Презентация perfect competition1

- Размер: 691 Кб

- Количество слайдов: 58

Описание презентации Презентация perfect competition1 по слайдам

1 Perfect Competition These slides supplement the textbook, but should not replace reading the textbook

2 What is market structure? Important features of a market, such as the number of firms, product uniformity, ease of entry, and forms of competition

3 What are the four types of Markets? Perfect Competition Monopolistic Competition Oligopoly Monopoly

4 What is a perfectly competitive market? homogeneous product many buyers and sellers no one has much market power easy entry & easy exit can sell all bring to market

5 What is a price taker? A firm that faces a given market price and whose actions have no effect on that market price

6 Why is a firm that is part of a perfectly competitive market a price taker? Because if the firm charges higher than the market price it will not sell even one unit

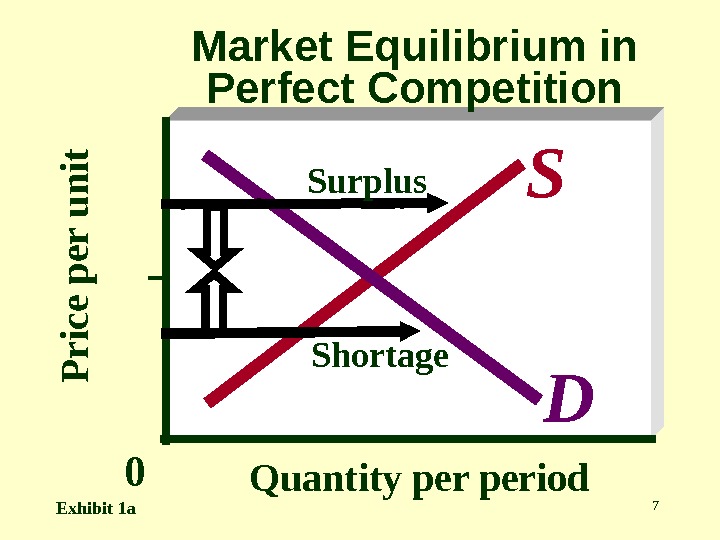

7 P r i c e p e r u n i t. Quantity period. Market Equilibrium in Perfect Competition DS 0 Exhibit 1 a Surplus Shortage

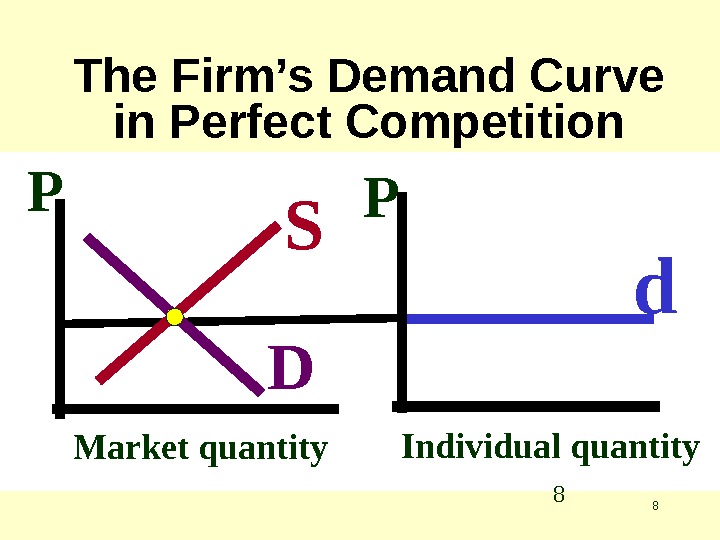

8 The Firm’s Demand Curve in Perfect Competition Market quantity. P S D Individual quantity. P d

9 How does the firm maximize profit? By finding the rate of output that makes total revenue minus total cost as large as possible

