37a9db9c1e021e38e5b8a78f1c2b50e6.ppt

- Количество слайдов: 47

Market forces I: Price Impact J. Doyne Farmer Santa Fe Institute La Sapienza, 8 marzo Research supported by Barclays Bank

Market forces I: Price Impact J. Doyne Farmer Santa Fe Institute La Sapienza, 8 marzo Research supported by Barclays Bank

Market forces • Supply and demand are in a loose sense like forces in physics. • What determines supply and demand curves? • Are they the best approach? – Market dynamics – Observability problems

Market forces • Supply and demand are in a loose sense like forces in physics. • What determines supply and demand curves? • Are they the best approach? – Market dynamics – Observability problems

Standard approach to determining supply and demand • Assume agents selfishly maximize utility • Make an assumption about optimization algorithm agents use: – Standard: Perfect rationality – “Behavioral”: One rational, others noise • Make an assumption about markets – Market clearing – Price taking • Simplifications: (no production, no inter-temporal reasoning, … • Economy is at a Nash equilibrium • Research since 1980: Modify assumptions

Standard approach to determining supply and demand • Assume agents selfishly maximize utility • Make an assumption about optimization algorithm agents use: – Standard: Perfect rationality – “Behavioral”: One rational, others noise • Make an assumption about markets – Market clearing – Price taking • Simplifications: (no production, no inter-temporal reasoning, … • Economy is at a Nash equilibrium • Research since 1980: Modify assumptions

What drives changes in prices? • Standard view: expectations about future earnings driven by new information – new information alters expected earnings and changes fundamental value – prices quickly adjust to new fundamental value – prices are unpredictable because new information is by definition random

What drives changes in prices? • Standard view: expectations about future earnings driven by new information – new information alters expected earnings and changes fundamental value – prices quickly adjust to new fundamental value – prices are unpredictable because new information is by definition random

Rationality?

Rationality?

Elliot waves

Elliot waves

Fibonnaci predicts social trends!

Fibonnaci predicts social trends!

Overfitting

Overfitting

•") Problems with standard view • Far too much trading (> 50 x GDP) • Volatility is not random – size of price changes is correlated in time • Many price changes not information driven • Prices deviate from fundamental values • Prices have exploitable patterns – weak, difficult to find, but not zero

Problems with standard view • Far too much trading (> 50 x GDP) • Volatility is not random – size of price changes is correlated in time • Many price changes not information driven • Prices deviate from fundamental values • Prices have exploitable patterns – weak, difficult to find, but not zero

Volatility

Volatility

•") Problems with standard view • Far too much trading (> 50 x GDP) • Volatility is not random – size of price changes is correlated in time • Many price changes not information driven • Prices deviate from fundamental values • Prices have exploitable patterns – weak, difficult to find, but not zero

Problems with standard view • Far too much trading (> 50 x GDP) • Volatility is not random – size of price changes is correlated in time • Many price changes not information driven • Prices deviate from fundamental values • Prices have exploitable patterns – weak, difficult to find, but not zero

•") Problems with standard view • Far too much trading (> 50 x GDP) • Volatility is not random – size of price changes is correlated in time • Many price changes not information driven • Prices deviate from fundamental values • Prices have exploitable patterns – weak, difficult to find, but not zero

Problems with standard view • Far too much trading (> 50 x GDP) • Volatility is not random – size of price changes is correlated in time • Many price changes not information driven • Prices deviate from fundamental values • Prices have exploitable patterns – weak, difficult to find, but not zero

to fundamental") Prices do not match fundamental values Comparison of pseudo S&P index (solid) to fundamental value estimate based on dividends (dashed)

Prices do not match fundamental values Comparison of pseudo S&P index (solid) to fundamental value estimate based on dividends (dashed)

•") Problems with standard view • Far too much trading (> 50 x GDP) • Volatility is not random – size of price changes is correlated in time • Many price changes not information driven • Prices deviate from fundamental values • Prices have exploitable patterns – weak, difficult to find, but not zero

