7a097df6172716603b452ef2914ccdbc.ppt

- Количество слайдов: 64

Microeconomics Unit 2

Microeconomics Unit 2

interdependence mutually reliant on each other factor market exchanges that businesses must make in order to produce things product market Producers need consumers to buy and consumers need producers to provide goods and services market in which consumers purchase goods & services produced by business Where businesses shop or spend money on the 4 factors of production Where consumers shop medium of exchange anything accepted as payment for goods and services Money standard of value gives a value or price What we expect to pay for something

interdependence mutually reliant on each other factor market exchanges that businesses must make in order to produce things product market Producers need consumers to buy and consumers need producers to provide goods and services market in which consumers purchase goods & services produced by business Where businesses shop or spend money on the 4 factors of production Where consumers shop medium of exchange anything accepted as payment for goods and services Money standard of value gives a value or price What we expect to pay for something

Unit 2 - Microeconomic Concepts Interdependence I. __________and the Flow of Money The Circular Flow of Economic Activity - 3 major actors Households 1. __________HH) Businesses 2. ________(Firms) 3. __________(G) Government -2 major markets Product 1. ______Market Factor 2. ____(Resource) Market

Unit 2 - Microeconomic Concepts Interdependence I. __________and the Flow of Money The Circular Flow of Economic Activity - 3 major actors Households 1. __________HH) Businesses 2. ________(Firms) 3. __________(G) Government -2 major markets Product 1. ______Market Factor 2. ____(Resource) Market

What is Money? a. coins and bills b. a good c. a service d. anything used for exchange

What is Money? a. coins and bills b. a good c. a service d. anything used for exchange

Money has 3 functions - they are: Medium of Exchange 1. ___________-- assessed value then exchanged for goods Standard of value 2. ________-- gives a value or price Store of value 3. _______-- can be used at a later date

Money has 3 functions - they are: Medium of Exchange 1. ___________-- assessed value then exchanged for goods Standard of value 2. ________-- gives a value or price Store of value 3. _______-- can be used at a later date

") When you buy a hamburger for lunch, you are using money as a a) standard of deferred payment b) standard of value c) medium of exchange d) store of value

When you buy a hamburger for lunch, you are using money as a a) standard of deferred payment b) standard of value c) medium of exchange d) store of value

A $20, 000 price tag on a new car is an example of money as a) standard of deferred payment b) standard of value c) medium of exchange d) store of value

A $20, 000 price tag on a new car is an example of money as a) standard of deferred payment b) standard of value c) medium of exchange d) store of value

l How is money different than barter? People _______they owned for ______ trade goods they want ____. l. Which is better - money or barter? Money, wasn't always easy to find person with good or service willing to trade

l How is money different than barter? People _______they owned for ______ trade goods they want ____. l. Which is better - money or barter? Money, wasn't always easy to find person with good or service willing to trade

Penny Sacagawea Nickel Jefferson Dime Quarter 1/2 Dollar Kennedy Roosevelt Lincoln Washington

Penny Sacagawea Nickel Jefferson Dime Quarter 1/2 Dollar Kennedy Roosevelt Lincoln Washington

One Two Five Ten Twenty Fifty Hundred Franklin Lincoln Jefferson Grant Hamilton Washington Jackson

One Two Five Ten Twenty Fifty Hundred Franklin Lincoln Jefferson Grant Hamilton Washington Jackson

supply quantity of a product that consumers are willing and able to buy at a certain price amount of a product that would be offered for sale law of demand states that the quantity demanded of a good varies inversely with its price law of supply higher the price a company can charge, the more it is willing supply price monetary value of a product as established by supply and demand equilibrium where consumers and producers agree on a price for an item demand Things we want and are able to buy How much a producer/business wants to sell Price increases, demand decreases Price decreases, demand increases Price increases, supply increases Price decreases, supply decreases What a product cost Producers charge as high a price as consumers will pay.

supply quantity of a product that consumers are willing and able to buy at a certain price amount of a product that would be offered for sale law of demand states that the quantity demanded of a good varies inversely with its price law of supply higher the price a company can charge, the more it is willing supply price monetary value of a product as established by supply and demand equilibrium where consumers and producers agree on a price for an item demand Things we want and are able to buy How much a producer/business wants to sell Price increases, demand decreases Price decreases, demand increases Price increases, supply increases Price decreases, supply decreases What a product cost Producers charge as high a price as consumers will pay.