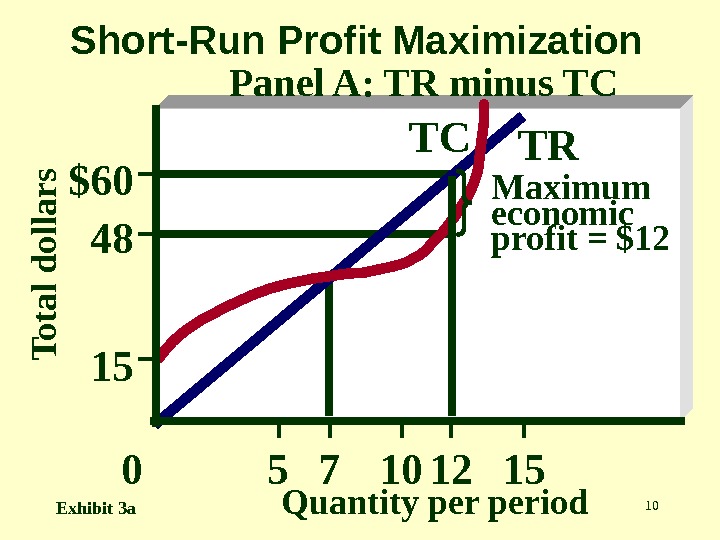

107 Maximum economic profit = $12 12 TRTC $60 48 15 T o t a l d o lla r s Quantity period. Short-Run Profit Maximization Panel A: TR minus TC 151050 Exhibit 3 a

11 What is marginal revenue? The change in total revenue resulting from a one-unit change in sales

12 What is marginal cost? The change in total cost resulting from a one-unit change in sales

13 At what point are profits maximized? At the level of output where MR = MC , or the last unit of output where MR > M

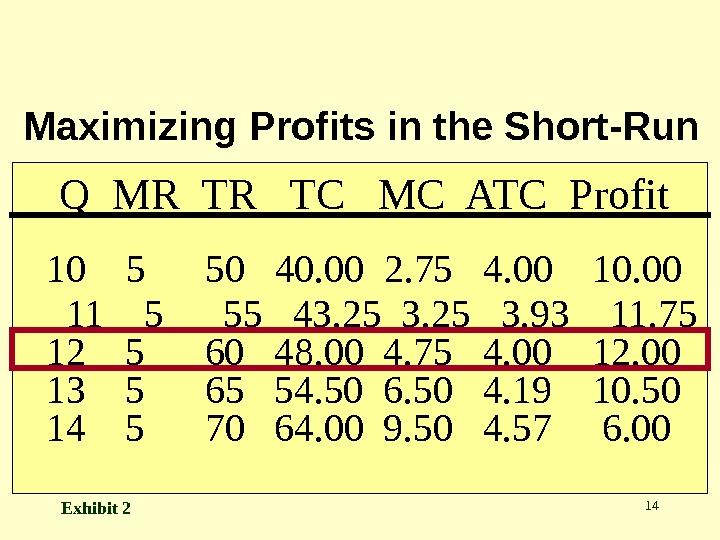

14 Q MR TR TC MC ATC Profit 10 5 50 40. 00 2. 75 4. 00 10. 00 11 5 55 43. 25 3. 93 11. 75 12 5 60 48. 00 4. 75 4. 00 12. 00 13 5 65 54. 50 6. 50 4. 19 10. 50 14 5 70 64. 00 9. 50 4. 57 6. 00 Exhibit 2 Maximizing Profits in the Short-Run

15 Why does MR = P in Perfect Competition? Because no matter how many units are brought to market, the firm can sell all of them at the market price