Problems with standard view • Far too much trading (> 50 x GDP) • Volatility is not random – size of price changes is correlated in time • Many price changes not information driven • Prices deviate from fundamental values • Prices have exploitable patterns – weak, difficult to find, but not zero

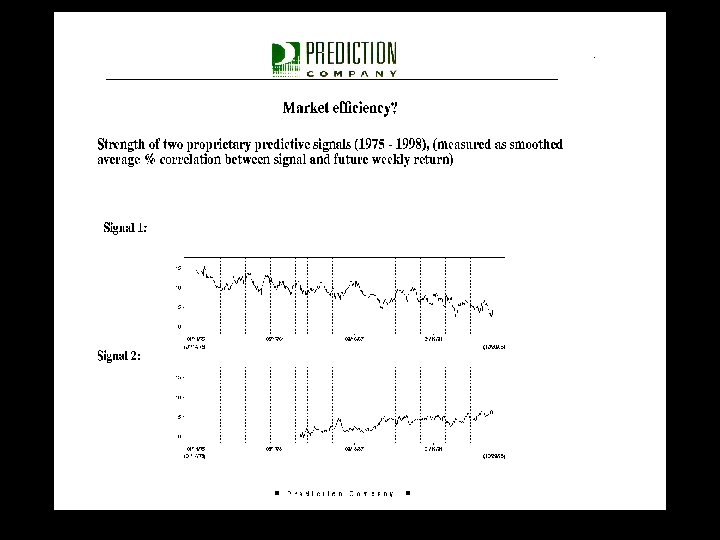

• Does fully automated proprietary trading") Prediction Company (cofounded in 1991 with Norman Packard) • Does fully automated proprietary trading in international stock markets under profit sharing relationship with United Bank of Switzerland (Warburg Dillon Read) • “Cerebellar” approach to market forecasting – – empirically search for patterns in historical data keys are feature extraction, central limit theorem little understanding of origin of patterns relies on abundant past data, stationary conditions • 50 employees.

Prediction Company (cofounded in 1991 with Norman Packard) • Does fully automated proprietary trading in international stock markets under profit sharing relationship with United Bank of Switzerland (Warburg Dillon Read) • “Cerebellar” approach to market forecasting – – empirically search for patterns in historical data keys are feature extraction, central limit theorem little understanding of origin of patterns relies on abundant past data, stationary conditions • 50 employees.

Profits? • Finding a persistent pattern doesn’t mean you can make an infinite amount of money. – (reason is market impact) – depends on timescale • How much you can make is sensitively dependent on market impact

Profits? • Finding a persistent pattern doesn’t mean you can make an infinite amount of money. – (reason is market impact) – depends on timescale • How much you can make is sensitively dependent on market impact

• Response of price to receipt of an") Price Impact (also called market impact) • Response of price to receipt of an order • Related to derivative of aggregate demand function = demand - supply. • With a few caveats, has the important advantage of being directly measurable. – No information about price level, only price change

Price Impact (also called market impact) • Response of price to receipt of an order • Related to derivative of aggregate demand function = demand - supply. • With a few caveats, has the important advantage of being directly measurable. – No information about price level, only price change

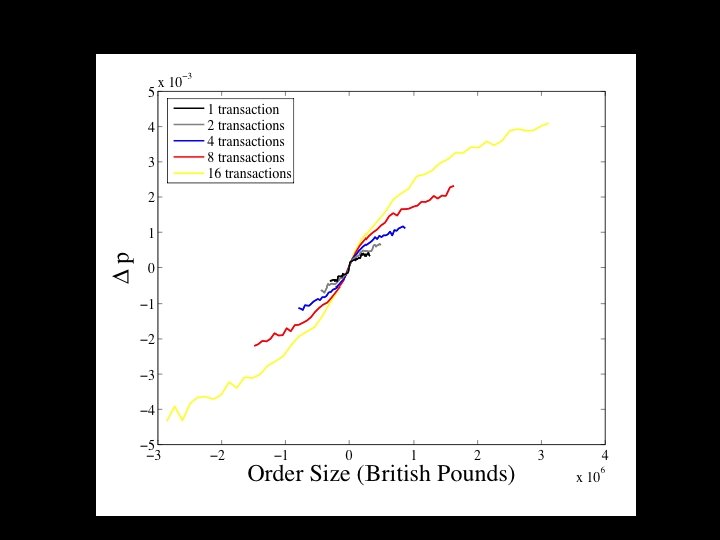

Price impact vs. order size for different market capitalizations With Fabrizio Lillo and Rosario Mantegna

