Money Market 2016 Master Students 28 oct.pptx

- Количество слайдов: 177

Money Market Introduction and Basics

Administrative Degree programme: Semester: Lecturer: Course methods: MIBF 1 Thomas Glanz ILV PRF Language: ECTS Credits: Places Available for Incoming Students: English 2. 0 4

Administrative Learning outcomes of the course unit The students are able to describe the organization and fundamental functions of Treasury departments in respect to bank controlling (matched market rate concept, funding, liquidity) and trading. The students have knowledge concerning the different asset classes and their products. They are capable of analyzing them and may also construct simple forecasting models for the different asset classes. Based on the results of these forecasting models, the students are able to conduct a portfolio selection. Furthermore, the students have the ability to conduct performance and attribution analyses, have a basic knowledge concerning alternative investments and structured products and know how to use these in a portfolio management process.

Course Contents short recapitulation of the most common products in the asset class money market, FX and equities; potential benchmarks for this asset class; usages of these asset classes like refinancing and hedging in the context of bank controlling) active vs. passive strategies; Estimation of the long-term return distribution of exchange rates; quantitative forecast models for the short-/mid-term distribution of exchange rates (e. g. time series analysis, neural networks, multiple regression on macro variables)trading strategies for this asset class controlling an MM+FX+EQ portfolio using derivatives; selection and optimization for an MM+FX+EQ portfolio: performance and attribution analysis for an MM+FX+EQ portfolio; linkage between treasury, risk and controlling

Timetable

Evaluation • Total points possible to achieve -> 100 Presentation October 24, 2015 -> 7 5 minutes person Midterm Test - October 31, 2015 -> 23 Final Exam – November 14, 2015 -> 70 Positive grade more than 50 points

0660 778 66 69")

Contact • glanz. thomas@gmail. com • SMS (NO calls!!) 0660 778 66 69

Quick Introduction • Given name • Profession • Previous Bachelor/Master

What is Money Market? • Mechanism dealing with lending and borrowing money (< 1 yr) • Highly liquid financial instruments • Short maturities • Cash or money substitutes • Very low default risk Liquidity shortages are funded, whereas excess liquidity is invested at short notice. Advantage? ? ? Cost savings (less reserves needed/tied up)

What is Money Market?

MM Conventions • Simple interest • Generally ACT/360 • Exceptions (ACT/365 for GBP, HKD, SGD, PLN, ZAR)

Day conventions

How to count the days? • Actual: actual numbers of days that elapse • 30: Each month counts as 30 days (remaining days in a month are subtracted)

How to count the days? • 30 E: Each month counts as 30 days (the 31 st is treated as if it was the 30 th; remaining days are subtracted) This method is used in the Euromarket (some continental European markets)

How to count the days? Calculate 1 st of March 2004 until 31 st of March 2004

How to count the days

Yield curve

Yield curve

Hypothesis of yield curve shape

Simple Interest Calculation Example: 1 month deposit of 5 m EUR at 3% (31 days) Interest = 5 m x 0. 03 x 31/360 = 12, 916. 67

Average Interest Calculation

• Capitalisation or compount interest. Investment over several terms without")

Effective Interest Rate (compound) • Capitalisation or compount interest. Investment over several terms without interest payments are paid out

Solution

")

Forward Rates (<1 year)

Future Value <1 year

Calculating present value <1 year

Example present value

Interest when PV and FV are known <1 year

Example

Converting discount rate into yield

Example

Converting MM to Bond Basis and vice versa

Non annual into effective IR

Example

Annual into non annual

Example

Example II

Maturities • O/N • T/N • S/N

Price of money • http: //www. youtube. com/watch? v=g. N 6 z 7 uru nf 0 • https: //www. youtube. com/watch? v=DSU 7 XH qvnl. E

Money Market Cash Instruments • • • Interbank Loans / deposits Repurchase-agreements Certificates of deposit Bills of exchange Commercial papers Federal saving bonds (T-bills) Non negotiable

Money Market Cash Instruments • Main goal of banks and other market participants – to maintain their liquidity • Participants with surplus may earn interest • Participants with shortage can borrow from liquid market • Result ? – If the money market is very liquid, banks assume that their demand of money can be satisfied easily and immediately. This means that they can work with a smaller amount of capital in order to increase their aggregate earnings .

Money Market Cash Instruments • Banks need liquidity to satisfy statutory regulations • Banks need to meet requirement to fully covering their obligations at any time • National Bank? – Controlling inflation – active policies in mm – Managing exchange rate (e. g. SNB 1. 20, Bo. J) – Controlling lending operations of the state

Coupon vs Discount Instruments • Coupon Instruments: Issued at face value – Notional and interest paid back at maturity • Coupon instruments: Interbank Deposits, CD´s, Repo • Discount Instruments: issued with discount from notional value. – Notional amount paid back • Discount instruments: CP, T-bills, Eligible bills

")

True yield vs Discount rate • Yield (interest rate p. a. , effective rate) – Quoted on basis of the invested capital (present value) • Discount rate: – calculated on basis of the future value

Cash Instruments

Interbank Deposits

Interbank Deposit

Interbank Deposit

Interbank Deposit

Interbank Deposit

Interbank Deposit Example

Interbank Deposit

Example

Euro Currency Market

Certificates of Deposit

Certificate of Deposit

Certificate of Deposit

Certificate of Depotis • Link to interest rates • http: //www. bankrate. com/cd. aspx • Insured by FDIC ? • http: //www. chicagofed. org

CD Primary Issue

CD Secondary Market

Example Secondary Market

Eligible Bills

Example

Commecial Papers

Conventions of CP

Origin of CP Market

Terms and Yield of CP

Ratings of CP

Treasury bills

Quotation Primary Market T-bill

Quotation Secondary Market

Example of discount instrument • You buy a EUR-CP, 100 EUR at 5% interest rate for 360 days. What • are the cash-flows? • T 0: 95, 238 [100 / (1+0, 05*360/360)] • T 1: 100

• A 1 -month deposit at 6 % p. a. (= 0. 5 % per month) • earns more interest than a 12 -month deposit at 6 % p. a. • 1 -month deposit at 6. 00 % p. a. (0. 5 % per month) • comparable annual yield = (1, 005)12 – 1 • = 0. 0616778 or 6. 16778 % • 12 -month deposit at 6 % p. a. • comparable annual yield = 6. 00 %