16 What is average revenue? Total revenue divided by output TR / Q

17 Why does AR=P in all markets? Because each unit is sold for the same price at one point in time

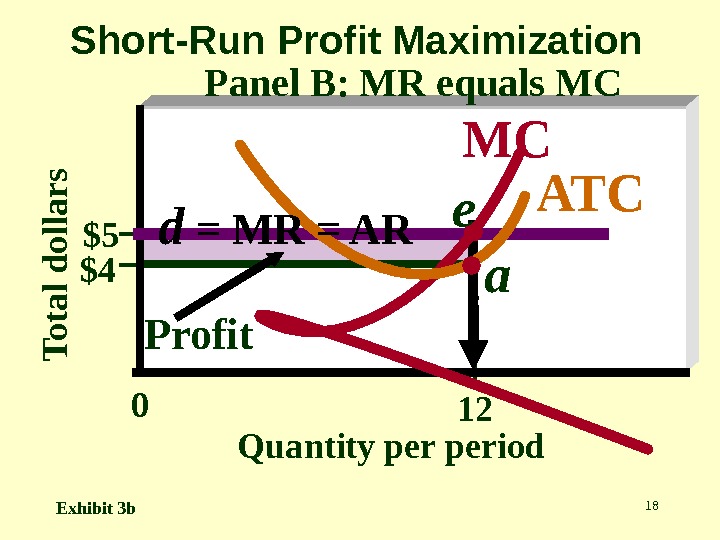

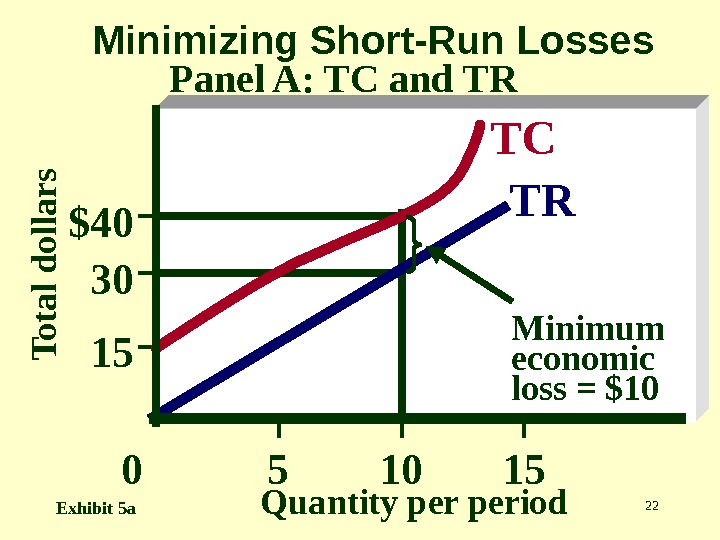

18 T o t a l d o lla r s. Quantity period. Short-Run Profit Maximization Panel B: MR equals MC 120$5 $4 Profit d = MR = AR ATCMC e a Exhibit 3 b

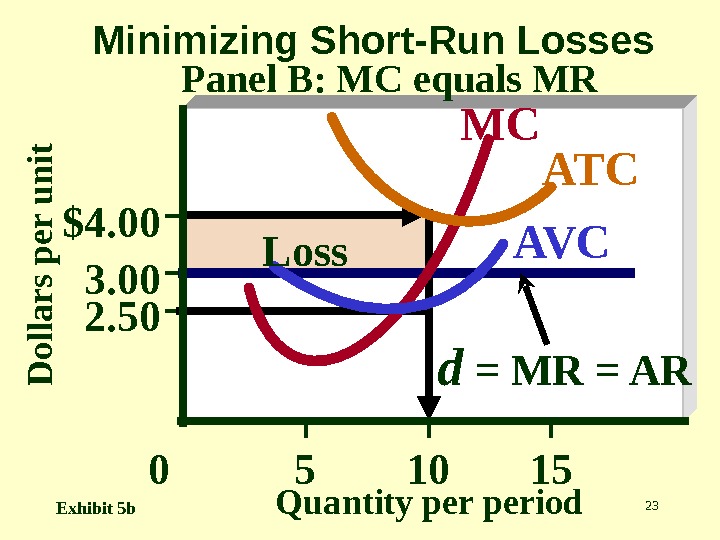

19 At what point are losses minimized? At the level of output where MR = MC , or the last unit of output where MR > M

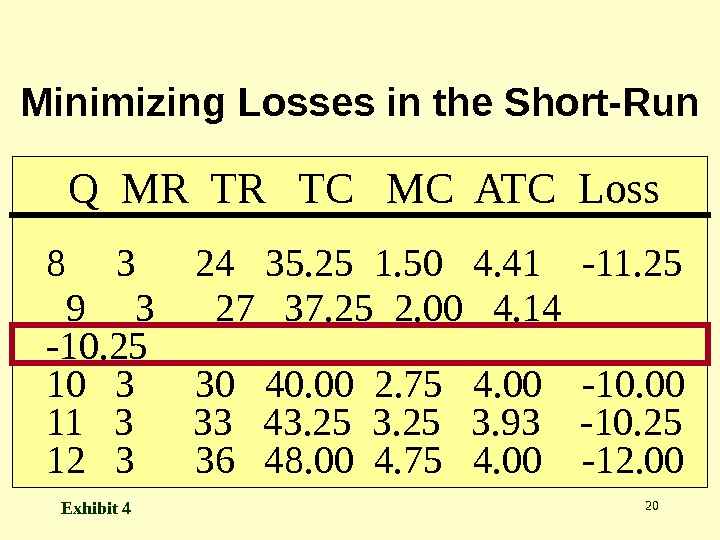

20 Q MR TR TC MC ATC Loss 8 3 24 35. 25 1. 50 4. 41 -11. 25 9 3 27 37. 25 2. 00 4. 14 -10. 25 10 3 30 40. 00 2. 75 4. 00 -10. 00 11 3 33 43. 25 3. 93 -10. 25 12 3 36 48. 00 4. 75 4. 00 -12. 00 Exhibit 4 Minimizing Losses in the Short-Run