Chapter 4: Demand What is Demand: Willingness to buy a product at a certain price. Characteristics of Demand Desire to buy Willingness to buy Ability to buy **Watch Demand video**

Chapter 4: Demand What is Demand: Willingness to buy a product at a certain price. Characteristics of Demand Desire to buy Willingness to buy Ability to buy **Watch Demand video**

that you") Creating Demand Schedules 1. Think of a few products (goods or services) that you spend your money on. 2. Write down one product that you purchase frequently and one that you don’t purchase very often in the charts below. Product You Purchase Frequently: ____ Price Quantity willing to buy at price Product You Don’t Buy Often: ______ Price Quantity willing to buy at price Which product has more utility? ? Why? ? Gives you happiness!

Creating Demand Schedules 1. Think of a few products (goods or services) that you spend your money on. 2. Write down one product that you purchase frequently and one that you don’t purchase very often in the charts below. Product You Purchase Frequently: ____ Price Quantity willing to buy at price Product You Don’t Buy Often: ______ Price Quantity willing to buy at price Which product has more utility? ? Why? ? Gives you happiness!

Creating Demand Curves 1. Plot your Demand Schedule onto the graphs below. 0 1 2 3 4 5 6 The Demand Schedule and Demand Curve prove the Law of Demand. P P Q Q Creates an Inverse Relationship. (reverse order or direction). Law of Demand is from an economic model based on rational behavior.

Creating Demand Curves 1. Plot your Demand Schedule onto the graphs below. 0 1 2 3 4 5 6 The Demand Schedule and Demand Curve prove the Law of Demand. P P Q Q Creates an Inverse Relationship. (reverse order or direction). Law of Demand is from an economic model based on rational behavior.

Which of the following is true concerning the Law of Demand? 1. states that as price goes down, quantity demanded goes up 2. states an inverse relationship between price and quantity 3. states that as price goes up, quantity demanded goes up 4. states that as price goes up, quantity demand goes down a. 1 and 2 b. 1, 2 and 3 c. 1, 2 and 4 d. 1, 2, 3, 4

Which of the following is true concerning the Law of Demand? 1. states that as price goes down, quantity demanded goes up 2. states an inverse relationship between price and quantity 3. states that as price goes up, quantity demanded goes up 4. states that as price goes up, quantity demand goes down a. 1 and 2 b. 1, 2 and 3 c. 1, 2 and 4 d. 1, 2, 3, 4

A demand schedule a. relates price to quantity supplied b. is a demand curve when graphed out c. cannot change d. shows a direct relationship between price and quantity

A demand schedule a. relates price to quantity supplied b. is a demand curve when graphed out c. cannot change d. shows a direct relationship between price and quantity

1. According to the graph above, at what price will Tom’s quantity demanded of Tootsie Roll pops be 4 pops? Price Per tootsie Role Pop $1. 25 Demand $1. 00 $. 75 $. 50 Always slopes downward Quantity Demand $. 25 0 1 2 3 4 Tootsie Roll Pops per day 5 2. The price of pops has just increased by $. 25 from an earlier, low price. Based on Tom’s demand curve, how many less pops does he now demand? 1 The entire line on the graph represents demand. The points on the line represent the change in quantity demanded. The change along the demand curve is caused by prices. A change (shift) in Demand is caused by a Detriment in Demand. . .

1. According to the graph above, at what price will Tom’s quantity demanded of Tootsie Roll pops be 4 pops? Price Per tootsie Role Pop $1. 25 Demand $1. 00 $. 75 $. 50 Always slopes downward Quantity Demand $. 25 0 1 2 3 4 Tootsie Roll Pops per day 5 2. The price of pops has just increased by $. 25 from an earlier, low price. Based on Tom’s demand curve, how many less pops does he now demand? 1 The entire line on the graph represents demand. The points on the line represent the change in quantity demanded. The change along the demand curve is caused by prices. A change (shift) in Demand is caused by a Detriment in Demand. . .

price elasticity measure of responsiveness to a change in price If there is a high need for a product, then price does not matter. A luxury or want – the higher the price, the less likely will buy. substitute goods Products that are alike. can be used in place of another the use of one complimentary increases the use goods of another Products that “go together”. . . like a couple!

