f23addcc140a35db0af780f901cc815f.ppt

- Количество слайдов: 103

Jerry Rhinehart, CIC, CLU, Ch.") National Health Care Reform – PPACA – (Part 1) Jerry Rhinehart, CIC, CLU, Ch. FC, RHU Panama City, FL

National Health Care Reform – PPACA – (Part 1) Jerry Rhinehart, CIC, CLU, Ch. FC, RHU Panama City, FL

Areas to be Covered 1. What are some key terms that are associated with the NHCR? 2. What are recent changes to the NHCR since its implementation (March 23, 2010)? 3. What is the time-line of implementation regarding the various components of the NHCR? 4. What are the potential penalties to individuals for non-compliance? 5. What are potential penalties and incentives that might impact employers? 1

Areas to be Covered 1. What are some key terms that are associated with the NHCR? 2. What are recent changes to the NHCR since its implementation (March 23, 2010)? 3. What is the time-line of implementation regarding the various components of the NHCR? 4. What are the potential penalties to individuals for non-compliance? 5. What are potential penalties and incentives that might impact employers? 1

e the se not Plea AIMER DISCL 2

e the se not Plea AIMER DISCL 2

NHR - 100 Years in the Making 3 6

NHR - 100 Years in the Making 3 6

Patient Protection and Affordability Care Act } Signed in to law March, 2010 } Health. Care. gov 7

Patient Protection and Affordability Care Act } Signed in to law March, 2010 } Health. Care. gov 7

8

8

Patient Protection and Affordability Care Act } NAHU. org } KFF. org (Henry J. Kaiser Family Foundation) } aetna. com/health-reformconnection/index. html 8

Patient Protection and Affordability Care Act } NAHU. org } KFF. org (Henry J. Kaiser Family Foundation) } aetna. com/health-reformconnection/index. html 8

9

9

9

9

9

9

10

10

10

10

Introduction to Key ACA Terms MLR (Medical Loss Ratio – 80% Small Group and Individual – 85% Large Group) (eff 01 -01 -2011) Example of NAIC Calculation Model for MLR Refunds: Total Premium received by the insurer from the enrollee (minus applicable taxes & fees) $400 x 12 = $4, 800 X The difference between the required MLR and the insurer’s MLR = x 80% - 77% = 3% = Rebate $144 Note: Insurers must make the 1 st round of rebates to affected consumers by August 2012 11

Introduction to Key ACA Terms MLR (Medical Loss Ratio – 80% Small Group and Individual – 85% Large Group) (eff 01 -01 -2011) Example of NAIC Calculation Model for MLR Refunds: Total Premium received by the insurer from the enrollee (minus applicable taxes & fees) $400 x 12 = $4, 800 X The difference between the required MLR and the insurer’s MLR = x 80% - 77% = 3% = Rebate $144 Note: Insurers must make the 1 st round of rebates to affected consumers by August 2012 11

Introduction to Key ACA Terms nt does NOT LR requireme NOTE: The M lly or partially RISA plans - fu apply to E on page 12. unded. See note self-f 12

Introduction to Key ACA Terms nt does NOT LR requireme NOTE: The M lly or partially RISA plans - fu apply to E on page 12. unded. See note self-f 12

Introduction to Key ACA Terms MLR (Medical Loss Ratio – 80% Small Group and Individual – 85% Large Group) (eff 01 -01 -2011) "The National Association of Insurance Commissioners estimates that Americans would have received nearly $2 billion if MLR had been in effect in 2010. ” Consumers Union (01/2012) Note: Insurers must make the 1 st round of rebates to affected consumers by August 2012 11

Introduction to Key ACA Terms MLR (Medical Loss Ratio – 80% Small Group and Individual – 85% Large Group) (eff 01 -01 -2011) "The National Association of Insurance Commissioners estimates that Americans would have received nearly $2 billion if MLR had been in effect in 2010. ” Consumers Union (01/2012) Note: Insurers must make the 1 st round of rebates to affected consumers by August 2012 11

Introduction to Key ACA Terms MLR (Medical Loss Ratio – 80% Small Group and Individual – 85% Large Group) (eff 01 -01 -2011) FPL (Federal Poverty Level – 133% - 400%) (eff 0101 -2014) 11

Introduction to Key ACA Terms MLR (Medical Loss Ratio – 80% Small Group and Individual – 85% Large Group) (eff 01 -01 -2011) FPL (Federal Poverty Level – 133% - 400%) (eff 0101 -2014) 11

Federal Poverty Level (FPL) – National Incomes (Gross)") Key Provisions of Insurance Reform (2014) Federal Poverty Level (FPL) – National Incomes (Gross) except for Hawaii and Alaska - 2011 - 2012 Income Single Family of 4 100% FPL 133% FPL 400% FPL $10, 890 $14, 484 $43, 560 $22, 350 $29, 726 $89, 400 Note: Incomes shown are approximate Source: KFF. org and Federal Government (Federal Register, January 20, 2011 - Vol 76, pp 3637 -3638 – see http: //aspe. hhs. gov/poverty/10 poverty. shtml 11

Key Provisions of Insurance Reform (2014) Federal Poverty Level (FPL) – National Incomes (Gross) except for Hawaii and Alaska - 2011 - 2012 Income Single Family of 4 100% FPL 133% FPL 400% FPL $10, 890 $14, 484 $43, 560 $22, 350 $29, 726 $89, 400 Note: Incomes shown are approximate Source: KFF. org and Federal Government (Federal Register, January 20, 2011 - Vol 76, pp 3637 -3638 – see http: //aspe. hhs. gov/poverty/10 poverty. shtml 11

Introduction to Key ACA Terms MLR (Medical Loss Ratio – 80% Small Group and Individual – 85% Large Group) (eff 01 -01 -2011) FPL (Federal Poverty Level – 133% - 400%) (eff 0101 -2014) FTE (Full Time Employee – 30 hours per week) 11

Introduction to Key ACA Terms MLR (Medical Loss Ratio – 80% Small Group and Individual – 85% Large Group) (eff 01 -01 -2011) FPL (Federal Poverty Level – 133% - 400%) (eff 0101 -2014) FTE (Full Time Employee – 30 hours per week) 11

Introduction to Key ACA Terms MLR (Medical Loss Ratio – 80% Small Group and Individual – 85% Large Group) (eff 01 -01 -2011) FPL (Federal Poverty Level – 133% - 400%) (eff 0101 -2014) FTE (Full Time Employee – 30 hours per week) (eff 01 -01 -2014) Health Insurance Exchange (eff 01 -01 -2014) 11

Introduction to Key ACA Terms MLR (Medical Loss Ratio – 80% Small Group and Individual – 85% Large Group) (eff 01 -01 -2011) FPL (Federal Poverty Level – 133% - 400%) (eff 0101 -2014) FTE (Full Time Employee – 30 hours per week) (eff 01 -01 -2014) Health Insurance Exchange (eff 01 -01 -2014) 11

Introduction to Key ACA Terms MLR (Medical Loss Ratio – 80% Small Group and Individual – 85% Large Group) (eff 01 -01 -2011) FPL (Federal Poverty Level – 133% - 400%) (eff 0101 -2014) FTE (Full Time Employee – 30 hours per week) (eff 01 -01 -2014) Health Insurance Exchange (eff 01 -01 -2014) Exchange Navigators (eff 01 -01 -2014) 11

Introduction to Key ACA Terms MLR (Medical Loss Ratio – 80% Small Group and Individual – 85% Large Group) (eff 01 -01 -2011) FPL (Federal Poverty Level – 133% - 400%) (eff 0101 -2014) FTE (Full Time Employee – 30 hours per week) (eff 01 -01 -2014) Health Insurance Exchange (eff 01 -01 -2014) Exchange Navigators (eff 01 -01 -2014) 11

