56222b5424eb219fa48cc1a400220c53.ppt

- Количество слайдов: 38

Debt Agreements – the basics")

Part IX (9)Debt Agreements – the basics

What is a Part IX Debt Agreement ? • Legally binding agreement between a debtor and a creditor • Debtor maintains normal contractual payments to secured creditors, while unsecured creditors including fees and costs are consolidated into one affordable payment. • Doesn’t have the serious consequences of a bankruptcy ?

Financial Counsellor Perspective Why consider a Debt Agreement over a bankruptcy? • owns a property or has an asset realisable in bankruptcy • high income & may need to pay income contributions • employment / license could be affected by full bankruptcy ie, security guard or real estate agent • is likely to receive a monetary gain within a bankruptcy period ie, inheritance • Listed on Public Record (NPII) for 5 years. Bankruptcy is forever. • Hardship periods are coming to an end • Lump sum available to avoid 3 year bankruptcy term • Company Directorship • Sole Trader is required to have full name in the title of their business

Eligibility • Must be less than the following amounts: • $1, 578. 94 - Weekly Income (net) • $109, 473. 00 – Assets • $109, 473. 00 - Unsecured debts • Not been a discharged bankrupt or in a Debt Agreement within the past 10 years • Must be insolvent (unable to pay debts) • Can afford to make payments towards a Debt Agreement

Consequences of a Debt Agreement • The debtor is not bankrupt and therefore avoid restrictions of a full bankruptcy • Proposing a Debt Agreement is an act of bankruptcy • Need more than 50% of creditors to vote ($value) • Once accepted: * Protects assets & enforcement action from creditors * Stops interest • The debtor is released from provable debts upon it’s completion • Listed on Public Record (NPII) 5 Years • Listed on a Credit History for 5 years • A debtor cannot borrow more than $5, 507 without disclosing he/she in a current Debt Agreement • Debtor can still be a Company Director

Aim of Debt Agreements • Be affordable • Be attractive to debtors as an alternative to bankruptcy • Be attractive to creditors as an alternative to bankruptcy • Protect assets and employment • Stop interest

Australia Tax Office debts • ATO expect all tax returns (& BAS Statements (if applicable) to be up to date before considering a positive vote towards a Debt Agreement. • The RDAA (Registered Debt Agreement Administrator) would expect Tax Returns to be up to date to disclose a true reflection of a debtor’s financial situation, ie. Threshold assessment and certification duties • ATO will keep refunds

Confirm, assess & substantiate a debtors: • Insolvency")

Role of Administrator – (pre lodgement) Confirm, assess & substantiate a debtors: • Insolvency status • Debts are fully disclosed and correct • Income is accurate • Affordability • Explanation of circumstances to creditors • To provide the best outcome for both debtor & creditors Provide the debtor with the following: • A Copy of Prescribed Information document • The consequences of a Debt Agreement • Other available options for dealing with their debts