A US commercial paper is issued on Sep 30, 20 XX with")

Calculations 1) A US commercial paper is issued on Sep 30, 20 XX with a discount of 2% and a nominal of 10 m USD. Maturity is Oct 31, 20 XX a) Which amount do you receive when you issue the CP? b) Whats the annual yield Solution: Sep 30 to Oct 31 (ACT): 31 days PV=10 m-(10 m x 0. 02 x 31/360)= 9, 982, 777. 78 r=0. 02/(1 -0. 02 x 31/360)=0. 02003

A EUR CP is issued with an interest rate of 6")

Calculations • 2) A EUR CP is issued with an interest rate of 6 percent with 60 days to maturity and a nominal of 5 m EUR a) Which amount do you receive when you issue the CP? b) Calculate the annual yield Solution: 5 m / (1+0. 06 x 60/360)=4, 950, 495. 05 Annual yield: 6 percent

Assuming 1 year maturity which instrument has the highest yield? –")

Calculations • 3) Assuming 1 year maturity which instrument has the highest yield? – US-CP 5% – EUR-CP 5% – T-Bill 4. 5% – EUR CD 4. 5% Solution: same maturity discount higher than yield Therefore: US-CP

quotes")

Calculations • The price of a 90 day USD T-bill (nominal 1 m) quotes currently for 994, 000 USD. Whats the annual discount factor and the annual yield? Solution: discount 1 m – 0. 994 m=6000 d=6000/1 m x 360/90=0. 024 or 1 m-(1 m x „X“ x 90/360)=994. 000 r=0. 024/(1 -0. 024 x 90/360)=0. 02414

long with a forward")

Calculation • You are a GBP 9/12 FRA (91 days) long with a forward rate of 4 percent was fixed. After 3 months spotrate is EUR/GBP 0. 8562 and interest rates are: Deposits Maturity Rate days 3 months 3. 3% 91 days 6 months 3. 4% 183 days 9 months 3. 5% 274 days 12 months 3. 6% 365 days 3/6 3. 47% 92 days 6/9 3. 639% 91 days 9/12 3. 801% 91 days FRA Whats the marketvalue of the FRA in GBP and whats the market value in EUR?

=100 mx(0.")

Solution FRA • 9 months spot rate and 6/9 Forward rate • PV(GBP)=100 mx(0. 03639 -0. 04)x 91/365 (why 365? ? ) 1+0. 035 x 274/365 Result: - 87, 698. 55 GBP • PV(GBP)= -87, 698. 55/0. 8562 = -102, 427. 65

It is Friday and you need to refinance 100 m EUR. Therefore")

Overnight 1) It is Friday and you need to refinance 100 m EUR. Therefore you decide to take an overnight loan for following quotation 0. 08%/0, 15%. What amount do you have to pay back? 2) It is Monday and you have excess liquidity in GBP. You decide to invest overnight for 0. 30%/0. 45%. How much will you receive back?

•")

Solution Overnight • 100 m + (100 m x 0. 0015 x 3/360) • Or 100 m x (1+0. 0015 x 3/360)= 1 m + 1250 EUR • 100 m x 0. 003 x 1/365 = 821. 92 GBP