Price impact vs. order size for different market capitalizations With Fabrizio Lillo and Rosario Mantegna

Data collapse • Use market capitalization C as liquidity proxy • Find empirically to minimize variance

Data collapse • Use market capitalization C as liquidity proxy • Find empirically to minimize variance

Master price impact curve

Master price impact curve

Zero intelligence model of price formation • Assume agents place orders to buy or sell, make cancellations, “at random” – make everything a Poisson process – make distributions and rates uniform – equal for buying and selling. • What are properties of resulting prices? – Dimensional analysis (price, time, shares) – Scaling laws for spread and volatility in terms of parameters of order flow

Zero intelligence model of price formation • Assume agents place orders to buy or sell, make cancellations, “at random” – make everything a Poisson process – make distributions and rates uniform – equal for buying and selling. • What are properties of resulting prices? – Dimensional analysis (price, time, shares) – Scaling laws for spread and volatility in terms of parameters of order flow

Giulia Iori Continuous double auction model collaborators Eric Smith Giulia Iori Marcus Daniels Laszlo Gillemot Supriya Krishnamurthy

Giulia Iori Continuous double auction model collaborators Eric Smith Giulia Iori Marcus Daniels Laszlo Gillemot Supriya Krishnamurthy

Continuous double auction Continuous: Market operates asynchronously Double: Price adjustment in orders both to buy and to sell Execution priority: • Lower priced sell orders or higher priced buy orders have priority • First order placed has priority when multiple orders have same price. VOLUME LIMIT ORDERS SPREAD (BEST) BID (BEST) ASK BUY SELL VOLUME PRIORITY price ($)

Continuous double auction Continuous: Market operates asynchronously Double: Price adjustment in orders both to buy and to sell Execution priority: • Lower priced sell orders or higher priced buy orders have priority • First order placed has priority when multiple orders have same price. VOLUME LIMIT ORDERS SPREAD (BEST) BID (BEST) ASK BUY SELL VOLUME PRIORITY price ($)

Patient trading Limit Order BUY / SELL # OF SHARES LIMIT PRICE VOLUME • • Patient traders place non-marketable limit orders that do not lead to an immediate transaction • • Non-marketable limit orders accumulate • Limit order book is a storage device BID ASK NEW ASK price ($)

Patient trading Limit Order BUY / SELL # OF SHARES LIMIT PRICE VOLUME • • Patient traders place non-marketable limit orders that do not lead to an immediate transaction • • Non-marketable limit orders accumulate • Limit order book is a storage device BID ASK NEW ASK price ($)

Impatient trading Market Order BUY / SELL # OF SHARES VOLUME Market order: • An order to buy or sell up to a given volume • No limit price is defined • Executed immediately • Often causes unfavorable price impact BID ASK NEW ASK price ($)

Impatient trading Market Order BUY / SELL # OF SHARES VOLUME Market order: • An order to buy or sell up to a given volume • No limit price is defined • Executed immediately • Often causes unfavorable price impact BID ASK NEW ASK price ($)

Order cancellation VOLUME Limit order cancellations: • Limit orders can be cancelled by the owner • Market defined expiration price ($)

Order cancellation VOLUME Limit order cancellations: • Limit orders can be cancelled by the owner • Market defined expiration price ($)

u. Limit order arrival: Poisson process in time") ZI model (Unrealistic but somewhat tractable) u. Limit order arrival: Poisson process in time & price; ØMarket order arrival: Poisson process in time; ØCancellation: ØSeparate random in time (like radioactive decay); processes for buying and selling, with same parameters. Depth profile n p, t : Number of shares in limit order book at price p, time t. BID SELL LIMIT ORDERS BUY MARKET ORDERS 0 ASK BUY LIMIT ORDERS SELL MARKET ORDERS