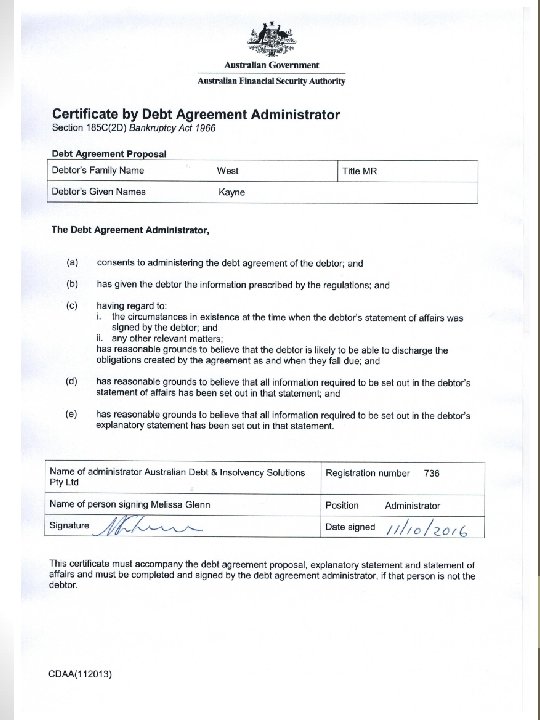

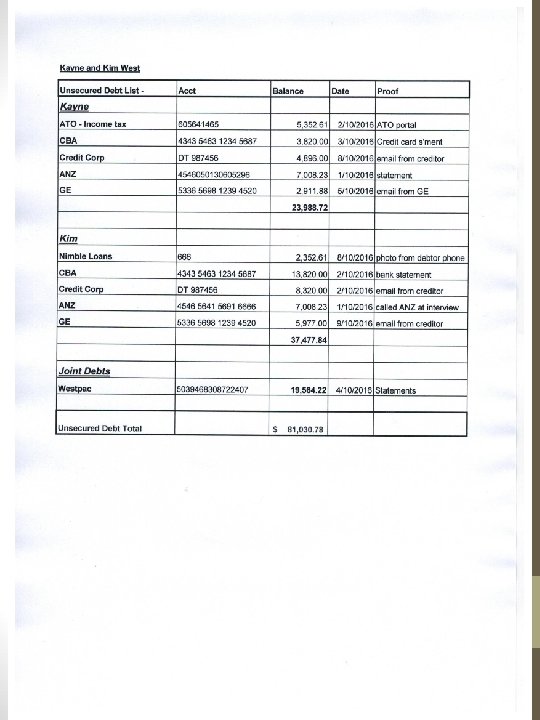

Case study. . • Kayne and Kim West – Debt Agreement or not?