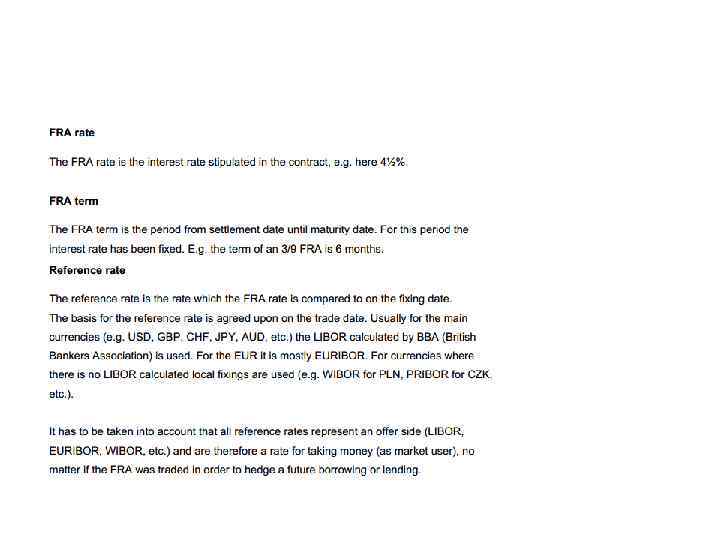

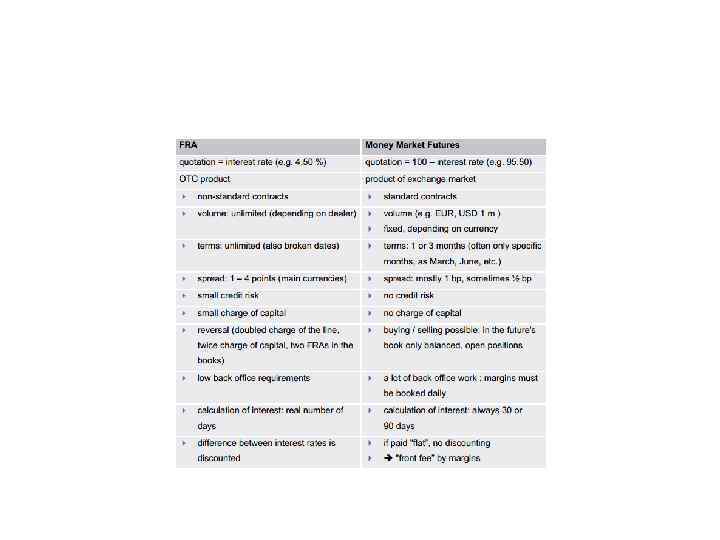

FRA

FRA Terminology

FRA

Example

Solution Example

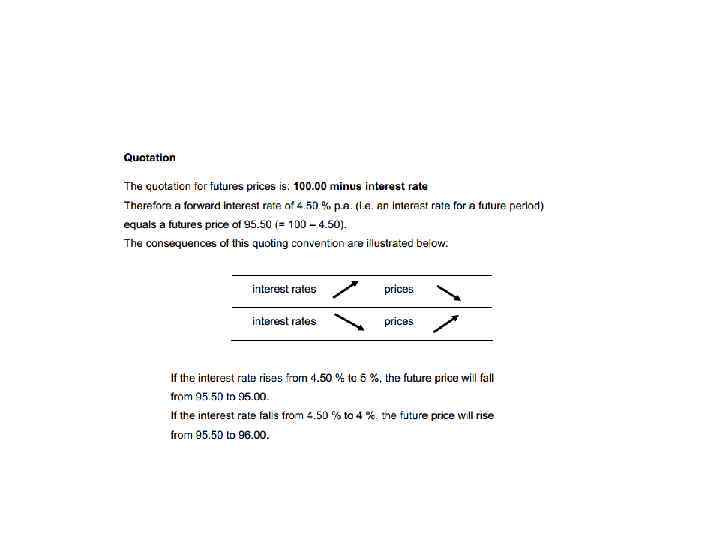

FRA Quotation

Example for Quotation

FRA

Credit Risk FRA

Principle of FRA

FRA and Yield curve

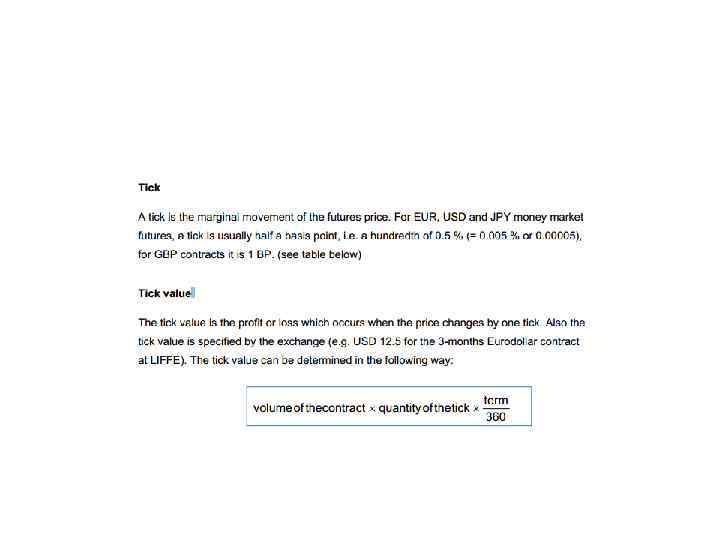

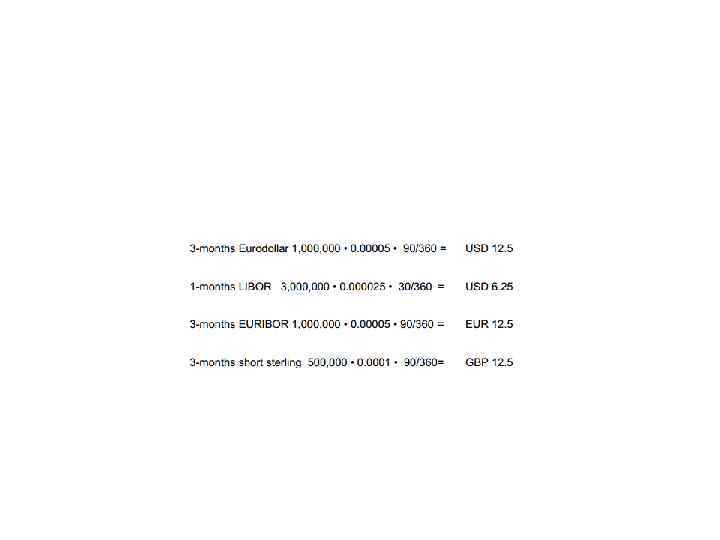

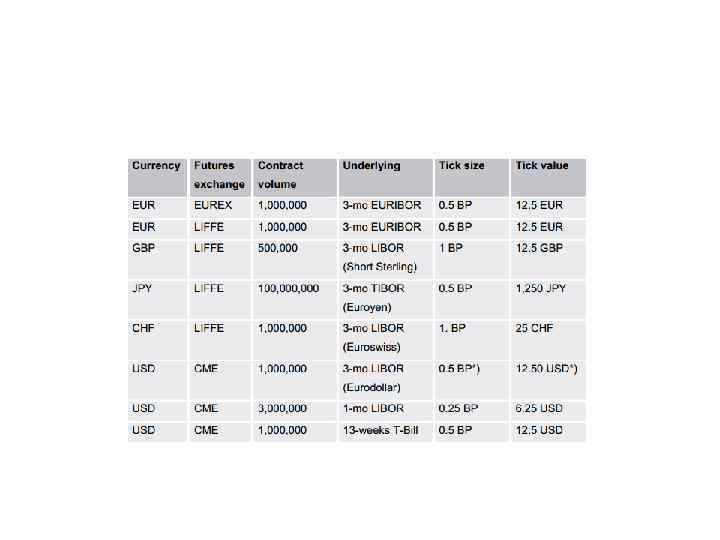

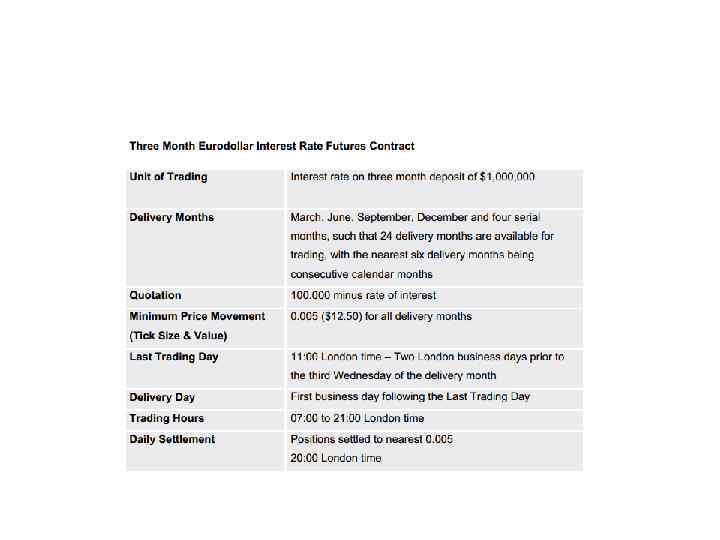

MM Futures

MM futures

MM futures conventions

Margin System • Margin reduces credit risk to a minimum • Initial Margin: fixed amount up-front • Variation Margin: difference of closing price and closing price. Daily settlement. • Example: buy 100 Eurodollar Futures. – Price 96. 60 – Next day closing price 96. 65 • Change 5 bp (10 ticks) x 25 (12. 5) x 100 = 12. 500 credit – Next day closing price 96. 57 • Change 8 bp (16 ticks) x 25 (12. 5) x 100 = 20. 000 charge