– DELAYED - Now voluntary for 2011.") Recent Legislative Changes W-2 Reporting (Fall 2010) – DELAYED - Now voluntary for 2011. Implementation begins in 2012 for ALL ‘ERs that provide health insurance. 12

Recent Legislative Changes W-2 Reporting (Fall 2010) – DELAYED - Now voluntary for 2011. Implementation begins in 2012 for ALL ‘ERs that provide health insurance. 12

– DELAYED - Now voluntary for 2011.") Recent Legislative Changes W-2 Reporting (Fall 2010) – DELAYED - Now voluntary for 2011. Implementation begins in 2012 for ALL ‘ERs that provide health insurance. 1099 Reporting ($600) – Spring 2011 - REPEALED 12

Recent Legislative Changes W-2 Reporting (Fall 2010) – DELAYED - Now voluntary for 2011. Implementation begins in 2012 for ALL ‘ERs that provide health insurance. 1099 Reporting ($600) – Spring 2011 - REPEALED 12

– DELAYED - Now voluntary for 2011.") Recent Legislative Changes W-2 Reporting (Fall 2010) – DELAYED - Now voluntary for 2011. Implementation begins in 2012 for ALL ‘ERs that provide health insurance. 1099 Reporting ($600) – Spring 2011 - REPEALED Voucher option – Spring 2011 - REPEALED 12

Recent Legislative Changes W-2 Reporting (Fall 2010) – DELAYED - Now voluntary for 2011. Implementation begins in 2012 for ALL ‘ERs that provide health insurance. 1099 Reporting ($600) – Spring 2011 - REPEALED Voucher option – Spring 2011 - REPEALED 12

– DELAYED - Now voluntary for 2011.") Recent Legislative Changes W-2 Reporting (Fall 2010) – DELAYED - Now voluntary for 2011. Implementation begins in 2012 for ALL ‘ERs that provide health insurance. 1099 Reporting ($600) – Spring 2011 - REPEALED Voucher option – Spring 2011 - REPEALED CLASS (LTC Option) – Late-Summer 2011 – TABLED (U. S House of Representatives “repealed” it 02 -02 -2012) 12

Recent Legislative Changes W-2 Reporting (Fall 2010) – DELAYED - Now voluntary for 2011. Implementation begins in 2012 for ALL ‘ERs that provide health insurance. 1099 Reporting ($600) – Spring 2011 - REPEALED Voucher option – Spring 2011 - REPEALED CLASS (LTC Option) – Late-Summer 2011 – TABLED (U. S House of Representatives “repealed” it 02 -02 -2012) 12

Health Reform Implementation Timeline 2010 Insurance reforms 13

Health Reform Implementation Timeline 2010 Insurance reforms 13

Provide dependent coverage up to age 26 (eff") Key Provisions of Insurance Reforms (2010) Provide dependent coverage up to age 26 (eff 09 -23 -10) - Includes adult children that no longer attending college, those not living with their parents, and those adult children who are married (even with their own children). * This provision does not extend to the spouse or any children of the adult child being covered. - Applies to plans that already offer dependent coverage. If coverage exist, the ‘ER must inform ‘EEs that their children, who may have aged out of the plan, will again be eligible starting January 1, 2011. - Grandfathered plans will only provide coverage if dependents have no other ‘ER-sponsored coverage. 13

Key Provisions of Insurance Reforms (2010) Provide dependent coverage up to age 26 (eff 09 -23 -10) - Includes adult children that no longer attending college, those not living with their parents, and those adult children who are married (even with their own children). * This provision does not extend to the spouse or any children of the adult child being covered. - Applies to plans that already offer dependent coverage. If coverage exist, the ‘ER must inform ‘EEs that their children, who may have aged out of the plan, will again be eligible starting January 1, 2011. - Grandfathered plans will only provide coverage if dependents have no other ‘ER-sponsored coverage. 13

Provide dependent coverage up to age 26 (eff") Key Provisions of Insurance Reforms (2010) Provide dependent coverage up to age 26 (eff 09 -23 -10) - No coverage is required for children who are offered health benefits by their own employer. - This exemption expires 1 -1 -2014 when employers will be required to offer coverage to all children to age 26 – regardless of access to other employer coverage. 13

Key Provisions of Insurance Reforms (2010) Provide dependent coverage up to age 26 (eff 09 -23 -10) - No coverage is required for children who are offered health benefits by their own employer. - This exemption expires 1 -1 -2014 when employers will be required to offer coverage to all children to age 26 – regardless of access to other employer coverage. 13

Provide dependent coverage up to age 26 (eff") Key Provisions of Insurance Reforms (2010) Provide dependent coverage up to age 26 (eff 09 -23 -10) - No coverage is required for children who are offered health benefits by their own employer. - This exemption expires 1 -1 -2014 when employers will be required to offer coverage to all children to age 26 – regardless of access to other employer coverage. - The government has estimated that as many as 1. 6 million uninsured individuals ages 19 -25 will gain coverage in 2011 with an increase premium of: 0. 7% in 2011 1. 0% in 2012 1. 0% in 2013 13

Key Provisions of Insurance Reforms (2010) Provide dependent coverage up to age 26 (eff 09 -23 -10) - No coverage is required for children who are offered health benefits by their own employer. - This exemption expires 1 -1 -2014 when employers will be required to offer coverage to all children to age 26 – regardless of access to other employer coverage. - The government has estimated that as many as 1. 6 million uninsured individuals ages 19 -25 will gain coverage in 2011 with an increase premium of: 0. 7% in 2011 1. 0% in 2012 1. 0% in 2013 13

Prohibit individual and group plans from placing limits") Key Provisions of Insurance Reforms (2010) Prohibit individual and group plans from placing limits on coverage (eff 09 -23 -10) 13

Key Provisions of Insurance Reforms (2010) Prohibit individual and group plans from placing limits on coverage (eff 09 -23 -10) 13

Policy Limits (Annual and / Lifetime) - Lifetime") Key Provisions of Insurance Reforms (2010) Policy Limits (Annual and / Lifetime) - Lifetime limits prohibited on health coverage (2010) - Annual limits prohibited (2014)

Key Provisions of Insurance Reforms (2010) Policy Limits (Annual and / Lifetime) - Lifetime limits prohibited on health coverage (2010) - Annual limits prohibited (2014)

Policy Limits (Annual and / Lifetime) - Lifetime") Key Provisions of Insurance Reforms (2010) Policy Limits (Annual and / Lifetime) - Lifetime limits prohibited on health coverage (2010) - Annual limits prohibited (2014) (“Mini-Med” issue)

Key Provisions of Insurance Reforms (2010) Policy Limits (Annual and / Lifetime) - Lifetime limits prohibited on health coverage (2010) - Annual limits prohibited (2014) (“Mini-Med” issue)

Policy Limits (Annual and / Lifetime) - Lifetime") Key Provisions of Insurance Reforms (2010) Policy Limits (Annual and / Lifetime) - Lifetime limits prohibited on health coverage (2010) - Annual limits prohibited (2014) (“Mini-Med” issue) Effective 2014 No Plan Can Have an Annual Policy Limit and Phased in as Follows: 2011 - $750, 000 2012 - $1. 25 million 2013 - $2 million

Key Provisions of Insurance Reforms (2010) Policy Limits (Annual and / Lifetime) - Lifetime limits prohibited on health coverage (2010) - Annual limits prohibited (2014) (“Mini-Med” issue) Effective 2014 No Plan Can Have an Annual Policy Limit and Phased in as Follows: 2011 - $750, 000 2012 - $1. 25 million 2013 - $2 million

“WAIVERS” - As of Aug 30, 2011 there") Key Provisions of Insurance Reforms (2010) “WAIVERS” - As of Aug 30, 2011 there have been 1, 497 “waivers” granted by HHS. “Waivers” were granted for 1 year and then could be re-filed. - New “waivers” ended as of 09 -22 -11. To date @3 million EEs are “waived” – 1. 5 million are in Unions.

