392fcbe1ef2d48462d20d144ead64b35.ppt

- Количество слайдов: 55

Options for Dealing with Systemic Banking Crises Bernard Lietaer blietaer@earthlink. net WAAS Hyderabad

- $17")

Losses Acknowledged to September 2008 • • • • Lehman Brothers (USA) - $17 billion (bankrupt) Bear Stearns (USA) - $3. 2 billion (bankrupt) Merrill Lynch (USA) - $46 billion (acquired) JP Morgan (USA) - $5 billion (reformed to bank holding company) Morgan Stanley (USA) - $12 billion (reformed) Citigroup (USA) - $47 billion Bank of America - $7 billion Goldman Sachs (USA) - $3. 8 billion Wachovia (USA) - $6 billion UBS (Swiss) - $37 billion Credit Suisse (Swiss) - $6 billion Northern Rock Bank (UK) – £ 50 billion + (went bankrupt) Royal Bank of Scotland (UK) - $11. 8 billion • • • • Barclays Bank (UK) - $9. 9 billion HSBC (Bank, UK) - $6 billion HBOS (Bank, UK) - $2 billion Lloyds TSB Bank (UK) - $1. 7 billion Deutsche Bank (Germany) - $10 billion Bayern. LB (Germany) - $3 billion IKB (Germany) - $2. 6 billion Commerzbank (Germany) - $1. 1 billion West. LB (Germany) - $1. 5 billion Credit Agricole (France) - $7 billion Societe Generale (France) - $6 billion Nataxis (France) - $4. 3 billion Uni. Credit (Italy) - $1. 6 billion National Australia Bank - $1 billion • Total acknowledged to August 2008: $ 358. 7 billion out of a total subprime losses of $ 1200 billion…

In short, our global financial system is in…

Implications? • “Let's recognize that this is a once-in-a-halfcentury, probably once-in-a-century type of event. ” Alan Greenspan => back to the 1930 s? • “This recession will be long, ugly, painful and deep. ” Nouriel Roubini, Prof NY University • Last time we dealt with a crisis of this size, we “solved it” by creating widespread fascism and WW 2 – Can we do better this time?

Plan • • Why Save the Banks? Symptom Alleviation Options Systemic Cause Systemic Options Pros and Cons My Proposal Conclusions

Why Save the Banks? • Lesson from the 1930 s: “ 2 d Wave” Crisis – When many banks bankrupt at the same time they trigger a “ 2 d Wave” recession in the “real economy” – Reason: banks stop financing “real economy” • Banks have monopoly of issuing legal tender => Strangulation of all other economic sectors • Consequence: “Moral Hasard”: – “Too Big to Fail” banks take high risks – If profitable => private winnings – If failed => governments will bail them out…

• • • Sweden USA Spain Japan Venezuela")

Costs of Bank Bailouts (% GDP) • • • Sweden USA Spain Japan Venezuela Mexico Chili Thailand Malaysia Argentina South Korea 1991 1988 1977 -85 1997 1994 -5 1994 1981 -83 1997 -98 1980 -82 1997 -98 • USA 2008 (so far) 3. 6% 3. 7% 16. 8% 24% 18% 19. 3% 41. 2% 45% 55. 3% 60% 5. 8%

Plan • • Why Save the Banks? Symptom Alleviation Options Systemic Cause Systemic Options Pros and Cons My Proposal Conclusions

Symptom Alleviation Options • Nationalizing the Problem Assets – Preferred by banking system – US approach – Most expensive solution because un-leveraged • Nationalizing the Banks – European approach – Leverage of bank capital to money creation (minimum x 10) – NB: Actual leverage ratio: Deutsche Bank 1. 2% UBS 2. 1% Barclays 2. 4%

