2e95cb8ffd2c6021d3effb8b20dae1be.ppt

- Количество слайдов: 30

Results of the Ester Project in Latvia Valdis Avotins, LIDA Salamanca Joint Workshop, June 23, 2005

Results of the Ester Project in Latvia Valdis Avotins, LIDA Salamanca Joint Workshop, June 23, 2005

Agenda • • NIP Need: Market failure Risk capital program Technology incubator & seed program • Questions

Agenda • • NIP Need: Market failure Risk capital program Technology incubator & seed program • Questions

Goals of the innovation strategy RIS Latvia

Goals of the innovation strategy RIS Latvia

22 experts’ evaluation Research Innovation Assistant Prototype infrastructure Risk EMP Tech Incubator, Capital FF Co. E liaison offices, seed IPR

22 experts’ evaluation Research Innovation Assistant Prototype infrastructure Risk EMP Tech Incubator, Capital FF Co. E liaison offices, seed IPR

Existing/ approved initialised Launch expected Planning in 2006/7 Entrepreneurshi p promotion OTHER SUPPORT TTO BUSINESS SUPPORT TFM scheme Market exposure MARKET INTELLIGENCE IPR protection in start-ups NEW PRODUCTS TECHNOLOGICAL INCUBATION START-UP SCHEME FINANCING SEED SCHEME Ideas Validation Prototyping VENTURE CAPITAL SAP Fast growth

Existing/ approved initialised Launch expected Planning in 2006/7 Entrepreneurshi p promotion OTHER SUPPORT TTO BUSINESS SUPPORT TFM scheme Market exposure MARKET INTELLIGENCE IPR protection in start-ups NEW PRODUCTS TECHNOLOGICAL INCUBATION START-UP SCHEME FINANCING SEED SCHEME Ideas Validation Prototyping VENTURE CAPITAL SAP Fast growth

Good investment environment • Rapid GDP growth 2000 2001 2002 2003 2004 6. 9 8 6. 4 7. 5 8. 5 • “Latvia is ranked among the top ten counties worldwide in terms of business start up time and length of bankruptcy procedures. ” Doing Business in 2004, World Bank • Wall Street Journal Index of Economic Freedom • Rank 28, Score 2. 31, (Israel Rank 33, score 2. 36) • The overall tax burden of GDP is only 29. 1%

Good investment environment • Rapid GDP growth 2000 2001 2002 2003 2004 6. 9 8 6. 4 7. 5 8. 5 • “Latvia is ranked among the top ten counties worldwide in terms of business start up time and length of bankruptcy procedures. ” Doing Business in 2004, World Bank • Wall Street Journal Index of Economic Freedom • Rank 28, Score 2. 31, (Israel Rank 33, score 2. 36) • The overall tax burden of GDP is only 29. 1%

Background conditions • Low general entrepreneurship activity – Lowest amount of SME’s in EU (18 on 1000 inhabitants; EU average 51/1000) • Low share of innovative enterprises – 20% (incl. adoption) compared to EU average of 45% – Share of high-tech products in export ~6% – Employment in mid-to-high-tech is 23% of EU average • Lack of appropriate financial instruments for the needs of high-tech/ innovative companies at early stage of their development

Background conditions • Low general entrepreneurship activity – Lowest amount of SME’s in EU (18 on 1000 inhabitants; EU average 51/1000) • Low share of innovative enterprises – 20% (incl. adoption) compared to EU average of 45% – Share of high-tech products in export ~6% – Employment in mid-to-high-tech is 23% of EU average • Lack of appropriate financial instruments for the needs of high-tech/ innovative companies at early stage of their development

3500 3000 2500 exports 2000 ($millions) 1500 1000") Jaffa Oranges vs. Software (1992 -2001) 3500 3000 2500 exports 2000 ($millions) 1500 1000 500 19 92 19 93 19 94 19 95 19 96 19 97 19 98 19 99 20 00 20 01 0 Dr. Eli Opper, Chief Scientist Software Citrus

Jaffa Oranges vs. Software (1992 -2001) 3500 3000 2500 exports 2000 ($millions) 1500 1000 500 19 92 19 93 19 94 19 95 19 96 19 97 19 98 19 99 20 00 20 01 0 Dr. Eli Opper, Chief Scientist Software Citrus

A. RISK CAPITAL SCHEME Reasonable investments in LVL 0. . . 10, 000. . . 25, 000. . . 50, 000. . . 100, 000. . . 250, 000. . . 500, 000. . . 1 m. . . 2. 5 m. . . NLBDF 33 projects 1995 – 2004 BSEF, BALTCAP, NCH, BALEF 34 projects First risk Capital investment 67 projects financed via Risk Capital No Start-up investments No Seed money

