15f9a489b3db26ae1d79d7ba18b253f1.ppt

- Количество слайдов: 37

Retirement Financial Planning Annie’s Project February 6, 2007 Coweta Oklahoma

Critical questions to address n How do you envision retirement? q q n n n Where will retirees live? What will retirees do? Business? Hobbies? How much income will you need? What income sources will you have? What expectations do you have for the farm? q q Farm transferred slowly, or sold outright If transferring to next generation, will retiring generation still be involved?

Steps in planning n Anticipate your retirement lifestyle q q n Build a spending and investing plan q q n Gather data Establish goals Establish income needs Identify time lines for goals Estimate investment returns Factor in taxes or potential changes Control your assets as you near retirement

Anticipate your lifestyle…. “Too many of us are spending money we haven’t earned to buy things we don’t need to impress people we don’t like. ” H. Jackson Browne

Anticipate your lifestyle n n World travel, luxury hotels? Volunteer work? Hobbies? Support kids, grandkids?

Actual Sources of Retirement Income Source: Glennis Couchman

Evaluate your income sources n n n Spousal income Social Security Farm assets Work during retirement Pension plans Savings and investments

income starting in 2015 at")

Evaluate your income sources First year Social Security (SS) income starting in 2015 at age 65 (born in 1950) Salary in Year Before Retirement $30, 000 Wage Earner’s Monthly Benefit Wage Earner’s Annual Benefit $943 $11, 316 $40, 000 $1, 139 $13, 668 $50, 000 $1, 335 $16, 020 $60, 000 $1, 531 $18, 372

q q q Minimum age to")

Evaluate your income sources n Social Security (SS) q q q Minimum age to receive SS = 62 (80% of benefits) Age 65+ to get full SS benefits Retirement benefits increase each year retirement is delayed up to age 70 No reduction in SS benefits no matter how much you earn after age 65 Average monthly benefit paid to an individual retired worker is 804. Check your earnings record periodically: www. ssa. gov

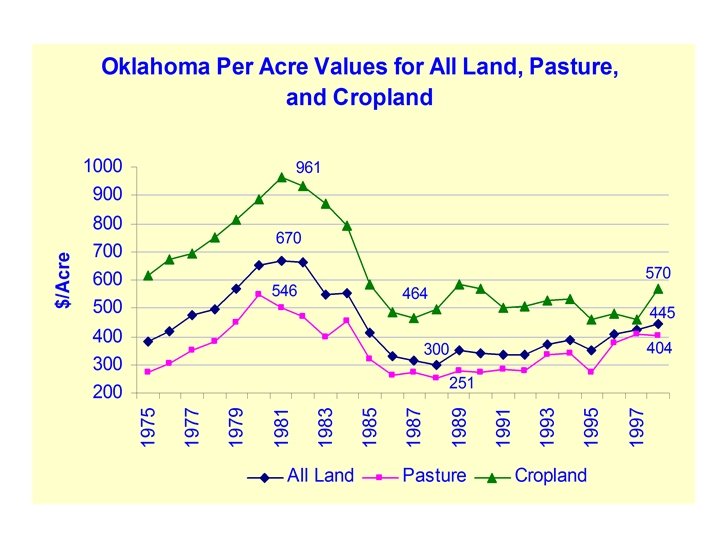

Evaluate your income sources n n Lease out farm assets q Land: $9 for native pasture, $13 for bermuda, $28 for cropland n CR-216, OK pasture rental rates and CR-230, OK cropland rental rates n F-214, Developing cash lease agreements for farmland F 215, Developing share lease agreements for farmland q Need $25, 000 in cash income? n 2, 778 acres of native pasture, or n 1, 923 acres of bermuda, or n 893 acres of cropland q Livestock n WF-571, Breeding livestock lease agreements and WF-572, Stocker lease agreements q Machinery and equipment Consult with your tax advisor

Evaluate your income sources n Sale of land, breeding livestock, machinery and equipment q q q Tax basis – Purchased, inherited, or gifted Market value Taxable income n n n Ordinary income (depreciation recapture) Capital gain (sale price in excess of purchase price) Consult with your tax advisor

How much retirement value in the million dollar farm? n n n Farm would sell for $1, 000 but selling costs might approach $100, 000 = net sale price of $900, 000? Taxable gain = ? Capital gain tax rate of 5% or 15%? Is there debt? Equity to retire on?

Evaluate your income sources n Work during retirement q Social Security earnings limits n n q Some limits if retiring early Age 65+, no limit on earnings Enhance benefits by filling in zero years

Evaluate your income sources n Pension plans q Payment options n n q q q Single life Joint and survivor Term certain Lump sum Cash flow Taxes Survivor benefits and beneficiaries