Unresolved Problems of Conventional Solutions • “ 2 d Wave” problem only partially solved – Banks restart lending normally only after their balance sheet is restored – Even with bailouts, takes minimum 3 -6 years • When large scale problem: 2 d Wave vicious circle – Bad bank balance sheet => lending restrictions => recession => worsens banks’ balance sheet => more lending restrictions…=> depression? • Deals only with central institutions problems – Bankruptcy of financial institutions that are not “too big to fail” – Local and State governments in financial trouble… • Further worsens unemployment and social problems • Example: New York has to cut 2009 budget by US 1. 5 Billion…

Plan • • Why Save the Banks? Symptom Alleviation Options Systemic Cause Systemic Options Pros and Cons My Proposal Conclusions

Symptoms of Systemic Cause? • This is the biggest but not the first such crisis – World bank identified 96 banking crises and 176 monetary crises in recent 20 year period – Such crisis are a remarkably “hardy perennial” (Kindleberger) • 48 well documented major crashes between 1637 and 1929. – Happened under very different regulatory systems, different countries, at different development levels, at very different times… • My claim: financial system is systemically unstable – “An accident waiting to happen” explains also why huge efforts by very bright and dedicated people (in central banks and private financial system) repeatedly fail to avoid crashes…

Complexity Theory • Robert Ulanowicz: 25 years of quantitative modeling of real-life ecosystems using complexity, information and network theory • Key finding: Sustainability is measurable with a single metric as an optimal balance between “throughput efficiency” and “rebound capacity”. • NB: Emergent properties from a network structure are independent from what is being processed: biomass in an ecosystem, electrons in electrical circuit, money in an economy…

(Diversity + Interconnections) Throughput Efficiency (A) (Streamlined)")

Sustainability in Natural Ecosystems Rebound capacity (F) (Diversity + Interconnections) Throughput Efficiency (A) (Streamlined) 0% 100% Optimum Sustainability

(Diversity + Interconnections) Throughput Efficiency")

“Window of Vitality” in Natural Ecosystems Rebound capacity (F) (Diversity + Interconnections) Throughput Efficiency (A) (Streamlined) 0% “Window of Vitality” 100% Optimum Sustainability

(Diversity + Interconnections) Throughput Efficiency (A) (Streamlined)")

Application to Monetary System Rebound capacity (F) (Diversity + Interconnections) Throughput Efficiency (A) (Streamlined) 0% Current operation of Financial system “Window of Vitality” Effect of Monopoly Of Conventional Money 100% Optimum Sustainability

Rebound capacity (F) (Diversity + Interconnections) Throughput Efficiency (A)")

Application to Monetary System (2) Rebound capacity (F) (Diversity + Interconnections) Throughput Efficiency (A) (Streamlined) 0% Current operation of Financial system “Window of Vitality” Optimum Effect of Complementary Currencies 100% Sustainability

Plan • • Why Save the Banks? Symptom Alleviation Options Systemic Cause Systemic Options Pros and Cons My Proposal Conclusions

Systemic Solution #1 Nationalize the Money Creation Process • Money is a public good, that was first privatized in favor of banks in 17 th century, to finance wars – Anomaly: bailing out banks with bank-debt money reimbursed with interest by taxpayers? • Governments can spend money into existence – Banks become simply money brokers – Banks lend out what they receive in deposit Þ End of fractional reserve system => no bank failures anymore (However, will be fiercely resisted by bank system…) • Risk: politicizing money creation process can lead to hyper -inflation – However, fractional reserve process has also created periodic hyper -inflation…

accept")

Systemic Solution #2 Ending Monopoly of Bank-debt money • Governments (central and/or local) accept in partial payment of taxes carefully selected complementary currencies (other than bank-debt money). – Complementary currencies could be those created by local governments, or by corporations (b 2 b such as WIR, Terra), or even local non profits (social purpose currencies). – Very flexible (choice of currency, time, percent accepted, etc. ) – Example of partial precedent: Russia accepted payment of taxes in copper during rubble crisis. • Doesn’t end privilege of bank-debt money as legal tender, only temporarily their monopoly. . . – Doesn’t end the banks’ business model – Complementary currency management can in fact be a new banking service • Criticism: less efficient…but that is exactly what is recommended