price elasticity measure of responsiveness to a change in price If there is a high need for a product, then price does not matter. A luxury or want – the higher the price, the less likely will buy. substitute goods Products that are alike. can be used in place of another the use of one complimentary increases the use goods of another Products that “go together”. . . like a couple!

that someone gets from the use") Utility the amount of usefulness or satisfaction (happiness) that someone gets from the use of a product (good or service). Marginal Utility – the extra usefulness (or happiness) a person gets from acquiring or using one more unit of a product. Diminishing Marginal Utility - the extra satisfaction we get from using additional quantities of the products begins to diminish (disappear). Real World Example: For instance, if I haven’t had any pizza in a long time, I’ll get a huge amount of utility from eating a slice. The melted cheese, the basil and garlic in the sauce, and the warmth in my mouth all make me very, very happy (utility). But the thrill of pizza is dampened by eating that first slice so that if I eat a second slice, it’s still very good, but not a good as the first. And if I have a third slice, it’s not as good as the second. And if I keep eating and eating, the additional slices of pizza will soon get sickening and produce pain instead of pleasure if I eat them. This phenomenon isn’t limited to pizza; it applies to nearly everything. Unless you’re addicted to something, you get tired of it as you have more of it, and each additional unit brings you less happiness than the previous unit. (excerpt from Economics for Dummies).

Utility the amount of usefulness or satisfaction (happiness) that someone gets from the use of a product (good or service). Marginal Utility – the extra usefulness (or happiness) a person gets from acquiring or using one more unit of a product. Diminishing Marginal Utility - the extra satisfaction we get from using additional quantities of the products begins to diminish (disappear). Real World Example: For instance, if I haven’t had any pizza in a long time, I’ll get a huge amount of utility from eating a slice. The melted cheese, the basil and garlic in the sauce, and the warmth in my mouth all make me very, very happy (utility). But the thrill of pizza is dampened by eating that first slice so that if I eat a second slice, it’s still very good, but not a good as the first. And if I have a third slice, it’s not as good as the second. And if I keep eating and eating, the additional slices of pizza will soon get sickening and produce pain instead of pleasure if I eat them. This phenomenon isn’t limited to pizza; it applies to nearly everything. Unless you’re addicted to something, you get tired of it as you have more of it, and each additional unit brings you less happiness than the previous unit. (excerpt from Economics for Dummies).

Factors Affecting Quantity Demand Decrease in Demand Increase in Demand 1. The Income Effect When prices drop, people have more money to spend on more stuff; therefore, quantity demanded increases. 2. The Substitution Effect When prices increase, consumers find a replacement product. Example: Blow Pops price increase might be an incentive for folks to buy Tootsie Roll pops instead.

Factors Affecting Quantity Demand Decrease in Demand Increase in Demand 1. The Income Effect When prices drop, people have more money to spend on more stuff; therefore, quantity demanded increases. 2. The Substitution Effect When prices increase, consumers find a replacement product. Example: Blow Pops price increase might be an incentive for folks to buy Tootsie Roll pops instead.

Factors Affecting Change in Demand People are now willing to buy _________of different amounts same price the product at the _____. This causes a shift in the demand curve to the right or left. change When there is a __________, the entire in demand shifts demand curve ______to the right ______or the ______. left Right movement shows an increase ______in demand. Left movement shows a ______in demand. decrease

Factors Affecting Change in Demand People are now willing to buy _________of different amounts same price the product at the _____. This causes a shift in the demand curve to the right or left. change When there is a __________, the entire in demand shifts demand curve ______to the right ______or the ______. left Right movement shows an increase ______in demand. Left movement shows a ______in demand. decrease

Factors Affecting Change in Demand People are now willing to buy different amounts of the product at the same prices. This causes a shift in the demand curve to the right or left. 1. Consumer Income a. When consumer income increases ____, consumers can afford to buy more goods and services (even at the same prices). Where does the line move to when consumer income increases? b. When consumer income decreases ____, it causes consumers less to buy ____. Where does the line move to when consumer income decreases?

Factors Affecting Change in Demand People are now willing to buy different amounts of the product at the same prices. This causes a shift in the demand curve to the right or left. 1. Consumer Income a. When consumer income increases ____, consumers can afford to buy more goods and services (even at the same prices). Where does the line move to when consumer income increases? b. When consumer income decreases ____, it causes consumers less to buy ____. Where does the line move to when consumer income decreases?

