ed7eb176fcf4818101f5cb0c52f3bcb8.ppt

- Количество слайдов: 61

Regression with a Binary Dependent Variable

Linear Probability Model p Probit and Logit Regression p n n p Probit Model Logit Regression Estimation and Inference n n n Nonlinear Least Squares Maximum Likelihood Marginal Effect Application p Misspecification p

has been continuous: n n district-wide average")

p So far the dependent variable (Y) has been continuous: n n district-wide average test score traffic fatality rate What if Y is binary? p Y = get into college; X= father’s years of education p Y = person smokes, or not; X = income p Y = mortgage application is accepted, or not; X=income, house characeteristics, marital status, race.

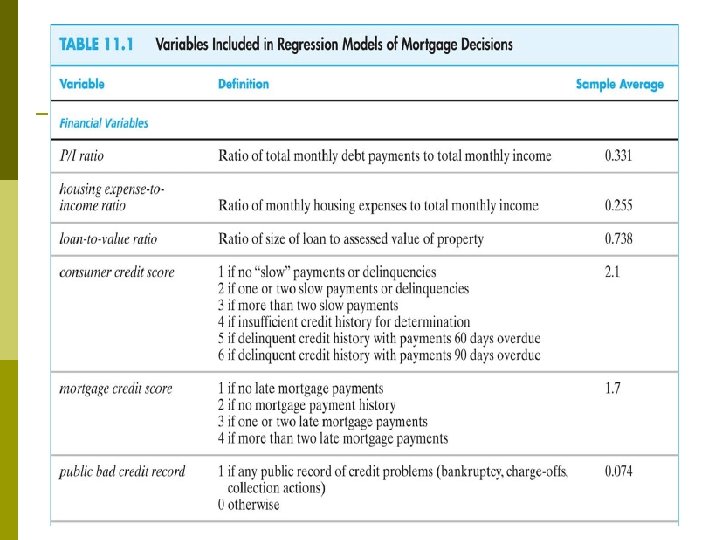

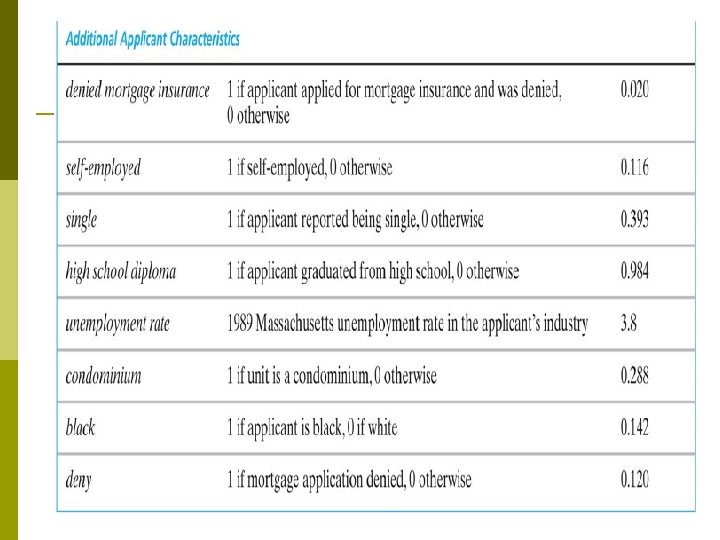

Example: Mortgage denial and race The Boston Fed HMDA data set p Individual applications for single-family mortgages made in 1990 in the greater Boston area. p 2380 observations, collected under Home Mortgage Disclosure Act (HMDA). Variables p Dependent variable: n p Is the mortgage denied or accepted? Independent variables: n n n income, wealth, employment status other loan, property characteristics race of applicant

The Linear Probability Model p A natural starting point is the linear regression model with a single regressor: But, p What does mean when Y is binary? Is ? p What does the line mean when Y is binary? p What does the predicted value mean when Y is binary? For example, what does = 0. 26 mean?