Plan • • Why Save the Banks? Symptom Alleviation Options Systemic Cause Systemic Options Pros and Cons My Proposal Conclusions

Options for Managing Banking Crises Approach Taxpayers/ Central Governments Bankers Local Governments 2 d Wave Systemic Cause delayed Unaddressed Conventional Nationalizing Problem Assets Most Expensive Preferred Nationalizing Banks Unconventional Nationalizing Money Creation Complementary Currencies (no leverage) Equity Dilution End of current business model Unaddressed 10 x leverage Unaddressed delayed Unaddressed LT solution (but inflation? ) Unaddressed Governments spend money into existence Unaddressed LT & ST solution Systemic Solution ‘ End of monopoly of money creation LT solution

Plan • • Why Save the Banks? Symptom Alleviation Options Systemic Cause Systemic Options Pros and Cons My Proposal Conclusions

My Proposal • Bailouts will happen in any case, and my proposal kicks in if and only if the recession or depression of “ 2 d Wave” starts biting… • Temporarily, while banks can’t fulfill their funding role at appropriate levels, have local and states accept partial payment of taxes in selective and robust complementary currencies – Selection of currencies can be lined up with political objectives – Start with robust B 2 B currencies (because best auditable) – Implement WIR and Terra type systems… • Complementary currencies are useful to solve problems even without any crisis – Over time, local and state governments can encourage them in other ways than acceptance in taxes in the future

Plan • • Why Save the Banks? Symptom Alleviation Options Systemic Cause Systemic Options Pros and Cons My Proposal Conclusions

Conclusions • Re-regulation is necessary and will be on everybody’s agenda, but it can only make such crises less frequent, not eliminate them. • We can do better than in the 1930 s – avoiding fascism and a World War? – but only if we consider systemic options… • The systemic option of complementary currency is – within the political decision power of local and state governments – Very flexible in terms of how and for what it is implemented – An acceptable compromise for banking system?

Follow up

Key Points • Systemic problems in Today’s International Money System Ø “We now have a non-system” Schmidt, Chancellor of Germany Ø “We need a new Global Currency” Paul Volcker, ex-Chairman Federal Reserve Board Ø “I foresee private currency markets in the 21 st century” Alan Greenspan, Chairman, Federal Reserve Board • Growing Risk of a Global Recession or Depression Both problems solved by a business initiative to create Terra, a new Electronic International Complementary Currency A Complementary Currency is a medium of exchange circulating in parallel with - not replacing - conventional currencies. Familiar example of complementary currency: Frequent Flier Miles

A better way?

Four Systemic Problems with Today’s Money System 1. Financial Instabilities The current banking crisis is #97 over past two decades 2. World Bank No International Standard of Value Currency Risk now dominant risk in International Business • • 3. When coverage is available hedging costs are incurred. When coverage not available (e. g. LDCs), less investments lead to despair and ultimately extremism/terrorism. Pro-cyclical Money Creation amplifies business cycle Today’s money created as bank-debt • • Ø 4. During booms, credit is easy => more boom During busts, no credit is available => worse bust Roller-coaster in sales, payments, staff hiring and firing “Short-termism” Unsustainable strategies • Discounted cash-flow with positive interest rate currency => long-term irrelevant

While effective conventional solutions are…

Presentation Outline 1. 2. 3. 4. The Problems Solution Win-Win Strategy Current Status of Project

Solutions are not to be found within the box

Thinking out of the Box? “Never, think outside the box. ”

Proposed Solution Definition • Terra = reference unit defined as standardized basket of key internationally traded commodities & services Example: 100 Terra = 1 barrel of oil + 10 bushels of wheat + 20 kg of copper … + 1/10 of ounce of gold NB: any standardizable good or service can be included – Similar stability to gold standard, but with basket instead of single commodity (more stable than any one component) Þ more stable than today’s national currencies Þ 4 fold reduction of volatility compared to US$ on basis of 9 -12 commodity basket – Terra is Inflation-resistant by definition