A. RISK CAPITAL SCHEME Reasonable investments in LVL 0. . . 10, 000. . . 25, 000. . . 50, 000. . . 100, 000. . . 250, 000. . . 500, 000. . . 1 m. . . 2. 5 m. . . NLBDF 33 projects 1995 – 2004 BSEF, BALTCAP, NCH, BALEF 34 projects First risk Capital investment 67 projects financed via Risk Capital No Start-up investments No Seed money

Sources for Deal flow • Heritage from USSR at the end of 90`s • 30. 000 academic scientists • 13. 000 engineers involved in R&D • Large brain gain opportunities • Higher education institutions Institutions No of students • Infrastructure 2001 36 110. 500 2002 37 118. 944 • 6 R&D Centers of excellence • 20 Technology and industrial parks • EU grants 2003 49 127. 656

Sources for Deal flow • Heritage from USSR at the end of 90`s • 30. 000 academic scientists • 13. 000 engineers involved in R&D • Large brain gain opportunities • Higher education institutions Institutions No of students • Infrastructure 2001 36 110. 500 2002 37 118. 944 • 6 R&D Centers of excellence • 20 Technology and industrial parks • EU grants 2003 49 127. 656

Program’s objectives • Facilitate entrepreneurship promoting access to risk capital financing • Facilitate the establishment and development of new venture capital funds, motivate them invest in SME`s by offering state aid to private investors • Attract private investors to invest in Latvia Risk Capital in Latvia 11

Program’s objectives • Facilitate entrepreneurship promoting access to risk capital financing • Facilitate the establishment and development of new venture capital funds, motivate them invest in SME`s by offering state aid to private investors • Attract private investors to invest in Latvia Risk Capital in Latvia 11

") How? • Public Private Partnership – Budget 14. 5 m € (75% from ERDF) – Public investment in a Fund – Up to 70% (target 50/50) – No more than 5. 5 m € in the single Fund • State Support to Private Investors

How? • Public Private Partnership – Budget 14. 5 m € (75% from ERDF) – Public investment in a Fund – Up to 70% (target 50/50) – No more than 5. 5 m € in the single Fund • State Support to Private Investors

Founding of VC Fund of Funds Private Investors Limited by 70% or 5, 7 million € At least 30% of total investment in new VC fund Target : 50/50 Investment Fund ~ 8. . . 10 million € 3 new funds

Founding of VC Fund of Funds Private Investors Limited by 70% or 5, 7 million € At least 30% of total investment in new VC fund Target : 50/50 Investment Fund ~ 8. . . 10 million € 3 new funds

Investment Fund • Partnerships with life cycle for 7 to 10 years • Managed by private management company • Business decisions made by private investors • State support to private investors

Investment Fund • Partnerships with life cycle for 7 to 10 years • Managed by private management company • Business decisions made by private investors • State support to private investors

Selection of Fund Managers Open tender procedure, main criteria: • Experience and professionalism of team members • Business plan • Involved private investors and amount of private funds

Selection of Fund Managers Open tender procedure, main criteria: • Experience and professionalism of team members • Business plan • Involved private investors and amount of private funds

Venture Capital") Decision-making procedure Investment committee (representatives of all investors, one member from FF) Venture Capital Fund ~ 8. . . 10 million € SME 1 SME 2 • • • SME 10 -15

Decision-making procedure Investment committee (representatives of all investors, one member from FF) Venture Capital Fund ~ 8. . . 10 million € SME 1 SME 2 • • • SME 10 -15

Restrictions for investment • SMEs registered in Latvia • Maximum investment 1 m € in one project • Maximum 300 k € in the first investment tranche • Time between trenches at least 12 months • Some sector restrictions (EU regulations)

Restrictions for investment • SMEs registered in Latvia • Maximum investment 1 m € in one project • Maximum 300 k € in the first investment tranche • Time between trenches at least 12 months • Some sector restrictions (EU regulations)

Return Distribution Mechanism 1. 2. 3. 4. Fund’s management expenses; Repay the original capital invested by private investors; Repay 25% of the original capital invested by the state; Priority return (hurdle rate) on private investors’ capital (6%); 5. Repay the remaining 75% of the state’s invested capital; 6. Hurdle rate return (6%) on the state’s invested capital; 7. Remaining profit, if any to private investors and FMC

Return Distribution Mechanism 1. 2. 3. 4. Fund’s management expenses; Repay the original capital invested by private investors; Repay 25% of the original capital invested by the state; Priority return (hurdle rate) on private investors’ capital (6%); 5. Repay the remaining 75% of the state’s invested capital; 6. Hurdle rate return (6%) on the state’s invested capital; 7. Remaining profit, if any to private investors and FMC