21 What will a firm do if average variable cost exceeds price at every level of production? Shut down

22$40 30 15 T o t a l d o lla r s Quantity period. Minimizing Short-Run Losses 151050 Minimum economic loss = $10 TRTCPanel A: TC and TR Exhibit 5 a

23$4. 00 3. 00 2. 50 151050 D o lla r s p e r u n it Quantity period. Minimizing Short-Run Losses MC AVC ATC d = MR = ARPanel B: MC equals MR Exhibit 5 b Loss

24 What is the firm’s short-run supply curve? A curve that indicates the quantity a firm supplies at each price in the short run

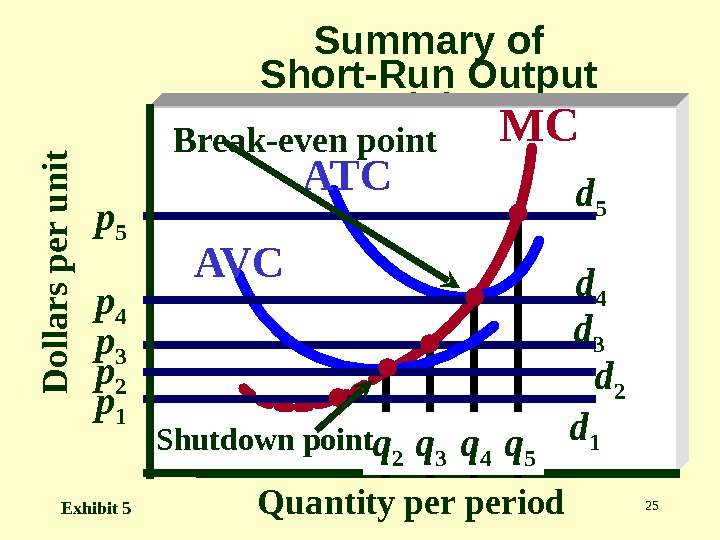

25 D o lla r s p e r u n it Quantity period Summary of Short-Run Output Decisions p 1 p 2 p 3 p 4 p 5 q 2 q 3 q 4 q 5 MC ATC AVC Shutdown point Break-even point d 1 d 2 d 3 d 4 d 5 Exhibit

26 What is the firm’s short run supply curve? That portion of its MC curve which lies above its AVC curve

27 T o t a l d o lla r s Quantity period. Relationship between Short-Run Profit Maximization and Market Equilibrium Panel A: Firm 12105 0$5 4 Profit d=MR ATCMC = s Exhibit 8 a AV

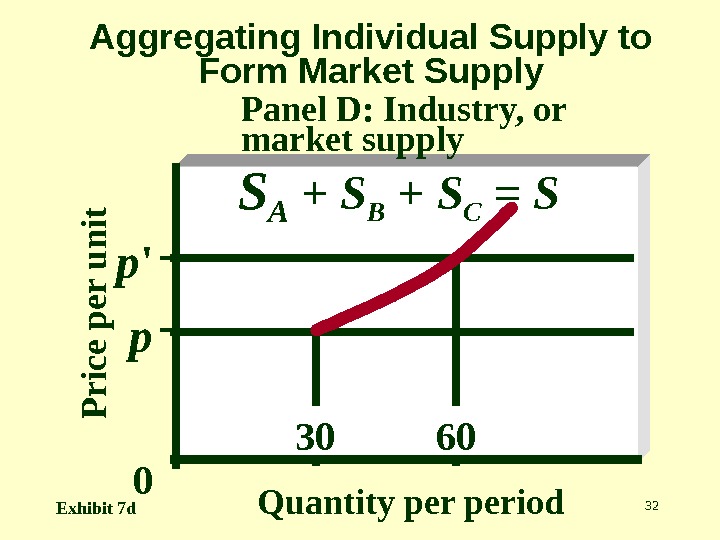

28 What is the industry’s short-run supply curve? A curve that indicates the quantity all firms in an industry supply at each price in the short run

29 Aggregating Individual Supply to Form Market Supply Panel A: Firm AP r ic e p e r u n it Quantity periodp ‘ p 10 20 0 S A Exhibit 7 a