= 0, so When Y is binary, so")

Recall assumption #1: E(ui |Xi ) = 0, so When Y is binary, so

When Y is binary, the linear regression model, is called the linear probability model. p The predicted value is a probability: n n p = probability that Y=1 given x. = the predicted probability that Yi = 1, given X. = change in probability that Y = 1 for a given x:

Example: linear probability model, HMDA data Mortgage denial v. ratio of debt payments to income (P/I ratio) in the HMDA data set

Linear probability model: HMDA data p What is the predicted value for P/I ratio =. 3? p Calculating “effects”: increase P/I ratio from. 3 to. 4: p The effect on the probability of denial of an increase in P/I ratio from. 3 to. 4 is to increase the probability by. 061, that is, by 6. 1 percentage points.

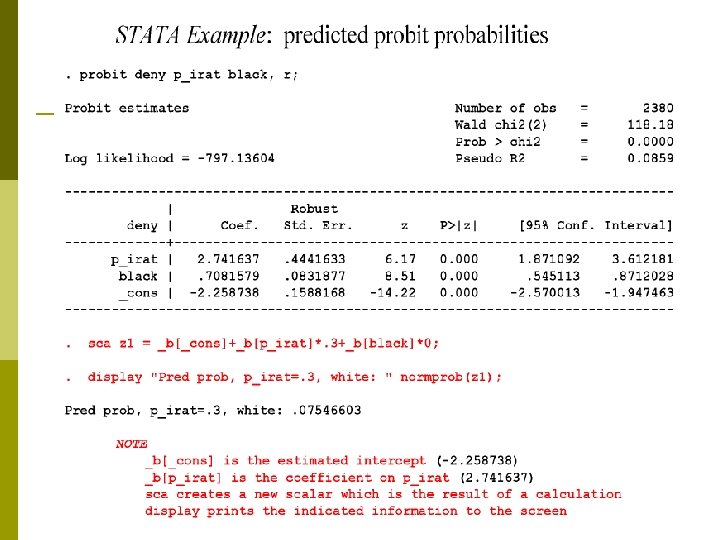

Next include black as a regressor: Predicted probability of denial: p for black applicant with P/I ratio =. 3: p p for white applicant with P/I ratio =. 3: difference =. 177 = 17. 7 percentage points. p Coefficient on black is significant at the 5% level. p

The linear probability model: Summary Models probability as a linear function of X. p Advantages: p n n p Disadvantages: n n p simple to estimate and to interpret inference is the same as for multiple regression (need heteroskedasticity-robust standard errors) Does it make sense that the probability should be linear in X? Predicted probabilities can be < 0 or > 1! These disadvantages can be solved by using a nonlinear probability model: probit and logit regression.

Probit and Logit Regression The problem with the linear probability model is that it models the probability of Y = 1 as being linear: Instead, we want: p 0 ≤ Pr(Y = 1|X) ≤ 1 for all X. p Pr(Y = 1|X) to be increasing in X (for > 0). This requires a nonlinear functional form for the probability. How about an “S-curve”.

≤ 1")

The probit model satisfies these conditions: p 0 ≤ Pr(Y = 1|X) ≤ 1 for all X. p Pr(Y = 1|X) to be increasing in X (for > 0).

Probit regression models the probability that Y=1 using the cumulative standard normal distribution function, evaluated at Φ is the cumulative normal distribution function. p is the “z-value” or “z-index” of the probit model. Example: Suppose , so p p Pr(Y = 1|X =. 4) = area under the standard normal density to left of z = -. 8, which is

=. 2119")

Pr(Z ≤-0. 8) =. 2119

Why use the cumulative normal probability distribution? The “S-shape” gives us what we want: p 0 ≤ Pr(Y = 1|X) ≤ 1 for all X. p Pr(Y = 1|X) to be increasing in X (for > 0). p Easy to use - the probabilities are tabulated in the cumulative normal tables. p Relatively straightforward interpretation: p n n n z-value = is the predicted z-value, given X is the change in the z-value for a unit change in X

Another way to see the probit model is through the interpretation of a latent variable. p Suppose there exists a latent variable , p where is unobserved. p The observed Y is 1 if , and is 0 if < 0. Note that implies homoscedasticity. p

In other words, Similarly,

Furthermore, since we only can estimate and , not 0 , and separately. It is assumed that = 1. Therefore,