Key Provisions of Insurance Reforms (2010) “WAIVERS” - As of Aug 30, 2011 there have been 1, 497 “waivers” granted by HHS. “Waivers” were granted for 1 year and then could be re-filed. - New “waivers” ended as of 09 -22 -11. To date @3 million EEs are “waived” – 1. 5 million are in Unions.

Pre-existing conditions - Creates a temporary program to") Key Provisions of Insurance Reforms (2010) Pre-existing conditions - Creates a temporary program to provide health coverage to individuals with pre-existing medical conditions who have been uninsured for at least six months. The plan will be operated by the states or the federal government. - Children under age 19 cannot be denied insurance coverage due to a pre-existing condition. 13

Key Provisions of Insurance Reforms (2010) Pre-existing conditions - Creates a temporary program to provide health coverage to individuals with pre-existing medical conditions who have been uninsured for at least six months. The plan will be operated by the states or the federal government. - Children under age 19 cannot be denied insurance coverage due to a pre-existing condition. 13

Pre-existing conditions - Creates a temporary program to") Key Provisions of Insurance Reforms (2010) Pre-existing conditions - Creates a temporary program to provide health coverage to individuals with pre-existing medical conditions who have been uninsured for at least six months. The plan will be operated by the states or the federal government. - Children under age 19 cannot be denied insurance coverage due to a pre-existing condition. Tax credit to small employer (25 and under) that provide health insurance - with wage restrictions. (More discussion later) 13

Key Provisions of Insurance Reforms (2010) Pre-existing conditions - Creates a temporary program to provide health coverage to individuals with pre-existing medical conditions who have been uninsured for at least six months. The plan will be operated by the states or the federal government. - Children under age 19 cannot be denied insurance coverage due to a pre-existing condition. Tax credit to small employer (25 and under) that provide health insurance - with wage restrictions. (More discussion later) 13

Pre-existing conditions - Creates a temporary program to") Key Provisions of Insurance Reforms (2010) Pre-existing conditions - Creates a temporary program to provide health coverage to individuals with pre-existing medical conditions who have been uninsured for at least six months. The plan will be operated by the states or the federal government. - Children under age 19 cannot be denied insurance coverage due to a pre-existing condition. Tax credit to small employer (25 and under) that provide health insurance - with wage restrictions. (More discussion later) MLR (80% - 85%) Required “wellness” benefits for certain groups 13

Key Provisions of Insurance Reforms (2010) Pre-existing conditions - Creates a temporary program to provide health coverage to individuals with pre-existing medical conditions who have been uninsured for at least six months. The plan will be operated by the states or the federal government. - Children under age 19 cannot be denied insurance coverage due to a pre-existing condition. Tax credit to small employer (25 and under) that provide health insurance - with wage restrictions. (More discussion later) MLR (80% - 85%) Required “wellness” benefits for certain groups 13

Health Reform Implementation Timeline 2010 Insurance reforms Medicare Tax changes 13

Health Reform Implementation Timeline 2010 Insurance reforms Medicare Tax changes 13

Prevention / Wellness (Medicare) Tax Changes") Health Reform Implementation Timeline 2011 Long-term care (CLASS) Prevention / Wellness (Medicare) Tax Changes 14

Health Reform Implementation Timeline 2011 Long-term care (CLASS) Prevention / Wellness (Medicare) Tax Changes 14

New or revised taxes to help pay for") Key Provisions of Tax Changes (2011) New or revised taxes to help pay for NHCR - Exclude OTC drugs (not prescribed) from reimbursement or coverage under a CDHP (HSA, FSA, etc. ). Insulin is not included in this provision. - Increase tax / penalty from 10% to 20% on non-qualified distributions from CDHP - New annual fees on the pharmaceutical manufacturing sector 14

Key Provisions of Tax Changes (2011) New or revised taxes to help pay for NHCR - Exclude OTC drugs (not prescribed) from reimbursement or coverage under a CDHP (HSA, FSA, etc. ). Insulin is not included in this provision. - Increase tax / penalty from 10% to 20% on non-qualified distributions from CDHP - New annual fees on the pharmaceutical manufacturing sector 14

Health Reform Implementation Timeline 2012 Medicare 14

Health Reform Implementation Timeline 2012 Medicare 14

Health Reform Implementation Timeline 2012 NEW – 08/01/2012 (8 new preventive health benefits to women at no cost). They include: 14

Health Reform Implementation Timeline 2012 NEW – 08/01/2012 (8 new preventive health benefits to women at no cost). They include: 14

Health Reform Implementation Timeline 2012 NEW – 08/01/2012 (8 new preventive health benefits to women at no cost). They include: - contraceptives, breast-feeding supplies, screenings for gestational diabetes and sexually transmitted infections, and domestic violence, as well as routine check-ups for breast and pelvic exams, Pap tests, and prenatal care. 14

Health Reform Implementation Timeline 2012 NEW – 08/01/2012 (8 new preventive health benefits to women at no cost). They include: - contraceptives, breast-feeding supplies, screenings for gestational diabetes and sexually transmitted infections, and domestic violence, as well as routine check-ups for breast and pelvic exams, Pap tests, and prenatal care. 14

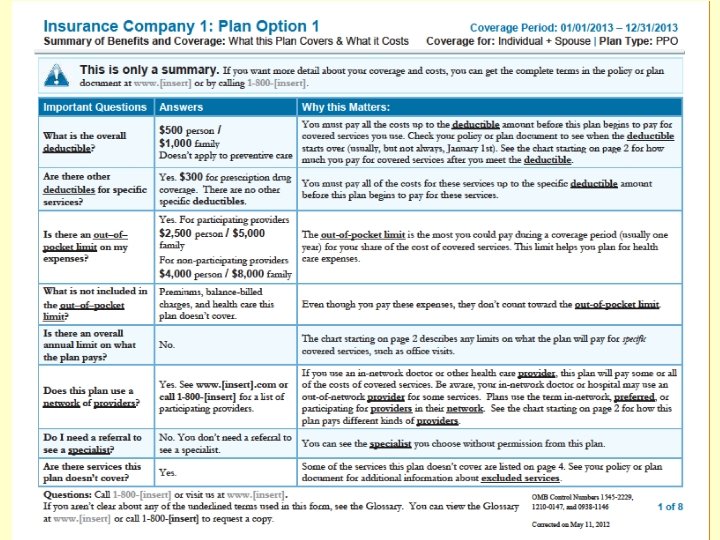

Health Reform Implementation Timeline 2012 Summary of Benefit (Standardized language – eff 09 -23 -12)

Health Reform Implementation Timeline 2012 Summary of Benefit (Standardized language – eff 09 -23 -12)

. gov hcare www. healt mary m Search: Su over efits and C of Ben age

. gov hcare www. healt mary m Search: Su over efits and C of Ben age

14") Health Reform Implementation Timeline 2013 Insurance Reforms (CO-OP - $6 Billion) 14

Health Reform Implementation Timeline 2013 Insurance Reforms (CO-OP - $6 Billion) 14

