5baac75d31e077528235e14b5f941822.ppt

- Количество слайдов: 72

Money Supply and Monetary Policy The mechanics of money supply determination Stylized central bank balance sheet Central Bank _______________________________________ Government securities (GS) | CB notes – currency held by the non-bank public Loans to banks (DL) | CB notes – cash held by banks (vault, ATMs) Foreign exchange reserves (FX) | Commercial bank deposits

Money Supply and Monetary Policy The mechanics of money supply determination Stylized central bank balance sheet Central Bank _______________________________________ Government securities (GS) | CB notes – currency held by the non-bank public Loans to banks (DL) | CB notes – cash held by banks (vault, ATMs) Foreign exchange reserves (FX) | Commercial bank deposits

Money Supply and Monetary Policy The mechanics of money supply determination B = monetary base C = currency in circulation and held by the non-bank public R = Bank reserves = vault cash plus CB deposits B=C+R

Money Supply and Monetary Policy The mechanics of money supply determination B = monetary base C = currency in circulation and held by the non-bank public R = Bank reserves = vault cash plus CB deposits B=C+R

Money Supply and Monetary Policy The mechanics of money supply determination B = monetary base C = currency in circulation and held by the non-bank public R = Bank reserves = vault cash plus CB deposits B=C+R Commercial Banking System ____________________________________ Reserves (R) | Checkable deposits (D) Bank loans (L) | Loans from the central bank (DL) Other assets (e. g. t-bills) | Households (non-bank public) ____________________________________ Checkable deposits at banks (D) | Net worth Currency (C) | Bank loans (L) Other assets (e. g. physical capital) | M=C+D

Money Supply and Monetary Policy The mechanics of money supply determination B = monetary base C = currency in circulation and held by the non-bank public R = Bank reserves = vault cash plus CB deposits B=C+R Commercial Banking System ____________________________________ Reserves (R) | Checkable deposits (D) Bank loans (L) | Loans from the central bank (DL) Other assets (e. g. t-bills) | Households (non-bank public) ____________________________________ Checkable deposits at banks (D) | Net worth Currency (C) | Bank loans (L) Other assets (e. g. physical capital) | M=C+D

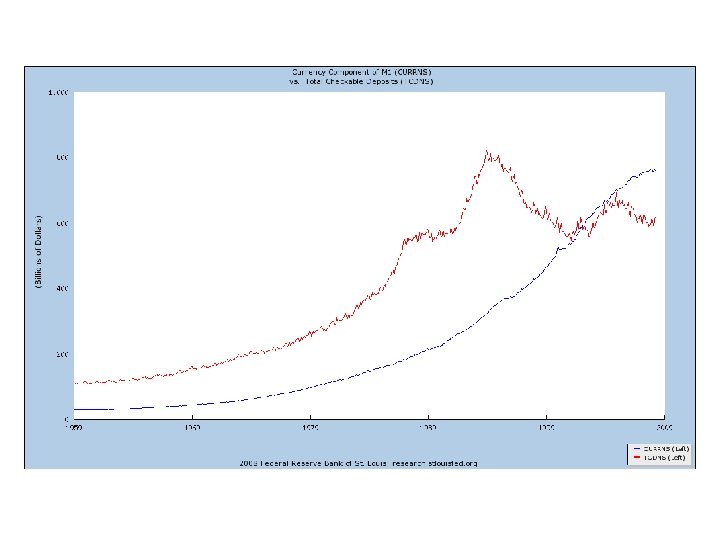

Money Supply and Monetary Policy The mechanics of money supply determination US data, April 2008 ($ billions): Monetary base (B) Bank reserves (R) Currency (C) Checkable deposits (D) M 1 $803 $43 $760 (much of which is held abroad, 60%? ) $617 (at banks and other depository institutions) $1, 377

Money Supply and Monetary Policy The mechanics of money supply determination US data, April 2008 ($ billions): Monetary base (B) Bank reserves (R) Currency (C) Checkable deposits (D) M 1 $803 $43 $760 (much of which is held abroad, 60%? ) $617 (at banks and other depository institutions) $1, 377

Money Supply and Monetary Policy The mechanics of money supply determination Changing the monetary base Bank of England buys £ 1000 government bonds: Central Bank ___________________________ Govt. Sec. +1000 | Reserves + 1000 Barclays Bank ____________________________ Reserves +1000 | Deposits + 1000

Money Supply and Monetary Policy The mechanics of money supply determination Changing the monetary base Bank of England buys £ 1000 government bonds: Central Bank ___________________________ Govt. Sec. +1000 | Reserves + 1000 Barclays Bank ____________________________ Reserves +1000 | Deposits + 1000

Money Supply and Monetary Policy The mechanics of money supply determination Changing the monetary base The money multiplier: m = (M/B) = (C + D)/(C +R) = (k + 1)/(k+q) k = C/D is the household’s desired currency/deposit ratio (household behavior) q = desired reserve/deposit ratio of the banking system (bank behavior) m = the money multiplier

Money Supply and Monetary Policy The mechanics of money supply determination Changing the monetary base The money multiplier: m = (M/B) = (C + D)/(C +R) = (k + 1)/(k+q) k = C/D is the household’s desired currency/deposit ratio (household behavior) q = desired reserve/deposit ratio of the banking system (bank behavior) m = the money multiplier

Money Supply and Monetary Policy The mechanics of money supply determination Changing the monetary base M = m∙B ∆M = m·∆B q = 0. 10 k = 0. 50 m = 1. 5/0. 6 = 2. 5 ∆B = 1000 (this is the increase in the size of the Bank’s liabilities) → ∆M = 2. 5· 1000 = £ 2, 500.

Money Supply and Monetary Policy The mechanics of money supply determination Changing the monetary base M = m∙B ∆M = m·∆B q = 0. 10 k = 0. 50 m = 1. 5/0. 6 = 2. 5 ∆B = 1000 (this is the increase in the size of the Bank’s liabilities) → ∆M = 2. 5· 1000 = £ 2, 500.

Money Supply and Monetary Policy The mechanics of money supply determination Changing the monetary base More examples: Discount loan Change in foreign reserves (foreign exchange intervention) Monetizing government deficits

Money Supply and Monetary Policy The mechanics of money supply determination Changing the monetary base More examples: Discount loan Change in foreign reserves (foreign exchange intervention) Monetizing government deficits

Money Supply and Monetary Policy The mechanics of money supply determination Determinants of the multiplier Desired reserve ratio 1) Opportunity cost: the expected return on loans (net of interest paid on reserves) 2) Probability of withdrawals 3) Required reserves by central bank

Money Supply and Monetary Policy The mechanics of money supply determination Determinants of the multiplier Desired reserve ratio 1) Opportunity cost: the expected return on loans (net of interest paid on reserves) 2) Probability of withdrawals 3) Required reserves by central bank

Money Supply and Monetary Policy The mechanics of money supply determination Determinants of the multiplier Desired reserve ratio q = 0. 10 k = 0. 50 m = 1. 5/0. 6 = 2. 5

Money Supply and Monetary Policy The mechanics of money supply determination Determinants of the multiplier Desired reserve ratio q = 0. 10 k = 0. 50 m = 1. 5/0. 6 = 2. 5

Money Supply and Monetary Policy The mechanics of money supply determination Determinants of the multiplier Desired reserve ratio q = 0. 10 k = 0. 50 m = 1. 5/0. 6 = 2. 5 q = 0. 25 k = 0. 50 m = 1. 5/0. 75 = 2

