ecfcf6a4601cbef6f8143ddce353bec6.ppt

- Количество слайдов: 84

Module III: Financing

What is a Business Plan • Roadmap to success • Written document describing all relevant internal and external elements and strategies for starting a new venture • Where I am Where am I going • How to get there? • Guide and structure to manage in the dynamic world.

For preparing a Business Plan we must answer a following questions: 1. WHAT is a Business Plan? 2. WHO needs a Business Plan? 3. HOW to prepare a Business Plan?

Who draws it • • • Entrepreneur with help Skills required: Financial – tax Plan, forecasts Mkt People mgt Designing Organizing The entrepreneur assesses his own skill and takes partners to strengthen weakness.

Who uses • Investors Banker • VC • Advisors Suppliers • Employees • Contents influence the reader Therefore all issues must be addressed.

Who needs a business plan? • You need a business plan if you’re running a business; • You need a business plan if you’re applying for a business loan; • You need a business plan if you’re looking for business investment, new products or new services; • You need a business plan to communicate with a management team.

Business plan based on » Entrepreneurship » The business idea » Business areas

Outline of a business plan Executive summary Business description: products and services offered Market strategies Competitive analysis and positioning Operations and management plan Financial components - condensed information on each of-the chapters bellow type of business; - products and services - operations plan; offered; - management team. - market and target market; - ownership of the business --demand requirements and capital for the product or and its service; legal analysis; - competitionstructure; sources; - profitability consideration. - promotion; - -identification of balance sheet; - dissemination and -competitive strenght break-even analysis; delivery; position. - income statement; - pricing projection. - cash flow strategy.

PROJECT FINANCE What is Project Finance • Project financing refers to a financing in which lenders to a project look primarily to the cash flow and assets of that project as the source of payment of their loans.

Stages of Financing Early stage financing/ seed financing Expansion Financing Mezzanine financing Provided for product development, for initial marketing To support production activity requiring Inventories and sales. For introduction of new product line, new technology, additional product development

• Bridge financing: refers to short term funding requirement pending the flow of funds expected from different anticipated and expected sources. • IPO DRIVEN COMPANIES • RESTRUCRUTING IS UNDERTAKEN • Acquisition/ Buyout financing: AF to finance acquisition deal to expand business. While leveraged buyout financing enables an operating management group to acquire a product line or business from either private or public company.

What are the different sources of project financing available? Internal Sources External Sources

Sources of Internal Funds • Bootstrapping: that’s using one’s own money to get one’s business off the ground. It is a way of starting a venture or expanding one’s operation without depending on outside sources of funding. Methods for funding through bootstrapping: Trade credit customers Cash flows Real estate Equipment suppliers

Internal source of finance: Business Growth

Internal Sources of Finance and Growth • • ‘Organic growth’ – growth generated through the development and expansion of the business itself. Can be achieved through: Generating increasing sales – increasing revenue to impact on overall profit levels Use of retained profit – used to reinvest in the business • Sale of assets – can be a double edged sword – reduces capacity? •

External Sources of Finance • Long Term – may be paid back after many years or not at all! • Short Term – used to cover fluctuations in cash flow • ‘Inorganic Growth’ – growth generated by acquisition

– Ordinary Shares")

Long Term • Shares (Shareholders are part owners of a company) – Ordinary Shares (Equities): • • Ordinary shareholders have voting rights Dividend can vary Last to be paid back in event of collapse Share price varies with trade on stock exchange – Preference Shares: • Paid before ordinary shareholders • Fixed rate of return • Cumulative preference shareholders – have right to dividend carried over to next year in event of non-payment – New Share Issues – arranged by merchant or investment banks – Rights Issue – existing shareholders given right to buy new shares at discounted rate – Bonus or Scrip Issue – change to the share structure – increases number of shares and reduces value but market capitalisation stays the same

– Debentures")