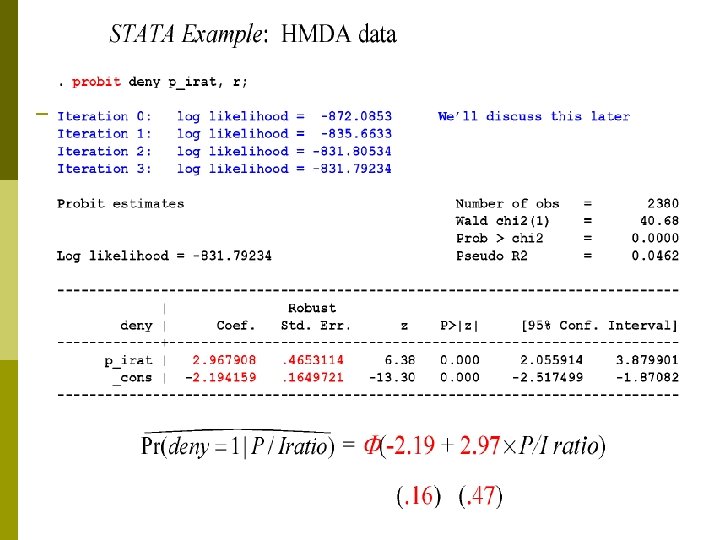

STATA Example: HMDA data, ctd. Positive coefficient: does this make sense? p Standard errors have usual interpretation. p Predicted probabilities: p p Effect of change in P/I ratio from. 3 to. 4: Pr(deny = =. 4) =. 159 Predicted probability of denial rises from. 097 to. 159.

Probit regression with multiple regressors Φ is the cumulative normal distribution function. p is the “z-value” or “z-index” of the probit model. p is the effect on the z-score of a unit change in X 1, holding constant X 2. p

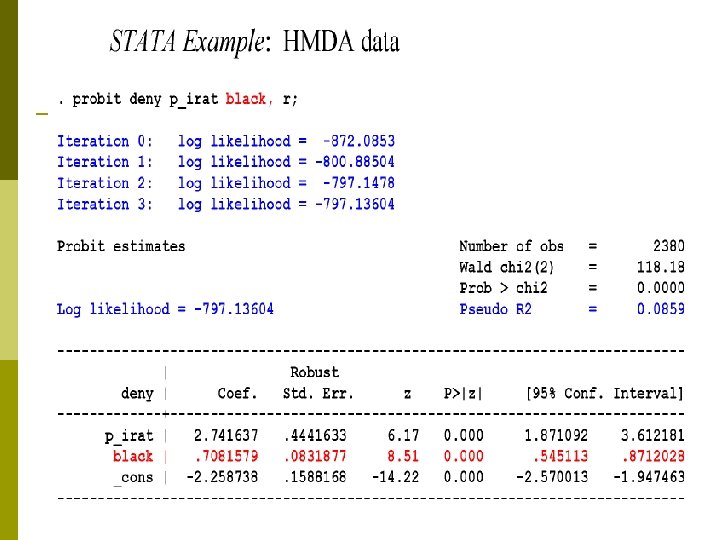

STATA Example: HMDA data, ctd. Is the coefficient on black statistically significant? p Estimated effect of race for P/I ratio =. 3: p p Difference in rejection probabilities =. 158 (15. 8 percentage points)

Logit regression models the probability of Y = 1 as the cumulative standard logistic distribution function, evaluated at F is the cumulative logistic distribution function:

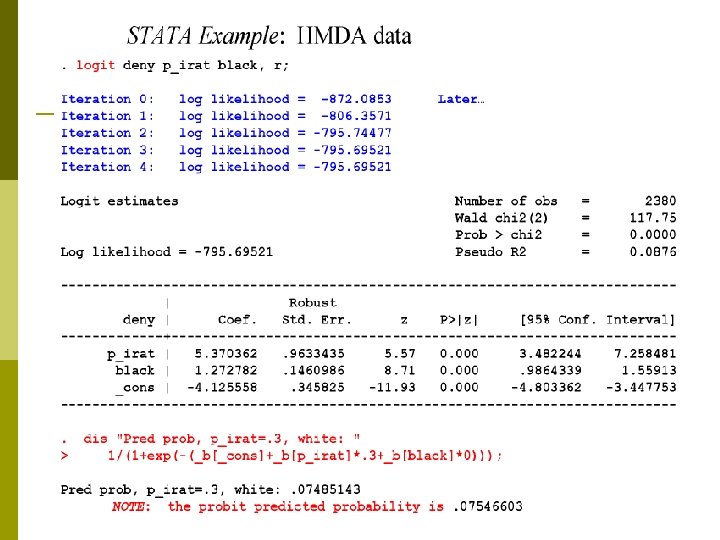

where Example: Why bother with logit if we have probit? p Historically, logit is more convenient to compute. p In practice, very similar to probit.

Predicted probabilities from estimated probit and logit models usually are very close.

Estimation and Inference p Probit model: p Estimation and inference n n n How to estimate and ? What is the sampling distribution of the estimators? Why can we use the usual methods of inference? First discuss nonlinear least squares (easier to explain). p Then discuss maximum likelihood estimation (what is actually done in practice). p

Probit estimation by nonlinear least squares Recall OLS: The result is the OLS estimators and. In probit, we have a different regression function - the nonlinear probit model. So, we could estimate and by nonlinear least squares: p p Solving this yields the nonlinear least squares estimator of the probit coefficients.

How to solve this minimization problem? p Calculus doesn’t give and explicit solution. p Must be solved numerically using the computer, e. g. by “trial and error” method of trying one set of values for O , then trying another, and another, . . . p Better idea: use specialized minimization algorithms. In practice, nonlinear least squares isn’t used because it isn’t efficient - an estimator with a smaller variance is. . .

Probit estimation by maximum likelihood The likelihood function is the conditional density of Y 1, … , Yn given X 1, … , Xn, treated as a function of the unknown parameters and. p The maximum likelihood estimator (MLE) is the value of ( , ) that maximize the likelihood function. p The MLE is the value of ( , ) that best describe the full distribution of the data. p In large samples, the MLE is: n n n consistent. normally distributed. efficient (has the smallest variance of all estimators).

Special case: the probit MLE with no X Y = 1 with probability p, =0 with probability (1 -p) (Bernoulli distribution) Data: Y 1, … , Yn, i. i. d. Derivation of the likelihood starts with the density of Y 1: so

: Because Y 1 and Y 2 are")

Joint density of (Y 1, Y 2): Because Y 1 and Y 2 are independent, Joint density of (Y 1, … , Yn):

The likelihood is the joint density, treated as a function of the unknown parameters, which is p, p The MLE maximizes the likelihood. It is standard to work with the log likelihood, ln f (p; Y 1, … , Yn):

Solving for p yields the MLE. That is, satisfies,

: For Yi i. i. d. Bernoulli,")

The MLE in the “no-X” case (Bernoulli distribution): For Yi i. i. d. Bernoulli, the MLE is the “natural” estimator of p, the fraction of 1’s, which is YN. p We already know the essentials of inference: p n n p In large n, the sampling distribution of = is normally distributed. Thus inference is “as usual”: hypothesis testing via t-statistic, confidence interval as ± 1. 96 SE. STATA note: to emphasize requirement of large-n, the printout calls the t-statistic the z-statistic.

The probit likelihood with one X The derivation starts with the density of Y 1, given X 1:

p The probit likelihood function is the joint density of Y 1, … , Yn given X 1, … , Xn, treated as a function of ,

The probit likelihood function: Can’t solve for the maximum explicitly. p Must maximize using numerical methods. p As in the case of no X, in large samples: p n n p are consistent. are normally distributed. Their standard errors can be computed. Testing, confidence intervals proceeds as usual. For multiple X’s, see SW App. 11. 2.

The logit likelihood with one X The only difference between probit and logit is the functional form used for the probability: Φ is replaced by the cumulative logistic function. p Otherwise, the likelihood is similar; for details see SW App. 11. 2. p As with probit, p n n are consistent. are normally distributed. Their standard errors can be computed. Testing, confidence intervals proceeds as usual.