Money Supply and Monetary Policy The mechanics of money supply determination Determinants of the multiplier Desired reserve ratio q = 0. 10 k = 0. 50 m = 1. 5/0. 6 = 2. 5 q = 0. 25 k = 0. 50 m = 1. 5/0. 75 = 2

Money Supply and Monetary Policy The mechanics of money supply determination Determinants of the multiplier Desired currency ratio 1) Opportunity costs: negatively related to returns on alternative assets 2) Risk: banking panics and runs 3) Transactions costs: convenience of using cash (e. g. it’s anonymous)

Money Supply and Monetary Policy The mechanics of money supply determination Determinants of the multiplier Desired currency ratio 1) Opportunity costs: negatively related to returns on alternative assets 2) Risk: banking panics and runs 3) Transactions costs: convenience of using cash (e. g. it’s anonymous)

Money Supply and Monetary Policy The mechanics of money supply determination Determinants of the multiplier Desired currency ratio q = 0. 10 k = 0. 50 m = 1. 5/0. 6 = 2. 5 q = 0. 10 k = 0. 60 m = 1. 5/0. 7 = 2. 29

Money Supply and Monetary Policy The mechanics of money supply determination Determinants of the multiplier Desired currency ratio q = 0. 10 k = 0. 50 m = 1. 5/0. 6 = 2. 5 q = 0. 10 k = 0. 60 m = 1. 5/0. 7 = 2. 29

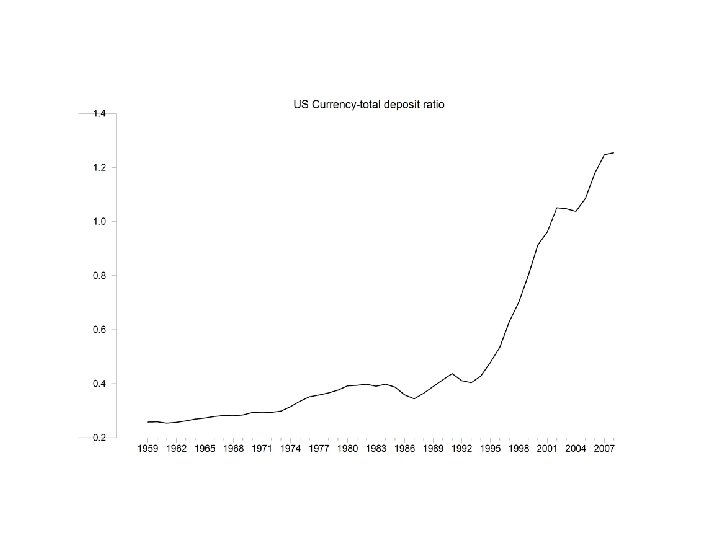

Money Supply and Monetary Policy The mechanics of money supply determination The currency ratio and the multiplier during the Great Depression – Massive increases in desired reserve and currency ratios because of uncertainty in the banking system – Check tax

Money Supply and Monetary Policy The mechanics of money supply determination The currency ratio and the multiplier during the Great Depression – Massive increases in desired reserve and currency ratios because of uncertainty in the banking system – Check tax

Money Supply and Monetary Policy The mechanics of money supply determination The currency ratio and the multiplier during the Great Depression – Massive increases in desired reserve and currency ratios because of uncertainty in the banking system – Check tax Current trends Increase in mid-90’s due to financial innovations and strong foreign demand for US currency.

Money Supply and Monetary Policy The mechanics of money supply determination The currency ratio and the multiplier during the Great Depression – Massive increases in desired reserve and currency ratios because of uncertainty in the banking system – Check tax Current trends Increase in mid-90’s due to financial innovations and strong foreign demand for US currency.

Money Supply and Monetary Policy Organization of modern central banks The Federal Reserve System 1) Board of Governors 2) District banks 3) FOMC (Federal Open Market Committee). 4) Member banks Map: http: //federalreserve. gov/otherfrb. htm Ben Bernanke

Money Supply and Monetary Policy Organization of modern central banks The Federal Reserve System 1) Board of Governors 2) District banks 3) FOMC (Federal Open Market Committee). 4) Member banks Map: http: //federalreserve. gov/otherfrb. htm Ben Bernanke

Money Supply and Monetary Policy Organization of modern central banks The Bank of England 1) Court of Directors 2) Monetary Policy Committee (MPC) 3) Debt Management Office (DMO) 4) Financial Services Authority (FSA) Mervyn King

Money Supply and Monetary Policy Organization of modern central banks The Bank of England 1) Court of Directors 2) Monetary Policy Committee (MPC) 3) Debt Management Office (DMO) 4) Financial Services Authority (FSA) Mervyn King

Money Supply and Monetary Policy Organization of modern central banks The European Central Bank Created in 1992 (Maastricht 1992) with the decision for monetary unification. ECB and ESCB began in 1999 with the Euro began circulating in 2002. 15 countries currently in the Euro system (UK – not). ECB located in Frankfurt, Germany. Governing council: 6 member of Exec. Board and national CB pres. Jean-Claude Trichet

Money Supply and Monetary Policy Organization of modern central banks The European Central Bank Created in 1992 (Maastricht 1992) with the decision for monetary unification. ECB and ESCB began in 1999 with the Euro began circulating in 2002. 15 countries currently in the Euro system (UK – not). ECB located in Frankfurt, Germany. Governing council: 6 member of Exec. Board and national CB pres. Jean-Claude Trichet

Money Supply and Monetary Policy Organization of modern central banks Aside: the creation of the Euro, ECB and ESCB ECU (European Currency Unit) was a ‘basket’ of European currencies used during the ERM. 1 Jan. 1999: exchange rates of 11 original members irrevocably fixed, which determined a fixed exchange rate between each nation’s currency and the ‘basket’ now called the Euro. Until 1 Jan. 2003, national currencies continued to circulate, but central bank transactions were in terms of Euros at these fixed rates. Rates: http: //en. wikipedia. org/wiki/Euro

Money Supply and Monetary Policy Organization of modern central banks Aside: the creation of the Euro, ECB and ESCB ECU (European Currency Unit) was a ‘basket’ of European currencies used during the ERM. 1 Jan. 1999: exchange rates of 11 original members irrevocably fixed, which determined a fixed exchange rate between each nation’s currency and the ‘basket’ now called the Euro. Until 1 Jan. 2003, national currencies continued to circulate, but central bank transactions were in terms of Euros at these fixed rates. Rates: http: //en. wikipedia. org/wiki/Euro

Money Supply and Monetary Policy Organization of modern central banks Aside: the creation of the Euro, ECB and ESCB A 2 -country example: Germany and France Basket: 4 francs and 2 marks (the ECU) Dec. 31: fix franc/mark rate at 1. 5; then Francs per ECU/Euro = 4 (francs) + 2∙ 1. 5 (francs) = 7 francs Marks per ECU/Euro = 4/1. 5 + 2 = 4. 67 marks

Money Supply and Monetary Policy Organization of modern central banks Aside: the creation of the Euro, ECB and ESCB A 2 -country example: Germany and France Basket: 4 francs and 2 marks (the ECU) Dec. 31: fix franc/mark rate at 1. 5; then Francs per ECU/Euro = 4 (francs) + 2∙ 1. 5 (francs) = 7 francs Marks per ECU/Euro = 4/1. 5 + 2 = 4. 67 marks