ZI model (Unrealistic but somewhat tractable) u. Limit order arrival: Poisson process in time & price; ØMarket order arrival: Poisson process in time; ØCancellation: ØSeparate random in time (like radioactive decay); processes for buying and selling, with same parameters. Depth profile n p, t : Number of shares in limit order book at price p, time t. BID SELL LIMIT ORDERS BUY MARKET ORDERS 0 ASK BUY LIMIT ORDERS SELL MARKET ORDERS

Parameters of model Order flow rates Discreteness parameters Three fundamental dimensional quantities: shares S, price P, time T

Parameters of model Order flow rates Discreteness parameters Three fundamental dimensional quantities: shares S, price P, time T

Price impact from ZI model Real data shows less variation with epsilon than theory predicts

Price impact from ZI model Real data shows less variation with epsilon than theory predicts

Market impact fn- non dim units") Market impact function (non-dimensional units) Market impact fn- non dim units

Market impact function (non-dimensional units) Market impact fn- non dim units

Testing prediction of spread • Equation of state from mean field theory

Testing prediction of spread • Equation of state from mean field theory

From top 10 Russian jokes, Oct. 23, 2003 с сайта "Немецкая волна" http: //www. dw-world. de/russian/0, 3367, 2212_A_985770_1_A, 00. html Ученые-экономисты давно стараются понять закономерности, которым подчиняются биржевые курсы, и используют для этого математические модели. На протяжении многих десятилетий такие модели исходили из представлений о брокерах как об аналитиках с выдающимися умственными способностями, обладающих исчерпывающей информацией о рынке и действующих исключительно рационально. Однако удовлетворительно описать реальные изменения биржевых курсов эти модели оказались не в состоянии. Значительно успешнее справляется с этой задачей новая модель, предложенная Дойном Фармером (J. Doyne Farmer), сотрудником Института Санта-Фе в штате Нью-Мексико. Она базируется на предположении, что брокеры Ц полные Ђидиотыї, действующие совершенно случайно и к тому же лишенные какой бы то ни было информации. Сравнив данные, рассчитанные на основе этой модели, с реальными курсами лондонской фондовой биржи за период с 1998 -го по 2000 -й годы, ученые выявили очень высокую степень совпадения

From top 10 Russian jokes, Oct. 23, 2003 с сайта "Немецкая волна" http: //www. dw-world. de/russian/0, 3367, 2212_A_985770_1_A, 00. html Ученые-экономисты давно стараются понять закономерности, которым подчиняются биржевые курсы, и используют для этого математические модели. На протяжении многих десятилетий такие модели исходили из представлений о брокерах как об аналитиках с выдающимися умственными способностями, обладающих исчерпывающей информацией о рынке и действующих исключительно рационально. Однако удовлетворительно описать реальные изменения биржевых курсов эти модели оказались не в состоянии. Значительно успешнее справляется с этой задачей новая модель, предложенная Дойном Фармером (J. Doyne Farmer), сотрудником Института Санта-Фе в штате Нью-Мексико. Она базируется на предположении, что брокеры Ц полные Ђидиотыї, действующие совершенно случайно и к тому же лишенные какой бы то ни было информации. Сравнив данные, рассчитанные на основе этой модели, с реальными курсами лондонской фондовой биржи за период с 1998 -го по 2000 -й годы, ученые выявили очень высокую степень совпадения