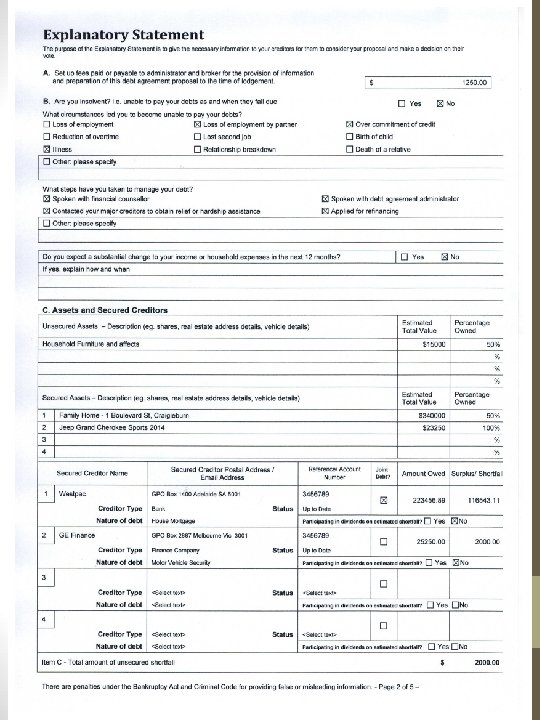

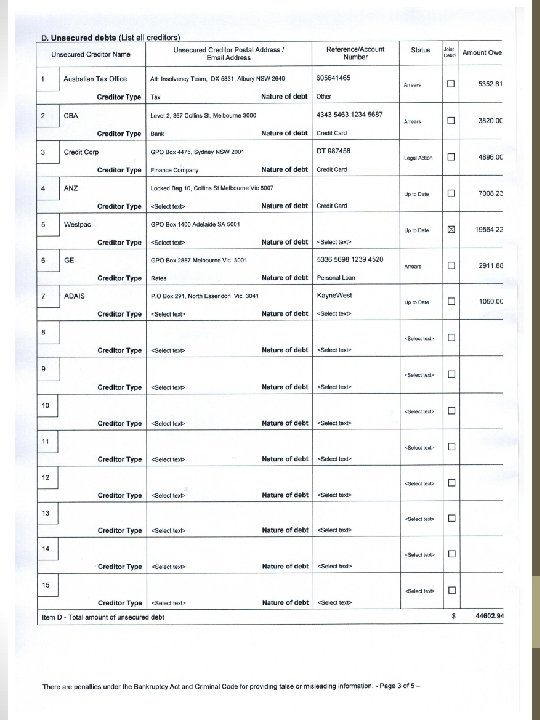

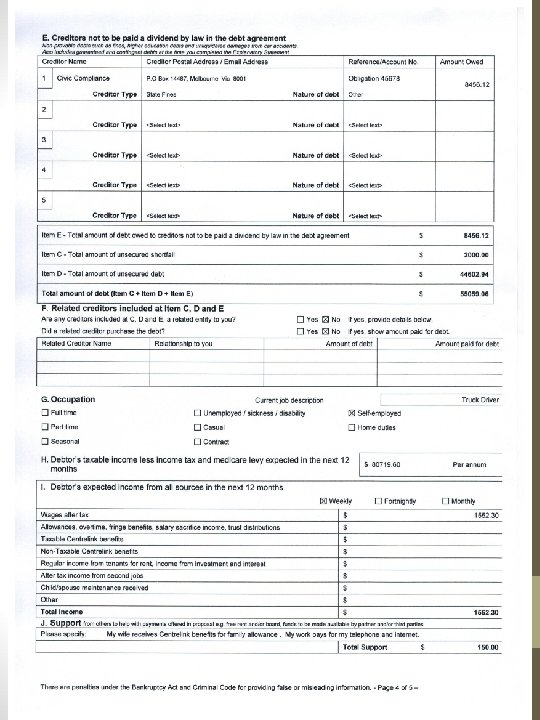

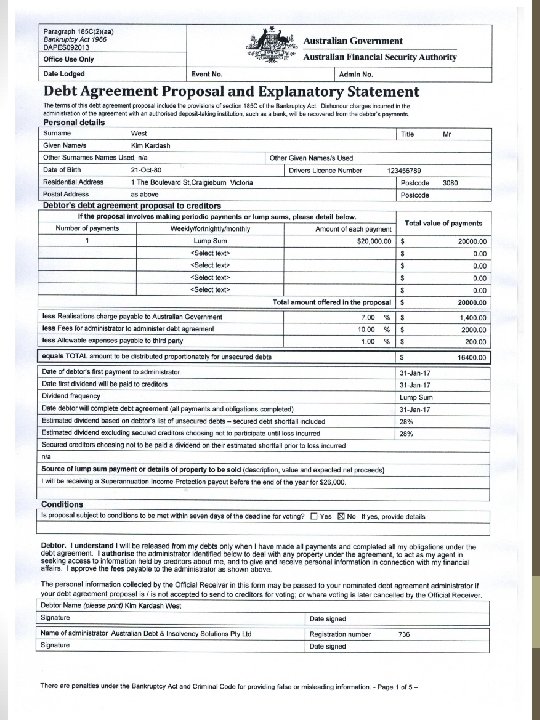

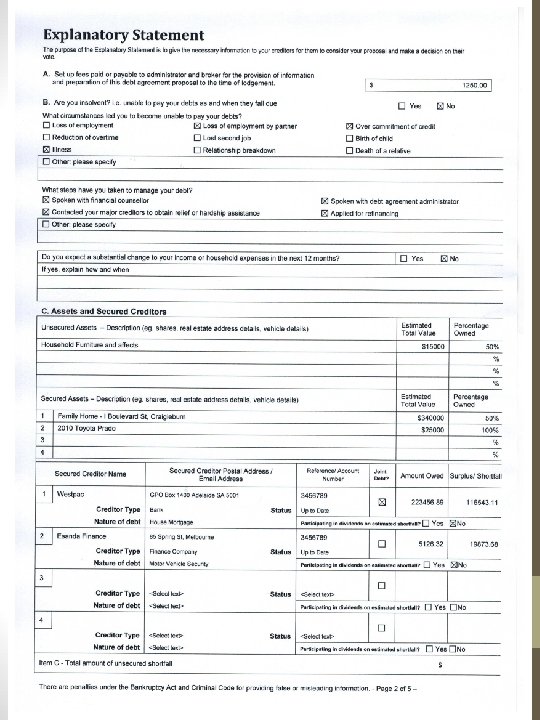

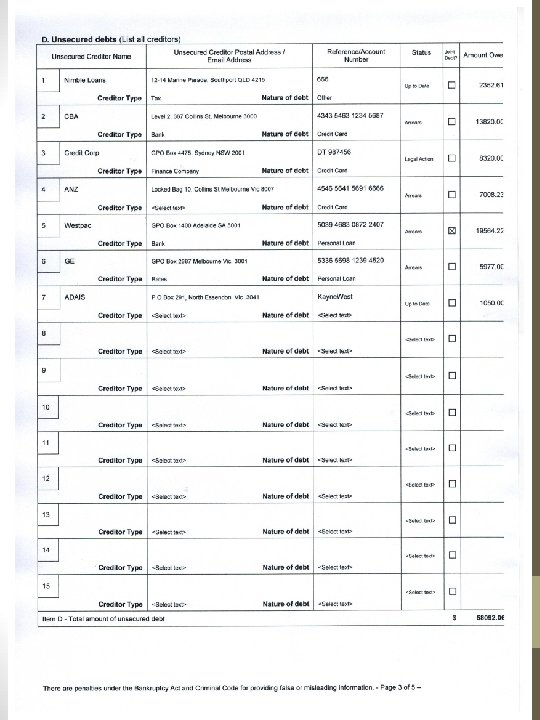

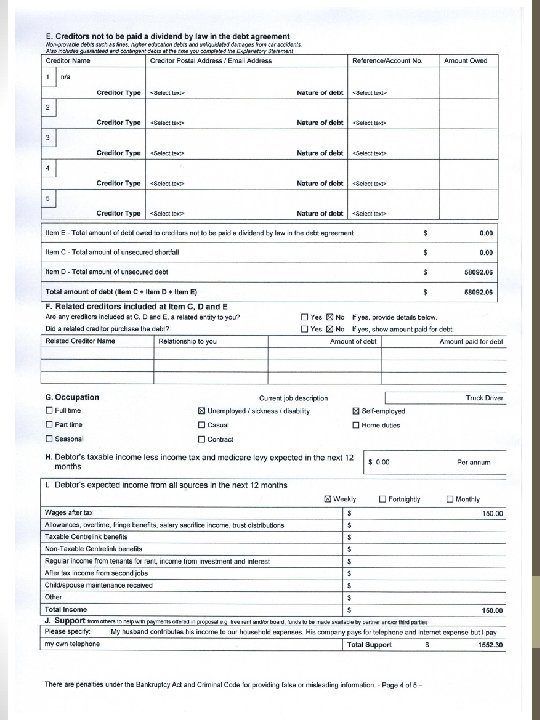

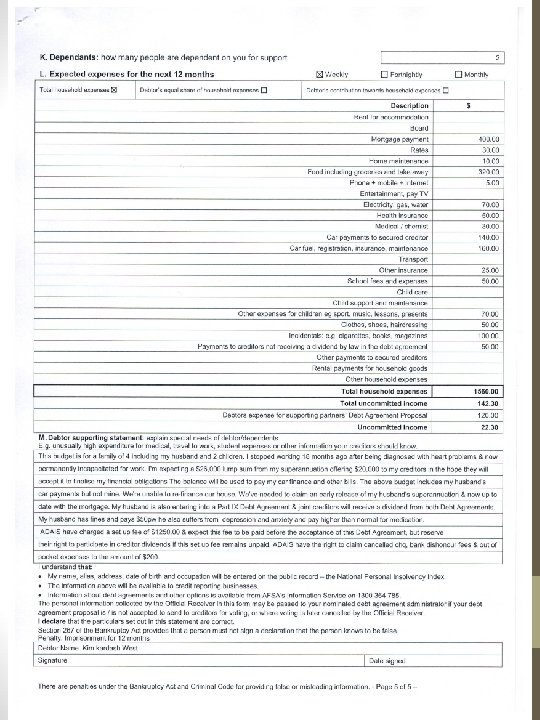

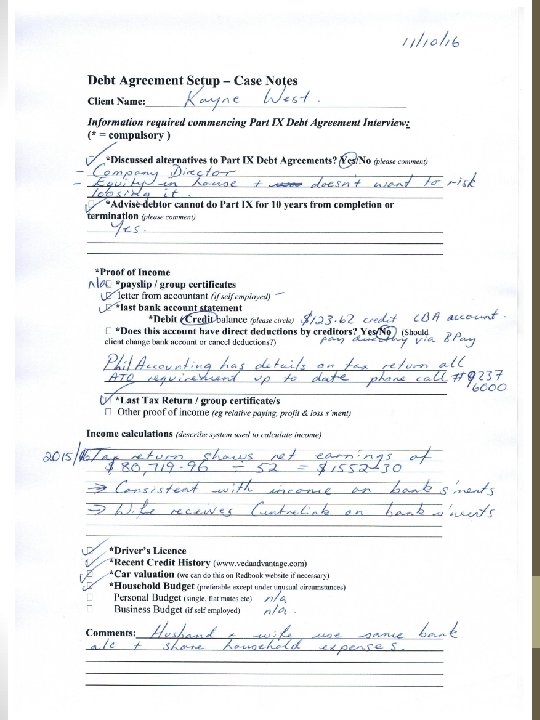

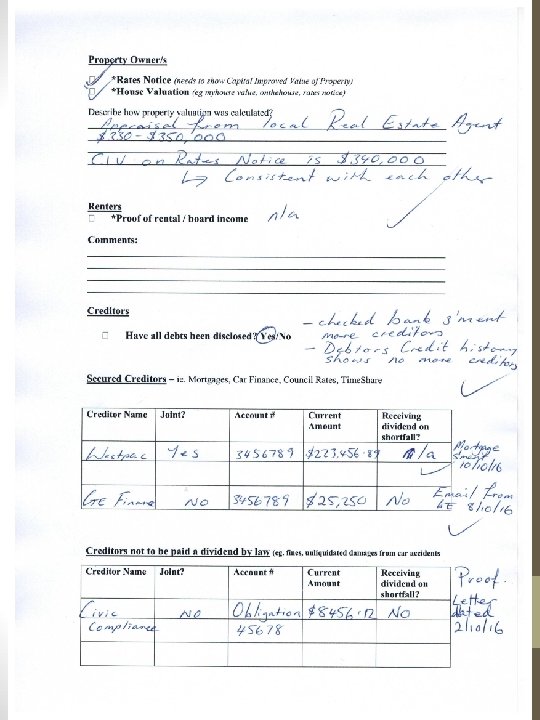

• The Facts: • Kim and Kayne were managing minimum payments until Kim became permanently incapacitated 18 months ago, therefore unable to work and used existing credit cards to help pay the bills. • Kayne: • Owns a 2012 Jeep Cherokee which is financed through GE Finance with a balance of $25, 250 with 4 years until payments are finished. The Jeep is valued at approximately $23, 250. 00 • He is a truck driver and the sole director of Big Bad Trucks Pty Ltd. His main contractor requires he trades as a company. This company pays for his telephone and internet. • His average net weekly income is approximately $1552. 