Money Supply and Monetary Policy Organization of modern central banks Aside: the creation of the Euro, ECB and ESCB Prior to monetary union: Bank of France ____________________________________ French gov’t securities ₣ 1 billion | ₣ 1 billion Reserves at banks Bundesbank ____________________________________ German gov’t securities DM 2 billion | DM 2 billion Reserves at banks

Money Supply and Monetary Policy Organization of modern central banks Aside: the creation of the Euro, ECB and ESCB Prior to monetary union: Bank of France ____________________________________ French gov’t securities ₣ 1 billion | ₣ 1 billion Reserves at banks Bundesbank ____________________________________ German gov’t securities DM 2 billion | DM 2 billion Reserves at banks

Money Supply and Monetary Policy Organization of modern central banks Aside: the creation of the Euro, ECB and ESCB After unification to a single currency European Central Bank ____________________________________ French gov’t securities € 7 billion | € 16. 3 billion European MB German gov’t securities € 9. 3 billion |

Money Supply and Monetary Policy Organization of modern central banks Aside: the creation of the Euro, ECB and ESCB After unification to a single currency European Central Bank ____________________________________ French gov’t securities € 7 billion | € 16. 3 billion European MB German gov’t securities € 9. 3 billion |

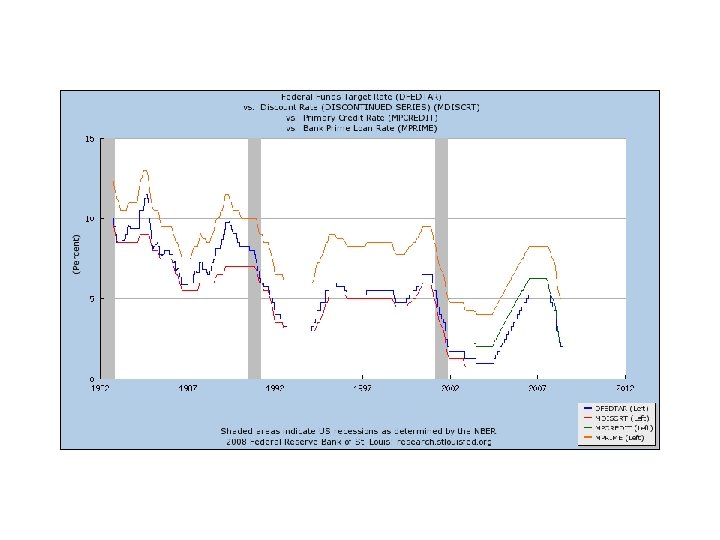

• Open") Money Supply and Monetary Policy Tools of monetary policy (focus on Fed) • Open market operations – FOMC directive – Defensive versus dynamic

Money Supply and Monetary Policy Tools of monetary policy (focus on Fed) • Open market operations – FOMC directive – Defensive versus dynamic

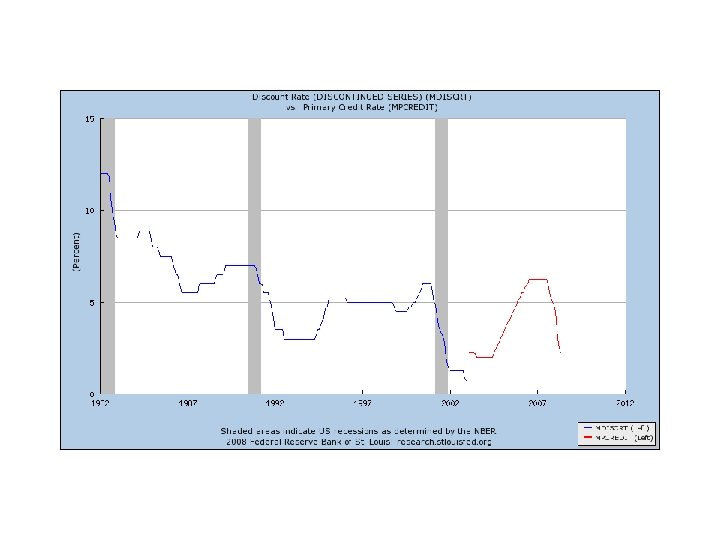

Money Supply and Monetary Policy Tools of monetary policy • Discount policy – Oldest and original tool of the Fed – Primary tool: setting the discount rate – Types of discount lending (since 2003) • Primary credit (rate set slightly above fed funds rate) • Secondary credit (50 basis points above fed funds)

Money Supply and Monetary Policy Tools of monetary policy • Discount policy – Oldest and original tool of the Fed – Primary tool: setting the discount rate – Types of discount lending (since 2003) • Primary credit (rate set slightly above fed funds rate) • Secondary credit (50 basis points above fed funds)

Money Supply and Monetary Policy Tools of monetary policy • Discount policy – New types of discount lending • • Term auction facility for banks since Dec. 2007 Discount lending facilities for primary bond dealers – Unlike typical discount loans, TAF sets amount, not rate. Banks bid for funds, offering a rate; the Fed makes loans to those banks offering the highest rates, until the loans are exhausted. Benefit: available to any bank willing to pay. • In Dec. 2007, $11. 6 billion in TAF loans; as of $127 billion

Money Supply and Monetary Policy Tools of monetary policy • Discount policy – New types of discount lending • • Term auction facility for banks since Dec. 2007 Discount lending facilities for primary bond dealers – Unlike typical discount loans, TAF sets amount, not rate. Banks bid for funds, offering a rate; the Fed makes loans to those banks offering the highest rates, until the loans are exhausted. Benefit: available to any bank willing to pay. • In Dec. 2007, $11. 6 billion in TAF loans; as of $127 billion

Money Supply and Monetary Policy Tools of monetary policy • Reserve requirements 0% on checkable deposits up to 9. 3 million, 3% on deposits between 9. 3 million and $43. 9 million, and 10% beyond.

Money Supply and Monetary Policy Tools of monetary policy • Reserve requirements 0% on checkable deposits up to 9. 3 million, 3% on deposits between 9. 3 million and $43. 9 million, and 10% beyond.

Money Supply and Monetary Policy Tools of monetary policy • For any given bank, the fed determines that bank’s daily average checking account balances and daily average vault cash during a two week period beginning on a Tuesday and ending on a Monday. Based on this average value of checking account balances, the Fed applies the percentages above to get a dollar value for required reserves. The bank is required to have sufficient reserves (vault cash and fed deposits) on this amount on average during a two week maintenance period that begins 17 days after the computation period ends. If the bank has sufficient vault cash, the reserve requirement is satisfied for the current maintenance period. If not, the bank must hold deposits at the Fed such that the daily average of these deposits over the two week maintenance period meets the requirements when added to the previously measure vault cash.

Money Supply and Monetary Policy Tools of monetary policy • For any given bank, the fed determines that bank’s daily average checking account balances and daily average vault cash during a two week period beginning on a Tuesday and ending on a Monday. Based on this average value of checking account balances, the Fed applies the percentages above to get a dollar value for required reserves. The bank is required to have sufficient reserves (vault cash and fed deposits) on this amount on average during a two week maintenance period that begins 17 days after the computation period ends. If the bank has sufficient vault cash, the reserve requirement is satisfied for the current maintenance period. If not, the bank must hold deposits at the Fed such that the daily average of these deposits over the two week maintenance period meets the requirements when added to the previously measure vault cash.