2. Consumer Tastes What affects consumers tastes: advertising, news reports, trends, new products, and seasons. a. Consumer tastes increase when a product is successfully advertised. Where does the line move to when consumer tastes increases? b. Consumers get tired of a product, they will buy less at each and every price. Where does the line move to when consumer tastes decreases?

2. Consumer Tastes What affects consumers tastes: advertising, news reports, trends, new products, and seasons. a. Consumer tastes increase when a product is successfully advertised. Where does the line move to when consumer tastes increases? b. Consumers get tired of a product, they will buy less at each and every price. Where does the line move to when consumer tastes decreases?

3. Substitutes Can be used in place of other products. When prices rise, substitutes are purchased. Price of margarine: Demand for butter:

3. Substitutes Can be used in place of other products. When prices rise, substitutes are purchased. Price of margarine: Demand for butter:

4. Complements a. Use of one product increases the demand of another product. Draw the shifts on the graphs. b. Increases in the price of one product may decrease the _____for its complement.

4. Complements a. Use of one product increases the demand of another product. Draw the shifts on the graphs. b. Increases in the price of one product may decrease the _____for its complement.

5. Change in Expectations The way people think about the future. a. A technological breakthrough where consumers buy less now would make the demand curve shift to the left. Draw the shifts on the graphs. b. A bad year for crops so that consumers might stock up on certain foods before they become scarce would make the demand curve shift right.

5. Change in Expectations The way people think about the future. a. A technological breakthrough where consumers buy less now would make the demand curve shift to the left. Draw the shifts on the graphs. b. A bad year for crops so that consumers might stock up on certain foods before they become scarce would make the demand curve shift right.

5. Change in Population a. More consumers, more ____. b. Less consumers, less demand. Draw the shifts on the graphs.

5. Change in Population a. More consumers, more ____. b. Less consumers, less demand. Draw the shifts on the graphs.

The shift from the red demand curve to the blue curve represents a a. increase in demand b. decrease in demand c. change is price d. change in quantity P Q

The shift from the red demand curve to the blue curve represents a a. increase in demand b. decrease in demand c. change is price d. change in quantity P Q

Which of the following shows an increase in price? A B P P Q Q D C P P Q Q

Which of the following shows an increase in price? A B P P Q Q D C P P Q Q

If the government issues a decrease in taxes of 10%, then the demand curve for goods would A B P P Q Q D C P P Q Q

If the government issues a decrease in taxes of 10%, then the demand curve for goods would A B P P Q Q D C P P Q Q

Silly Bands cause cancer, the fad ends. The demand curve. . . A B C D

Silly Bands cause cancer, the fad ends. The demand curve. . . A B C D

If the price of good A rises and the demand for good B rises, then A and B are a. substitutes b. complements c. not related d. scarce

If the price of good A rises and the demand for good B rises, then A and B are a. substitutes b. complements c. not related d. scarce

Business is going well and Dad expects a raise. What will happen to your family's demand for eating out? A C B D

Business is going well and Dad expects a raise. What will happen to your family's demand for eating out? A C B D

New tight immigration laws make it hard for others to come to the USA? What happens to the demand for housing? A C B D

New tight immigration laws make it hard for others to come to the USA? What happens to the demand for housing? A C B D

Which of the following will not occur if the price of hamburger meat falls, other things being constant? a. the demand for hamburger buns will increase b. people will substitute hamburgers for hotdogs c. the demand for hotdogs will rise d. the quantity of hamburgers demanded will increase

Which of the following will not occur if the price of hamburger meat falls, other things being constant? a. the demand for hamburger buns will increase b. people will substitute hamburgers for hotdogs c. the demand for hotdogs will rise d. the quantity of hamburgers demanded will increase

Demand Elasticity price The extent to which a change in _____ causes a change in ________. quantity demanded *For most goods consumers _____ care about changes in price. *Tells how ____consumers are sensitive price to changes in ______. Q How much consumers change __ in P relation to changes in __?

Demand Elasticity price The extent to which a change in _____ causes a change in ________. quantity demanded *For most goods consumers _____ care about changes in price. *Tells how ____consumers are sensitive price to changes in ______. Q How much consumers change __ in P relation to changes in __?

