fc9093a8cdb0d516bab9ef7e65c30d92.ppt

- Количество слайдов: 67

Revenue Policy, Revenue Administration, and Decentralization Public Finance and Management Course, World Bank, April 23, 2007 Richard M. Bird

Overview p Revenue-expenditure linkages n n p Macro – Fiscal space: MTFF, stabilization, elasticity Micro – decentralization, earmarking, charges Questions considered n n n Who pays? How? What difference does it make?

Potential Sources of Revenue Charges and fees p Earnings – SOEs, etc. p Regulatory taxes p Seignorage p Inflation tax p Borrowing p General taxation p

For Example - User Charges In principle, user charges for services are excellent sources of revenue, especially local revenue n n They are economically efficient They can also be fair and equitable

User Charges But in practice, they are not used as extensively as they should be and are seldom well-designed. Too often, user charges are Inefficient p Inequitable p Costly to administer p

User Charges These problems arise largely because most user charges are imposed simply for revenue purposes with no real attention to their design. Moreover, even well-designed charges are seldom politically popular, especially if they are imposed for a service that has previously been underpriced.

User Charges How to Do It – in principle 1. 2. 3. 4. Impose charges only where it pays to do so – especially public utilities such as water and electricity Design such charges efficiently Ensure public acceptance of charges e. g. through attention to distributional aspects Avoid “nuisance” charges

Why Introducing or Increasing User Charges is Tricky in Practice p You have to n n n n Know the product Know the data Adjust data as necessary Set the prices Justify any subsidy clearly Think through how to implement it And, importantly, sell the scheme to both clients and suppliers Of course can say much the same about any change in revenue policy but budgetary impacts usually larger so more likely to pay attention to (most of) these points

Turning to Taxes: Key Questions How do tax systems differ across countries? p What can, or should, taxes do? p What criteria are useful in thinking about the design and operation of tax systems? p What constraints may limit the tax policy options available in a particular country? p

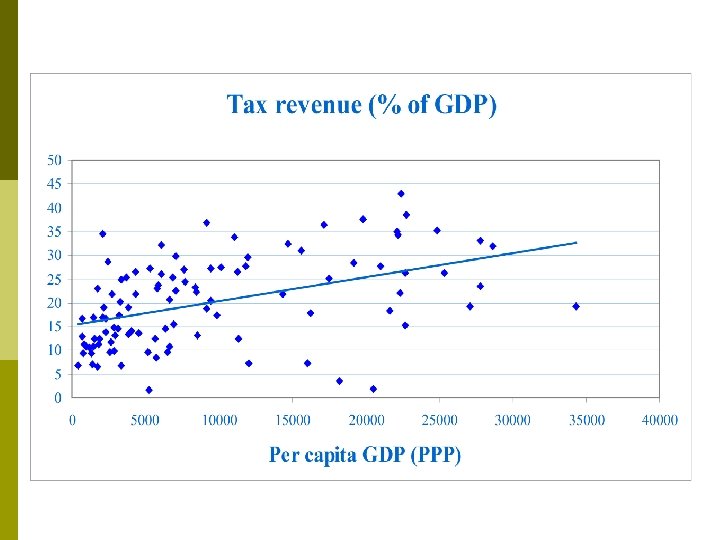

The Tax Burden Tax Revenue as a Percentage of GDP by GDP/Capita Category, 1999 -2001

")

Tax Capacity (2001)

What explains differences? Different demands and tastes for government services p Different capacities to tax p n n Level of economic development Size of informal economy Different abilities to impose and collect taxes p Other revenue sources p

Tax Instruments: Regional Differences in Reliance Latin America: Percentage of Total Tax Revenue, 1975 -2002

Tax Instruments: Regional Differences in Reliance Africa: Percentage of Total Tax Revenue, 1975 -2002