Open Interest

Calculating FRA from Future Price • If maturity and period of FRA matches with future, you can derive FRA rate from future price. • Future Strip – Trade date: Friday Apr 08 2005. What is the bid rate of a 2/11 IMM Fra – You can buy futures strip JUN, SEP and DEC

Derive IMM FRA rates Then effective rate formula:

NON IMM FRA • Effective rate weighted with period • Example: start Fri Apr 08, 2005 and Spot value Tue Apr 12, 2005 – What is the bid rate of a 3 x 9 spot FRA (184 days)

EXAMPLE non IMM FRA Calculate!

Convexity

Convexity Example

Calculate Hedge Ratio

Hedge Ratio

FX Spot • Sale of one currency for another (delivery usually 2 days after the deal)

FX Spot • Delivery date called value date • 2 Business days (exception USD/CAD 1 working day) • FX markets in middle east closed on Friday but opened on Saturday.

SWIFT codes • 3 letter code used for SWIFT messages • Became international accepted standards • Some nicknames are common – GBP/USD: cable – CHF: Swissi – SEK: Stocki – AUD: Aussi – NZD: Kiwi

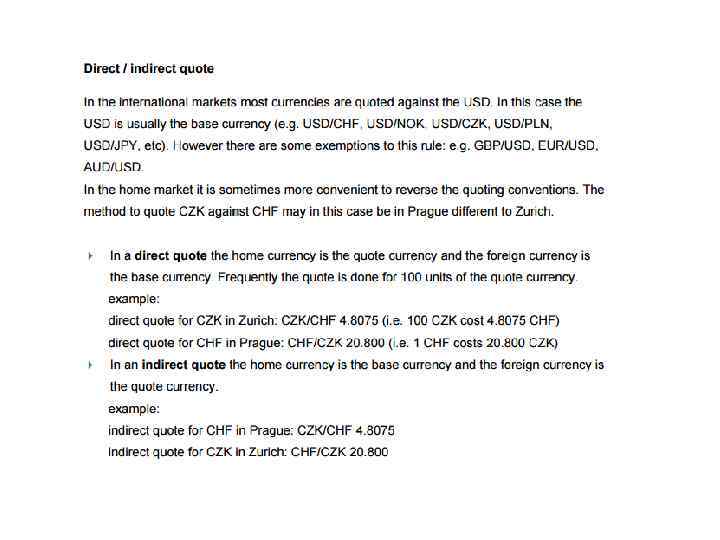

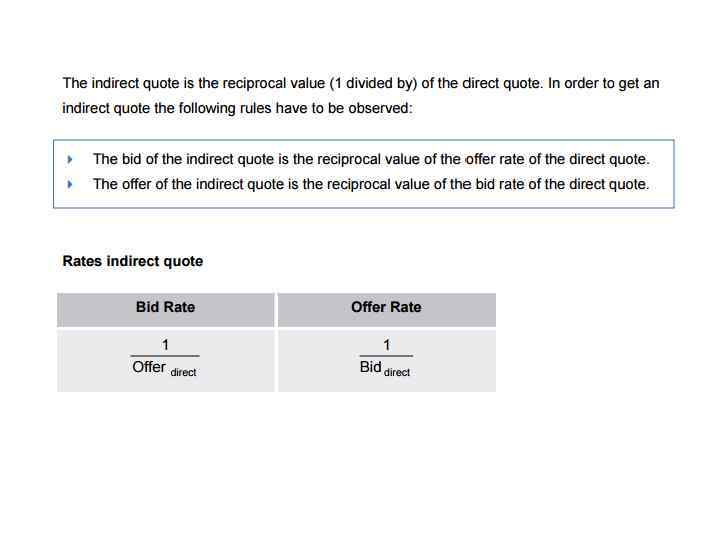

Base currency and quote currency • 1 unit of base currency equals to XX units of quote currency – Base ccy/quote ccy e. g. EUR/USD

Overview Ccy codes

Bid and offer Rate

Example

PIP • 1/100 of a currency – USD 0. 0001 – BUT YEN it is 1/100

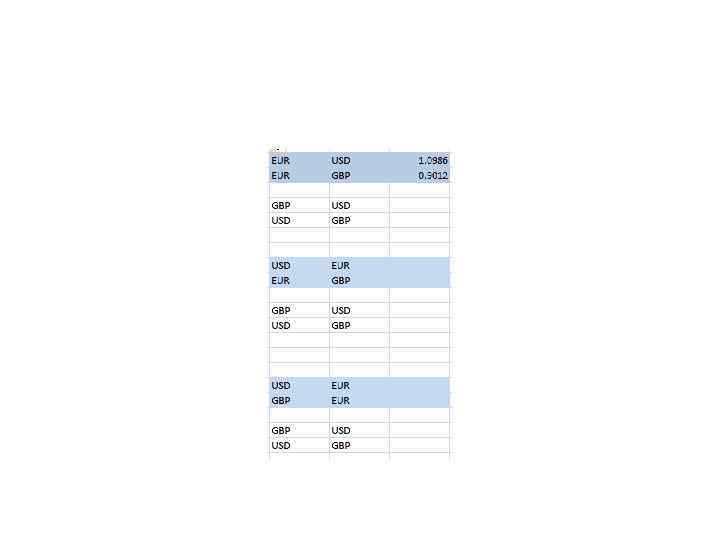

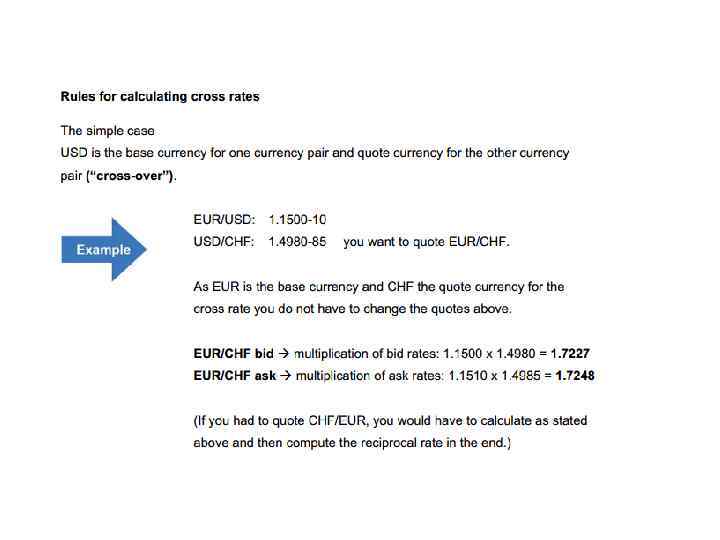

Cross Rates

Cross Rates

and the Swiss franc,")