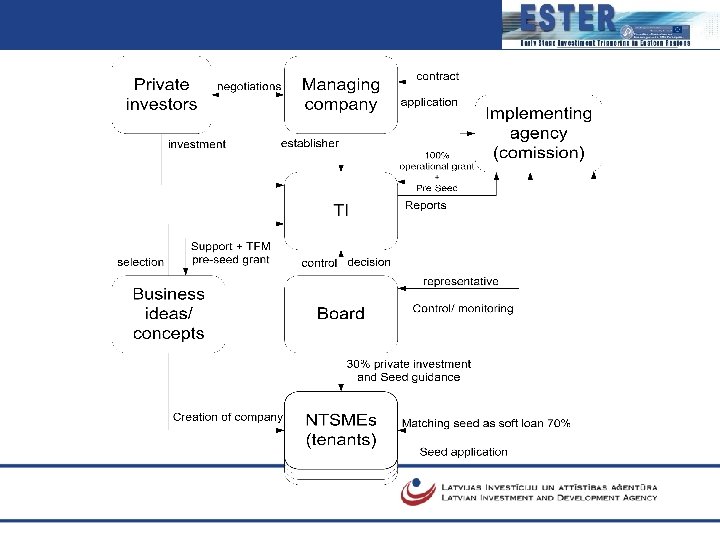

B. The designeddraft Growth Future Scheme 4 1. Technology incubator grant 2. Pre-seed grant – Think for month 3. Seed soft loan Management companies or Operators of TI’s – private companies providing space & infrastructure, management and S&M advice, basic business services and private investment structuring in exchange for equity position in the tenant company Target groups: – Potential entrepreneurs from industry – Potential entrepreneurs from academia – Repatriating scientists and R&D personnel – Regional inventors Tested in Israel, with WB experts, EU experts, local expert panels

B. The designeddraft Growth Future Scheme 4 1. Technology incubator grant 2. Pre-seed grant – Think for month 3. Seed soft loan Management companies or Operators of TI’s – private companies providing space & infrastructure, management and S&M advice, basic business services and private investment structuring in exchange for equity position in the tenant company Target groups: – Potential entrepreneurs from industry – Potential entrepreneurs from academia – Repatriating scientists and R&D personnel – Regional inventors Tested in Israel, with WB experts, EU experts, local expert panels

New forms of Business Incubation in late 1990 s has been driven to multiply the number of succesful, fast-growth, high technology businesses in US a) Its led by serial entrepreneur; b) it has its own seed fund drawn from founder’s own, VCF or corporate partner’s capital; c) it may have specific sector focus Conventional incubators offer “heat, light and dial tone”, but “Smart” Venture Investment claim to offer more, developing ideas and incubating them in-house as well as providing late seed capital and A, B and C round investment. Incubation today is seen as a way in which capital can be efficiently applied to support new technology businesses Gill D. , Martin C. , Minshall T. , Rigby M. Funding Technology. Lessons from America. 2000

New forms of Business Incubation in late 1990 s has been driven to multiply the number of succesful, fast-growth, high technology businesses in US a) Its led by serial entrepreneur; b) it has its own seed fund drawn from founder’s own, VCF or corporate partner’s capital; c) it may have specific sector focus Conventional incubators offer “heat, light and dial tone”, but “Smart” Venture Investment claim to offer more, developing ideas and incubating them in-house as well as providing late seed capital and A, B and C round investment. Incubation today is seen as a way in which capital can be efficiently applied to support new technology businesses Gill D. , Martin C. , Minshall T. , Rigby M. Funding Technology. Lessons from America. 2000

Political Goals 1. 2. 3. 4. Improve the competitiveness of Latvia by facilitating development of high & medium tech industries; Create a potential for participation in future technologies (prestige, future competitiveness); Development of new sustainable export industries (Israeli & Finnish experience); Create economic champions / change the attitude of society towards technology commercialization. High growth high-tech company establishment is more expensive and it shows remarkable return after 8 -10 years : § longer establishment cycle; § specific infrastructure required; § specific knowledge needed.

Political Goals 1. 2. 3. 4. Improve the competitiveness of Latvia by facilitating development of high & medium tech industries; Create a potential for participation in future technologies (prestige, future competitiveness); Development of new sustainable export industries (Israeli & Finnish experience); Create economic champions / change the attitude of society towards technology commercialization. High growth high-tech company establishment is more expensive and it shows remarkable return after 8 -10 years : § longer establishment cycle; § specific infrastructure required; § specific knowledge needed.