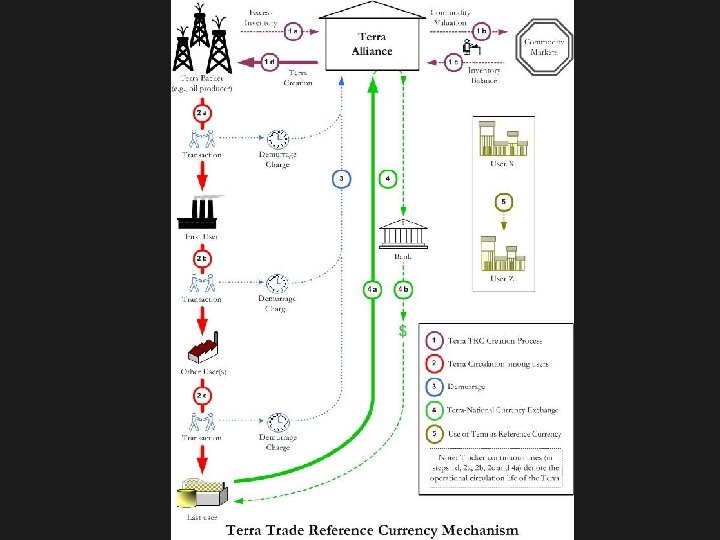

Issuing Mechanism • Terra Alliance (user’s alliance) issues Terra as inventory")

Proposed Solution (2) Issuing Mechanism • Terra Alliance (user’s alliance) issues Terra as inventory receipts for goods sold to it by producers – Example: oil company sells 1 million barrels to Terra Alliance, and gets credited with Terras at market prices, and can use Terras to pay suppliers… • Fully backed currency => Robust currency • Storage costs of basket is paid by the bearer of the Terra = demurrage of 3. 5 -4. 0% per year => Terras pure medium of exchange and contracts, not store of value • When recession looms => excess inventories of commodities => more Terras in circulation => activates economy in countercycle with economy

Legal/Tax Aspects - From legal and tax viewpoint: Terra is simply")

Proposed Solution (3) Legal/Tax Aspects - From legal and tax viewpoint: Terra is simply standardized “countertrade” (international barter) – – - Volume of countertrade now over $1 Trillion/year, more than 10% of all international trade, growing at 15%/year Example: Pepsi-Cola gets paid in Russia with Stolichnaya Vodka No need for new international treaty or governmental legislation

Presentation Outline 1. 2. 3. 4. Defining the Problems Solution Win-Win Strategy Current Status of Project

Win-win Strategy • Reasons for blockage of previous proposals: – They were all trying to replace the official money system • In contrast, Terra is complementary currency – They were expensive in implementation • In contrast, Terra operation is completely selffinancing – They were upsetting substantial vested interest • In contrast, Terra is a win-win for all key parties

Advantages for business users • More stable and predictable international currency")

Win-win Strategy (2) Advantages for business users • More stable and predictable international currency – No or less hedging costs – No or less inflation • Countercyclical – Less roller-coaster of business cycle – Less roller-coaster in finding staff and then firing them • Less Short-termism – Demurrage charge realigns financial interests with longer-term thinking – Leaving a better world for our grand-children…

How does one convince a corporate elephant to change? Regulation Education Financial Incentive

10")

Sustainability: The Monetary Engine What do we invest in? Physical Reality (Tree Metaphor) 10 years Costs: 10 $ $ 100 years $ 1, 000 Costs: 10 $ Currency with Positive Interest @ 5%/year $ 61. 39 Financial Viewpoint $7. 60 Value discounted to today: Currency with Demurrage @ 5%/year Demurrage = time-related charge (opposite of interest) $ 167. 02 $ 168, 903. 82 Value discounted to today: ÞShort-term thinking is not intrinsic to human nature, but created by today’s money system Þ NB: Historical Precedents: Dynastic Egypt, “Age of Cathedrals”

Benefits for everybody • Makes Sustainability a realistic global objective =>Reversing")

Win/win Solution (4) Benefits for everybody • Makes Sustainability a realistic global objective =>Reversing the hourglass?