Elastic Demand large price A change ______in causes a ____ change in _________. quantity demanded P Examples of goods that have elastic demand Candy ELASTIC Q

Elastic Demand large price A change ______in causes a ____ change in _________. quantity demanded P Examples of goods that have elastic demand Candy ELASTIC Q

Inelastic Demand small price A change ______in causes a ____ change in _________. quantity demanded P Examples of goods that have inelastic demand Medicine Q INELASTIC

Inelastic Demand small price A change ______in causes a ____ change in _________. quantity demanded P Examples of goods that have inelastic demand Medicine Q INELASTIC

P Q Demand Schedule Inverse Relationship Demand Curve P Quantity") LAW OF DEMAND (review) P Q Demand Schedule Inverse Relationship Demand Curve P Quantity Demanded Price $30 0 25 0 20 1 15 3 10 5 5 8 Q

LAW OF DEMAND (review) P Q Demand Schedule Inverse Relationship Demand Curve P Quantity Demanded Price $30 0 25 0 20 1 15 3 10 5 5 8 Q

Law of Supply Amount of a product that would be offered for sale at each possible price in the market. Law of Supply has a direct relationship: P P Q Q

Law of Supply Amount of a product that would be offered for sale at each possible price in the market. Law of Supply has a direct relationship: P P Q Q

Supply Schedule Table showing quantities supplied at prices. Product you offer: Lawn mowing Price $30. 00 $20. 00 $10. 00 $5. 00 $2. 00 Quantity willing to sell

Supply Schedule Table showing quantities supplied at prices. Product you offer: Lawn mowing Price $30. 00 $20. 00 $10. 00 $5. 00 $2. 00 Quantity willing to sell

Supply Curve P Supply & Quantity Supplied Q

Supply Curve P Supply & Quantity Supplied Q

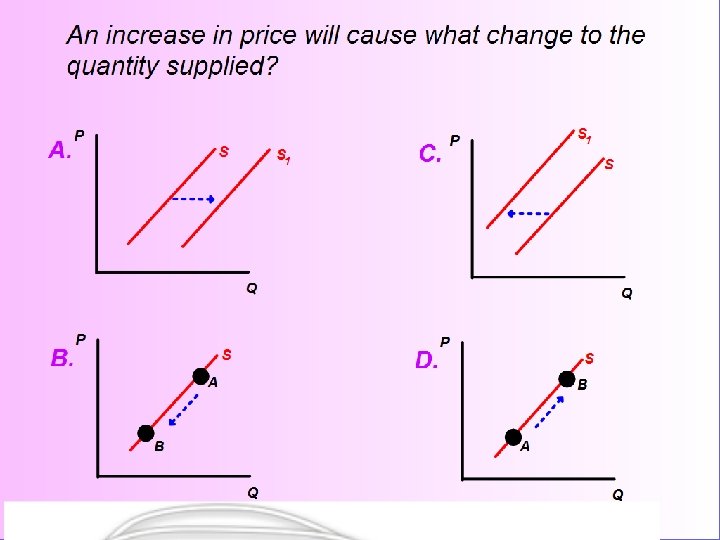

Factors Affecting Quantity Supplied Remember: The Quantity Supplied is the amount that producers bring to market at any given price. A change in quantity supplied is the change in amount offered for sale in response to a change in price. A change in quantity supply shows a movement along the supply curve. This movement can be a decrease or an increase. Example: 4 CDs are supplied when the price is $15. If the price increases to $20, then 6 CDs are supplied.

Factors Affecting Quantity Supplied Remember: The Quantity Supplied is the amount that producers bring to market at any given price. A change in quantity supplied is the change in amount offered for sale in response to a change in price. A change in quantity supply shows a movement along the supply curve. This movement can be a decrease or an increase. Example: 4 CDs are supplied when the price is $15. If the price increases to $20, then 6 CDs are supplied.

Factors Affecting Change in Supply Increase in Supply Decrease in Supply

Factors Affecting Change in Supply Increase in Supply Decrease in Supply

1. Resources A change in the cost of inputs can cause a change in supply. a. Supply might increase because of a decrease in the cost of inputs, such as labor or packaging. If the price of inputs drops, then producers are willing and able to make more of a product_. Where does the line move to when the price of inputs decreases? b. If the price of inputs increases, then producers are not as willing or able to produce more because it costs more. Where does the line move to when price of inputs increases?

1. Resources A change in the cost of inputs can cause a change in supply. a. Supply might increase because of a decrease in the cost of inputs, such as labor or packaging. If the price of inputs drops, then producers are willing and able to make more of a product_. Where does the line move to when the price of inputs decreases? b. If the price of inputs increases, then producers are not as willing or able to produce more because it costs more. Where does the line move to when price of inputs increases?