Long term • Loans (Represent creditors to the company – not owners) – Debentures – fixed rate of return, first to be paid – Bank loans and mortgages – suitable for small to medium sized firms where property or some other asset acts as security for the loan – Merchant or Investment Banks – act on behalf of clients to organise and underwrite raising finance – Government/EU – may offer loans in certain circumstances • Grants

Short Term • • • Bank loans – necessity of paying interest on the payment, repayment periods from 1 year upwards but generally no longer than 5 or 10 years at most Overdraft facilities – the right to be able to withdraw funds you do not currently have – Provides flexibility for a firm – Interest only paid on the amount overdrawn – Overdraft limit – the maximum amount allowed to be drawn - the firm does not have to use all of this limit Trade credit – Careful management of trade credit can help ease cash flow – usually between 28 and 90 days to pay Factoring – the sale of debt to a specialist firm who secures payment and charges a commission for the service. Leasing – provides the opportunity to secure the use of capital without ownership – effectively a hire agreement

'Inorganic Growth' • Acquisitions • The necessity of financing external inorganic growth – Merger: • firms agree to join together – both may retain some form of identity – Takeover: • One firm secures control of the other, the firm taken over may lose its identity

Seed Funding • This is meant for developing a business idea, creating the first product and test marketing the new product or service for the first time. Sources are: 1. Government 2. Angel or private investors

Angel Investors • Individual venture capitalist interested in providing budding entrepreneurs with seed and start up financing are called as Angel Investors. They are also called as Business Angels are private investors who invest in unquoted small and medium sized businesses. They provide not only finance but experience and business skills. Business Angels invest in the early stage of business development filling, in part, the equity gap. • Provides capital for business start up • Look forward for equity stake in company. Benefits: 1. Advice based on experience in technology and marketing. 2. Networking with customers for sales. 3. Contacts for raising further money. 4. Far less intrusive and interfering as compare to venture capitalist.

• Business owners often report that company finance of Rs. 10, 000 to 250, 000 can be very difficult to obtain - even from traditional sources such as banks and venture capitalists. Banks generally require security and most venture capital firms are not interested in financing such small amounts. In these circumstances, companies often have to turn to "Business Angels". • Business angels are wealthy, entrepreneurial individuals who provide capital in return for a proportion of the company equity. They take a high personal risk in the expectation of owning part of a growing and successful business.

Types of Angel Investors • Corporate angels: Senior professionals at fortune 1000 corporations who have been laid off with generous severances or have taken early retirements. • Entrepreneurial angels: Most of them own and operate highly successful businesses and are really looking for synergy with their current business, a way to diversify their portfolio.

• Enthusiast angels: For them investing and encouraging new start ups is a hobby and thus they do not seek a role in management or a place on the board. They tend to invest in technology that can bring out a major change in markets in future. • Micro management Angels: They are very serious investors most of them attain their wealth through their own efforts. They look forward to have a controlling position and active role in the company strategy.

• Professional angels: They like to invest in companies that offer products or services in which they have a rich professional background and thus offer their sector expertise to the investee company without getting deeply involved in the business. • Where to look for angel funding: a. Universities b. Business Incubators

Venture Capital

Venture Capital

Venture Capital • Pooling of capital in the form of limited companies – Venture Capital Companies • Looking for investment opportunities in fast growing businesses or businesses with highly rated prospects • May also buy out firms in administration who are going concerns • May also provide advice, contacts and experience

NATURE OF VC INVESTORS IN VC MANAGED BY VC FIRM • Wealthy partners • Pension funds • Other institutions • Foreign Investors PROVIDE FUNDS GAIN RETURN FEES

• Venture Capital funds in India are governed by the SEBI is the nodal agency for registration and regulation of domestic overseas venture capital funds. • It provides broad guidelines and procedures for the establishment of venture capital funds both within India and outside it; their management structure and set-up as well as size and investment criteria of the funds.

