Trade Agreement

Central America Free Trade Agreement

CAFTA WHO so Far? El Salvador, Guatemala, Honduras, Nicaragua l Costa Rica & Dominican Republic to be Added w/in Months l l About ½ of Markets Open to U. S. Agriculture When Implemented (Jan. 2005)? ? – l HQ Beef, Cotton, Wheat, Soybeans Rest Over 15 -20 Years: Pork, Beef, Poultry, Rice, Corn, Dairy

CAFTA WHO so Far? El Salvador, Guatemala, Honduras, Nicaragua l Costa Rica & Dominican Republic to be Added w/in Months l l About ½ of Markets Open to U. S. Agriculture When Implemented (Jan. 2005)? ? – l HQ Beef, Cotton, Wheat, Soybeans Rest Over 15 -20 Years: Pork, Beef, Poultry, Rice, Corn, Dairy

Mexico North Houston, 1, 300 Miles NW Dominican Republic, 800 Miles NE

Mexico North Houston, 1, 300 Miles NW Dominican Republic, 800 Miles NE

3. 9 $8, 300 El Salvador 6. 5") CAFTA Demographics Costa Rica Pop. (mil) 3. 9 $8, 300 El Salvador 6. 5 $4, 600 Guatemala 13. 9 $3, 900 Honduras 6. 7 $2, 500 Nicaragua 5. 1 $2, 200 Dom. Rep. 8. 7 $6, 300 Country GDP/ Person Total/Avg. 44. 8 $4, 633 Total/Avg Poverty % 20. 6 Lit. % 96 Ag. Pop. % 20 48 75 53 50 80. 2 30 70. 6 76. 1 67. 5 50 34 42 25 84. 7 17 45. 3 79. 2 32. 2

CAFTA Demographics Costa Rica Pop. (mil) 3. 9 $8, 300 El Salvador 6. 5 $4, 600 Guatemala 13. 9 $3, 900 Honduras 6. 7 $2, 500 Nicaragua 5. 1 $2, 200 Dom. Rep. 8. 7 $6, 300 Country GDP/ Person Total/Avg. 44. 8 $4, 633 Total/Avg Poverty % 20. 6 Lit. % 96 Ag. Pop. % 20 48 75 53 50 80. 2 30 70. 6 76. 1 67. 5 50 34 42 25 84. 7 17 45. 3 79. 2 32. 2

2002

2002

U. S. Agricultural Exports to Central America Total, 1990: $482 million Total, 2000: $1118 million Grains & Feeds $217 Oilseeds $90 Other $69 Oilseeds $194 Vegetables Tobacco $27 Animals $33 $47 Grains & Feeds $422 Rice $56 Other $196 Animals $162 Vegetables $89

U. S. Agricultural Exports to Central America Total, 1990: $482 million Total, 2000: $1118 million Grains & Feeds $217 Oilseeds $90 Other $69 Oilseeds $194 Vegetables Tobacco $27 Animals $33 $47 Grains & Feeds $422 Rice $56 Other $196 Animals $162 Vegetables $89

U. S. Rice Exports, 1993 and 2002 Thousand Metric Tons 1993 Total: 2, 860 TMT 1, 000 2002 Total: 3, 809 TMT 897 691 800 625 620 573 600 481 419 417 400 200 324 315 266 112 99 88 65 0 1993 N Amer. C Amer. 2002 Asia W Europe Carib. Mid East Source: Foreign Agricultural Service, USDA, www. fas. usda. gov/ustrade Africa S Amer.

U. S. Rice Exports, 1993 and 2002 Thousand Metric Tons 1993 Total: 2, 860 TMT 1, 000 2002 Total: 3, 809 TMT 897 691 800 625 620 573 600 481 419 417 400 200 324 315 266 112 99 88 65 0 1993 N Amer. C Amer. 2002 Asia W Europe Carib. Mid East Source: Foreign Agricultural Service, USDA, www. fas. usda. gov/ustrade Africa S Amer.

U. S. Agricultural Imports from Central America Total, 2000: $2977 million Total, 1990: $1699 million Fish Coffee Shellfish Bananas $732 Sugar $159 $211 Coffee $611 $133 $372 Fish $478 Other $742 Bananas $453 Shellfish $368 Fruits $274 Other $1361

U. S. Agricultural Imports from Central America Total, 2000: $2977 million Total, 1990: $1699 million Fish Coffee Shellfish Bananas $732 Sugar $159 $211 Coffee $611 $133 $372 Fish $478 Other $742 Bananas $453 Shellfish $368 Fruits $274 Other $1361

Free Trade Area of the Americas

Free Trade Area of the Americas

FTAA Open Markets in Western Hemisphere – Average US Ag. Tariffs 12% – South America: 40% – Caribbean: 85% l Negotiations Moving Forward, But Slower than Expected: Brazil a Sticking Point l Target Date for Completion 1/05 l Target Date for Implementation 1/06 l