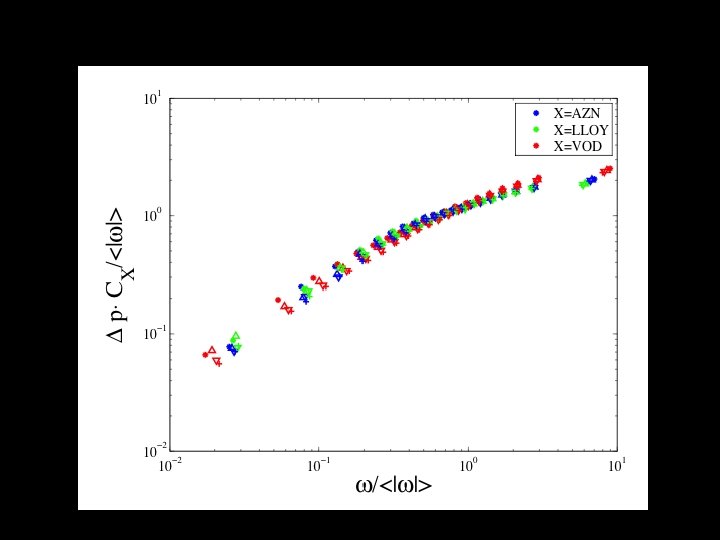

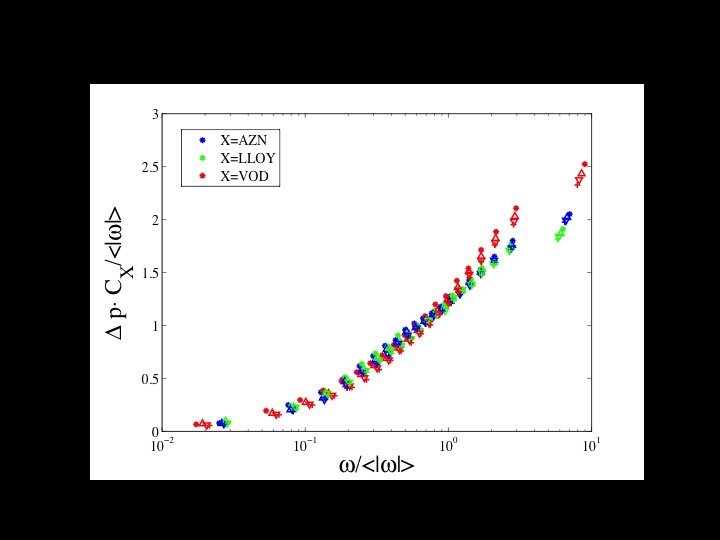

Price impact on longer timescales • Aggregate signed volumes for N successive transactions. • Aggregate signed price return for N successive transactions. • Vary N. • Normalize x and y axis according to mean value of absolute aggregate signed volume.

Price impact on longer timescales • Aggregate signed volumes for N successive transactions. • Aggregate signed price return for N successive transactions. • Vary N. • Normalize x and y axis according to mean value of absolute aggregate signed volume.