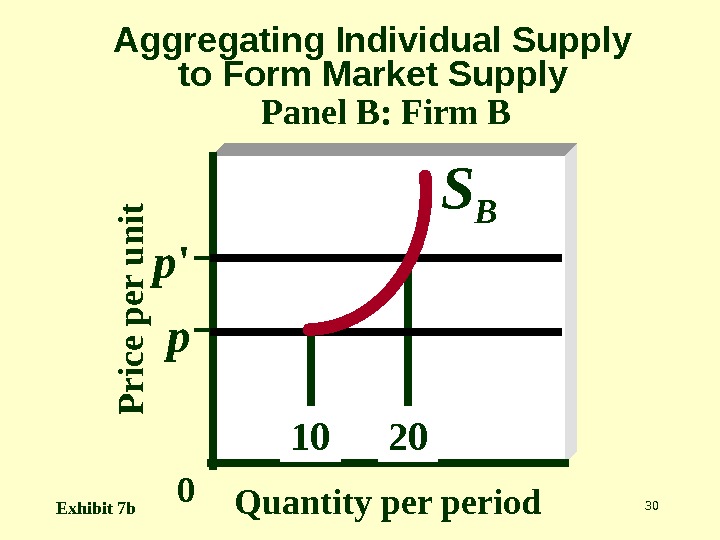

30 Aggregating Individual Supply to Form Market Supply Panel B: Firm BP r ic e p e r u n it Quantity periodp ‘ p 10 20 0 S B Exhibit 7 b

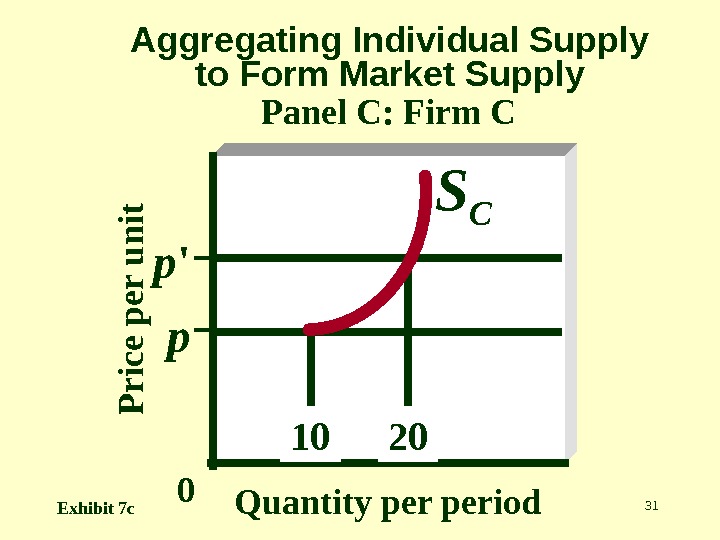

31 Aggregating Individual Supply to Form Market Supply Panel C: Firm CP r ic e p e r u n it Quantity periodp ‘ p 10 20 0 S C Exhibit 7 c

32 Aggregating Individual Supply to Form Market Supply Panel D: Industry, or market supply. P r ic e p e r u n it Quantity periodp ‘ p 30 60 S A + S B + S C = S 0 Exhibit 7 d

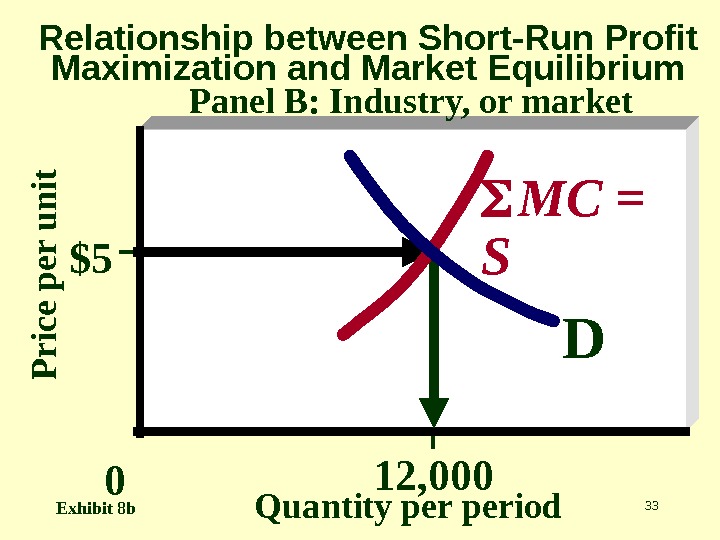

33 P r ic e p e r u n it Quantity period. Relationship between Short-Run Profit Maximization and Market Equilibrium Panel B: Industry, or market 12, 000 0$5 D MC = S Exhibit 8 b