What is VC? • • Investment in High risk projects High return potential projects Equity related instruments

BUSINESS ANGELS & VENTURE CAPITALISTS • Main Differences • Business Angels • Venture. Capitalists • Personal • Entrepreneurs • Money managers • Money Invested • Own money • Fund provider • Firms funded • Small, early stage • Medium to large • Due diligence done • Minimal • Extensive • Location of inv. • Of concern • Of lesser concern • Contract used • Simple • Comprehensive • Monitoring after inv. • Active, hands-on • Strategic • Involvement in mgt • Important • Of lesser concern • Exiting the firm • Of lesser concern • Highly important

Venture capitalist VS Banker VC Banker Equity participation Lends money Participation in management No involvement in management Keeps collateral

Structure of VCs • Mostly funds – Charge about 2% + success fee • Also companies • Limited partnerships • Prevalence of banks – Revenue implications

VC : Advantages • • No fixed expense of debt servicing Financial flexibility Sharing of risk Value added investing – Attracting talent – Networking with service providers/suppliers – Accessing markets • Enhanced credibility with lenders

VC : Disadvantages • • Dilution of shareholding Increased 3 rd party governance Increased controls Increased commitment to stated strategy

Types of VC Early stage financing • Seed capital or pre-start up or R&D • Start up financing • Second round financing Later stage financing • Expansion • Replacement • Turnaround

VC investment & exit

Venture Capital In India Overseas venture capital has been allowed In India with effect from September 1995. Idea is to help smaller unlisted companies.

Number Of Investments Investor 2005 2006 2007 2008 2009 Total Sequoia Capital India 7 12 13 18 3 53 Ventureast 5 11 4 9 3 32 Intel Capital 3 7 4 8 1 23 Helion Venture Partners 0 4 8 8 2 22 DFJ India 0 3 3 9 2 17 Nexus India Capital 0 1 4 9 2 16 NEA Indo. US Ventures 0 0 5 9 0 14 IDG India Ventures 0 0 6 5 0 11

VC financing of SMEs takes the form of equity (shares, rights, warrants, convertibles. . ) • Time period – 4 -7 years • Target rate of return – 30 -40% • Financial partners required high rate of return 2 main exits: IPO, trade sale • IPO – firms issues shares to the public – become public • Trade sale – firms is sold to larger company

The Role of the VC n n n Board involvement Management recruitment Future capital raising Access to business network Strategy development Patience!

Future of VC in India • Potential is there, needs to be tapped • Lack of appropriately trained persons to manage funds • General public, including others like bank staff, CAs, legal advisors etc. not completely aware of finer points of such funding • The entrepreneurial ecosystem is yet to develop, of course some cities like Bangalore are slowly having a variety of experts in this space

Future VC in India • There are limited takers for smaller projects • Real early stage, high growth, high risk projects, finding it difficult to raise funding • There are issues of exit and other related issues

Funding from banks • Criteria for lending decisions by banks Character collateral conditions Criteria for lending Decisions By banks Competence and commitment capacity capital

Lending strategy of banks • • Business plan Financial statement Profile of promoter Asset base – Gross – Net • Credit scoring

How Banks cover risks • Collateral – Internal incl. a/c receivable – External • Personal guarantees • Debt covenants • Short maturity debt

• Banks mainly extend two types of facilities: a. Non Fund based limits: involve a commitment without outflow of cash unless and until such facility devolves on to a bank. b. Fund based Limits: involve money given to the company in the form of cash.

Why the difficulty to get loans • • • No guarantee BANK afraid of NPA Poor information Fear of bank harsh actions Complex and documentary procedures Corruption Inconvenient and costly to maintain proper books of a/c for monthly reports Third party guarantee in shadow Display of bank name prominently Managerial incompetence & ignorance of standards. Severity of competition lowering prices-poor cash cycle

Managing banks • • Complete paperwork in time Submit financial statements as scheduled Route all transactions through bank Ask for extras – free drafts, alerts, etc show confidence and well being Transmit good news Be proactive about inspections

Relevance of financial statements Good idea Good opportunity Good market potential Good Financials Degree of financial strengths and weaknesses can be measured through financial statements

")

Purpose of financial statements ( profit &loss a/c, Balance sheet, Fund flow, Cash flow) • A financial statement is a written document that provides a gist of the venture’s accounting data and indicates the venture’s financial conditions / position. • It indicates the present and expected financial health of the venture. • It is a tool used for financial reporting of the business to different stakeholders.