Medicare Tax Change") Health Reform Implementation Timeline 2013 Insurance Reforms (CO-OP - $6 Billion) Medicare Tax Change 15

Health Reform Implementation Timeline 2013 Insurance Reforms (CO-OP - $6 Billion) Medicare Tax Change 15

New or revised taxes to help pay for") Key Provisions of Tax Changes (2013) New or revised taxes to help pay for NHCR - Increase threshold for the itemized deduction for unreimbursed medical expenses from 7½% to 10% of AGI 15

Key Provisions of Tax Changes (2013) New or revised taxes to help pay for NHCR - Increase threshold for the itemized deduction for unreimbursed medical expenses from 7½% to 10% of AGI 15

New or revised taxes to help pay for") Key Provisions of Tax Changes (2013) New or revised taxes to help pay for NHCR - Increase threshold for the itemized deduction for unreimbursed medical expenses from 7½% to 10% of AGI - Increase the Medicare Part A tax rate on wages by 0. 9% (from 1. 45% to 2. 35%) on earnings over $200 K (individual) and $250 K (married/ filing jointly). 3. 8% assessment on unearned income (high income tax payers only) for retiree Medicare Part D 15

Key Provisions of Tax Changes (2013) New or revised taxes to help pay for NHCR - Increase threshold for the itemized deduction for unreimbursed medical expenses from 7½% to 10% of AGI - Increase the Medicare Part A tax rate on wages by 0. 9% (from 1. 45% to 2. 35%) on earnings over $200 K (individual) and $250 K (married/ filing jointly). 3. 8% assessment on unearned income (high income tax payers only) for retiree Medicare Part D 15

New or revised taxes to help pay for") Key Provisions of Tax Changes (2013) New or revised taxes to help pay for NHCR - Increase threshold for the itemized deduction for unreimbursed medical expenses from 7½% to 10% of AGI - Increase the Medicare Part A tax rate on wages by 0. 9% (from 1. 45% to 2. 35%) on earnings over $200 K (individual) and $250 K (married/ filing jointly). 3. 8% assessment on unearned income (high income tax payers only) - Max contribution to FSA for medical - $2, 500 per year 15

Key Provisions of Tax Changes (2013) New or revised taxes to help pay for NHCR - Increase threshold for the itemized deduction for unreimbursed medical expenses from 7½% to 10% of AGI - Increase the Medicare Part A tax rate on wages by 0. 9% (from 1. 45% to 2. 35%) on earnings over $200 K (individual) and $250 K (married/ filing jointly). 3. 8% assessment on unearned income (high income tax payers only) - Max contribution to FSA for medical - $2, 500 per year 15

New or revised taxes to help pay for") Key Provisions of Tax Changes (2013) New or revised taxes to help pay for NHCR - Increase threshold for the itemized deduction for unreimbursed medical expenses from 7½% to 10% of AGI - Increase the Medicare Part A tax rate on wages by 0. 9% (from 1. 45% to 2. 35%) on earnings over $200 K (individual) and $250 K (married/ filing jointly). 3. 8% assessment on unearned income (high income tax payers only) - Max contribution to FSA for medical - $2, 500 per year - Excise tax (2. 3%) on medical devices (hip replacement, xray machine, etc. – numerous exceptions exists) 15

Key Provisions of Tax Changes (2013) New or revised taxes to help pay for NHCR - Increase threshold for the itemized deduction for unreimbursed medical expenses from 7½% to 10% of AGI - Increase the Medicare Part A tax rate on wages by 0. 9% (from 1. 45% to 2. 35%) on earnings over $200 K (individual) and $250 K (married/ filing jointly). 3. 8% assessment on unearned income (high income tax payers only) - Max contribution to FSA for medical - $2, 500 per year - Excise tax (2. 3%) on medical devices (hip replacement, xray machine, etc. – numerous exceptions exists) 15

New or revised taxes to help pay for") Key Provisions of Tax Changes (2013) New or revised taxes to help pay for NHCR - Increase threshold for the itemized deduction for unreimbursed medical expenses from 7½% to 10% of AGI - Increase the Medicare Part A tax rate on wages by 0. 9% (from 1. 45% to 2. 35%) on earnings over $200 K (individual) and $250 K (married/ filing jointly). 3. 8% assessment on unearned income (high income tax payers only) - Max contribution to FSA for medical - $2, 500 per year - Excise tax (2. 3%) on medical devices (hip replacement, xray machine, etc. – numerous exceptions exists) - Eliminated ‘ER deduction for retiree Medicare Part D 15

Key Provisions of Tax Changes (2013) New or revised taxes to help pay for NHCR - Increase threshold for the itemized deduction for unreimbursed medical expenses from 7½% to 10% of AGI - Increase the Medicare Part A tax rate on wages by 0. 9% (from 1. 45% to 2. 35%) on earnings over $200 K (individual) and $250 K (married/ filing jointly). 3. 8% assessment on unearned income (high income tax payers only) - Max contribution to FSA for medical - $2, 500 per year - Excise tax (2. 3%) on medical devices (hip replacement, xray machine, etc. – numerous exceptions exists) - Eliminated ‘ER deduction for retiree Medicare Part D 15

Health Reform Implementation Timeline 2014 Individual and Employer Requirements 15

Health Reform Implementation Timeline 2014 Individual and Employer Requirements 15

Require U. S. citizens and legal immigrants to have") Individual and Employer Requirements (2014) Require U. S. citizens and legal immigrants to have qualified health coverage 15

Individual and Employer Requirements (2014) Require U. S. citizens and legal immigrants to have qualified health coverage 15

Require U. S. citizens and legal immigrants to have") Individual and Employer Requirements (2014) Require U. S. citizens and legal immigrants to have qualified health coverage - Phased-in tax penalty 15

Individual and Employer Requirements (2014) Require U. S. citizens and legal immigrants to have qualified health coverage - Phased-in tax penalty 15

Require U. S. citizens and legal immigrants to have") Individual and Employer Requirements (2014) Require U. S. citizens and legal immigrants to have qualified health coverage - Phased-in tax penalty This was the “INDIVIDUAL MANDATE” litigation ruled upon by the SCOTUS in June of 2012 15

Individual and Employer Requirements (2014) Require U. S. citizens and legal immigrants to have qualified health coverage - Phased-in tax penalty This was the “INDIVIDUAL MANDATE” litigation ruled upon by the SCOTUS in June of 2012 15

Require U. S. citizens and legal immigrants to have") Individual and Employer Requirements (2014) Require U. S. citizens and legal immigrants to have qualified health coverage - Phased-in tax penalty This was the “INDIVIDUAL MANDATE” litigation ruled upon by the SCOTUS in June of 2012 - Possible penalties to ‘ER (50 or more FTEs – 30 hrs) - Complex rules and variables 15

Individual and Employer Requirements (2014) Require U. S. citizens and legal immigrants to have qualified health coverage - Phased-in tax penalty This was the “INDIVIDUAL MANDATE” litigation ruled upon by the SCOTUS in June of 2012 - Possible penalties to ‘ER (50 or more FTEs – 30 hrs) - Complex rules and variables 15

Require U. S. citizens and legal immigrants to have") Individual and Employer Requirements (2014) Require U. S. citizens and legal immigrants to have qualified health coverage (some exemptions apply) Who: Individuals and their tax-dependents What type of Qualified Health Plan (QHP) coverage is required: Employer sponsored plans; Individuals plans (in or out of the Exchange); “Grandfathered” plans; Government sponsored plans (Medicare, Medicaid, etc) 15