. So, two other")

Measures of fit The and don’t make sense here (why? ). So, two other specialized measures are used: p The fraction correctly predicted = fraction of Y ’s for which predicted probability is >50% (if Yi = 1) or is <50% (if Yi = 0). p The pseudo-R 2 measure the fit using the likelihood function: measures the improvement in the value of the log likelihood, relative to having no X’s (see SW App. 9. 2). This simplifies to the R 2 in the linear model with normally distributed errors.

Marginal Effect However, what we really care is not itself. We want to know how the change of X will affect the probability that Y = 1. For the probit model, where is pdf of the standard normal distribution.

depends on the")

The effect of the change in X on Pr(Y = 1|X) depends on the value of X. In practice, we usually evalute the marginal effect at the sample average. i. e. The marginal effect is

When X is binary, it is not clear what does the sample average mean. The marginal effect then measures the probability difference between X = 1 and X = 0. In STATA, the command dprobit reports the marginal effect, instead of

are an essential part of")

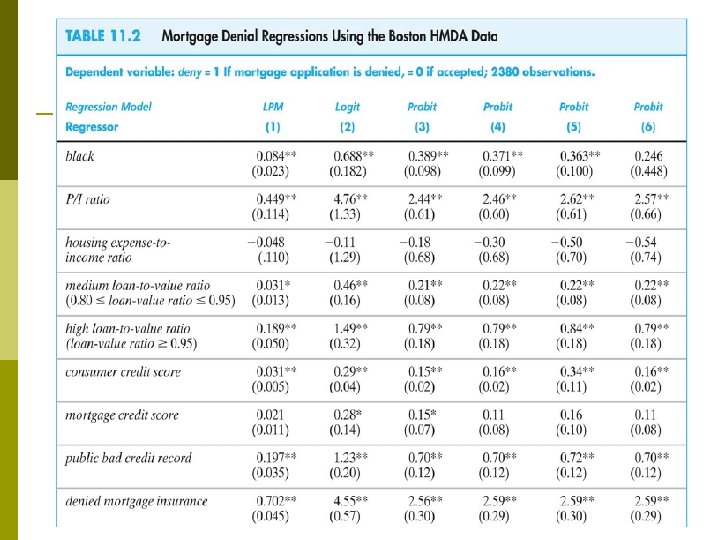

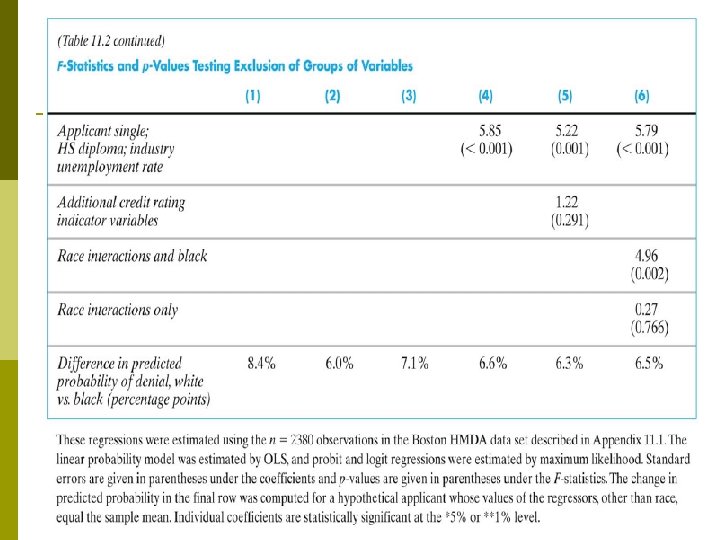

Application to the Boston HMDA Data Mortgages (home loans) are an essential part of buying a home. p Is there differential access to home loans by race? p If two otherwise identical individuals, one white and one black, applied for a home loan, is there a difference in the probability of denial? p

The HMDA Data Set Data on individual characteristics, property characteristics, and loan denial/acceptance. p The mortgage application process in 1990 -1991: p n n n p Go to a bank or mortgage company. Fill out an application (personal+financial info). Meet with the loan officer. Then the loan officer decides - by law, in a race-blind way. Presumably, the bank wants to make profitable loans, and the loan officer doesn’t want to originate defaults.