Money Supply and Monetary Policy Tools of monetary policy • An example: Suppose the computation period runs from Tuesday, May 27 to Monday, June 9. During this period, the average daily balance of your bank’s checking account liabilities was $75 million, and average daily vault cash was $1 million. Your required reserves would be (0. 03)(43. 9 – 9. 3) + (0. 10) (75 – 43. 9) = $4. 12 million. Thus, there is a required reserve balance of $3. 12 million. To satisfy the reserve requirement, your bank will have to hold average daily balances as deposits at the Fed equal to $3. 12 million during the two week maintenance period beginning on Thursday, June 26.

Money Supply and Monetary Policy Tools of monetary policy • An example: Suppose the computation period runs from Tuesday, May 27 to Monday, June 9. During this period, the average daily balance of your bank’s checking account liabilities was $75 million, and average daily vault cash was $1 million. Your required reserves would be (0. 03)(43. 9 – 9. 3) + (0. 10) (75 – 43. 9) = $4. 12 million. Thus, there is a required reserve balance of $3. 12 million. To satisfy the reserve requirement, your bank will have to hold average daily balances as deposits at the Fed equal to $3. 12 million during the two week maintenance period beginning on Thursday, June 26.

Money Supply and Monetary Policy Tools of monetary policy Reserve requirements as a ‘tax’ on lending: Assume a bank holds no reserves, and thus lends all deposits. If r is the interest rate charged on loans (L) and i the rate charged on deposits (D), then the banks profits are Profit = r∙L - i∙D = (r – i)D With a reserve requirement on deposits of q: Profit = r(D – R) - i∙D = r(D – q. D) - i∙D = [r(1 -q) – i ]D

Money Supply and Monetary Policy Tools of monetary policy Reserve requirements as a ‘tax’ on lending: Assume a bank holds no reserves, and thus lends all deposits. If r is the interest rate charged on loans (L) and i the rate charged on deposits (D), then the banks profits are Profit = r∙L - i∙D = (r – i)D With a reserve requirement on deposits of q: Profit = r(D – R) - i∙D = r(D – q. D) - i∙D = [r(1 -q) – i ]D

Goals and strategy of monetary policy Goals of monetary policy Fed: to conduct “the nation’s monetary policy by influencing the monetary and credit conditions in the economy in pursuit of maximum employment, stable prices, and moderate long-term interest rates. ” Bank of England: “The Bank’s monetary policy objective is to deliver price stability – low inflation – and, subject to that, to support the Government’s economic objectives including those for growth and employment. Price stability is defined by the Government’s inflation target of 2%. ”

Goals and strategy of monetary policy Goals of monetary policy Fed: to conduct “the nation’s monetary policy by influencing the monetary and credit conditions in the economy in pursuit of maximum employment, stable prices, and moderate long-term interest rates. ” Bank of England: “The Bank’s monetary policy objective is to deliver price stability – low inflation – and, subject to that, to support the Government’s economic objectives including those for growth and employment. Price stability is defined by the Government’s inflation target of 2%. ”

Goals and strategy of monetary policy Goals of monetary policy ECB: “To maintain price stability is the primary objective of the Eurosystem and of the single monetary policy for which it is responsible This is laid down in the Treaty establishing the European Community…The Treaty establishes a clear hierarchy of objectives for the Eurosystem. It assigns overriding importance to price stability. The Treaty makes clear that ensuring price stability is the most important contribution that monetary policy can make to achieve a favourable economic environment and a high level of employment. ”

Goals and strategy of monetary policy Goals of monetary policy ECB: “To maintain price stability is the primary objective of the Eurosystem and of the single monetary policy for which it is responsible This is laid down in the Treaty establishing the European Community…The Treaty establishes a clear hierarchy of objectives for the Eurosystem. It assigns overriding importance to price stability. The Treaty makes clear that ensuring price stability is the most important contribution that monetary policy can make to achieve a favourable economic environment and a high level of employment. ”

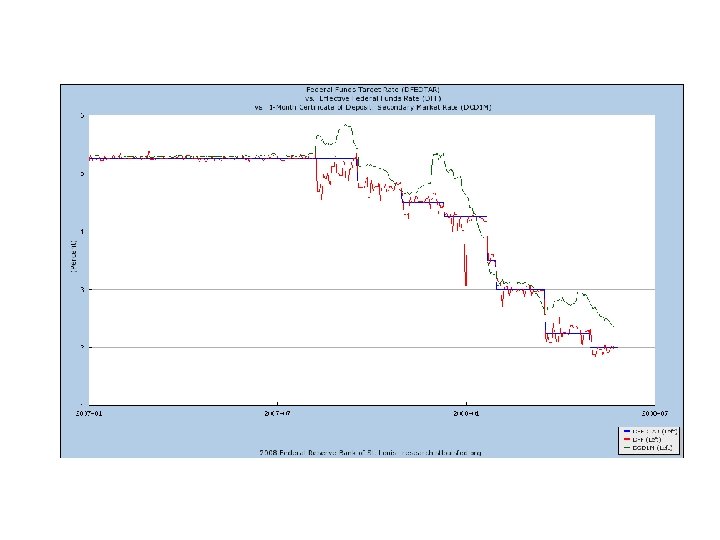

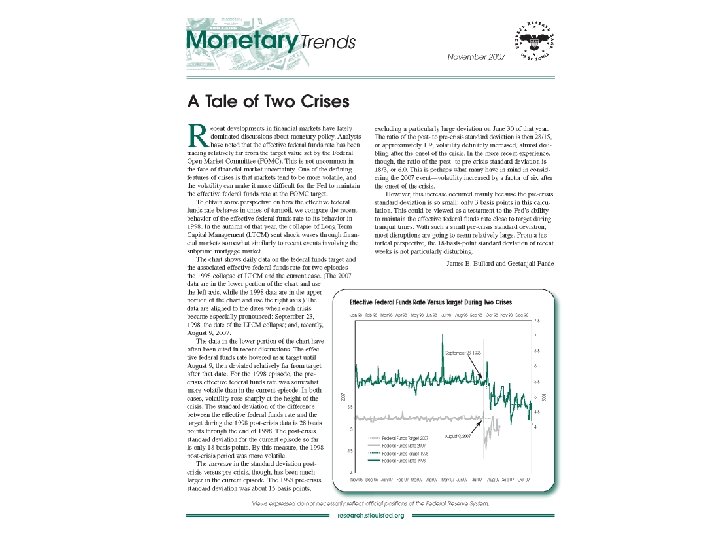

Goals and strategy of monetary policy Operating targets: day-to-day operations The Federal funds market: inter-bank market for borrowing and lending reserves (cash) on an overnight basis. The interest rate determined in this market is the federal funds rate. The FED cannot directly set this rate.

Goals and strategy of monetary policy Operating targets: day-to-day operations The Federal funds market: inter-bank market for borrowing and lending reserves (cash) on an overnight basis. The interest rate determined in this market is the federal funds rate. The FED cannot directly set this rate.

Goals and strategy of monetary policy Operating targets: day-to-day operations The Federal funds market: inter-bank market for borrowing and lending reserves (cash) on an overnight basis. The interest rate determined in this market is the federal funds rate. The FED cannot directly set this rate. A model of the federal funds market The model reflects the ‘market’ for bank reserves. Supply of reserves: determined primarily by the Fed Demand for reserves: determined by banks Equilibrium: federal funds rate adjusts until supply and demand for bank reserves are equal.