Individual and Employer Requirements (2014) Require U. S. citizens and legal immigrants to have qualified health coverage (some exemptions apply) Who: Individuals and their tax-dependents What type of Qualified Health Plan (QHP) coverage is required: Employer sponsored plans; Individuals plans (in or out of the Exchange); “Grandfathered” plans; Government sponsored plans (Medicare, Medicaid, etc) 15

Those who fall under the “requirement” but fail to") Individual Non-Compliance - ACA (2014) Those who fall under the “requirement” but fail to carry at least the “Bronze” plans will be subject to a penalty: (the greater of…) - $95 per year in 2014, $325 in 2015, $695 in 2016 (half that amount for children under age 18), up to maximum of three times those penalty amounts per family, OR, - 1% of income above the tax filing threshold in 2014, 2% in 2015, and 2½% in 2016 16

Individual Non-Compliance - ACA (2014) Those who fall under the “requirement” but fail to carry at least the “Bronze” plans will be subject to a penalty: (the greater of…) - $95 per year in 2014, $325 in 2015, $695 in 2016 (half that amount for children under age 18), up to maximum of three times those penalty amounts per family, OR, - 1% of income above the tax filing threshold in 2014, 2% in 2015, and 2½% in 2016 16

Those who fall under the “requirement” but fail to") Individual Non-Compliance - ACA (2014) Those who fall under the “requirement” but fail to carry at least the “Bronze” plans will be subject to a penalty: (the greater of…) - $95 per year in 2014, $325 in 2015, $695 in 2016 (half that amount for children under age 18), up to maximum of three times those penalty amounts per family, OR, - 1% of income above the tax filing threshold in 2014, 2% in 2015, and 2½% in 2016 The ACA does NOT refer to this penalty as a “tax” - rather “shared responsibility payment” 16

Individual Non-Compliance - ACA (2014) Those who fall under the “requirement” but fail to carry at least the “Bronze” plans will be subject to a penalty: (the greater of…) - $95 per year in 2014, $325 in 2015, $695 in 2016 (half that amount for children under age 18), up to maximum of three times those penalty amounts per family, OR, - 1% of income above the tax filing threshold in 2014, 2% in 2015, and 2½% in 2016 The ACA does NOT refer to this penalty as a “tax” - rather “shared responsibility payment” 16

What are the Potential Financial Penalties to Individuals who") Individual Non-Compliance - ACA (2014) What are the Potential Financial Penalties to Individuals who do NOT carry insurance? - Family of Four (includes 2 children under age 18) $100 K Taxable - Income 2014 2015 2016 $100, 000 $285 $975 $2, 085 Income $1, 000 (1%) $2, 000 (2%) $2, 500 (2½%) The penalty is the greater of the two calculations 16

Individual Non-Compliance - ACA (2014) What are the Potential Financial Penalties to Individuals who do NOT carry insurance? - Family of Four (includes 2 children under age 18) $100 K Taxable - Income 2014 2015 2016 $100, 000 $285 $975 $2, 085 Income $1, 000 (1%) $2, 000 (2%) $2, 500 (2½%) The penalty is the greater of the two calculations 16

So… individuals (and their tax-dependents) will have to prove") Individual and Employer Requirements (2014) So… individuals (and their tax-dependents) will have to prove they have purchased a QHP in 2014? How does it appear this will happen? When you file your taxes you will have to attach documentation from your health insurance carrier, employer, or Exchange If you are a W-2 employee and your employer does provides a QHP they will have to provide that information on your W-2 (or similar documentation)

Individual and Employer Requirements (2014) So… individuals (and their tax-dependents) will have to prove they have purchased a QHP in 2014? How does it appear this will happen? When you file your taxes you will have to attach documentation from your health insurance carrier, employer, or Exchange If you are a W-2 employee and your employer does provides a QHP they will have to provide that information on your W-2 (or similar documentation)

Affect Employers –") January 01, 2014 How Might the National Health Care Reform (ACA) Affect Employers – Large (50 FTEs and more) and Small (less than 50 FTEs)?

January 01, 2014 How Might the National Health Care Reform (ACA) Affect Employers – Large (50 FTEs and more) and Small (less than 50 FTEs)?

… But First - What is the Combined Average Health Insurance Premium Paid by the ‘ER and ‘EE? (2010) Premiums for Group Health Insurance - Single - $4, 940 (annual) – 18% of ‘EEs provided a single health plan pay NONE of the cost - Family - $13, 877 (annual) – 10% of ‘EEs provided a family health plan pay NONE of the cost Source: Agency for Healthcare Research & Quality (AHRQ. gov)

… But First - What is the Combined Average Health Insurance Premium Paid by the ‘ER and ‘EE? (2010) Premiums for Group Health Insurance - Single - $4, 940 (annual) – 18% of ‘EEs provided a single health plan pay NONE of the cost - Family - $13, 877 (annual) – 10% of ‘EEs provided a family health plan pay NONE of the cost Source: Agency for Healthcare Research & Quality (AHRQ. gov)

… But First - What is the Combined Average Health Insurance Premium Paid by the ‘ER and ‘EE? (2010) Premiums for Group Health Insurance - Single - $4, 940 (annual) – 18% of ‘EEs provided a single health plan pay NONE of the cost - Family - $13, 877 (annual) – 10% of ‘EEs provided a family health plan pay NONE of the cost What is the average percentage paid by ‘EEs that DO pay a portion of the Health Insurance premium? - Single – 21% of the total premium - Family – 27% of the total premium Source: Agency for Healthcare Research & Quality (AHRQ. gov)

… But First - What is the Combined Average Health Insurance Premium Paid by the ‘ER and ‘EE? (2010) Premiums for Group Health Insurance - Single - $4, 940 (annual) – 18% of ‘EEs provided a single health plan pay NONE of the cost - Family - $13, 877 (annual) – 10% of ‘EEs provided a family health plan pay NONE of the cost What is the average percentage paid by ‘EEs that DO pay a portion of the Health Insurance premium? - Single – 21% of the total premium - Family – 27% of the total premium Source: Agency for Healthcare Research & Quality (AHRQ. gov)

Percent of Workers Offered Employer. Sponsored Insurance 1995, 2001, and 2005 Source: KFF. org (09/2010)

Percent of Workers Offered Employer. Sponsored Insurance 1995, 2001, and 2005 Source: KFF. org (09/2010)

What is the likelihood Employers will “Play or Pay”?") Employer Responsibility / Penalties (2014) What is the likelihood Employers will “Play or Pay”? Source: Towerwatson. com, May 2010

Employer Responsibility / Penalties (2014) What is the likelihood Employers will “Play or Pay”? Source: Towerwatson. com, May 2010

What is the likelihood Employers will “Play or Pay”?") Employer Responsibility / Penalties (2014) What is the likelihood Employers will “Play or Pay”? The Congressional Budget Office projects that 3. 9 million people will pay penalties under the law rather than buy insurance. (CBO 04/22/2010) Source: Towerwatson. com, May 2010

Employer Responsibility / Penalties (2014) What is the likelihood Employers will “Play or Pay”? The Congressional Budget Office projects that 3. 9 million people will pay penalties under the law rather than buy insurance. (CBO 04/22/2010) Source: Towerwatson. com, May 2010

Large Employer (50+ ‘EEs) - Full time employees (30") Employer Responsibility / Penalties (2014) Large Employer (50+ ‘EEs) - Full time employees (30 hrs) - Part time employees 16

Employer Responsibility / Penalties (2014) Large Employer (50+ ‘EEs) - Full time employees (30 hrs) - Part time employees 16