FTAA Open Markets in Western Hemisphere – Average US Ag. Tariffs 12% – South America: 40% – Caribbean: 85% l Negotiations Moving Forward, But Slower than Expected: Brazil a Sticking Point l Target Date for Completion 1/05 l Target Date for Implementation 1/06 l

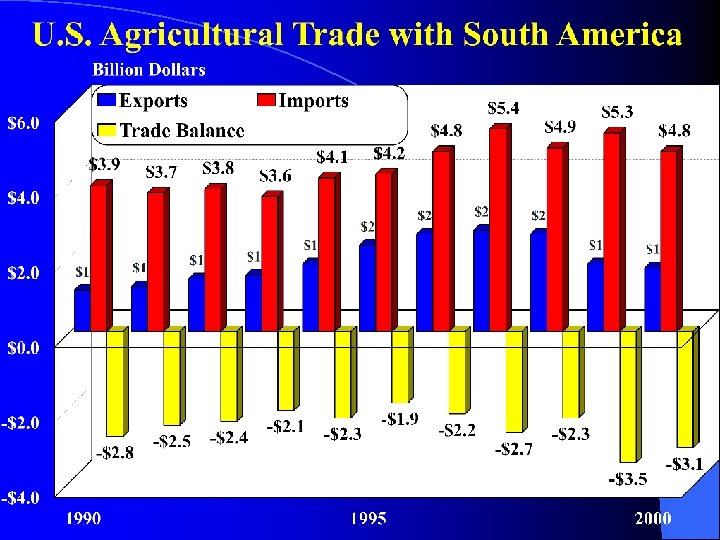

U. S. Agricultural Exports to South America Total, 1990: $1062 million Grains $575 Total, 2000: $1706 million Oilseeds $230 Grains $711 Animals $197 Oilseeds $141 Animals $131 Other $96 Cotton Vegetables $141 $59 Rice $62 Other $305 Vegetables $122 Source: Foreign Agricultural Trade of The United States , Calendar Year, USDA/ERS

U. S. Agricultural Exports to South America Total, 1990: $1062 million Grains $575 Total, 2000: $1706 million Oilseeds $230 Grains $711 Animals $197 Oilseeds $141 Animals $131 Other $96 Cotton Vegetables $141 $59 Rice $62 Other $305 Vegetables $122 Source: Foreign Agricultural Trade of The United States , Calendar Year, USDA/ERS

U. S. Agricultural Imports from South America Total, 1990: $5179 million Other $3288 Total, 2000: $6847 million Shellfish $657 Bananas $487 Sugar Prod. $279 Fruits $742 Fish $1410 Bananas $449 Coffee $799 Fish $788 Shellfish $491 Fruit Juices $644 Coffee $851 Other $4487 Source: Foreign Agricultural Trade of The United States , Calendar Year, USDA/ERS

U. S. Agricultural Imports from South America Total, 1990: $5179 million Other $3288 Total, 2000: $6847 million Shellfish $657 Bananas $487 Sugar Prod. $279 Fruits $742 Fish $1410 Bananas $449 Coffee $799 Fish $788 Shellfish $491 Fruit Juices $644 Coffee $851 Other $4487 Source: Foreign Agricultural Trade of The United States , Calendar Year, USDA/ERS

Raw Materials & Inputs

Raw Materials & Inputs

U. S. Oil Imports by Source NAFTA 14. 00 OPEC 11. 46 Million Barrels/Day (Avg. ) 12. 00 12. 03 11. 02 10. 16 10. 00 8. 00 Non-OPEC (Ex. NAFTA) 8. 02 7. 71 8. 33 8. 84 6. 91 5. 07 6. 00 4. 00 2. 00 0. 00 1985 1990 1993 NAFTA 1995 1997 2000 2001 2002 Petroleum Imports by Country of Origin, 1960 -2001. USDOE, EIA, Annual & Monthly Reports

U. S. Oil Imports by Source NAFTA 14. 00 OPEC 11. 46 Million Barrels/Day (Avg. ) 12. 00 12. 03 11. 02 10. 16 10. 00 8. 00 Non-OPEC (Ex. NAFTA) 8. 02 7. 71 8. 33 8. 84 6. 91 5. 07 6. 00 4. 00 2. 00 0. 00 1985 1990 1993 NAFTA 1995 1997 2000 2001 2002 Petroleum Imports by Country of Origin, 1960 -2001. USDOE, EIA, Annual & Monthly Reports