Relative Use of Different Tax Instruments. . . p Factors influencing relative mix of different tax instruments n n Revenue considerations Administrative considerations Fairness considerations Transition and political considerations

Trends in Tax Reform Increased reliance on VAT p Increased pressure to reduce trade taxes p Increased tax competition foreign investment p Reduction in top tax rates under individual income tax system p Reduction in top tax rates under business profits tax p Flat taxes? p

Predictions for Future p p Tax design will be largely dictated by domestic considerations But no tax system can now be designed without regard to tax systems of other countries Globalization will increase challenges in taxing income from capital Possibly …. regional cooperation may lead to increased harmonization of tax systems

What Can Taxes Do? Raise revenue to fund government operations p Assist in redistribution of wealth or income p Encourage or discourage certain activities p But always at some cost in terms of efficiency and growth p

Competing Government Objectives What considerations exist in choosing among the different objectives? p The real and perceived role of taxes in p n n n Encouraging economic growth Reducing disparity between the rich and the poor Reducing poverty Sharing the cost of government fairly Favoring the ‘good’, discouraging the ‘bad’ – one must walk very carefully in these treacherous grounds

Criteria for Evaluating Taxes Revenue productivity p Efficiency p Fairness p Administrative feasibility p As an available policy instrument – Yes, but…. . p

The cost of collecting taxes p Costs of taxation n Excess burden of taxes n Excess burden of tax evasion n Tax administration costs n Compliance - and avoidance - costs. n Psychic and social costs?

Efficiency p Taxes influence behavior n n n p Work vs. leisure Save vs. spend Choice of products Choice of organizational and financial structure Choice of location for investment Operate in formal economy vs. operate in informal economy “Deadweight” or “distortion” costs n n n Almost all taxes distort Costs are real costs—especially for economies where resources are scarce Focus on minimizing tax costs

Minimizing Deadweight Costs of Taxation is not a simple OT problem Tax bases should be as broad as possible p Tax rates should be as low as possible p Careful attention must be paid to taxes on production p BBLR vs. interventionist strategy? p

Fairness p Different ways to think about fairness n n n Horizontal and vertical equity Focus on single tax provision, single tax, or tax system as a whole Focus on government activity as a whole Tax incidence p Actual vs. perceived fairness – perceptions are reality in politics p

Costs of Redistribution through Taxation Trade-off of equity and efficiency p Costs of higher tax rates depends in part on the elasticity of wage supply – and on that of capital p Capital flight – into gray or black economy or out of the country p

Tax Policy and Tax Administration Tax policy + no administration = 0 p No policy + administration = ‘policy’ p Tax policy + administration = real policy p

Task of Tax Administration How much administration? – setting the budget: Lessons from history and experience? p How to administer? – organization (RA, LTO, etc. ) and strategy p How far to push it? – choices at the margin p

Benchmarking: The Concept Standards or norms: n Tax system performance n Tax structure n Tax administration structures n Tax administration resources n Tax administration IT systems

What is benchmarked, and how? Tax structure and performance p Organization p Legal framework p Enforcement p Collections p Systems and resources p

Example: Tax structure and performance p p p p p No. of taxes comprising 75% of total % of taxpayers providing 75% of total Tax ratio Indirect as % total No. of tax rates VAT collections as % total Administrative cost VAT productivity IT productivity

Example: Enforcement p p p Taxpayer current account Unbiased audit selection Auditors as % staff Use of external data Stop-filers as % active filers Crossing information among taxes No. of officials per 1000 population Active taxpayers per official Performance indicators for auditors % taxpayers subject to audit Unified audit

The Revenue Process Transformation Inputs Productivity Efficiency Systems Framework Management Environment

Uses and Limits of Benchmarking p Uses n n p To To reduce subjectivity of comparative exercises help detect and understand problem areas uncover information gaps help determine reform strategy Limitations n n n Must be collaboratively derived, not imposed Need to factor in critical environmental factors Inevitable bias towards quantifiable