2. Productivity What affects employees to work hard? a. When management motivates its workers, or if workers decide to work more efficiently, productivity should increase. ____________. Where does the line move to when workers work harder? b. If workers are unmotivated, untrained, or unhappy, productivity could decrease _____. Where does the line move to when workers are unhappy?

2. Productivity What affects employees to work hard? a. When management motivates its workers, or if workers decide to work more efficiently, productivity should increase. ____________. Where does the line move to when workers work harder? b. If workers are unmotivated, untrained, or unhappy, productivity could decrease _____. Where does the line move to when workers are unhappy?

3. Technology Is technology a good thing or a bad thing? a. New technology tends to increase supply because producers may be able to _________. increase productivity Where does the line move to when technology works great? b. However, sometimes new technology breaks down which stops can stop production until it is repaired. Where does the line move to when technology doesn’t work?

3. Technology Is technology a good thing or a bad thing? a. New technology tends to increase supply because producers may be able to _________. increase productivity Where does the line move to when technology works great? b. However, sometimes new technology breaks down which stops can stop production until it is repaired. Where does the line move to when technology doesn’t work?

4. Taxes and Subsidies Taxes Subsidies ______are payments to the government. _____are payments from the government to firms to either encourage or protect certain economic activities. a. Taxes – if taxes go down, then resources costs ______so the firm less more can produce _______. Subsidies – if government pays out a subsidy to a firm, they have more money to spend on inputs. Where does the line move to when taxes are low and subsidies are given? b. Taxes – if a producer’s inventory is taxed or if fees are paid to receive a license to produce, then the cost of production goes up. Subsidies – if repealed (taken away), then production decreases. Where does the line move to when taxes are high or no subsidy?

4. Taxes and Subsidies Taxes Subsidies ______are payments to the government. _____are payments from the government to firms to either encourage or protect certain economic activities. a. Taxes – if taxes go down, then resources costs ______so the firm less more can produce _______. Subsidies – if government pays out a subsidy to a firm, they have more money to spend on inputs. Where does the line move to when taxes are low and subsidies are given? b. Taxes – if a producer’s inventory is taxed or if fees are paid to receive a license to produce, then the cost of production goes up. Subsidies – if repealed (taken away), then production decreases. Where does the line move to when taxes are high or no subsidy?

5. Expectations about the future price of a product can also affect the supply curve. a. If producers think the price of their product will go up, they may wait to until then to supply more. Where does the line move NOW when the price of i. Phones is expected to go up in 3 months? b. If producers think the price of their product will go down, they will supply as much as possible now while the price is still high. Where does the line move NOW when the price of i. Phones is expected to go down in 3 months?

5. Expectations about the future price of a product can also affect the supply curve. a. If producers think the price of their product will go up, they may wait to until then to supply more. Where does the line move NOW when the price of i. Phones is expected to go up in 3 months? b. If producers think the price of their product will go down, they will supply as much as possible now while the price is still high. Where does the line move NOW when the price of i. Phones is expected to go down in 3 months?

6. Number of Sellers a. If the number of producers increase, then supply increases. Where does the line move if more car factories open? a. If the number of producers decreases, then supply decreases. Where does the line move when several car factories close down?

6. Number of Sellers a. If the number of producers increase, then supply increases. Where does the line move if more car factories open? a. If the number of producers decreases, then supply decreases. Where does the line move when several car factories close down?

A Pix is worth a 1, 000 words activity

A Pix is worth a 1, 000 words activity

Supply and Demand Together

Supply and Demand Together

Law of Demand Law of Supply Cut and Paste Activity

Law of Demand Law of Supply Cut and Paste Activity

a price floor; lowest legal price for labor price floor lowest legal price that can be paid for a good or service price ceiling maximum legal price that can be charged minimum wage shortage quantity demand is greater than quantity supplied The lowest an employer is allowed to pay you! Government states price can only go so low Government states price is allowed to only go so high Not enough product to go around surplus quantity supplied is greater than the quantity demanded Too much product; leftovers!

a price floor; lowest legal price for labor price floor lowest legal price that can be paid for a good or service price ceiling maximum legal price that can be charged minimum wage shortage quantity demand is greater than quantity supplied The lowest an employer is allowed to pay you! Government states price can only go so low Government states price is allowed to only go so high Not enough product to go around surplus quantity supplied is greater than the quantity demanded Too much product; leftovers!