The loan officer’s decision p Loan officer uses key financial variables: n n p P/I ratio housing expense-to-income ratio loan-to-value ratio personal credit history The decision rule is nonlinear: n n n loan-to-value ratio > 80% loan-to-value ratio > 95% (what happens in default? ) credit score

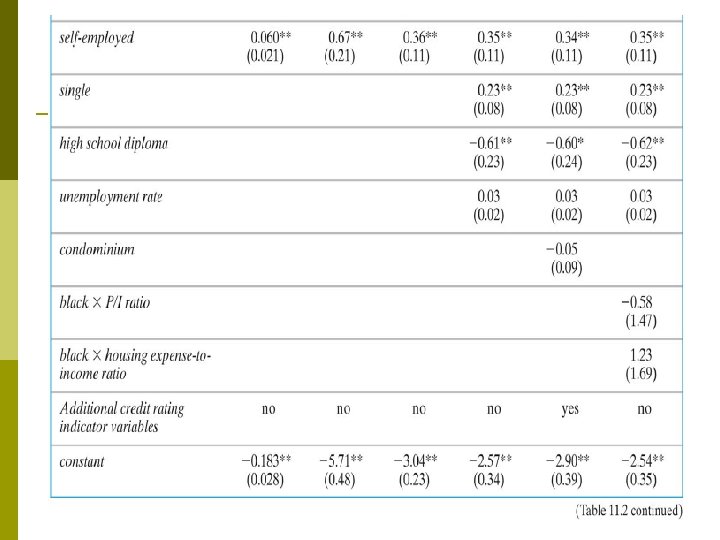

Regression specifications linear probability model p probit Main problem with the regressions so far: potential omitted variable bias. All these enter the loan officer decision function, are or could be correlated with race: p wealth, type of employment p credit history p family status Variables in the HMDA data set. . p

Summary of Empirical Results Coefficients on the financial variables make sense. p Black is statistically significant in all specifications. p Race-financial variable interactions aren’t significant. p Including the covariates sharply reduces the effect of race on denial probability. p LPM, probit, logit: similar estimates of effect of race on the probability of denial. p Estimated effects are large in a “real world” sense. p

Remaining threats to internal, external validity p Internal validity. n omitted variable bias p n n n what else is learned in the in-person interviews? functional form misspecification (no. . . ) measurement error (originally, yes; now, no. . . ) selection random sample of loan applications p define population to be loan applicants p n simultaneous causality (no) External validity p This is for Boston in 1990 -91. What about today? p

Misspecification is a big prolem in the maximum likelihood estimation. We only consider the problem of heteroscedasticity. p By assuming = 1 in the probit model, we only estimate and in the likelihood function. If ui is heteroscedastic such that Var(ui) = , then we need to estimate , and. p

p But the problem can be more than increasing number of parameters to be estimated. Suppose the heteroscedasticity is of the form then p The presence of heteroscedasticity causes inconsistency because the assumption of a constant is what allows us to identify 0 and.

p To take a very particular but informative case, suppose that the heteroscedasticity takes the form , then It is clear that our estimates will be inconsistent for and , but consistent for and. p The problem of misspecification such as heteorscedasticity calls for the use of linear probability model where although with White’s heteroscedasticity-consistent covariance matrix is not efficient, it is at least consistent. p

= Pr(Y=1|X). p Three models: p n")

Summary If Yi is binary, then E(Y|X) = Pr(Y=1|X). p Three models: p n n n linear probability model (linear multiple regression) probit (cumulative standard normal distribution) logit (cumulative standard logistic distribution) LPM, probit, logit all produce predicted probabilities. p Effect of ΔX is change in conditional probability that Y = 1. For logit and probit, this depends on the initial X. p Probit and logit are estimated via maximum likelihood. p n n Coefficients are normally distributed for large n. Large-n hypothesis testing, confidence intervals are as usual.

ed7eb176fcf4818101f5cb0c52f3bcb8.ppt