What Have We Learned? Know the environment – economic, legal, ‘social capital’, p Keep it simple p Taxpayers as “clients” – the marketing problem of self-assessed systems p

Tax Administration Reform The will to do it – A Champion p Strategy – IT is not the answer (but it is usually part of it); nor are RAs p Matching the Task to Resources p Tax Architecture, Tax Engineering, and Tax Management p A Problem in Risk Management p

Facilitating Compliance Identification – finding taxpayers p Assessment – determining tax bases p Collection – getting the revenue p Service – too often forgotten but a critical investment p

What are Compliance Costs? Citizen’s costs of meeting tax obligations p Excludes actual taxes paid and excess burdens. p Includes avoidance (“tax planning”) and evasion costs. p Includes costs of taxpayers, non-filers, third parties (banks, tax withholders, helping others) p

Administration costs versus CCs Substitutes…usually p Other things equal, social cost considerations should dictate the choice between compliance requirements and administration responsibilities p n p EG: Official versus self-assessment Other things may not be equal… n n Documents enclosed with tax returns Desk versus field audits, etc.

International evidence: Business income taxes

Keeping Taxpayers Honest Know the problem – know your clients; estimate tax gaps p Monitor closely – registration, filing, payment, appeal p Enforce – penalties, dispute settlement p

Controlling Corruption Incentives – C=M +D – A: limit opportunities, raise opportunity costs (positive and negative) p Training – professionalism p Organization – performance evaluation, etc. p Monitoring – internal audit, etc. p

Taxes and Decentralization Increasingly important to focus on assigning taxing and spending authority to lower levels of government p Decentralization may improve government service by increasing accountability p Not a panacea, but a potentially important linkage fostering ‘trust’ p

Overview of Decentralization The what, why, and why not of decentralization p How to do it: a case study p Financing sub-national government p Some questions for discussion p

To Decentralize or Not to Decentralize? p. Is it really the question? p. Decentralization is seldom ‘chosen’ p. Perhaps it should be…the economics… p. But no one gives up power easily and that’s what it’s really about: who decides what?

Choosing decentralization? p p Some countries are born decentralized Some choose to become decentralized And some have decentralization thrust upon them – for many diverse reasons But no matter why a country is (to some degree) decentralized, it has to work out just what decentralization means and how to do it.

Modes of Decentralization Administrative decentralization – the centre decides, the regions and localities administer p Political decentralization – sub-national governments decide p Fiscal decentralization p n n Done right: how to make political decentralization efficient and effective Done wrong: how to make a mess of things – by decentralizing the wrong things or doing the right things badly

Potential Benefits p Efficiency gains n n p ‘Laboratory’ for innovation n n p p The right services to the right people in the right amounts Creating incentives for growth More heads are better than fewer Learning from success…and failure Revenue mobilization – broaden the base? Political aspects n n n Improve governance Restoring (or redressing) regional balance Helping to build (or rebuild, or hold together) a nation

Potential Costs p Macroeconomic concerns n n p Equity concerns n n p p p Runaway deficits Unsustainable borrowing More local revenues increase regional imbalance Is local control helpful or harmful to the poor? Efficiency and effectiveness – can LG really do the job? Capacity – can LG really do the job? Critical infrastructure from a national perspective Corruption – more …or less? Political concerns – exit and loyalty

Striking the Balance p p p Much discussion but little solid evidence Complex, multi-faceted issue Some general ‘lessons’ n n n p Hard budget constraint - accountability n n n p p p Make rules clear to all Finance follows function Need for financial control system Some local revenue flexibility Get intergovernmental transfers right Borrowing – keep an eye open for problems Asymmetry – the big, the small and those in-between Universal problems, local solutions Strategy, process (‘buy-in’), time…. .