Benefits for everybody • Makes Sustainability a realistic global objective •")

Win/win Solution (5) Benefits for everybody • Makes Sustainability a realistic global objective • Terra countercyclical less instability in jobs

Main lesson from the Euro…

Follow-up Texts available: • • “Terra/TRC Summary” and “Terra/TRC White Paper” on www. terratrc. org “Of Human Wealth” (new synthesis book) “The Future of Money” (London: Random House): www. amazon. co. uk “The Future of Payment Systems” White Paper for banking sector (available for free on request via email). Internet: – www. terratrc. org dedicated website opened today – Email: blietaer@earthlink. net

Two Implicit Hypotheses in Economics 1. Money is “value neutral” – – 2. Our money system is a given, like the number of planets in the solar system… • • • Money is a passive medium of exchange that simply facilitates exchanges. The type of money used doesn’t affect the kind of transactions performed, doesn’t influence the investments made, or the relationships among their users. Because of hypothesis #1, the monopoly of national money doesn’t matter. The monopoly of national money is more “efficient” 100% of economic theory built on these hypotheses. – Both hypotheses have been proven invalid! – What becomes possible if we revisit them? => Addressing systems rather than symptoms…

Advantages for initiators • Co-designing the system • A way to")

Win-win Strategy (1) Advantages for initiators • Co-designing the system • A way to change illiquid assets (inventory) into working capital • Now: inventories are a cost item • With Terra: negligible costs for getting working capital • New strategic option whenever excess inventories • Now: either store at own costs or dump in market (further value reduction) • With Terra: sell to Terra Alliance that will keep it in storage, and storage costs for bearers of Terra • More cost effective countertrade • Now: typical costs 3 -5% of face value • With Terra: costs approx 0. 1% of face value • + All advantages of other business users

Benefits to the Banking Sector • Today, banks don’t play any")

Win/win Solution (3) Benefits to the Banking Sector • Today, banks don’t play any role in countertrade (up to 10 -15% of global trade and fastest growing sector) – Standardization introduced by Terra enables financial sector to provide its traditional services similar to any foreign exchange transaction (accounts, transfers, advice) • Terra is only contractual and planning instrument – Financing remains in conventional currency created by banking system • Terra is countercyclical stabilizes world economy – Positive impact on banking portfolios – Makes job of Central Banks easier

Win/win Solution 2. Benefits for Corporate Initiators “Side Effects” Today’s Way “Terra Bridge” Way Costs: Currency Risks (Hedging costs) Drop in LDC Investments Opportunity Costs: Foregone investments (ex: in LDCs) Misallocation Costs Poverty Social Adaptation Costs Political instability Ecological Degradation Standard Basket Stable Reference Value Anticyclical Dampening of Business Cycle Demurrage No Standard of Value Long-term thinking profitable Costs: Adaptations to business cycle Opportunity Costs: Operational Investments suboptimal Amplification of Business Cycle Costs: Regulatory Pressures Opportunity Costs: Long-term Investments suboptimal Expensive in direct costs and opportunity costs Short-termism 1. Cost Reductions - reduced storage costs - reduced hedging costs 2. More Stable Global Trade 3. Realigns financial interest with long -term view

LDCs Worldbank Commercial banks LDC “Terra Bridge” IMF Adjustment Programs Debts")

Win/win solution (3) LDCs Worldbank Commercial banks LDC “Terra Bridge” IMF Adjustment Programs Debts in hard Currencies Commodity Production Problems Poverty, Development Failure Dumping Terra issued directly Currencies FDI Scarcity of Hard to Producers Degradation of Terms of Trades Countercycli cal Storage Costs Wealth Creation by and in LDCs

392fcbe1ef2d48462d20d144ead64b35.ppt