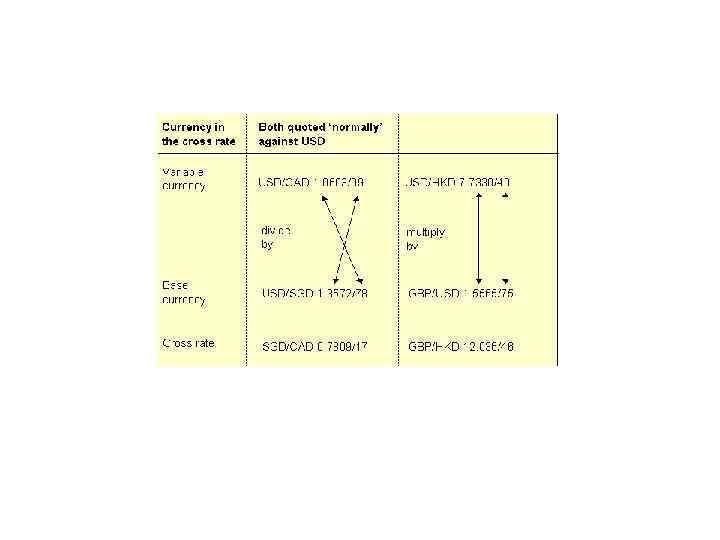

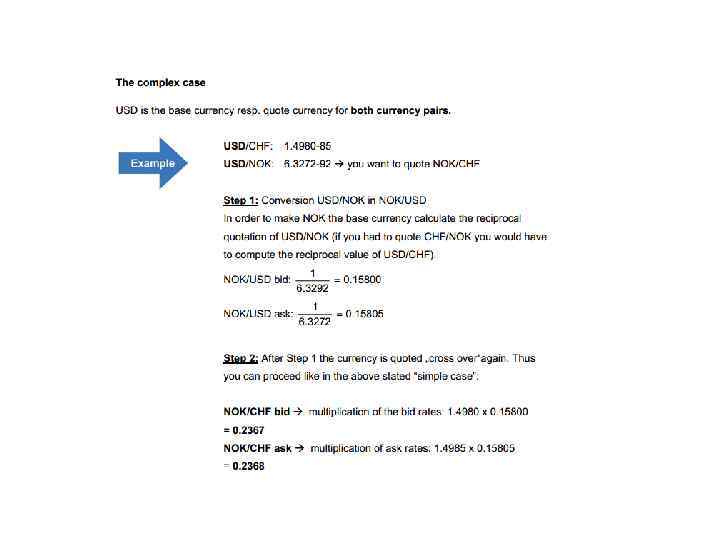

Cross Rates I • Let us take the yen (JPY) and the Swiss franc, for instance. Having the quotes of USD/JPY and USD/CHF against the U. S. dollar on hand, we can deduce a cross rate of the Swiss franc against the yen using the fractions methods. • CHF/JPY = USD/JPY : USD/CHF, • that means it is necessary to divide USD/JPY by USD/CHF. For instance, if USD/JPY costs 104. 78 and USD/CHF is 1. 0505, the cross rate of the Swiss franc against the yen will be equal to rounded CHF/JPY 99. 74.

Cross Rates II • The second type of calculation is used for the currencies with direct and reverse quotations against the U. S. dollar (in this case the dollar is the base currency of the pair for one currency and quoted currency for another). Let us consider the yen (JPY) and the Australian dollar (AUD). Keeping in mind the quotes of USD/JPY and AUD/USD against the U. S. dollar, we can deduce by the fractions rules the cross rate of the Swiss franc against the yen. • AUD/JPY = AUD/USD * USD/JPY, • So one has to multiply AUD/USD by USD/JPY. For instance, if USD/JPY worth 104. 78 and AUD/USD costs 1. 0564, the cross rate of the Australian dollar to the Japanese yen is equal to rounded AUD/JPY 110. 69.

Cross Rates III • The third type of calculation is used for the currencies with the reverse quotations against the U. S. dollar (dollar is the quoted currency for the both currencies). Let us consider the British pound and the Australian dollar. Having the GBP/USD and AUD/USD quotations against the dollar, we can deduce by the fractions rules the cross rate of British pound against the Australian dollar: • GBP/AUD = GBP/USD : AUD/USD, • i. e. we have to divide GBP/USD by AUD/USD. For instance, if GBP/USD is 0. 5028 and AUD/USD is 1. 0564, the cross rate of the British pound for the Australian dollar is equal to rounded GBP/AUD 0. 4760.

Cross Rate Bid Ask • It should be noted, that we have excluded from our consideration the notion of bid and ask price of the currency rate to simplify the calculation formulas, and we have used only current (spot) prices until now. But each major (dollar) quotation has two prices, as well as the crosses. So where should we put the bid and ask prices? The answer to this query is in understanding of logics of the cross rates calculation. Let us return to our example of the first type calculation, which involves the Swiss franc (CHF) and the yen (JPY). We are interested in the cross rate quotation CHF/JPY. In order to define the bid price of the Swiss franc in this quote (the bid/ask rates, as we have just known, always refer to the base currency) we need to think the following way. As we are interested in buying the Swiss francs, we have to purchase the dollars for the Japanese yens first, and then sell them for the Swiss francs. Thus, the bid rate of the USD/CHF pair is important for us. we should also consider the ask price of the USD/CHF quote. Thus, the bid price of the Swiss franc to be exchanged for the Japanese yen in the cross pair CHF/JPY is calculated by the following formula:

= USD/JPY(bid) : USD/CHF(ask) • In the same manner one can")

• CHF/JPY(bid) = USD/JPY(bid) : USD/CHF(ask) • In the same manner one can deduce a formula for the ask price of the Swiss franc vs the Japanese yen in the CHF/JPY cross pair quotation: • CHF/JPY(ask) = USD/JPY(ask) : USD/CHF(bid) • In the examples of the second and the third types of calculation we use the same formulas: • AUD/JPY(bid) = AUD/USD(bid) * USD/JPY(bid), • AUD/JPY(ask) = AUD/USD(ask) * USD/JPY(ask), • GBP/AUD(bid) = GBP/USD(bid) : AUD/USD(ask), • GBP/AUD(ask) = GBP/USD(ask) : AUD/USD(bid).