Goals and strategy of monetary policy Operating targets: day-to-day operations The Federal funds market: inter-bank market for borrowing and lending reserves (cash) on an overnight basis. The interest rate determined in this market is the federal funds rate. The FED cannot directly set this rate. A model of the federal funds market The model reflects the ‘market’ for bank reserves. Supply of reserves: determined primarily by the Fed Demand for reserves: determined by banks Equilibrium: federal funds rate adjusts until supply and demand for bank reserves are equal.

Goals and strategy of monetary policy Operating targets: day-to-day operations Supply of reserves = non-borrowed reserves + borrowed reserves Non-borrowed reserves: determined by the Fed, for any given fed funds rate. Borrowed reserves: discount loans to banks; if the fed funds rate is less than the discount rate, banks will not want to borrow from the Fed; if the fed funds rate is equal to or exceeds the discount rate, they will want to borrow as much as possible from the discount window.

Goals and strategy of monetary policy Operating targets: day-to-day operations Supply of reserves = non-borrowed reserves + borrowed reserves Non-borrowed reserves: determined by the Fed, for any given fed funds rate. Borrowed reserves: discount loans to banks; if the fed funds rate is less than the discount rate, banks will not want to borrow from the Fed; if the fed funds rate is equal to or exceeds the discount rate, they will want to borrow as much as possible from the discount window.

Goals and strategy of monetary policy Operating targets: day-to-day operations Demand for reserves: required reserves + excess reserves Required reserves depend on Fed’s reserve requirement and checking account deposits. Excess reserves depend a) withdrawal demands; b) opportunity cost; i. e. the federal funds rate. Lending in the federal funds market is an alternative to holding reserves: if the federal funds rate is high, opportunity cost of holding reserves is high (and vice versa). Thus, we assume a negative relation between the demand for reserves and the federal funds rate.

Goals and strategy of monetary policy Operating targets: day-to-day operations Demand for reserves: required reserves + excess reserves Required reserves depend on Fed’s reserve requirement and checking account deposits. Excess reserves depend a) withdrawal demands; b) opportunity cost; i. e. the federal funds rate. Lending in the federal funds market is an alternative to holding reserves: if the federal funds rate is high, opportunity cost of holding reserves is high (and vice versa). Thus, we assume a negative relation between the demand for reserves and the federal funds rate.

Goals and strategy of monetary policy Operating targets: day-to-day operations Equilibrium: If fed funds rate too low – excess demand for reserves, and rate will rise. If fed funds rate is too high – excess supply of reserves, and rate will fall. Only at that rate where the supply of reserves is equal to the overall demand for those reserves will the fed funds rate not change.

Goals and strategy of monetary policy Operating targets: day-to-day operations Equilibrium: If fed funds rate too low – excess demand for reserves, and rate will rise. If fed funds rate is too high – excess supply of reserves, and rate will fall. Only at that rate where the supply of reserves is equal to the overall demand for those reserves will the fed funds rate not change.

Goals and strategy of monetary policy Operating targets: day-to-day operations Graphical approach and some though experiments: Open market purchase by the FOMC – rate falls Increase in reserve demand – rate rises Increase in discount rate

Goals and strategy of monetary policy Operating targets: day-to-day operations Graphical approach and some though experiments: Open market purchase by the FOMC – rate falls Increase in reserve demand – rate rises Increase in discount rate

Goals and strategy of monetary policy Operating targets: day-to-day operations The Fed’s operating targets: the federal funds rate or non-borrowed reserves Fed funds rate: FOMC accommodates reserve demand shocks Non-borrowed reserves: FOMC does not accommodate such shocks. Since early 1980’s, the Fed has used the federal funds rate as its primary operating target. Active changes in policy are mostly reflected in changes in the Fed’s federal funds rate target.

Goals and strategy of monetary policy Operating targets: day-to-day operations The Fed’s operating targets: the federal funds rate or non-borrowed reserves Fed funds rate: FOMC accommodates reserve demand shocks Non-borrowed reserves: FOMC does not accommodate such shocks. Since early 1980’s, the Fed has used the federal funds rate as its primary operating target. Active changes in policy are mostly reflected in changes in the Fed’s federal funds rate target.

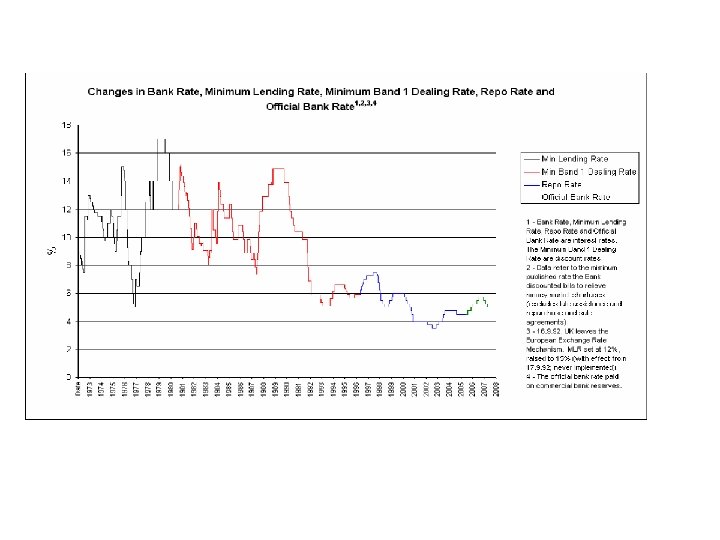

Goals and strategy of monetary policy Operating targets: day-to-day operations Operating targets at the Bank of England Since May 2006, the Band of England’s operating target has been ‘the official bank rate’ which is the interest rate paid on bank reserves. Prior to this, the official rate was the ‘repo’ rate, or rate on loans to banks. These rates are directly set by the MPC. Compare Fed and Bo. E: expansionary monetary policy . Fed: lower fed funds target by buying t-bills in the open market; as bank reserves increase, banks have an incentive to increase loans and money supply increases (through the multiplier effect). MPC: lower official bank rate, reducing opportunity cost of holding bank reserves, increasing lending

Goals and strategy of monetary policy Operating targets: day-to-day operations Operating targets at the Bank of England Since May 2006, the Band of England’s operating target has been ‘the official bank rate’ which is the interest rate paid on bank reserves. Prior to this, the official rate was the ‘repo’ rate, or rate on loans to banks. These rates are directly set by the MPC. Compare Fed and Bo. E: expansionary monetary policy . Fed: lower fed funds target by buying t-bills in the open market; as bank reserves increase, banks have an incentive to increase loans and money supply increases (through the multiplier effect). MPC: lower official bank rate, reducing opportunity cost of holding bank reserves, increasing lending

Goals and strategy of monetary policy Operating targets: day-to-day operations ECB operating target: The ECB provides standing facilities for bank lending and borrowing – it stands ready to lend reserves to banks at a set rate (say 4. 25%) and borrow from banks at a (lower) rate (say 4%). [The former is like the Fed’s discount rate, the latter is like the Bo. E’s payment of interest on reserves. ] The operating target rate is essentially the overnight lending rate for banks, the same as the fed funds rate. But the interest rate channel provides a direct boundary for this rate; e. g. no bank will lend to another bank at less than 4% and will borrow from another bank at more than 4. 25%. Example: suppose a bank in France holds € 1000, 300 of which is borrowed from the ECB from its standing facility. The bank will earn 4% on € 700, and will pay 4. 25% on € 300.