30 pw and based on recent tax returns. • $43, 552. 94 in unsecured debts and up to date with his tax obligations. • Suffers from depression and anxiety and is on medication to control this.

• Kim: • A Financial Counsellor helped her claim her superannuation via a MB Lawyers and will be receiving $26, 000 within the next few weeks. There is another claim for insurance but this could take many years to negotiate if at all. • Has a loan with Esanda Finance with a balance of $5, 126. 32. A 2010 Toyota Prado is secured to this loan and due to finish in a year’s time. The Prado is valued at $25, 000 • Unsecured debts of $ 57, 042. 06 • Receives Family Allowance from Centrelink of $300 fortnight • Joint details: • Mortgage on family home with Westpac with a balance of $223, 456. 89. •

• Mortgage is up to date after a Financial Counsellor organised an early release of Kayne’s superannuation. • House is valued at approximately $340, 000 • Approximately $15, 000 in furniture and household items (re-sale value) • A Statement of Financial Position shows uncommitted income of around $146. 30 pw, after taking into consideration house hold expenses. • The unsecured debt owed to Westpac for $19, 564. 22 is in joint names •

• Things to consider: • Kayne: • Consequences of full bankruptcy in relation to the following: • Income? • Employment? • Assets? • Civic Compliance Fines? • Is Kayne eligible to do a Part IX Debt Agreement? If so, how would this benefit him? • Can you suggest any other solutions for Kayne? • Kim: • Consequences of full bankruptcy in relation to the following: • Income? • Assets? • Is Kim eligible for a Part Ix Debt Agreement? If so, how would she benefit from it? • Can you suggest any other solutions for Kim?