• http: //support. instaforex. com/en/Chapter_7_ Cross-rates

Cross Rate example

Cross Rate Example

at a")

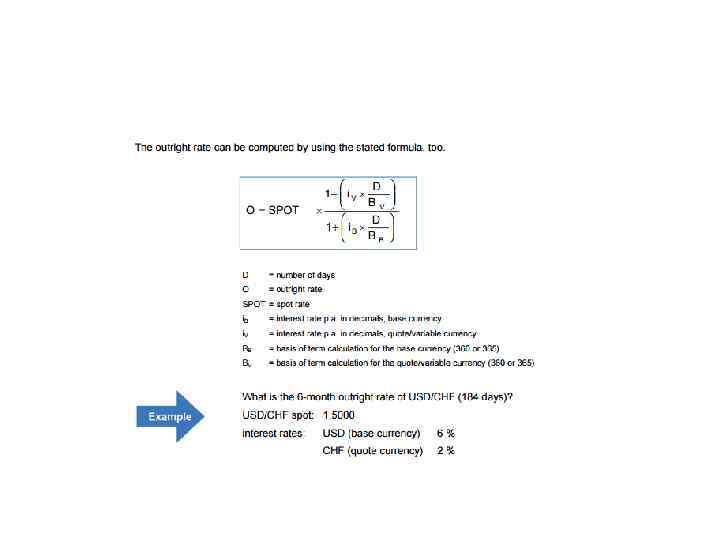

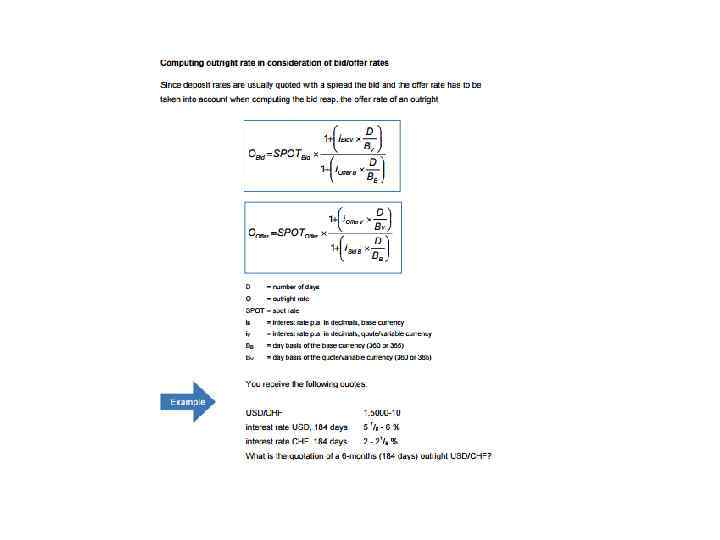

FX Forwards Outright • You exchange currencies in the future (fixed date) at a fixed rate • OTC contract • Outright rate differs from spotrate BUT are NOT a forecast for the spot rate at the end of the term! • Difference solely based on current interest differential

EXAMPLE USD/CHF spot 1. 5000 USD 6 month deposit rate = 6% CHF 6 month deposit rate = 2% Days = 184 You are long USD/CHF value date 6 months and you want to hedge the FX risk. • What can you do? • • •

Solution • You sell US spot against CHF f. e. 1, 000 for the rate of 1. 5000 – You take 1 m USD deposit for 6 percent – You give CHF deposit (1 m * 1. 5000 = 1. 5 m CHF) – 1 m USD * (1+0, 06/360*184)=1, 030, 666. 67 – 1. 5 m CHF * (1+0, 02/360*184)=1, 515, 333. 33 • 1, 515, 333/1, 030667=1. 4702 – You can also use the formula and will have same result!

for EUR/USD.")

Example II • What is the 1 year forward rate (365 days) for EUR/USD. Current spot rate equals 1. 2600 – Interest rates are EUR 2% and USD 4% (fictive!) – Solution: 1. 26 * 1+(0. 04*365/360) 1+(0. 02*365/360)

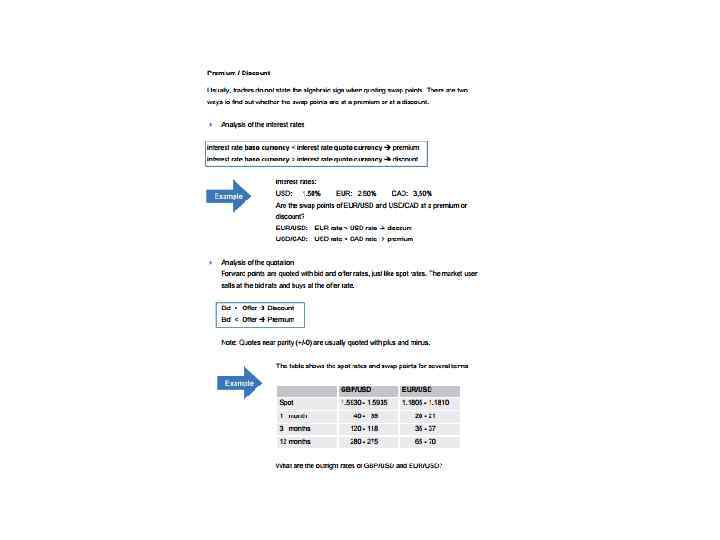

• Premium or")

