d6d6ebb1b57d5863e87d67c4461c1645.ppt

- Количество слайдов: 41

Reading company accounts possibilities and limitations of public domain information sources

Public domain sources information on individuals is scattered over several of these – and within each source

Wealth and income differ wealth is a ‘stock’ – a snapshot at a particular moment a ‘balance sheet’ item total assets minus total liabilities = ‘net worth’ income is a ‘flow’ over a given period, typically a year

‘Realisable’ wealth most assets have to be sold to be ‘realised’ (turned into actual cash) selling may be restricted (share ‘lock ins’, legal covenants, market conditions) the easier and quicker an asset can be realised the more ‘liquid’ it is

Liquidity of wealth high – cash deposits, easily marketable securities (government bonds, ‘blue chip’ shares) medium (able to borrow against them) – real estate, insurance policies low – infrequently traded securities (dot. com ‘millionaires’) other categories shift (property, precious metals/stones, works of art) category according to economic conditions

British official wealth statistics not current – based on estates of deceased admitted to probate in a given year – but worth noting wills are in the public domain however, aggregate data is available in terms of asset values

Sources of personal wealth 2006 Non-financial assets Residential buildings Other £ billion % of total wealth 3, 696 44. 7 772 9. 3

thus some 45% of personal wealth is tied up in bricks and mortar not easily fully ‘realisable’ – although can be borrowed against

Land Registries • official record of land ownership • www. landreg. gov. uk

What Land Registry records tell you registered owners of a property or piece of land (from 2000) price when last sold or estimated value if newly registered name of lender if it is mortgaged

Title number: CS 72510 This title is dealt with by Land Registry, Plymouth Office. This extract shows information current on [date and time] and so does not take account of any application made after that time even if pending in the Land Registry when this extract was issued. REGISTER EXTRACT Title Number : CS 72510 Address of Property : 23 Cottage Lane, Kerwick, PL 14 3 JP. Price Paid/Value Stated : £ 128, 000 Registered Owners : Peter Andrew Bartram and Susan Helen Bartram of : 23 Cottage Lane, Kerwick, (PL 14 3 JP). Lender : ILKINGHAM BUILDING SOCIETY The price paid/value stated information has been entered in the register since 1 April 2000.

current value of property")

- and what they don’t not comprehensive (although effectively so) current value of property present size of mortgage outstanding – residential mortgages often used to raise business capital most crucially – what real estate an individual owns

Sources of personal wealth 2006 Financial assets £ billion % of total wealth Life assurance & pensions Currency & deposits Securities & shares 2, 110 25. 5 996 12. 0 584 7. 0 112 1. 4 Other

Again much remains hidden life assurance policies not in the public domain pensions likewise (although some data for directors of listed companies) so we’ll concentrate on ‘securities and shares’ – and also directors’ remuneration

‘Securities and shares’ ‘securities’ is more commonly used for both – ‘shares’ confer ownership rights in companies and are publicly recorded – ‘securities’ here largely means holdings of ‘bonds’ (loans to governments and companies), which are not

Business vehicles Sole trader Partnership Company

– treated like companies for disclosure purposes and")

Partnership forms Limited Liability Partnerships (LLPs) – treated like companies for disclosure purposes and have to file accounts at Companies House Limited Partnerships – no financial statements filed General Partnerships – not recorded at Companies House

Companies Private Public Listed

Private companies often difficult to research in detail exemptions from filing mean that only 1 in 8 of actively trading companies file accounts at Companies House less information in private company accounts – so we’ll concentrate on Public Limited Liability companies (PLCs)

Sources of data primary secondary for an individual’s shareholdings and dividends directors’ remuneration

in registers held by company –")

Primary shareholder data recorded (along with any changes) in registers held by company – although this function outsourced to registrars by larger firms with many shareholders Annual Returns (include a full list of shareholders and the number of shares held) filed at Companies House – ‘bulk shareholders lists’ Directors’ Report in annual report and accounts show ‘substantial’ shareholdings Notes to accounts show ‘directors’ emoluments’

Directors’ Report data lists directors charitable contributions by company for PLCs only – ‘substantial shareholdings’ defined as 3% or more of total voting share capital

Substantial Shareholdings At the date of this report, the directors are aware of the following interests which represent a 3% or greater interest in the issued share capital of the Company in addition to those of the directors referred to in note 25 to the financial statements. Number of Percentage of ordinary shares issued ordinary share capital Wheddon Limited 33, 999 29. 8% OMX Securities Nominees Limited 7, 177, 033 6. 3% Pershing Keen Nominees Limited 5, 996, 808 5. 3% Charitable Contributions During the year the Group made charitable donations of £ 800 (2006: £ 575).