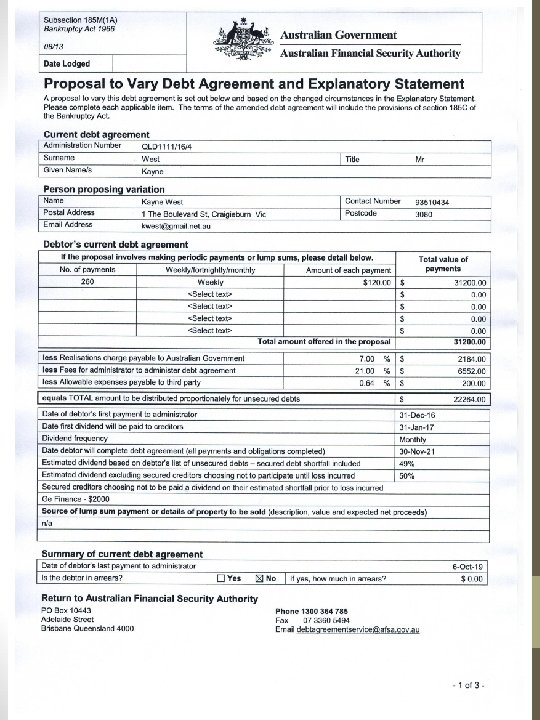

Varying a Debt Agreement by a debtor • Should be considered for debtors with significant changes in circumstances • New budget & financial statement is drawn up (Administrator’s duties still apply) • Any changes from the original proposal are disclosed to creditors (proof required) • Variation proposal lodged with AFSA. Again more than 50% of creditors vote on it’s acceptance • If not accepted original proposal remains in place

3 years later………… • Variation or Termination?

Facts 3 years later…………………………… Joint Circumstances: Both Kim and Kayne’s Debt Agreements were accepted by more than 50% of their creditors. Unfortunately, one of Kim and Kayne’s children has been diagnosed with a serious illness They’ve changed their mortgage to interest only. Equity in the property hasn’t changed since the original Debt Agreements were accepted. Kim: Her original Debt Agreement was paid out and a Completion Certificate sent to AFSA. Kim’s creditors were notified by AFSA and her NPII and Credit History should be updated to reflect this. The balance of Kim’s Super Income Protection Insurance Claim received another $10, 000 which was spent on a family holiday. Her health has further deteriorated and no longer able to drive. Kayne now drives her car and is unsecured to any loans.

• Kayne: Kayne has maintained his Debt Agreement payments as promised and has a balance of $12, 480 with 2 years of payments to go. • Kayne is forced to reduce his hours to help with the care of his daughter and wife. His income is now approximately $1, 252. 30 per week. • Kayne sold his Jeep Cherokee and paid out GE Finance in full • A new Statement of Financial Position shows there is not enough money to maintain the Debt Agreement Proposal payments

Suggestions and to what should Kayne do? Ask Creditors for a Variation? Why? Ask Creditors for a Termination? Why? Can he do both?

Terminating a Debt Agreement • Creditors may apply for termination • Debtors may apply for termination • Terminations are lodged with AFSA Creditors vote on the acceptance of a termination • If a debtor hasn’t made a payment for 6 months, it is automatically terminated • Debtors cannot go bankrupt without the Debt Agreement being terminated (unless terminated by a court)

‘As the nation’s credit card bill hit’s a staggering $51. 3 billion’, consumers are using plastic to just complete their weekly supermarket shops”

56222b5424eb219fa48cc1a400220c53.ppt