Price impact on longer time scales

Price impact on longer time scales

Statistical model

Statistical model

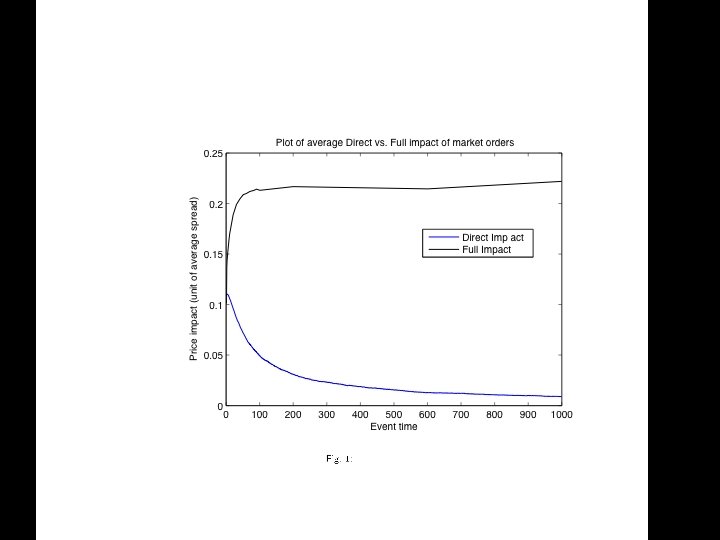

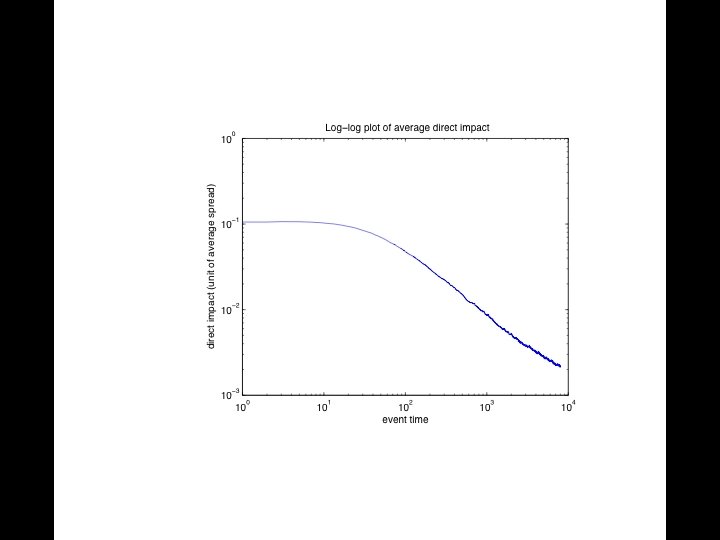

impact –") Decomposition of price impact Price impact has two parts: • Mechanical (direct) impact – When an order enters the book, it alters the state of the book, which alters future prices even if nothing else changes. • Indirect impact – Placement of the order may alter placement of future orders -- this measures interaction of agents. – Change can be due to direct impact or to other factors (e. g. direct observation of order placement) Is it possible to separate direct and indirect impacts?

Decomposition of price impact Price impact has two parts: • Mechanical (direct) impact – When an order enters the book, it alters the state of the book, which alters future prices even if nothing else changes. • Indirect impact – Placement of the order may alter placement of future orders -- this measures interaction of agents. – Change can be due to direct impact or to other factors (e. g. direct observation of order placement) Is it possible to separate direct and indirect impacts?

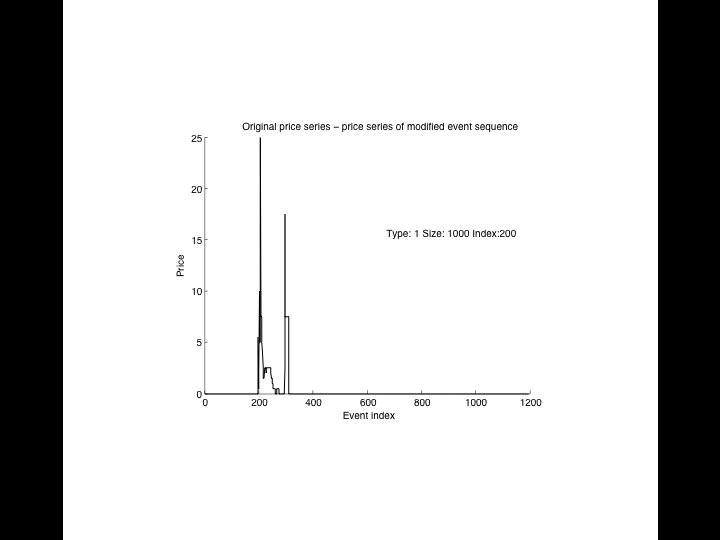

Measurement of direct impact • Any allowed sequence of orders and cancellations yields a unique price series – Cannot cancel an order that doesn’t exist • Can remove an order and then compute new series of prices – Can also partially remove an order – Can add orders • Difference in prices measures mechanical (direct) impact

Measurement of direct impact • Any allowed sequence of orders and cancellations yields a unique price series – Cannot cancel an order that doesn’t exist • Can remove an order and then compute new series of prices – Can also partially remove an order – Can add orders • Difference in prices measures mechanical (direct) impact