34 What is economic profit in the long run? Zero

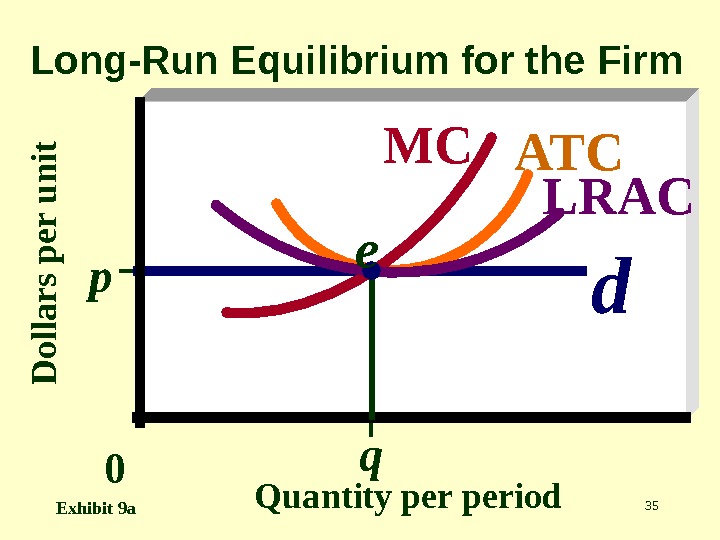

35 D o lla r s p e r u n it. Quantity period. Long-Run Equilibrium for the Firm q 0 p d. ATCMC LRAC e Exhibit 9 a

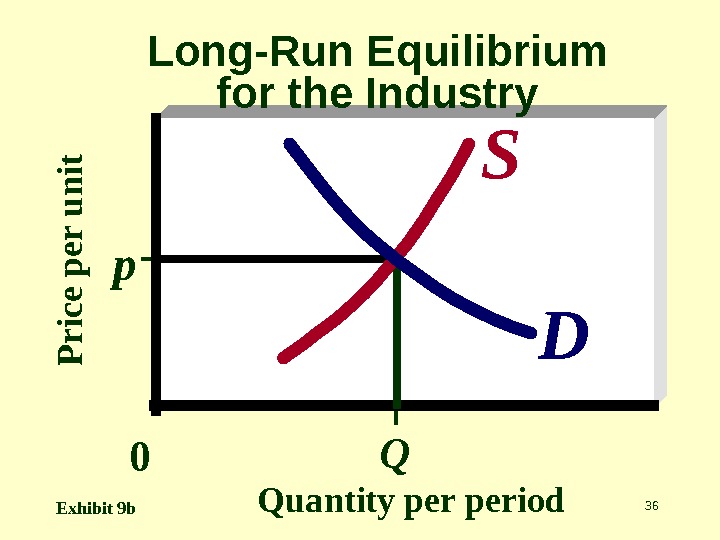

36 P r ic e p e r u n it Quantity period. Long-Run Equilibrium for the Industry Q 0 p DS Exhibit 9 b

37 What is the long-run industry supply curve? A curve that shows the relationship between price and quantity supplied once firms fully adjust to any change in market demand

38 What is an increasing-cost industry? An industry that faces higher per-unit production costs as industry output expands in the long run

39 Upward sloping. What is the shape of the long-run industry supply curve in an increasing cost industry?

40 What is production efficiency? The condition that exists when output is produced with the least-cost combination of inputs, given the state of technology

41 What is allocative efficiency? The condition that exists when firms produce the output that is most preferred by consumers

42 What is the marginal cost of each good equal to? The marginal benefit consumers derive from that good

43 What is consumer surplus? The difference between the maximum amount that a consumer is willing to pay for a given quantity of a good and what the consumer actually pays

44 What is producer surplus? The amount by which total revenue from production exceeds total variable cost

45 Consumer Surplus and Producer Surplus for a Competitive Market in the Short Run. D o lla r s p e r u n it Quantity period 5$10 0 10, 000 20, 00012, 0006 e m S DConsumer surplus Producer surplus Exhibit

46 EN

47 Appendix

48 What is a constant-cost industry? An industry that can expand or contract without affecting the long-run per-unit cost of production

49 What is the shape of the long-run industry supply curve? horizontal

50 D o lla r s p e r u n it. Quantity period q 0 p d. ATCMC LRAC d’ Profit q’p’ Panel A: the Firm Exhibit 10 a Long-Run Adjustment to an Increase in Demand in a Constant Cost Industry