Effectiveness of financial statements • • • Simplicity Understandability Reliability Compatibility Relevance True and fair representation of facts.

Financial Statements • Balance Sheet • Income Statement • Statement of Cash Flows

Basic Financial Concepts Financial Statements – Income Statement • How much money we made in the period – Revenue less Expenses • Continuity of Retained Earnings – At the bottom of the IS we add the current period’s income to the Retained Earnings at the beginning of the period (opening RE) to get Retained Earnings at the end of the period (closing RE)

Basic Financial Concepts Financial Statements – Balance Sheet • How much we have, what we owe, and what we’re worth – Assets – Liabilities – Equity

• Fund flow statement: keep track of all inflow and outflow of funds that might have occurred through cash receipts and payments or otherwise. • Cash flow statement: Reports a company’s change in cash and cash equivalents from one balance sheet date to another. The cash flow statement classifies the amount of the cahnge according to operating, investing and financing activities.

Basic Financial Concepts Financial Statements – Statement of Cash Flows • Where the cash came from and where the cash went – Shows how each of the 3 business activities affected cash during the period

Basic Financial Concepts The Activities of a Business • Each business has 3 types of activity – Operating Activities – Investing Activities – Financing Activities

Basic Financial Concepts The Activities of a Business - Operating Activities • The activities that the business was formed to carry out – Most items found on the Income Statement • Day to day sale of goods, advertising, wages • Excludes some unusual activities on the IS: e. g. Gain on Sale of Assets – Some activities not found on the Income Statement • Pay money we owe to a supplier • Collect money from a customer

Basic Financial Concepts The Activities of a Business – Investing Activities • Purchase or sale of fixed assets – Buy land or a building – Sell a car – Purchase production equipment

Basic Financial Concepts The Activities of a Business – Financing Activities • Getting enough money to run the business – Borrow money from the bank – Repay money to the bank – Pay interest to the bank – Issue new shares

Basic Financial Concepts The Activities of a Business • The 3 activities can be found in certain parts of the FS – Operating activities • Income Statement (after adjusting for non-operating items) • Balance Sheet (current assets & current liabilities) – Investing Activities • Balance Sheet (fixed assets) – Financing Activities • Balance Sheet (non-current liabilities & Equity)

CASH FLOW Many profitable firms round the globe fail becau of lack of cash…. .

Basic need for cash Repayment of • Creditors , employees , lenders or for unforeseen events Failure to it • Bankruptcy, negative impact on creditworthiness

CASH FLOW INCREASE IN CASH DECREASE IN CASH ACCOUNTS PAYABLE ACCOUNTS RECEIVABLE PRODUCTION/ CASH PURCHASES CASH SALES INVENTORY

Effective Cash Management • Meticulously analyses cash flows from the business. • Prepare a working cash flow budget • Continuously monitor the cash flow budget. • Find ways and means to improve cash flows • Use most efficiently the available cash.

Financial Projections Overview • Financial projections: simply future Financial Statements – Projected Balance Sheet – Projected Income Statement – Projected Statement of Cash Flows • A “Baht & Satang” summary of the business plan – Your business plan in the language of numbers

Financial Projections Overview The projections must be consistent with and support the written part of the business plan Any difference between the written plan and the projections means instant loss of credibility and NO MONEY from your potential investor!!!