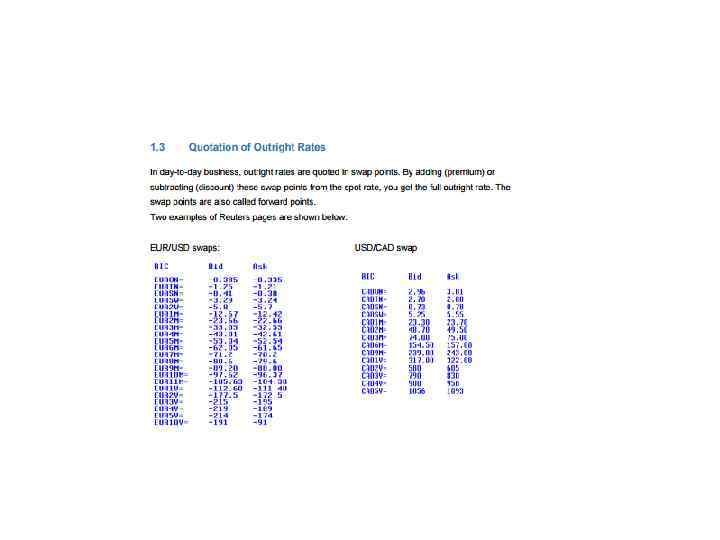

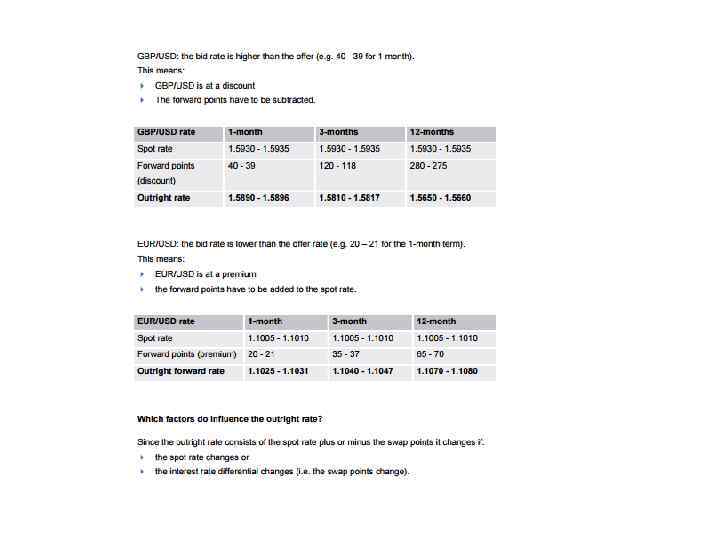

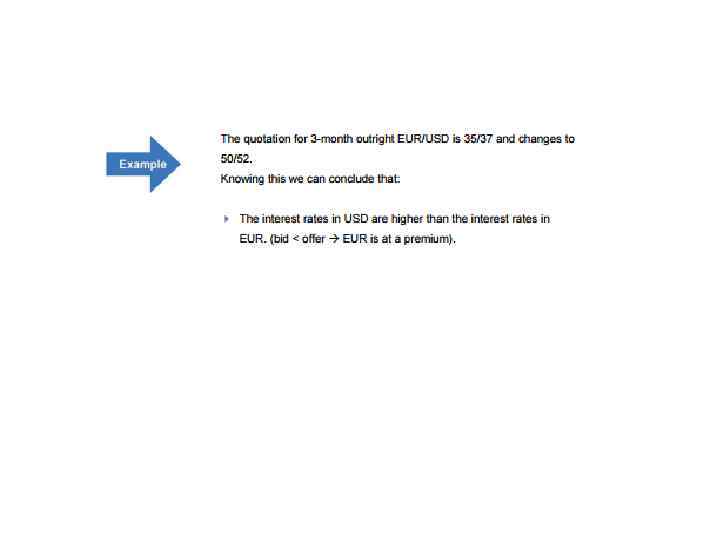

Quotation • Outright rates are quoted in swap points (forward points) • Premium or discount – If forward rate is greater than current spot rate = premium – If forward rate is less than the currecnt spot rate =disount • Base currency interest rate > quote currency -> discount and vice versa

FX Outright

• http: //www. financetrainer. com/fileadmin/inh alte/TOOLS_SKRIPTEN/0102_forwarde. pdf

FX Swaps • Contract between 2 parties to exchange currencies at spot and exchange them back later • You take the mid price You buy and sell a 10 m 6 months (181 days) EUR/USD FXS at 64. 82/64. 22. The spot rate is 1. 3015/30. What are the cashflows?

/2 • Then we deduct")

Solution • First we need the midprice (1. 3015+1. 30330)/2 • Then we deduct the swap points 0, 006482 • Result: 1. 295768 • Cashflow t 0 – + 10 m /- 13, 022, 500 (midprice!!) • Cashflow t 0, 5 – - 10 m/+12, 957, 680

Repos • Eighter a mechanism for borrowing/lending funds on a secured basis • Or a method of borrowing/lending securities against cash • Classic repo = one contract • Sell/buy-back = 2 contracts • Security lending

Repo

Repo • Security not pledged but sold -> legal title transferred -> ? ? • To deliver back not necessarily same securities • Risk and return remains with……? ? – -> economic ownership remains with…. ? ? ? • Who receives coupon or dividend? • What happens with it? (manufactured dividend)

– Act/360 or Act/365 (GBP) •")

Repo • Quotation p. a. (like interbank deposits) – Act/360 or Act/365 (GBP) • • Always based on securities -> seller is who? Buyer (reverse repo) is who? Bid rate higher than offer rate. (3. 28 – 25) Market maker buys at the bid rate (seller has to pay the higher interest) and sells it at offer rate (buyer receives the lower interest)

Types of Repo´s

Legal Framework

• Focus on the cash • Whats the difference")

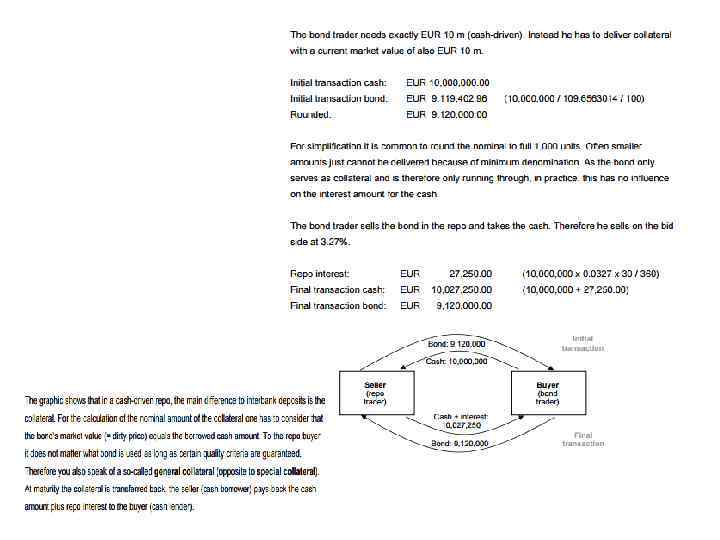

Cash driven repo (most common) • Focus on the cash • Whats the difference to interbank deposit? ? – Therefore …………. . lower refinancing rate – And …………reduced credit risk.