Background Existing market gap for early stage investment and low local entrepreneurial spirit results in few investments particularly in high growth Start-ups The Need: sharing investor risk to encourage investments and increase the number of high growth start-up companies Solution: outsourced integrated service to motivated professional venture teams

Background Existing market gap for early stage investment and low local entrepreneurial spirit results in few investments particularly in high growth Start-ups The Need: sharing investor risk to encourage investments and increase the number of high growth start-up companies Solution: outsourced integrated service to motivated professional venture teams

Side measures for Deal flow • Entrepreneurship motivation scheme - outflow of 300 busines ideas, 100 marketing plans, 50 business plans; • Reposition of entrepreneurial culture : • by informative seminars, work shops, presentations, publications in media, etc; • Awareness creation program; • “Think for month” (pre-seed grant); • Innovation assistant grant scheme; • motivation scheme for inventors in universities and R&D institutes; • Innovation courses and innovation MBA program in RTU; • Technology transfer centre; • Business labs and Liaison offices in universities; • Ventspils school of entrepreneurship (Chalmers model)

Side measures for Deal flow • Entrepreneurship motivation scheme - outflow of 300 busines ideas, 100 marketing plans, 50 business plans; • Reposition of entrepreneurial culture : • by informative seminars, work shops, presentations, publications in media, etc; • Awareness creation program; • “Think for month” (pre-seed grant); • Innovation assistant grant scheme; • motivation scheme for inventors in universities and R&D institutes; • Innovation courses and innovation MBA program in RTU; • Technology transfer centre; • Business labs and Liaison offices in universities; • Ventspils school of entrepreneurship (Chalmers model)

") 1. Technology Incubator grant • • 9 year program (3 x 3 support periods) Public – private partnership model Decisions made by TI private operators (PO) Grant is paid to TI operator as 30% fixed rate and 35 k. EUR per one tenant, minimum 2 tenants are required, quarterly payments • Public grant up to 75% (max. 500 k EUR) of TI’s annual budget • Based on Venture business not traditional incubation!

1. Technology Incubator grant • • 9 year program (3 x 3 support periods) Public – private partnership model Decisions made by TI private operators (PO) Grant is paid to TI operator as 30% fixed rate and 35 k. EUR per one tenant, minimum 2 tenants are required, quarterly payments • Public grant up to 75% (max. 500 k EUR) of TI’s annual budget • Based on Venture business not traditional incubation!

2. Pre-seed: TFM • to validate a business plans before starting a new company and to leverage private equity finance in later stages • An individual person with a business project entailing fast growth (turnover increase to at least 40 -50% per year) for 0 24 months • Financing covers up to 100% of eligible costs, 1 month Form of intervention Performance based grants up to 3 k. Euro

2. Pre-seed: TFM • to validate a business plans before starting a new company and to leverage private equity finance in later stages • An individual person with a business project entailing fast growth (turnover increase to at least 40 -50% per year) for 0 24 months • Financing covers up to 100% of eligible costs, 1 month Form of intervention Performance based grants up to 3 k. Euro

3. The seed program • • • Investment management: TI PO Recipients – young (<6 month) SMEs after business concept validation max 300 K EUR soft loan, matching with private equity investment 70%: 30% converts to non-refundable grant in the case of failure Project duration 6 -24 months when sales appear 5% from annual turnover should be paid back until all loan is repaid

3. The seed program • • • Investment management: TI PO Recipients – young (<6 month) SMEs after business concept validation max 300 K EUR soft loan, matching with private equity investment 70%: 30% converts to non-refundable grant in the case of failure Project duration 6 -24 months when sales appear 5% from annual turnover should be paid back until all loan is repaid

Return: • Number of incubators and their capacity utilized • Number of newly created technological companies • Number of companies graduating from TI • Number of successful IPOs, M&As, investments in the next rounds • Total private investment attracted to the companies

Return: • Number of incubators and their capacity utilized • Number of newly created technological companies • Number of companies graduating from TI • Number of successful IPOs, M&As, investments in the next rounds • Total private investment attracted to the companies

Selection criteria 1. For TIs operators 2. For SMEs • • • TI management experience and professionalism of team members in new high growth SMEs creation Business plan Amount of offered financing Planned running costs per SME, share of private coinvestment • • • Registrated commercial entity in LR, younger than 6 months, planned growth over 50% Not yet in market, IPR owner or exclusive user High- or medium-tech Explicit orientation towards global market (export) Worked out draft business or / and technology plan Manageable company Significant milestones for 24 months

Selection criteria 1. For TIs operators 2. For SMEs • • • TI management experience and professionalism of team members in new high growth SMEs creation Business plan Amount of offered financing Planned running costs per SME, share of private coinvestment • • • Registrated commercial entity in LR, younger than 6 months, planned growth over 50% Not yet in market, IPR owner or exclusive user High- or medium-tech Explicit orientation towards global market (export) Worked out draft business or / and technology plan Manageable company Significant milestones for 24 months

Thank you for attention!

Thank you for attention!