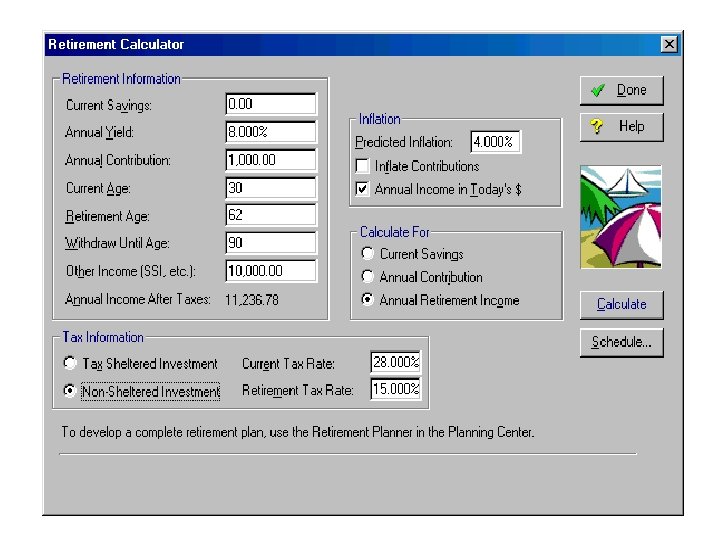

Evaluate your income sources n Savings and investments q Taxable accounts and investments n n n q Employer sponsored plans n n q q Savings accounts CDs Bonds Stocks Mutual funds 401(k)s, 403(b)s and profit-sharing plans Must begin to withdraw funds by age 70 ½ from certain tax advantaged retirement plans or face penalty IRAs Annuities and other insurance contracts Don’t expect to get rich quick!

Savings Needed for Retirement Quicken Financial Planner assumptions: retire now at age 62, assets are owned free and clear, overall retirement tax rate of 15%, withdrawals until age 85, inflation = 3% Investment Rate of return 3% $300, 000 $600, 000 $900, 000 $12, 425 $24, 850 $37, 275 5% $14, 847 $29, 693 $44, 540 7% $17, 486 $34, 973 $52, 459

Build a realistic investing plan 73 year average annual return: 1926 -1999 Source: The Vanguard Group

Evaluate your income sources n Add it up q q q n Spousal income Social Security Sale/lease of farm assets Work during retirement Pension plans Savings and investments How diversified are you?

How to increase retirement income? n n n Retire later Work during retirement Set aside more Diversify your retirement portfolio Take advantage of IRAs Tap the equity in your home and land

Build a realistic spending plan n n n n Family living needs Farm expenses (cash and capital investment) Life expectancy and age of retirement Health insurance Long term care insurance Life insurance Taxes Emergency funds Inflation

Build a realistic spending plan n Family living needs q q n Housing, food, clothing, health, taxes, insurance, transportation, education, childcare/eldercare, charitable contributions, organizations Capital expenses (home improvements, vehicle replacement) Loan repayment Leisure, recreation, entertainment, luxuries Worksheet

Family Living Expenses Source: KS Farm Business Management Association, 2005

Family Living Expenses Source: KS Farm Business Management Association, 2005

Cash Needs Over Time?

Build a realistic spending plan n Farm expenses q q q Three year trend worksheet IFFS IFMAPS Enterprise budget software Quicken for farm financial records

Build a realistic spending plan n Plan to beat the averages At age… You should plan to live another… Females Males 45 46 years 43 years 50 41 38 55 36 32 60 31 27 65 27 22

Build a realistic spending plan n Health, disability, long term care insurance, life insurance q q Nursing home costs $50 -70, 000/year on average nationally. Have to pay in 40 quarters to get disability

Build a realistic spending plan Spendable income needed during retirement to buy what $10, 000 buys at the start of retirement No. of years after the start of retirement Inflation rate 2% 4% 6% 5 11, 041 12, 167 13, 382 10 12, 190 14, 802 17, 908 15 13, 459 18, 009 23, 966 20 14, 859 21, 911 32, 071 25 16, 406 26, 658 42, 919 Source: Planning Ahead for Retirement, TIAA-CREF

The realistic spending plan n n n n Family living needs Farm expenses Life expectancy and age of retirement Health insurance Long term care insurance Life insurance Inflation Tax considerations Emergency funds needed

Manage your assets as you near retirement n n Start learning now about your alternatives Using your investments during retirement q q n n Use dividends and interest, shift to other investments, use principal balances Short-term reserves, taxable accounts, tax-exempt accounts, tax-deferred investments Make your investments last Change your investments?

Close to Retirement? n n n How much income will you need in retirement? How do you plan to dispose of farm assets? How will you invest the proceeds? What will you do with your time? Have you discussed your plan with others that it will impact? Consult with an accountant and lawyer….

Steps in planning n n n Anticipate your retirement lifestyle Evaluate your income sources Create realistic spending and investing plans Control your assets as you near retirement Review, update your estate plan

Cracks in the Nest Egg n Planning too late q q n Miscalculating how much is enough q q q n Failing to take advantage of the years immediately before retirement Ignoring employer sponsored plans Failing to consider long-term care needs Failing to consider the effects of inflation and taxes Underestimating life expectancy Underestimating expenses in retirement Investing too conservatively Failing to protect your assets q q q Making large loans to family and friends Over-managing a retirement portfolio Taking too much risk with investments Wall Street Journal, Oct. 22, 2001

Financial Planning Tools n n n n Quicken: www. quicken. com The Motley Fool: http: //www. fool. com/ American Savings Education Council: http: //www. asec. org/ Smart Money: http: //www. smartmoney. com/ Fidelity Investments: http: //www. fidelity. com Vanguard Group: http: //www. vanguard. com TIAA-CREF: http: //tiaa-cref. org/

15f9a489b3db26ae1d79d7ba18b253f1.ppt