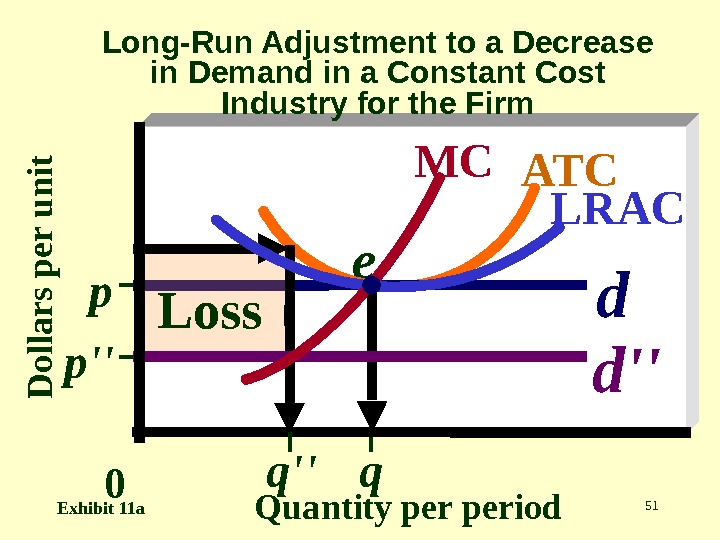

51 D o lla r s p e r u n it Quantity period. Long-Run Adjustment to a Decrease in Demand in a Constant Cost Industry for the Firm q 0 p d. ATCMC LRAC e p» q» d»Loss Exhibit 11 a

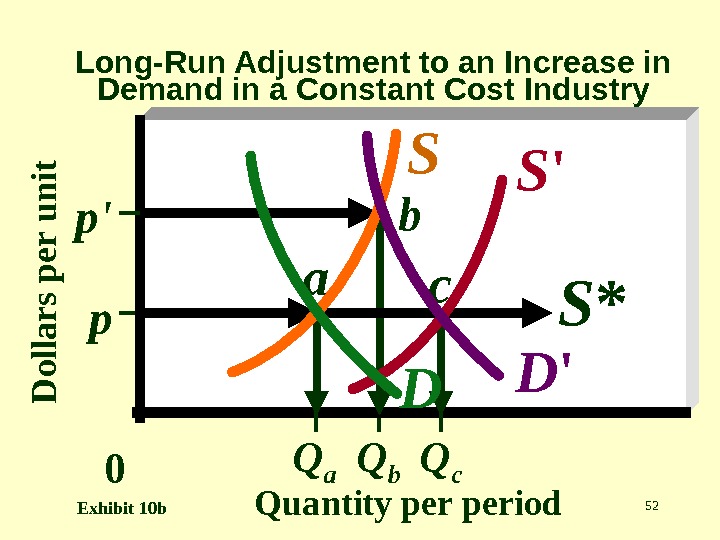

52 D o lla r s p e r u n it Quantity period. Long-Run Adjustment to an Increase in Demand in a Constant Cost Industry Q b 0 p Q cp’ Q a S *S ‘S D ‘ Da b c Exhibit 10 b

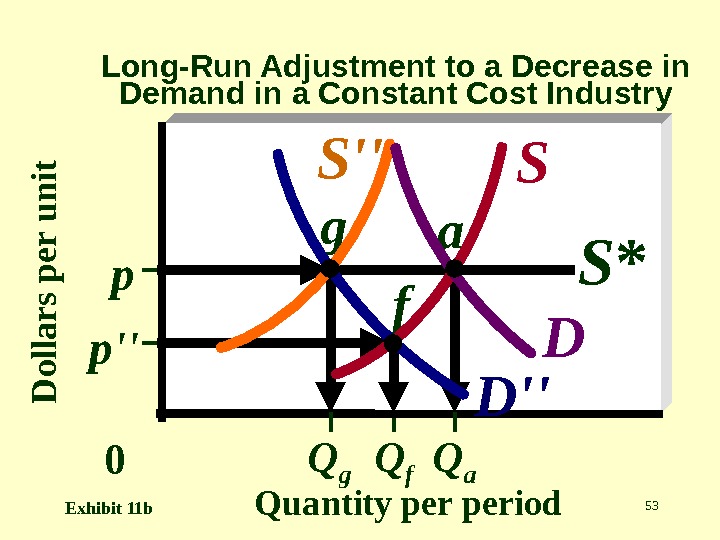

53 D o lla r s p e r u n it Quantity period Q f 0 p» Q ap Q g S *SS» D D»g a f Exhibit 11 b Long-Run Adjustment to a Decrease in Demand in a Constant Cost Industry

