ecc375e8c101228e700290374080c4f2.ppt

- Количество слайдов: 22

TAX BENEFIT GUIDELINES PAUL D. MALEY IOTA ANNUAL MEETING NOVEMBER 21, 2009 ORLANDO FL

RULES AND EXAMPLES SEE: http: //www. irs. gov/pub/irs-pdf/p 526. pdf • Under a new recordkeeping rule effective for all cash, check, electronic funds transfers, credit card charges, or other monetary contributions of any amount made in taxable years beginning after August 17, 2006, the donor must obtain and keep a bank record or a written communication from the donee as a record of the contribution. Written records prepared by the donor (such as check registers or personal notations) are no longer sufficient to support charitable contributions.

• A donor claiming a deduction of $250 or more is also required to obtain and keep a contemporaneous written acknowledgment for a charitable contribution.

• If the donee provides goods or services to the donor in exchange for the contribution (a quid pro quo contribution), the written acknowledgment must include a good faith estimate of the value of the goods or services. The donee is not required to record or report this information to the IRS on behalf of a donor. The donor is responsible for requesting and obtaining the written acknowledgement from the donee.

• For claimed contributions over $5, 000, generally a qualified appraisal prepared by a qualified appraiser must be obtained. For appraisals prepared in connection with returns or submissions filed after August 17, 2006, see Notice 2006 -96.

REAL BENFIT OF CASH DONATION • • • TAX BRACKET -- $ -- BENEFIT – LOSS 10% $100 $10 $90 15% $100 $15 $85 25% $100 $25 $75 28% $100 $28 $72 33% $100 $33 $67

CONSIDERATION • • WHAT IS REASONABLE WHAT IS NOT YOU ARE LIABLE DOCUMENT ALL EXPENSES KEEP A LOG KEEP ALL RECEIPTS BE SURE EXPENSES CAN MEET SCRUTINY

DEFINTIONS • Event cycle: reasonable time period from when you have to leave your home to get to the event and back • Expense: that which is unique to the event and passes the reasonableness test • IOTA reference: IOTA officer who can provide advice on whether the expense is legitimate or not • Bribe: a donation necessary to effect access to the event. Unless directly an admission fee, this is not a legitimate deduction. • Donated: means you send it to the treasurer for documentation and receipt. You do not have possession of it unless IOTA loans it to you for use and return within a prestated time period.

EXAMPLE-1 • EQUIPMENT -MUST BE DONATED TO IOTA PER IOTA REFERENCE CONTACT -MUST DOCUMENT COST, DATE OF PURCHASE -EQUIPMENT MUST BE DIRECTLY APPLICABLE TO IOTA APPLICATION -MUST BE USED EXCLUSIVELY FOR IOTA ACTIVITY -GET RECIPT FROM IOTA AFTER DONATION

USE OF YOUR OWN EQUIPMENT WITHOUT DONATION • MUST PASS REASONABLENSS TEST PER IOTA REFERENCE CONTACT • E. g. telescope: can deduct repairs to it provided it is used EXCLUSIVELY for IOTA activities • Buy an upgraded finder: YES, IF DONATED • Buy a focal reducer used only for IOTA activity: YES, IF DONATED • Tape for tape recorder: YES (considered an expendable item) • Batteries for shortwave radio: YES (considered an expendable item)