U. S. Fertilizer Imports Canada 20. 0 W. Europe ROW 18. 1 16. 6 Million Metric Tons 13. 6 13. 7 13. 9 15. 0 14. 6 17. 0 15. 3 14. 9 12. 2 10. 8 10. 4 10. 0 5. 0 0. 0 1990 USDA, FAS 1993 1995 2000 2002

U. S. Fertilizer Imports Canada 20. 0 W. Europe ROW 18. 1 16. 6 Million Metric Tons 13. 6 13. 7 13. 9 15. 0 14. 6 17. 0 15. 3 14. 9 12. 2 10. 8 10. 4 10. 0 5. 0 0. 0 1990 USDA, FAS 1993 1995 2000 2002

U. S. Fertilizer Imports from ROW Annual Average 1990 -92 250 226 1, 000 Metric Tons 200 193 200 150 117 111 100 50 0 a o ag us r la b To / ad id in Tr co i ar Be / ia i ex M lg Bu s us R l e ra le hi C Is

U. S. Fertilizer Imports from ROW Annual Average 1990 -92 250 226 1, 000 Metric Tons 200 193 200 150 117 111 100 50 0 a o ag us r la b To / ad id in Tr co i ar Be / ia i ex M lg Bu s us R l e ra le hi C Is

U. S. Fertilizer Imports from Row, 2002 1600 1400 1291 1, 000 Metric Tons 1200 1000 800 438 600 394 289 400 216 178 160 200 88 72 31 0 t ai o cc o or uw K M a bi a a i an u th Li t yp Eg el zu e en V n ai hr Ba r a at Q s o g ba To ra i. A ud Sa / ad id u ar el /B ia s us in Tr R

U. S. Fertilizer Imports from Row, 2002 1600 1400 1291 1, 000 Metric Tons 1200 1000 800 438 600 394 289 400 216 178 160 200 88 72 31 0 t ai o cc o or uw K M a bi a a i an u th Li t yp Eg el zu e en V n ai hr Ba r a at Q s o g ba To ra i. A ud Sa / ad id u ar el /B ia s us in Tr R

Gains to Trade

Gains to Trade

Exports, Imports, Farm Income U. S. Agricultural Exports to W. H. Countries Up 8% After Full Phase. In to $600 million l U. S. Agricultural Imports from W. H. Countries Up 6% to $850 Million l U. S. Farm Income Up $200 Million/Year l ERS, USDA, 2000.

Exports, Imports, Farm Income U. S. Agricultural Exports to W. H. Countries Up 8% After Full Phase. In to $600 million l U. S. Agricultural Imports from W. H. Countries Up 6% to $850 Million l U. S. Farm Income Up $200 Million/Year l ERS, USDA, 2000.

Sector Impacts More Exports of Corn, Soybeans, Cotton l More Imports/Competition for Sugar, Peanuts, Citrus, Some Vegetables l FTAA Likely to $4. 0 Billion to U. S. GDP/Year l ERS, USDA, 2000.

Sector Impacts More Exports of Corn, Soybeans, Cotton l More Imports/Competition for Sugar, Peanuts, Citrus, Some Vegetables l FTAA Likely to $4. 0 Billion to U. S. GDP/Year l ERS, USDA, 2000.

So What for Texas? More Exports & Potential for Higher Prices l Access to Lower Cost Inputs l More Competition in Some Sectors – Sugar, Peanuts, Textiles, Maybe Cotton – Meats-But Sanitary Issues Critical – Winter Vegetables & Some Fruit Products: SPS Important l Opportunity for Input on Agreements as ‘Fast Track’ is Implemented l

So What for Texas? More Exports & Potential for Higher Prices l Access to Lower Cost Inputs l More Competition in Some Sectors – Sugar, Peanuts, Textiles, Maybe Cotton – Meats-But Sanitary Issues Critical – Winter Vegetables & Some Fruit Products: SPS Important l Opportunity for Input on Agreements as ‘Fast Track’ is Implemented l

Issues for Texas Are More Trade Agreements a Desirable Outcome? l Without CAFTA & FTAA, U. S. Market Access Limited l Even with Agreements, No Guarantee of Strong Export Growth l Political & Economic Stability Disrupt Trade l With or Without Agreements, More Trade Disputes Certain l

Issues for Texas Are More Trade Agreements a Desirable Outcome? l Without CAFTA & FTAA, U. S. Market Access Limited l Even with Agreements, No Guarantee of Strong Export Growth l Political & Economic Stability Disrupt Trade l With or Without Agreements, More Trade Disputes Certain l

Center for North American Studies C NAS “Informed Decisions for Global Change” Parr Rosson Ph: 979 -845 -3070 E-mail: prosson@tamu. edu

Center for North American Studies C NAS “Informed Decisions for Global Change” Parr Rosson Ph: 979 -845 -3070 E-mail: prosson@tamu. edu