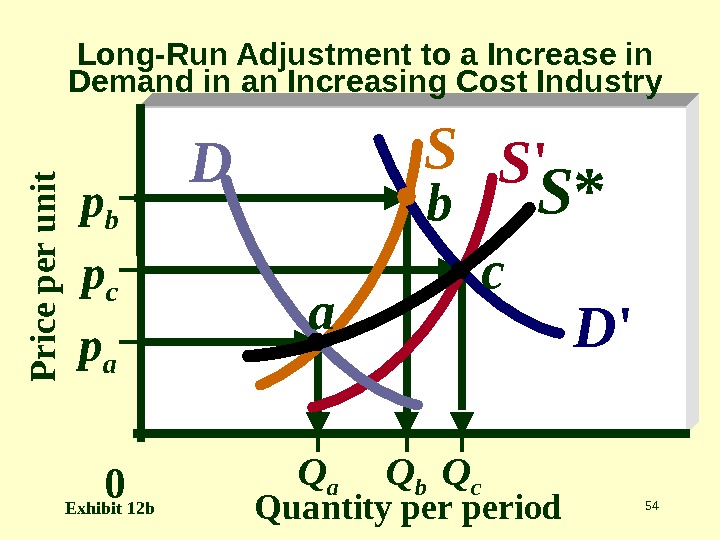

54 P r ic e p e r u n it Quantity period Q b 0 p ap cp b Q c. Q a S *S ‘S D D ‘a b c Exhibit 12 b Long-Run Adjustment to a Increase in Demand in an Increasing Cost Industry

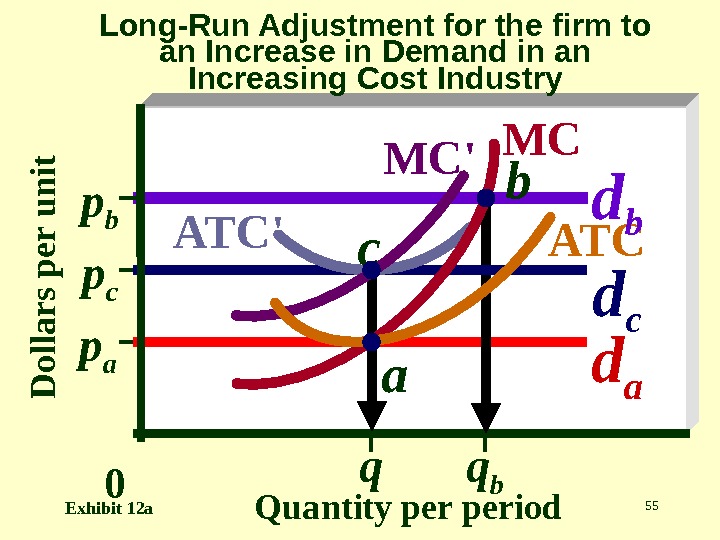

55 D o lla r s p e r u n it Quantity period q b 0 p a d a. ATCMC’ ap c q d ccp b MC ATC’ d bb Exhibit 12 a Long-Run Adjustment for the firm to an Increase in Demand in an Increasing Cost Industry

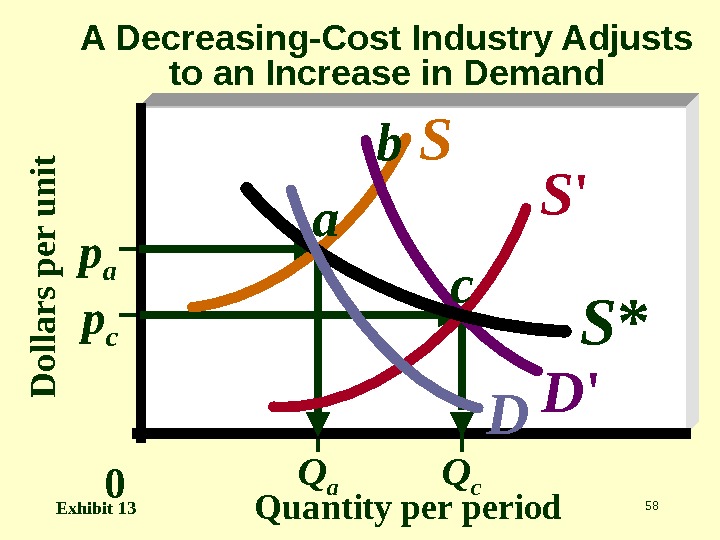

56 What is a decreasing-cost industry? The rare case in which an industry faces lower per-unit production costs as industry output expands in the long run

57 Downward sloping. What is the shape of the long-run industry supply curve in a decreasing cost industry?

58 D o lla r s p e r u n it Quantity period. A Decreasing-Cost Industry Adjusts to an Increase in Demand 0 p a p c Q c. Q a S *S ‘S D D ‘a b c Exhibit