X marks the spot! The point where the supply and demand curves cross determines ____________. market equilibrium Market equilibrium indicates how much a product ______ costs much of it gets sold and how _________. Because quantity demanded equals ______quantity supplied, both producers and consumers are happy.

X marks the spot! The point where the supply and demand curves cross determines ____________. market equilibrium Market equilibrium indicates how much a product ______ costs much of it gets sold and how _________. Because quantity demanded equals ______quantity supplied, both producers and consumers are happy.

Surplus The situation that results when the supplied quantity _____of a product exceeds demanded _____the quantity _____. Generally happens because the price of the product is ____ above equilibrium the market ________price. Shortage The situation that results when the demanded quantity _____for a product exceeds supplied ____the quantity _____. Generally happens because the price of the product is _______the below equilibrium market _______price.

Surplus The situation that results when the supplied quantity _____of a product exceeds demanded _____the quantity _____. Generally happens because the price of the product is ____ above equilibrium the market ________price. Shortage The situation that results when the demanded quantity _____for a product exceeds supplied ____the quantity _____. Generally happens because the price of the product is _______the below equilibrium market _______price.

Surplus *______causes price to drop _____ Shortage increase *____causes price to _______

Surplus *______causes price to drop _____ Shortage increase *____causes price to _______

price ceiling A ________ is a legally maximum established _____price. Govt’s _____enact price _______when they fear that the ceilings price might be higher than they desire it to be. When a price ceiling lower _______is _______than the equilibrium price, it can cause a _______. shortage Ceiling – shortage because producers can not set a high price so more people are able to buy. Example: rent-control laws that limit the increase in rents from year to year.

price ceiling A ________ is a legally maximum established _____price. Govt’s _____enact price _______when they fear that the ceilings price might be higher than they desire it to be. When a price ceiling lower _______is _______than the equilibrium price, it can cause a _______. shortage Ceiling – shortage because producers can not set a high price so more people are able to buy. Example: rent-control laws that limit the increase in rents from year to year.

A _______is a price floor legally established Govt’s minimum _____price. _____ enact price _______when floors they fear that the price might be lower than they desire it floor to be. When a price ______ is ____than the higher equilibrium price, it can cause surplus a ______. Floor – surplus because producers can set a high price so more people are not able to buy. Examples of price floors include farm products and the minimum wage.

A _______is a price floor legally established Govt’s minimum _____price. _____ enact price _______when floors they fear that the price might be lower than they desire it floor to be. When a price ______ is ____than the higher equilibrium price, it can cause surplus a ______. Floor – surplus because producers can set a high price so more people are not able to buy. Examples of price floors include farm products and the minimum wage.

competition pure competition monopolistic competition oligopoly monopoly a struggle amongst businesses market structure where a large number of buyers and sellers who exchange identical goods market structure having all conditions of pure competition except for identical products; product differentiation market structure in which a few large sellers dominate the industry market structure in which one company has control over production & prices

competition pure competition monopolistic competition oligopoly monopoly a struggle amongst businesses market structure where a large number of buyers and sellers who exchange identical goods market structure having all conditions of pure competition except for identical products; product differentiation market structure in which a few large sellers dominate the industry market structure in which one company has control over production & prices

Competition creates lower ____________, prices for consumers profits for producers better less _________, and _____ products. Pure Competition Large number of sellers Same quality products No major barriers Free exchange of price Oligopolies Only a few firms (2 -12) High barriers to entry Must be aware of other prices Ex: car industry, cereal, soft drinks, tire industry Monopolistic Competition Only real difference is price Similar products, but not identical Ex: shoes, fast food, gas stations Monopolies One firm Little to no competition Higher prices Ex: public utilities

Competition creates lower ____________, prices for consumers profits for producers better less _________, and _____ products. Pure Competition Large number of sellers Same quality products No major barriers Free exchange of price Oligopolies Only a few firms (2 -12) High barriers to entry Must be aware of other prices Ex: car industry, cereal, soft drinks, tire industry Monopolistic Competition Only real difference is price Similar products, but not identical Ex: shoes, fast food, gas stations Monopolies One firm Little to no competition Higher prices Ex: public utilities

Oligopolies Monopolies Pure Competition Monopolistic Comp

Oligopolies Monopolies Pure Competition Monopolistic Comp