Goals and strategy of monetary policy Operating targets: day-to-day operations ECB operating target: The ECB provides standing facilities for bank lending and borrowing – it stands ready to lend reserves to banks at a set rate (say 4. 25%) and borrow from banks at a (lower) rate (say 4%). [The former is like the Fed’s discount rate, the latter is like the Bo. E’s payment of interest on reserves. ] The operating target rate is essentially the overnight lending rate for banks, the same as the fed funds rate. But the interest rate channel provides a direct boundary for this rate; e. g. no bank will lend to another bank at less than 4% and will borrow from another bank at more than 4. 25%. Example: suppose a bank in France holds € 1000, 300 of which is borrowed from the ECB from its standing facility. The bank will earn 4% on € 700, and will pay 4. 25% on € 300.

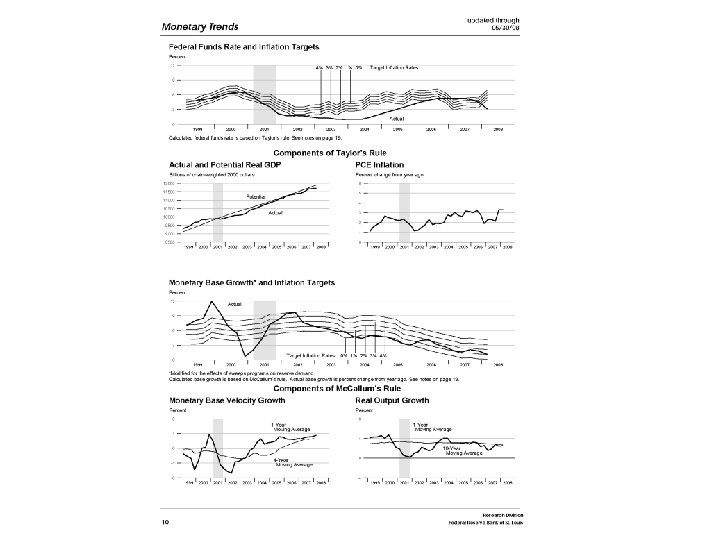

Goals and strategy of monetary policy Other aspects of policy implementation • Intermediate targets • Inflation targeting • Taylor’s rule – i = r* + π +. 5(y – y*) +. 5(π-π*) – i is fed funds target rate, r* is real interest rate at full employment, y is real output, y* is full employment output, π is the inflation rate and π* is the target inflation rate.

Goals and strategy of monetary policy Other aspects of policy implementation • Intermediate targets • Inflation targeting • Taylor’s rule – i = r* + π +. 5(y – y*) +. 5(π-π*) – i is fed funds target rate, r* is real interest rate at full employment, y is real output, y* is full employment output, π is the inflation rate and π* is the target inflation rate.

Goals and strategy of monetary policy Other aspects of policy implementation • Intermediate targets • Inflation targeting • Taylor’s rule – Example: As an example, suppose r*=2. 5 and y=y*. Assume that the target inflation rate is 2%. a) if π = 2%, then the target rate will be 4. 5% = 2. 5% + 2%. b) if π = 3%, then i = 2. 5% + 3% + 0. 5(1%) = 6%. Notice that the rule specifies that the target rate moves more than one for one with the rate of inflation.

Goals and strategy of monetary policy Other aspects of policy implementation • Intermediate targets • Inflation targeting • Taylor’s rule – Example: As an example, suppose r*=2. 5 and y=y*. Assume that the target inflation rate is 2%. a) if π = 2%, then the target rate will be 4. 5% = 2. 5% + 2%. b) if π = 3%, then i = 2. 5% + 3% + 0. 5(1%) = 6%. Notice that the rule specifies that the target rate moves more than one for one with the rate of inflation.

Goals and strategy of monetary policy Exchange rates and monetary policy Foreign exchange interventions Federal Reserve System ____________________________________ Domestic assets (T-bills and disc. loans) | Monetary base (bank reserves) Foreign reserves (foreign bonds) | ius = iuk + (∆S/S)

Goals and strategy of monetary policy Exchange rates and monetary policy Foreign exchange interventions Federal Reserve System ____________________________________ Domestic assets (T-bills and disc. loans) | Monetary base (bank reserves) Foreign reserves (foreign bonds) | ius = iuk + (∆S/S)

Goals and strategy of monetary policy Exchange rates and monetary policy Foreign exchange interventions Fed buys $1 million worth of pound assets US monetary base rises as non-borrowed reserves rise Federal funds rate will fall US assets become less desirable; by interest parity model, the pound will appreciate.

Goals and strategy of monetary policy Exchange rates and monetary policy Foreign exchange interventions Fed buys $1 million worth of pound assets US monetary base rises as non-borrowed reserves rise Federal funds rate will fall US assets become less desirable; by interest parity model, the pound will appreciate.

Goals and strategy of monetary policy Exchange rates and monetary policy Balance of payments and international flow of funds Sources of foreign exchange: selling goods and services abroad (exports) selling assets abroad (borrowing from foreigners) Uses of foreign exchange: buying goods and services abroad (imports) buying assets abroad (lending to foreigners)

Goals and strategy of monetary policy Exchange rates and monetary policy Balance of payments and international flow of funds Sources of foreign exchange: selling goods and services abroad (exports) selling assets abroad (borrowing from foreigners) Uses of foreign exchange: buying goods and services abroad (imports) buying assets abroad (lending to foreigners)

Goals and strategy of monetary policy Exchange rates and monetary policy Balance of payments and international flow of funds Sources of foreign exchange (excluding central banks): selling goods and services abroad (exports) selling assets abroad (borrowing from foreigners) Uses of foreign exchange (excluding central banks): buying goods and services abroad (imports) buying assets abroad (lending to foreigners) Trade (current account) balance: exports minus imports Capital account balance: capital inflows (borrowing) minus capital outflows (lending)

Goals and strategy of monetary policy Exchange rates and monetary policy Balance of payments and international flow of funds Sources of foreign exchange (excluding central banks): selling goods and services abroad (exports) selling assets abroad (borrowing from foreigners) Uses of foreign exchange (excluding central banks): buying goods and services abroad (imports) buying assets abroad (lending to foreigners) Trade (current account) balance: exports minus imports Capital account balance: capital inflows (borrowing) minus capital outflows (lending)

Goals and strategy of monetary policy Exchange rates and monetary policy Balance of payments and international flow of funds (Assume US is domestic country and UK is foreign country) Trade (current account) balance: exports minus imports Capital account balance: capital inflows (borrowing) minus capital outflows (lending) The balance of payments = trade balance plus capital account balance = sources minus uses of foreign exchange = increase in domestic central bank foreign reserves + decrease in foreign central bank dollar reserves

Goals and strategy of monetary policy Exchange rates and monetary policy Balance of payments and international flow of funds (Assume US is domestic country and UK is foreign country) Trade (current account) balance: exports minus imports Capital account balance: capital inflows (borrowing) minus capital outflows (lending) The balance of payments = trade balance plus capital account balance = sources minus uses of foreign exchange = increase in domestic central bank foreign reserves + decrease in foreign central bank dollar reserves

Goals and strategy of monetary policy Exchange rates and monetary policy Balance of payments and international flow of funds • Assume there are no capital flows or imports, only US exports of $1 million. There is a balance of payments surplus of $1 million. This means that US firms sell produced goods to UK households and receive pounds in exchange. By assumption, they don’t use these pounds to buy UK goods (no imports) or assets (no capital outflows); the latter also means they don’t simply trade pounds for dollars with private citizens. Since these are US firms, they ultimately want dollars, so either they sell these pounds to the Fed (an increase in foreign reserves held at the Fed), or they sell the pounds to the Bank of England for dollars (a decrease in dollar reserves held at the Bank of England). The former increases the US monetary base; the latter decreases the UK monetary base.