Cash driven repo

Classic Repo Cash Driven

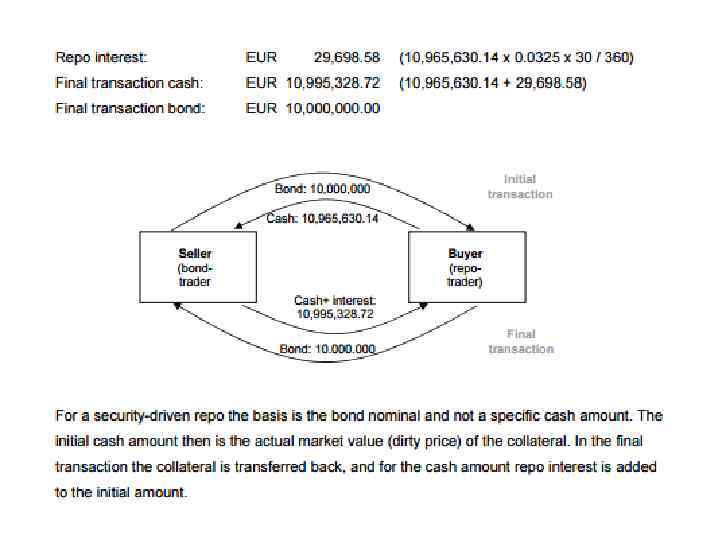

Security driven repo

Classic repo – security driven

Classic repo security driven

Repo market participants

Repo market participants

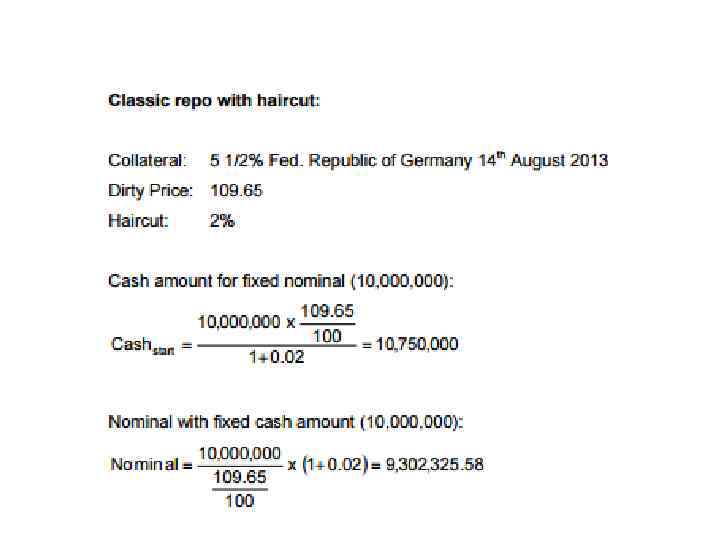

Initial Margin / Haircut

Calculation of haircut

Variation Margin

")

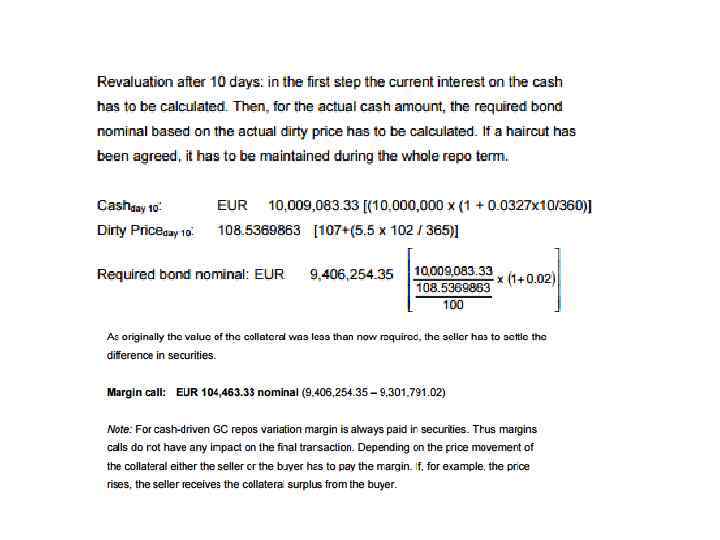

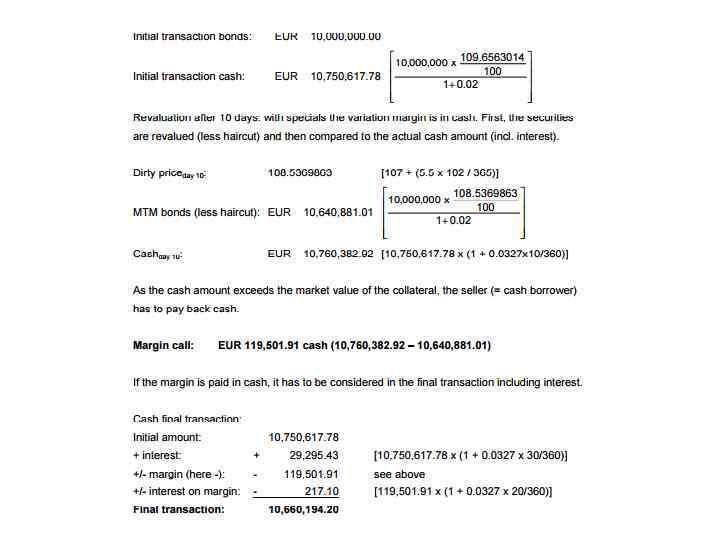

Margin Call (cash driven GC)

Margin call – security driven

Money Market 2016 Master Students 28 oct.pptx