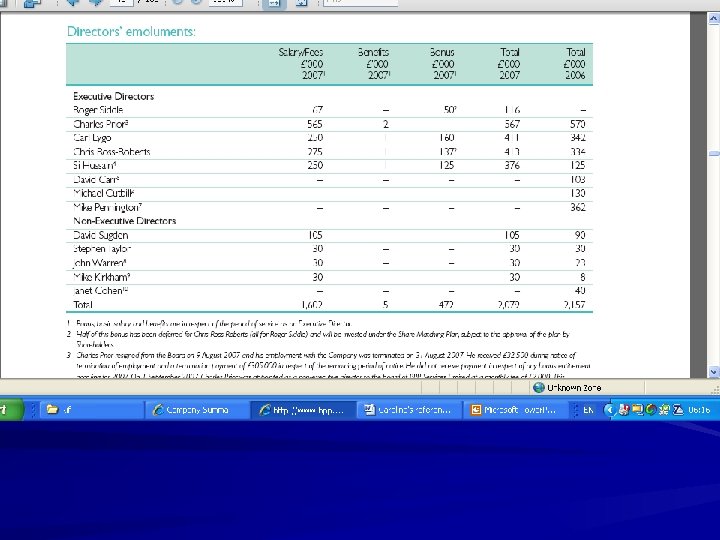

Notes to accounts ‘Directors emoluments’ are shown as a note however, less detail is available for smaller companies – data is shown as bands rather than exact figures – individual directors’ salaries not identified

Listed companies only following business scandals of late 1980 s growing emphasis on ‘corporate governance’ ‘Cadbury’ and other reports incorporated into ‘Combined Code’ for companies listed on London Stock Exchange a ‘Remuneration Report’ for board members filed with each annual report n. b. only around 1, 800 out of 11, 500 PLCs are listed

in their company by individual")

Remuneration report details of holdings (and their share options) in their company by individual directors is a key item

RNS announcements London Stock Exchange’s Regulatory News Service provides immediate information to market any change in a director’s holdings must be reported through the RNS also acquisition by any party of a 3% plus holding (or if existing one falls below this threshold) or if these holdings rise or decrease by more than 1% of total voting share capital

London Stock Exchange itself")

Some good sources Karen Blakeman’s portal (www. rba. co. uk) London Stock Exchange itself (www. londonstockexchange. com) Hemmington Scott (www. hemscott. com)

Share options rights given to directors to buy up to a given number of their company’s shares at a set price an incentive to push up market share price director who has exercised their option will profit if this rises above the ‘exercise price’ of option potentially very profitable so included in Remuneration Report

A complication shares can be held by ‘beneficial’ owners or by ‘nominees’ on their behalf primary sources often show holdings in names of nominees no legal mechanism to force private companies to reveal beneficial owners but PLCs can demand ‘Section 212 Notices’ disclosing this for substantial holdings

Fund Manager Nominee Beneficial Owner MULTI-MANAGED CHASE NOMINEES LIMITED REQUIRES 212 REPLY RBSTB NOMINEES LIMITED REQUIRES 212 REPLY VIDACOS NOMINEES LIMITED REQUIRES 212 REPLY BT GLOBENET NOMINEES LIMITED REQUIRES 212 REPLY VIDACOS NOMINEES LIMITED REQUIRES 212 REPLY CHASE NOMINEES LIMITED REQUIRES 212 REPLY MELLON NOMINEES UK LIMITED BOSTON SAFE CUSTODIANS CHASE NOMINEES LIMITED REQUIRES 212 REPLY BANK OF NEW YORK NOMINEES LIMITED REQUIRES 212 REPLY KAS NOMINEES LIMITED REQUIRES 212 REPLY BT GLOBENET NOMINEES LIMITED REQUIRES 212 REPLY NORTRUST NOMINEES LIMITED REQUIRES 212 REPLY MELLON NOMINEES UK LIMITED BOSTON SAFE CUSTODIANS NORTRUST NOMINEES LIMITED REQUIRES 212 REPLY BANK OF IRELAND NOMINEES LIMITED REQUIRES 212 REPLY RBSTB NOMINEES LIMITED ELECTRICITY SUPPLY PENSION SCHEME

Secondary shareholding services confined to quoted companies raw data taken from registrars, RNS announcements, Section 212 notices combined to allow analysis of both – a company’s shareholding structure – holdings by investors (but these are overwhelmingly institutional rather than personal investors)

Key UK services Argus – The Owners Service Citywatch see ‘Share Ownership’ in business information service aggregator Alacra (www. alacra. com)

Value of individual shareholdings total number of shares held multiplied by current share price (but check on trends in the price) however, shares only realisable if sold!

Dividends income from shareholdings in those companies actually paying them payouts are recorded as ‘Dividends Per Share’ in the ‘profit and loss account’ of the annual report – not the same as ‘Earnings Per Share’! multiply this by number of shares held to find total dividends an individual shareholder receives

Remuneration report corporate governance debate recognised salaries of directors are often only part of their remuneration so the report covers other elements – fees paid to them (such as ‘golden hellos’) – share options – bonuses – pension contributions paid by company – benefits (cars, private medical insurance, etc. )

Conclusions public domain documentation is not sufficient to research individual wealth yet it has an useful role to play just don’t expect assembling it to be quick or easy!

Finally, a source of help when all else has failed Free Pint (www. freepint. com) – a global community of researchers the ‘Bar’ allows one to table a question – or provide the answer or some guidance and advice

Feel free to get in touch! • Chris Murphy • Ravensbourne Research Limited • ravensbourneresearch@tiscali. co. uk • chrismurphy 1999@yahoo. co. uk • 020 8658 0487 • 0780 3507753

d6d6ebb1b57d5863e87d67c4461c1645.ppt