Goals and strategy of monetary policy Exchange rates and monetary policy Balance of payments and international flow of funds • Assume there are no capital flows or imports, only US exports of $1 million. There is a balance of payments surplus of $1 million. This means that US firms sell produced goods to UK households and receive pounds in exchange. By assumption, they don’t use these pounds to buy UK goods (no imports) or assets (no capital outflows); the latter also means they don’t simply trade pounds for dollars with private citizens. Since these are US firms, they ultimately want dollars, so either they sell these pounds to the Fed (an increase in foreign reserves held at the Fed), or they sell the pounds to the Bank of England for dollars (a decrease in dollar reserves held at the Bank of England). The former increases the US monetary base; the latter decreases the UK monetary base.

Goals and strategy of monetary policy Exchange rates and monetary policy Balance of payments and international flow of funds • Suppose again no imports or capital inflows and exports = $1 million. But now suppose that firms are willing to keep a quarter of this amount as pound deposits at UK banks. Thus, there will be capital outflows (in effect, US firms are lending to the UK) of $250 K, so that the balance of payments will be in surplus of $750 K (the trade balance is $1 million surplus while the capital account is in deficit of $250 K). This will increase Fed foreign reserves and decrease UK dollar reserves by a total of $750 K.

Goals and strategy of monetary policy Exchange rates and monetary policy Balance of payments and international flow of funds • Suppose again no imports or capital inflows and exports = $1 million. But now suppose that firms are willing to keep a quarter of this amount as pound deposits at UK banks. Thus, there will be capital outflows (in effect, US firms are lending to the UK) of $250 K, so that the balance of payments will be in surplus of $750 K (the trade balance is $1 million surplus while the capital account is in deficit of $250 K). This will increase Fed foreign reserves and decrease UK dollar reserves by a total of $750 K.

Goals and strategy of monetary policy Exchange rates and monetary policy Balance of payments and international flow of funds • Assume that US households lend $1 million to UK government by buying Treasury securities, no exports, imports or capital inflows. The US capital account balance is a deficit of $1 million; thus the balance of payments a deficit of $1 million. To finance this lending, the US household might reduce its dollar checking accounts to buy pounds from the Fed (which they then lend). Thus, Fed foreign reserves fall (as does the US monetary base). Alternatively, the household could pay the Bank of England dollars directly, so its dollar reserves and monetary base rise.

Goals and strategy of monetary policy Exchange rates and monetary policy Balance of payments and international flow of funds • Assume that US households lend $1 million to UK government by buying Treasury securities, no exports, imports or capital inflows. The US capital account balance is a deficit of $1 million; thus the balance of payments a deficit of $1 million. To finance this lending, the US household might reduce its dollar checking accounts to buy pounds from the Fed (which they then lend). Thus, Fed foreign reserves fall (as does the US monetary base). Alternatively, the household could pay the Bank of England dollars directly, so its dollar reserves and monetary base rise.

Goals and strategy of monetary policy Exchange rates and monetary policy International linkages and exchange rate regimes. Example: Bank of England raises UK interest rate, putting pressure on the pound to appreciate. Fixed exchange rate regime: Central banks act to maintain fixed nominal exchange rates through foreign exchange interventions. E. g. US sells pound reserves to buy dollars, thus reducing US monetary base, increasing US interest rates, and relieving the pressure on the pound to change. ius = iuk + (∆S/S)

Goals and strategy of monetary policy Exchange rates and monetary policy International linkages and exchange rate regimes. Example: Bank of England raises UK interest rate, putting pressure on the pound to appreciate. Fixed exchange rate regime: Central banks act to maintain fixed nominal exchange rates through foreign exchange interventions. E. g. US sells pound reserves to buy dollars, thus reducing US monetary base, increasing US interest rates, and relieving the pressure on the pound to change. ius = iuk + (∆S/S)

Goals and strategy of monetary policy Exchange rates and monetary policy International linkages and exchange rate regimes. Example: under fixed rates, US wants to lower target fed funds rate. Fed will act to increase monetary base and lower interest rates. If the UK does not lower its rates, the resulting US BOP deficit (because of lower US rates, capital will flow abroad) will cause foreign reserves to fall, reducing US monetary base, and offsetting the initial domestic open market operations. Thus, under fixed exchange rates, countries may have to give up independent monetary policy. In general, can’t have fixed exchange rates, capital mobility and indepenent monetary policy.

Goals and strategy of monetary policy Exchange rates and monetary policy International linkages and exchange rate regimes. Example: under fixed rates, US wants to lower target fed funds rate. Fed will act to increase monetary base and lower interest rates. If the UK does not lower its rates, the resulting US BOP deficit (because of lower US rates, capital will flow abroad) will cause foreign reserves to fall, reducing US monetary base, and offsetting the initial domestic open market operations. Thus, under fixed exchange rates, countries may have to give up independent monetary policy. In general, can’t have fixed exchange rates, capital mobility and indepenent monetary policy.

Goals and strategy of monetary policy Exchange rates and monetary policy International linkages and exchange rate regimes. Now that this bubble has burst, the cross-border monetary stimulus has changed direction. As the Fed has cut interest rates, emerging economies that link their currencies to the dollar have been forced to run a looser monetary policy, even though their economies are overheating. Emerging economies with currencies most closely aligned to the dollar, notably in Asia and the Gulf, have seen the biggest price rises. Countries, such as Mexico, that have more flexible exchange rates and are more committed to inflation targets have done better. -- The Economist, May 24, 2008

Goals and strategy of monetary policy Exchange rates and monetary policy International linkages and exchange rate regimes. Now that this bubble has burst, the cross-border monetary stimulus has changed direction. As the Fed has cut interest rates, emerging economies that link their currencies to the dollar have been forced to run a looser monetary policy, even though their economies are overheating. Emerging economies with currencies most closely aligned to the dollar, notably in Asia and the Gulf, have seen the biggest price rises. Countries, such as Mexico, that have more flexible exchange rates and are more committed to inflation targets have done better. -- The Economist, May 24, 2008

Goals and strategy of monetary policy Exchange rates and monetary policy International linkages and exchange rate regimes. • • Bretton Woods 1945 -1971 Currency devaluation; e. g. Britain and the ERM Floating exchange rates – no intervention Extreme fixed rate regimes – Monetary unification – Dollarization – Currency boards

Goals and strategy of monetary policy Exchange rates and monetary policy International linkages and exchange rate regimes. • • Bretton Woods 1945 -1971 Currency devaluation; e. g. Britain and the ERM Floating exchange rates – no intervention Extreme fixed rate regimes – Monetary unification – Dollarization – Currency boards