Large Employer (50+ ‘EEs) - Full time employees (30") Employer Responsibility / Penalties (2014) Large Employer (50+ ‘EEs) - Full time employees (30 hrs) - Part time employees Small Employer (1 to 49 ‘EEs) 16

Employer Responsibility / Penalties (2014) Large Employer (50+ ‘EEs) - Full time employees (30 hrs) - Part time employees Small Employer (1 to 49 ‘EEs) 16

Possible financial penalties for an ‘ER that DOES NOT") Employer Responsibility / Penalties (2014) Possible financial penalties for an ‘ER that DOES NOT offer coverage - If ANY FTE receives premium assistance (due to FPL) from the government (and through the Exchange) the ‘ER will face an annual fee of $2, 000 imposed on every full-time ‘EE (excluding the 1 st 30 ‘EEs). Penalties are pro-rated monthly. 16

Employer Responsibility / Penalties (2014) Possible financial penalties for an ‘ER that DOES NOT offer coverage - If ANY FTE receives premium assistance (due to FPL) from the government (and through the Exchange) the ‘ER will face an annual fee of $2, 000 imposed on every full-time ‘EE (excluding the 1 st 30 ‘EEs). Penalties are pro-rated monthly. 16

Possible financial penalties for an ‘ER that DOES NOT") Employer Responsibility / Penalties (2014) Possible financial penalties for an ‘ER that DOES NOT offer coverage - If ANY FTE receives premium assistance (due to FPL) from the government (and through the Exchange) the ‘ER will face an annual fee of $2, 000 imposed on every full-time ‘EE (excluding the 1 st 30 ‘EEs). Penalties are pro-rated monthly. - EXAMPLE … 16

Employer Responsibility / Penalties (2014) Possible financial penalties for an ‘ER that DOES NOT offer coverage - If ANY FTE receives premium assistance (due to FPL) from the government (and through the Exchange) the ‘ER will face an annual fee of $2, 000 imposed on every full-time ‘EE (excluding the 1 st 30 ‘EEs). Penalties are pro-rated monthly. - EXAMPLE … 16

For Employers That DO NOT Offer Coverage - An") Employer Responsibility / Penalties (2014) For Employers That DO NOT Offer Coverage - An ‘ER has 65 FTE workers, and does not offer coverage. There is at least one ‘EE who receives premium assistance from the gov’t - To determine the financial penalty - Deduct the 1 st 30 ‘EEs - Multiply remaining 35 by $2, 000 each - Annual penalty paid by the ‘ER 65 Total EEs - 30 35 x $2, 000 = $70, 000 16

Employer Responsibility / Penalties (2014) For Employers That DO NOT Offer Coverage - An ‘ER has 65 FTE workers, and does not offer coverage. There is at least one ‘EE who receives premium assistance from the gov’t - To determine the financial penalty - Deduct the 1 st 30 ‘EEs - Multiply remaining 35 by $2, 000 each - Annual penalty paid by the ‘ER 65 Total EEs - 30 35 x $2, 000 = $70, 000 16

For Employers That DO NOT Offer Coverage - An") Employer Responsibility / Penalties (2014) For Employers That DO NOT Offer Coverage - An ‘ER has 65 FTE workers, and does not offer coverage. There is at least one ‘EE who receives premium assistance from the gov’t - To determine the financial penalty - Deduct the 1 st 30 ‘EEs - Multiply remaining 35 by $2, 000 each - Annual penalty paid by the ‘ER 65 Total EEs - 30 35 x $2, 000 = $70, 000 16

Employer Responsibility / Penalties (2014) For Employers That DO NOT Offer Coverage - An ‘ER has 65 FTE workers, and does not offer coverage. There is at least one ‘EE who receives premium assistance from the gov’t - To determine the financial penalty - Deduct the 1 st 30 ‘EEs - Multiply remaining 35 by $2, 000 each - Annual penalty paid by the ‘ER 65 Total EEs - 30 35 x $2, 000 = $70, 000 16

Possible financial penalties for an ‘ER that DOES offer") Employer Responsibility / Penalties (2014) Possible financial penalties for an ‘ER that DOES offer coverage - If ANY FTE receives premium assistance (due to FPL) from the government (and through the Exchange) the ‘ER will face an annual fee of the lesser of $2, 000 imposed on every full-time ‘EE (excluding the 1 st 30 ‘EEs), OR $3, 000 for each FTE that receives a premium subsidy*. Penalties are prorated monthly. 16

Employer Responsibility / Penalties (2014) Possible financial penalties for an ‘ER that DOES offer coverage - If ANY FTE receives premium assistance (due to FPL) from the government (and through the Exchange) the ‘ER will face an annual fee of the lesser of $2, 000 imposed on every full-time ‘EE (excluding the 1 st 30 ‘EEs), OR $3, 000 for each FTE that receives a premium subsidy*. Penalties are prorated monthly. 16

Possible financial penalties for an ‘ER that DOES offer") Employer Responsibility / Penalties (2014) Possible financial penalties for an ‘ER that DOES offer coverage - If ANY FTE receives premium assistance (due to FPL) from the government (and through the Exchange) the ‘ER will face an annual fee of the lesser of $2, 000 imposed on every full-time ‘EE (excluding the 1 st 30 ‘EEs), OR $3, 000 for each FTE that receives a premium subsidy*. Penalties are prorated monthly. - EXAMPLE … 16

Employer Responsibility / Penalties (2014) Possible financial penalties for an ‘ER that DOES offer coverage - If ANY FTE receives premium assistance (due to FPL) from the government (and through the Exchange) the ‘ER will face an annual fee of the lesser of $2, 000 imposed on every full-time ‘EE (excluding the 1 st 30 ‘EEs), OR $3, 000 for each FTE that receives a premium subsidy*. Penalties are prorated monthly. - EXAMPLE … 16

For Employers That DO Offer Coverage - An ‘ER") Employer Responsibility / Penalties (2014) For Employers That DO Offer Coverage - An ‘ER has 65 FTE workers, and does offer coverage. There are 15 ‘EE who receives premium assistance from the government - To determine the financial penalty - Deduct the 1 st 30 ‘EEs - Multiply remaining 35 ‘EEs by $2, 000 each - Penalty paid by the ‘ER - OR - 15 ‘EEs receiving premium asst x $3, 000 - ‘ER assessed penalty – lesser of the two 65 Total EEs - 30 35 x $2, 000 = $70, 000 $45, 000 16

Employer Responsibility / Penalties (2014) For Employers That DO Offer Coverage - An ‘ER has 65 FTE workers, and does offer coverage. There are 15 ‘EE who receives premium assistance from the government - To determine the financial penalty - Deduct the 1 st 30 ‘EEs - Multiply remaining 35 ‘EEs by $2, 000 each - Penalty paid by the ‘ER - OR - 15 ‘EEs receiving premium asst x $3, 000 - ‘ER assessed penalty – lesser of the two 65 Total EEs - 30 35 x $2, 000 = $70, 000 $45, 000 16

For Employers That DO Offer Coverage - An ‘ER") Employer Responsibility / Penalties (2014) For Employers That DO Offer Coverage - An ‘ER has 65 FTE workers, and does offer coverage. There are 15 ‘EE who receives premium assistance from the government - To determine the financial penalty - Deduct the 1 st 30 ‘EEs - Multiply remaining 35 ‘EEs by $2, 000 each - Penalty paid by the ‘ER - OR - 15 ‘EEs receiving premium asst x $3, 000 - ‘ER assessed penalty – lesser of the two 65 Total EEs - 30 35 x $2, 000 = $70, 000 $45, 000 16