How to Decentralize Make local government responsible for some appropriate services and some appropriate revenues – get the balance right p Make LG accountable to local people - and also to central government through good financial management system p Let LG decide priorities p

How to Do It Successfully Seize on local willingness to act p Build trust within LG and between LG and CG p At the same time build legitimacy and sustainability for system p Communicate, communicate p

Fiscal Decentralization: The basic questions Who should do what? p How should it be accounted for? p Who should pay? p Determining local revenue sources p Closing the ‘fiscal gap’ and designing intergovernmental transfers p What is role of borrowing? p

What taxes for SNG? p Common criteria n n n n p Usual results n n n p Revenue adequacy, buoyancy Correspondence principle, local accountability Administrative and compliance cost Latitude for corruption Political acceptability Distortionary impact Effects on regional disparities Equity User fees, property taxes (esp. residential) Business taxes? Sales and income taxes – not in most cases Conclusion – usually unimportant or transfer dependent

What powers should LG have? n n n To To To decide what taxes and charges to levy? decide what rates to impose? identify and assess taxes? bill and collect taxes? spend the proceeds freely?

Local Tax Administration p Is it necessary? Not for any economic purpose. What sub-national governments need are taxes for which they are economically and politically accountable – but this does not require that they necessarily administer such taxes. p Is it desirable? There may be some informational and accountability advantages. If others administer local taxes, will the money come to local government? p Is it feasible? But there may also be serious resource and political constraints on local capacity to administer many taxes well. Consider splitting the task? (e. g. assessment)

Improving local government accountability p Financial accounting –the essential base n n n p Monitoring – Error correction n n p Framework laws Training, pilot projects Budgeting, reporting, auditing Policy, analysis, audit, feedback Dealing with hard cases Transparency and democracy

Fiscal transfers Close the ‘fiscal gap’ p Equalize fiscal capacity and need p Adjust for spillovers p Increase leverage of central expenditures p Serve political ends p Key point is that transfers are instruments: it’s outcomes that matter p

Closing the Gap Change revenue and/or expenditure assignments p Control/restrain local spending p Enhance local fiscal effort p Any form of fiscal transfer? p

Equalization A matter of taste p Equalize governments, not people. If concern is poverty alleviation, transfers are not the way to go p Unconditional – let them spend as they wish? p Avoid ‘fiscal dentistry’ – capacity measure is the (seldom used) key p

Some Key Design Issues The ‘distributable pool’ p Formulas incorporating elements related to objectives p Objectives drive design p Nothing stays the same p Should everyone be treated the same? p

")

Borrowing for local capital investment sometimes makes sense…when it is possible (capital markets exist) and when bailouts are ruled out (so that HBC is in place). p Usually, however, neither of these provisos holds, so any borrowing needs to be carefully watched p

Back to the National Level. A Last Look at Tax Reform: The Key Questions What is to be done? p How is it to be done? p Who is to do it? p When is it to be done? p What will happen as a result? p

Lessons from Developed Countries Need for a Champion p Both Wrapping and Contents of Package Matter p Visible benefits essential p Adequate discussion – virtues and limitations (from tax reform perspective) of democracy p

Lessons from Developing Countries p p p p Timing, timing Simplify – don’t “complify” Sequencing and Scope Clarity (versus the political advantages of keeping tax matters in ‘decent obscurity’) Details matter Incrementalism Politics…always and everywhere There is No Such Thing as a ‘Politician-Proof Policy’: but should there be?

An Example: 30 Years of Reform in Colombia Gradualism p Duration p Education p Did it Matter? The Question of ‘Fiscal Equilibrium’ p

Conclusion The Optimist - ‘Taxes are the price we pay for civilized society’ p The Pessimist - ‘To tax and be loved is not possible’ p The Realist? -‘Above all, do no harm – or at least as little as possible’ p The Realistic Optimist – Focus on improving the knowledge base and capacity for countries to solve their own problems – NOSFA rules! p

fc9093a8cdb0d516bab9ef7e65c30d92.ppt