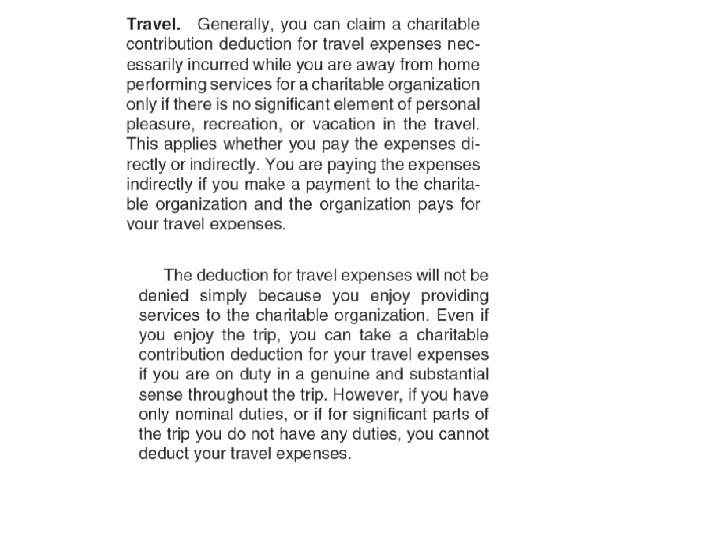

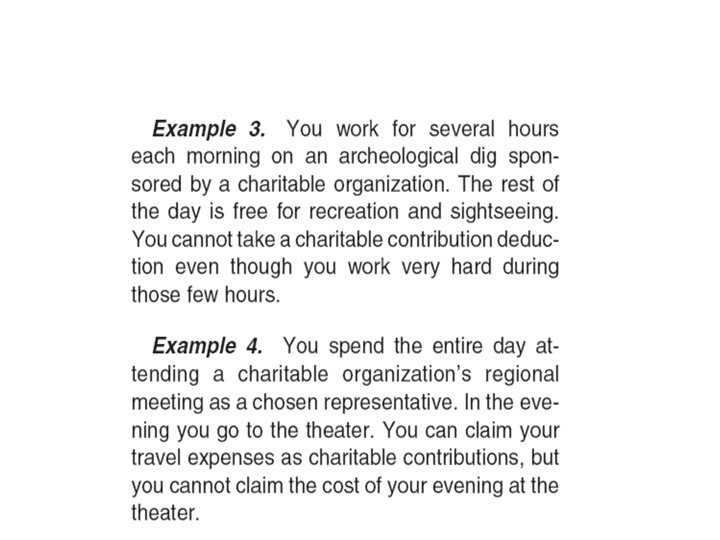

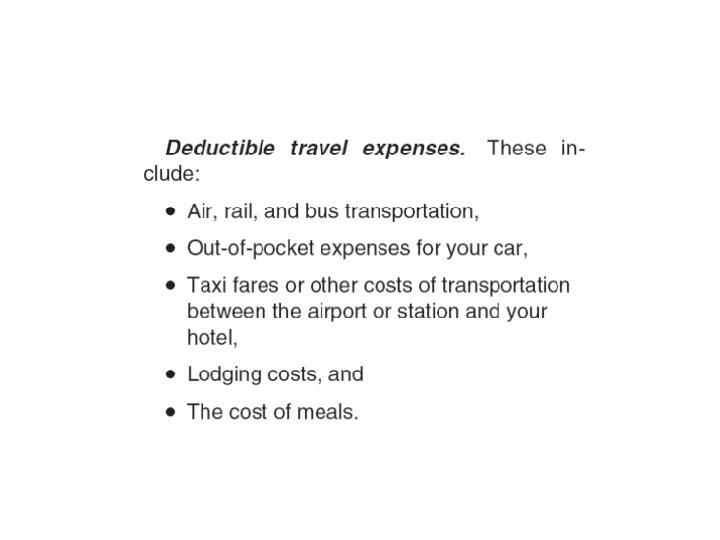

EXPENSES OF TRAVEL-1 • AIRFARE/TRAIN/SHIP/BUS: YES, provided it is directly from your home to the event and back; no deviations • MEALS: YES, provided within the reasonable time frame of the event cycle • GAS/OIL: YES • HOTEL: YES, if within event cycle • ENTERTAINMENT: NO! • BRIBES: NO! • RENT CAR: YES • TOLLS: YES

EXPENSES OF TRAVEL-2 • ADMISSION TO SIX FLAGS: NO, unless it is the observing site (highly improbable • ADMISSION TO PARK: YES, if it is the observing site • VISA FEE/DEPARTURE TAX: YES • CURRENCY EXCHANGE FEE: YES, if currency is to be used exclusively for legitimate IOTA expenses

EXPENSES OF TRAVEL-3 • POWER CHORD, EXTENSION CHORD OBTAINED ON TRIP BECAUSE IT WAS VITAL TO THE DATA COLLECTION: MAYBE • PHONE EXPENSE: MAYBE if used to obtain time signals for the event or to synchronize watch • INTERNET ACCESS FEES: MAYBE if used to access email/weather sites directly related to IOTA activities

EXPENSES OF TRAVEL-4 • MEDICAL EXPENSES: NO • LOST LUGGAGE EXPENSES: MAYBE • REPLACEMENT OF EQUIPMENT LOST OR DAMAGED IN TRANSIT: NO unless considered an ‘expendable item’. • THEFT: NO • COPIES: YES if directly related to the event • MEMORY STICK/CARDS: NO • CAMERA EQUIPMENT: NO, unless donated and used exclusively for IOTA activities

END

ecc375e8c101228e700290374080c4f2.ppt