Employer Responsibility / Penalties (2014) For Employers That DO Offer Coverage - An ‘ER has 65 FTE workers, and does offer coverage. There are 15 ‘EE who receives premium assistance from the government - To determine the financial penalty - Deduct the 1 st 30 ‘EEs - Multiply remaining 35 ‘EEs by $2, 000 each - Penalty paid by the ‘ER - OR - 15 ‘EEs receiving premium asst x $3, 000 - ‘ER assessed penalty – lesser of the two 65 Total EEs - 30 35 x $2, 000 = $70, 000 $45, 000 16

For Employers That DO Offer Coverage - An ‘ER") Employer Responsibility / Penalties (2014) For Employers That DO Offer Coverage - An ‘ER has 65 FTE workers, and does offer coverage. There are 15 ‘EE who receives premium assistance from the government - To determine the financial penalty - Deduct the 1 st 30 ‘EEs - Multiply remaining 35 ‘EEs by $2, 000 each - Penalty paid by the ‘ER - OR - 15 ‘EEs receiving premium asst x $3, 000 - ‘ER assessed penalty – lesser of the two 65 Total EEs - 30 35 x $2, 000 = $70, 000 $45, 000 16

Employer Responsibility / Penalties (2014) For Employers That DO Offer Coverage - An ‘ER has 65 FTE workers, and does offer coverage. There are 15 ‘EE who receives premium assistance from the government - To determine the financial penalty - Deduct the 1 st 30 ‘EEs - Multiply remaining 35 ‘EEs by $2, 000 each - Penalty paid by the ‘ER - OR - 15 ‘EEs receiving premium asst x $3, 000 - ‘ER assessed penalty – lesser of the two 65 Total EEs - 30 35 x $2, 000 = $70, 000 $45, 000 16

") … How Do They Count as it Relates to the ACA? (2014)

… How Do They Count as it Relates to the ACA? (2014)

Sample Calculation of Part-Time Employee’s Hours - 2014 ‘EE Name Week 1 Week 2 Week 3 Week 4 Sue 5 5. 5 6 3. 5 Bill 8 6 4 3 Mary -09 4 4 Juan David Will Jerome Marion Rita Jason TOTAL 6. 5 5 10 6 9 4. 5 7 7 -05 6 -04. 5 7 5 10 5. 5 6 9 4. 5 7 8 4 7 6 5 4. 5 7 Month Total 20 21 17 26. 5 19 27. 5 24 23 18 28 224

Sample Calculation of Part-Time Employee’s Hours - 2014 ‘EE Name Week 1 Week 2 Week 3 Week 4 Sue 5 5. 5 6 3. 5 Bill 8 6 4 3 Mary -09 4 4 Juan David Will Jerome Marion Rita Jason TOTAL 6. 5 5 10 6 9 4. 5 7 7 -05 6 -04. 5 7 5 10 5. 5 6 9 4. 5 7 8 4 7 6 5 4. 5 7 Month Total 20 21 17 26. 5 19 27. 5 24 23 18 28 224

Joe’s Burgers & Shakes - 3 locations") Employer Responsibility / Penalties (2014) Joe’s Burgers & Shakes - 3 locations

Employer Responsibility / Penalties (2014) Joe’s Burgers & Shakes - 3 locations

Joe’s Burgers & Shakes - 3 locations - 40") Employer Responsibility / Penalties (2014) Joe’s Burgers & Shakes - 3 locations - 40 FTEs

Employer Responsibility / Penalties (2014) Joe’s Burgers & Shakes - 3 locations - 40 FTEs

Joe’s Burgers & Shakes - 3 locations - 40") Employer Responsibility / Penalties (2014) Joe’s Burgers & Shakes - 3 locations - 40 FTEs - 20 PTEs at 24 hrs per week (1920 hrs / month) 1920 ÷ 120 = 16 PTEs + 40 FTEs =

Employer Responsibility / Penalties (2014) Joe’s Burgers & Shakes - 3 locations - 40 FTEs - 20 PTEs at 24 hrs per week (1920 hrs / month) 1920 ÷ 120 = 16 PTEs + 40 FTEs =

Joe’s Burgers & Shakes - 3 locations - 40") Employer Responsibility / Penalties (2014) Joe’s Burgers & Shakes - 3 locations - 40 FTEs - 20 PTEs 20 PTE x 24 hrs x 4 = 1920 hrs / 120 (minimum FTE work hrs in a month) = 16 ‘EEs 20 PTEs at 24 hrs per week (1920 hrs / month) 1920 ÷ 120 = 16 PTEs + 40 FTEs =

Employer Responsibility / Penalties (2014) Joe’s Burgers & Shakes - 3 locations - 40 FTEs - 20 PTEs 20 PTE x 24 hrs x 4 = 1920 hrs / 120 (minimum FTE work hrs in a month) = 16 ‘EEs 20 PTEs at 24 hrs per week (1920 hrs / month) 1920 ÷ 120 = 16 PTEs + 40 FTEs =

Joe’s Burgers & Shakes - 3 locations - 40") Employer Responsibility / Penalties (2014) Joe’s Burgers & Shakes - 3 locations - 40 FTEs - 20 PTEs 20 PTE x 24 hrs x 4 = 1920 hrs / 120 (minimum FTE work hrs in a month) = 16 ‘EEs 20 PTEs at 24 hrs per week (1920 hrs / month) 1920 ÷ 120 = 16 PTEs + 40 FTEs = 56

Employer Responsibility / Penalties (2014) Joe’s Burgers & Shakes - 3 locations - 40 FTEs - 20 PTEs 20 PTE x 24 hrs x 4 = 1920 hrs / 120 (minimum FTE work hrs in a month) = 16 ‘EEs 20 PTEs at 24 hrs per week (1920 hrs / month) 1920 ÷ 120 = 16 PTEs + 40 FTEs = 56

Joe’s Burgers & Shakes - 3 locations - 40") Employer Responsibility / Penalties (2014) Joe’s Burgers & Shakes - 3 locations - 40 FTEs - 20 PTEs 20 PTE x 24 hrs x 4 = 1920 hrs / 120 (minimum FTE work hrs in a month) = 16 ‘EEs 20 PTEs at 24 hrs per week (1920 hrs / month) 1920 ÷ 120 = 16 PTEs + 40 FTEs = 56 - Joe is now considered a “LARGE EMPLOYER”

Employer Responsibility / Penalties (2014) Joe’s Burgers & Shakes - 3 locations - 40 FTEs - 20 PTEs 20 PTE x 24 hrs x 4 = 1920 hrs / 120 (minimum FTE work hrs in a month) = 16 ‘EEs 20 PTEs at 24 hrs per week (1920 hrs / month) 1920 ÷ 120 = 16 PTEs + 40 FTEs = 56 - Joe is now considered a “LARGE EMPLOYER”

Joe’s Burgers & Shakes – Coverage NOT Offered -") Employer Responsibility / Penalties (2014) Joe’s Burgers & Shakes – Coverage NOT Offered - ‘ER has 40 FTE workers, and does not offer coverage. There is at least one ‘EE who receives premium assistance from the gov’t - To determine the financial penalty - Deduct the 1 st 30 ‘EEs - Multiply remaining 10 by $2, 000 each - Annual penalty paid by the ‘ER 40 Total EEs - 30 10 x $2, 000 = $20, 000

Employer Responsibility / Penalties (2014) Joe’s Burgers & Shakes – Coverage NOT Offered - ‘ER has 40 FTE workers, and does not offer coverage. There is at least one ‘EE who receives premium assistance from the gov’t - To determine the financial penalty - Deduct the 1 st 30 ‘EEs - Multiply remaining 10 by $2, 000 each - Annual penalty paid by the ‘ER 40 Total EEs - 30 10 x $2, 000 = $20, 000