Financial Projections Overview Elements & Chronology of the Projections • Explicitly stated assumptions • Projected Income Statement • Projected Statement of Cash Flows • Projected Balance Sheet • Analysis

Break- Even Analysis • It helps an entrepreneur to know how many units need to be sold, so as to achieve a break –even point, thus implying a point wherein the venture achieves a state of no loss no profit, i. e. sales is adequate enough to take care of cost of production. Total cost= F. C + V. C T. C. = F. C + C * Q C= per unit v. c of production and Q is the no. of units produced. BEP IS T. C=T. R SALES REVENUE = P*Q Price per unit of product and Q no. of units sold

Break-even analysis • Identify fixed and variable costs • Explore possibilities of changing fixed into variable costs • And vice-versa • Can be expressed in terms of – Capacity utilisation – Sales revenue

Application of BEA • • Helps in taking investment decisions Profit optimization planning Helps in pricing decision Can be modified to calculate profitability at various levels of capacity utilisation / sales

Funding opportunities for start up in India

Institutions providing funds to start ups Department of science and Industrial Research Ministry of MSMEs Department of science and technology SIDBI VENTURE SME Growth Fund Department of Biotechnology National Research development corporation Department of Information Technology Risk capital and Technology Finance Corporation ltd. Now called as IFCI Venture • Angel capital to start ups • Venture capital funding in India • •

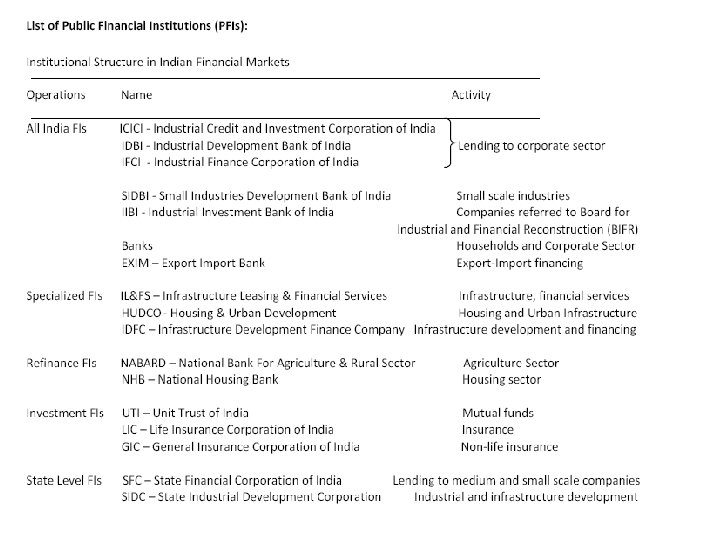

Banks and financial Institutions Funding Ventures

• Small")

Institutions assisting Entrepreneurs Small Scale Unit • National small Industries corporation (NSIC) • Small Industries Development Orgzn. (SIDO) • Khadi Village Industries Commission(KVIC) • Handloom Board • Silk Board

Medium and Large scale unit • Industrial finance corporation")

Institutions assisting Entrepreneurs( cont. ) Medium and Large scale unit • Industrial finance corporation of India(IFCI) • State industrial development corporation (SIDC) • ICICI bank, IDBI bank, SIDBI.

Services of SIDO • • • Technical resource centre Consultancy Marketing support Vendor development – Buyer seller meet Quality/ Technical up gradation Training facility – EDP, MDP, Skill development

Schemes of NSIC • • Bank credit facilitation Export credit insurance Performance & credit rating Raw materials assistance Bills discounting Government purchase Exhibitions

• Evolving effective training strategies")

National Institute for Entrepreneurship and Small Business Development (NIESBUD) • Evolving effective training strategies and methodology • Standardizing model syllabi for training various target groups • Developing training aids, manuals and tools • Facilitating and supporting Central / State/ Other agencies in organizing entrepreneurship development programmes • Conducting training programmes for promoters, trainers and entrepreneurs • Undertaking research and exchange experiences globally in development and growth of entrepreneurship.

ecfcf6a4601cbef6f8143ddce353bec6.ppt