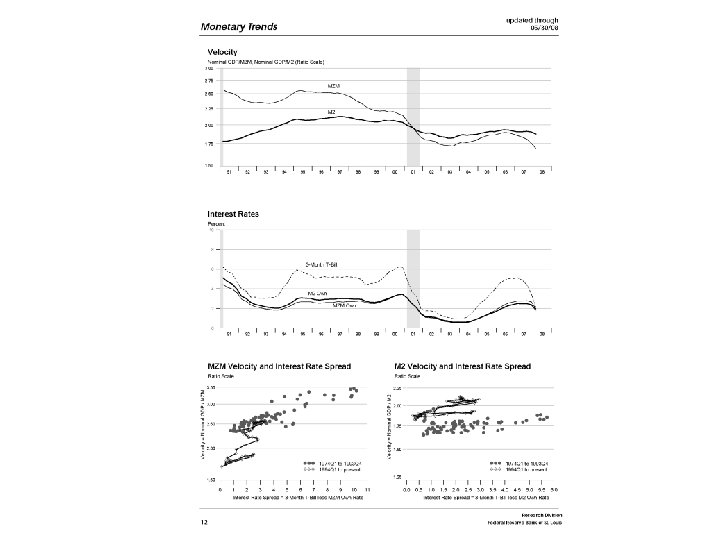

Linking money to the economy The effects of money in the long-run Equation of exchange and velocity MV = Py/M M is the stock of money, P is the price level, y is real output , and V is the velocity of money.

Linking money to the economy The effects of money in the long-run Equation of exchange and velocity MV = Py/M M is the stock of money, P is the price level, y is real output , and V is the velocity of money.

Linking money to the economy The effects of money in the long-run Equation of exchange and velocity MV = Py/M M is the stock of money, P is the price level, y is real output , and V is the velocity of money. M/P = (1/V)·y = k ·y

Linking money to the economy The effects of money in the long-run Equation of exchange and velocity MV = Py/M M is the stock of money, P is the price level, y is real output , and V is the velocity of money. M/P = (1/V)·y = k ·y

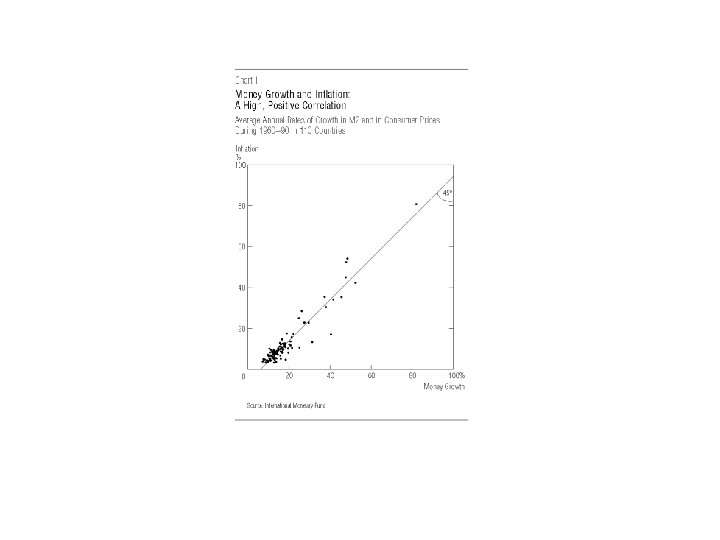

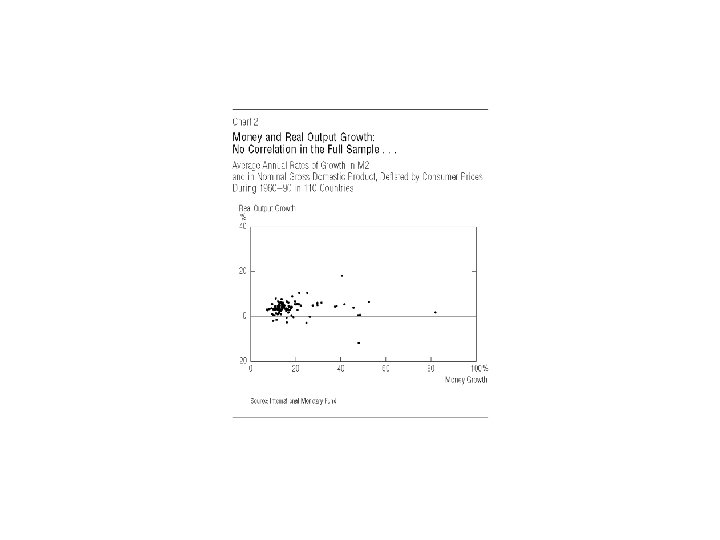

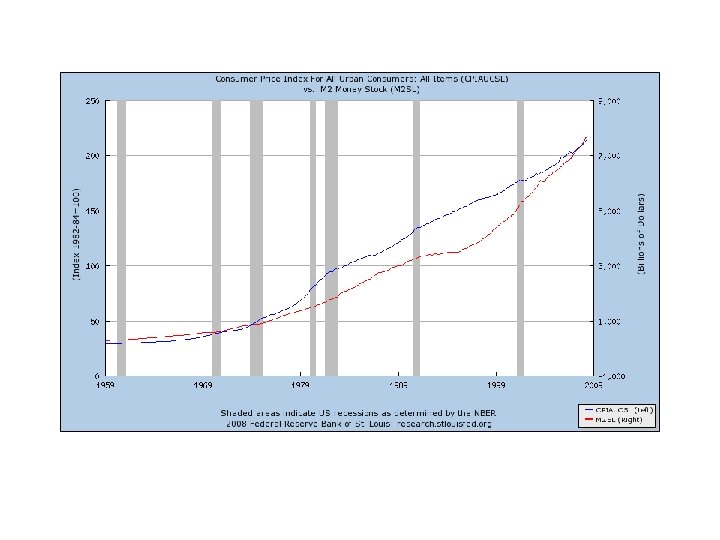

Linking money to the economy The effects of money in the long-run Quantity theory of money Assume: In the long-run 1) velocity independent of money stock; 2) output independent of money stock. → Changes in M cause proportionate changes in P (inflation). → Money is ‘neutral’ in the long-run.

Linking money to the economy The effects of money in the long-run Quantity theory of money Assume: In the long-run 1) velocity independent of money stock; 2) output independent of money stock. → Changes in M cause proportionate changes in P (inflation). → Money is ‘neutral’ in the long-run.

Linking money to the economy The effects of money in the long-run Quantity theory of money Assume: In the long-run 1) velocity independent of money stock; 2) output independent of money stock. Mechanism: when M rises (say), real money balances exceed the demand (which is independent of M by assumption); people try to get rid of excess money by spending. Because the amount of stuff to buy depends on resources and technology (which are independent of the stock of money), the only response is that overall prices are bid up.

Linking money to the economy The effects of money in the long-run Quantity theory of money Assume: In the long-run 1) velocity independent of money stock; 2) output independent of money stock. Mechanism: when M rises (say), real money balances exceed the demand (which is independent of M by assumption); people try to get rid of excess money by spending. Because the amount of stuff to buy depends on resources and technology (which are independent of the stock of money), the only response is that overall prices are bid up.

Linking money to the economy The effects of money in the long-run Quantity theory of money Assume: In the long-run 1) velocity independent of money stock; 2) output independent of money stock. M = (ky)P ∆M = (ky)∆P ∆M/M = (ky)∆P/M = ∆P/P

Linking money to the economy The effects of money in the long-run Quantity theory of money Assume: In the long-run 1) velocity independent of money stock; 2) output independent of money stock. M = (ky)P ∆M = (ky)∆P ∆M/M = (ky)∆P/M = ∆P/P