Joe’s Burgers & Shakes – Coverage IS Offered -") Employer Responsibility / Penalties (2014) Joe’s Burgers & Shakes – Coverage IS Offered - ‘ER has 40 FTE workers, and does offer coverage. There are 15 ‘EE who receives premium assistance from the government - To determine the financial penalty - Deduct the 1 st 30 ‘EEs - Multiply remaining 10 ‘EEs by $2, 000 each - Penalty paid by the ‘ER - OR - 15 ‘EEs receiving premium asst x $3, 000 - ‘ER assessed penalty – lesser of the two 40 Total EEs - 30 10 x $2, 000 = $20, 000 $45, 000 $20, 000

Employer Responsibility / Penalties (2014) Joe’s Burgers & Shakes – Coverage IS Offered - ‘ER has 40 FTE workers, and does offer coverage. There are 15 ‘EE who receives premium assistance from the government - To determine the financial penalty - Deduct the 1 st 30 ‘EEs - Multiply remaining 10 ‘EEs by $2, 000 each - Penalty paid by the ‘ER - OR - 15 ‘EEs receiving premium asst x $3, 000 - ‘ER assessed penalty – lesser of the two 40 Total EEs - 30 10 x $2, 000 = $20, 000 $45, 000 $20, 000

Consider this Scenario for the Uninformed Business Owner in") Employer Responsibility / Penalties (2014) Consider this Scenario for the Uninformed Business Owner in 2014

Employer Responsibility / Penalties (2014) Consider this Scenario for the Uninformed Business Owner in 2014

Consider this Scenario for the Uninformed Business Owner in") Employer Responsibility / Penalties (2014) Consider this Scenario for the Uninformed Business Owner in 2014 Mountain Top Resort - Golf Course and Lodge - 49 FETs - Provides NO QHP to its EEs

Employer Responsibility / Penalties (2014) Consider this Scenario for the Uninformed Business Owner in 2014 Mountain Top Resort - Golf Course and Lodge - 49 FETs - Provides NO QHP to its EEs

Consider this Scenario for the Uninformed Business Owner in") Employer Responsibility / Penalties (2014) Consider this Scenario for the Uninformed Business Owner in 2014 Mountain Top Resort - Golf Course and Lodge - 49 FETs - Provides NO QHP to its EEs - … so it pays NO ACA “shared responsibility penalty”

Employer Responsibility / Penalties (2014) Consider this Scenario for the Uninformed Business Owner in 2014 Mountain Top Resort - Golf Course and Lodge - 49 FETs - Provides NO QHP to its EEs - … so it pays NO ACA “shared responsibility penalty”

Consider this Scenario for the Uninformed Business Owner in") Employer Responsibility / Penalties (2014) Consider this Scenario for the Uninformed Business Owner in 2014 Mountain Top Resort - Golf Course and Lodge - 49 FETs - Provides NO QHP to its EEs - … so it pays NO ACA “shared responsibility penalty” - … but business gets better, so they hire a new EE (#50) for the entire year. Look what it will cost as mandated by the ACA:

Employer Responsibility / Penalties (2014) Consider this Scenario for the Uninformed Business Owner in 2014 Mountain Top Resort - Golf Course and Lodge - 49 FETs - Provides NO QHP to its EEs - … so it pays NO ACA “shared responsibility penalty” - … but business gets better, so they hire a new EE (#50) for the entire year. Look what it will cost as mandated by the ACA:

Consider this Scenario for the Uninformed Business Owner in") Employer Responsibility / Penalties (2014) Consider this Scenario for the Uninformed Business Owner in 2014 Mountain Top Resort - Golf Course and Lodge - 49 FETs - Provides NO QHP to its EEs - … so it pays NO ACA “shared responsibility penalty” - … but business gets better, so they hire a new EE (#50) for the entire year. Look what it will cost as mandated by the ACA: - $2, 000 x 20 (50 – 30) = $40, 000

Employer Responsibility / Penalties (2014) Consider this Scenario for the Uninformed Business Owner in 2014 Mountain Top Resort - Golf Course and Lodge - 49 FETs - Provides NO QHP to its EEs - … so it pays NO ACA “shared responsibility penalty” - … but business gets better, so they hire a new EE (#50) for the entire year. Look what it will cost as mandated by the ACA: - $2, 000 x 20 (50 – 30) = $40, 000

FPL and how it will work in 2014 (and") Employer Responsibility / Penalties (2014) FPL and how it will work in 2014 (and later) - Premium assistance for those individuals earning less than 400% of FPL. Currently (2011 -12 numbers) this is income at $43, 560 for an individual and $89, 400 for a family of four. - The premium assistance will INCREASE to the eligible individuals / families as the percentage of FPL goes DOWN.

Employer Responsibility / Penalties (2014) FPL and how it will work in 2014 (and later) - Premium assistance for those individuals earning less than 400% of FPL. Currently (2011 -12 numbers) this is income at $43, 560 for an individual and $89, 400 for a family of four. - The premium assistance will INCREASE to the eligible individuals / families as the percentage of FPL goes DOWN.

In terms of calculating potential penalties, part-time employees (and") Employer Responsibility / Penalties (2014) In terms of calculating potential penalties, part-time employees (and their hours) are only used to see if an employer is a “large employer”.

Employer Responsibility / Penalties (2014) In terms of calculating potential penalties, part-time employees (and their hours) are only used to see if an employer is a “large employer”.

In terms of calculating potential penalties, part-time employees (and") Employer Responsibility / Penalties (2014) In terms of calculating potential penalties, part-time employees (and their hours) are only used to see if an employer is a “large employer”. - Penalties (if any) are ONLY calculated on FTEs

Employer Responsibility / Penalties (2014) In terms of calculating potential penalties, part-time employees (and their hours) are only used to see if an employer is a “large employer”. - Penalties (if any) are ONLY calculated on FTEs

In terms of calculating potential penalties, part-time employees (and") Employer Responsibility / Penalties (2014) In terms of calculating potential penalties, part-time employees (and their hours) are only used to see if an employer is a “large employer”. - Penalties (if any) are ONLY calculated on FTEs - No penalties on part-time employee, even if that part-time employee received Premium Assistance.

Employer Responsibility / Penalties (2014) In terms of calculating potential penalties, part-time employees (and their hours) are only used to see if an employer is a “large employer”. - Penalties (if any) are ONLY calculated on FTEs - No penalties on part-time employee, even if that part-time employee received Premium Assistance.

In terms of calculating potential penalties, part-time employees (and") Employer Responsibility / Penalties (2014) In terms of calculating potential penalties, part-time employees (and their hours) are only used to see if an employer is a “large employer”. - Penalties (if any) are ONLY calculated on FTEs - No penalties on part-time employee, even if that part-time employee received Premium Assistance. - If no FTE receives Premium Assistance (only part-time) the employer will have no possibility of a penalty.

Employer Responsibility / Penalties (2014) In terms of calculating potential penalties, part-time employees (and their hours) are only used to see if an employer is a “large employer”. - Penalties (if any) are ONLY calculated on FTEs - No penalties on part-time employee, even if that part-time employee received Premium Assistance. - If no FTE receives Premium Assistance (only part-time) the employer will have no possibility of a penalty.

Thank You for Your Attendance") National Health Care Reform – PPACA – (Part 1) Thank You for Your Attendance

National Health Care Reform – PPACA – (Part 1) Thank You for Your Attendance