7ad18e8bdd8c72240f694d145f91cc22.ppt

- Количество слайдов: 50

Management at the Public-Private Interface: Using Industry Architecture as Method of Analysis A/Prof Jeffrey Funk National University of Singapore

Industry Architecture • Definitions – “an abstract description of the economic agents within an economic system” – represents the degree of vertical (dis) integration in an industry (Jacobides, Knudsen and Augier, 2006) • Changes in industry architecture (Brusoni and Prencipe, 2001; Jacobides, 2005; Jacobides and Winter, 2005) can come from – Technological changes – Institutional changes – Social changes • Advantages for public-private interface include ability to examine – degree of “openness” between different economic agents – Impact of policies on this openness

Use Three Examples to Discuss Role of Industry Architecture in: Management at Public-Private Interface • • Broadcasting Computers Mobile Internet All of these can be defined “loosely” as infrastructure

Example 1: Commercial Radio and Television Broadcasting • Similarities between countries – Most countries defined frequencies and standards for interface between transmitters and receivers • Differences between countries: – U. S. government did not create a single national provider and fund this provider with monthly fees on radio or television users – Instead, it • divided country into many small markets • licensed multiple firms in each market • restricted number of markets in which single firm could operate

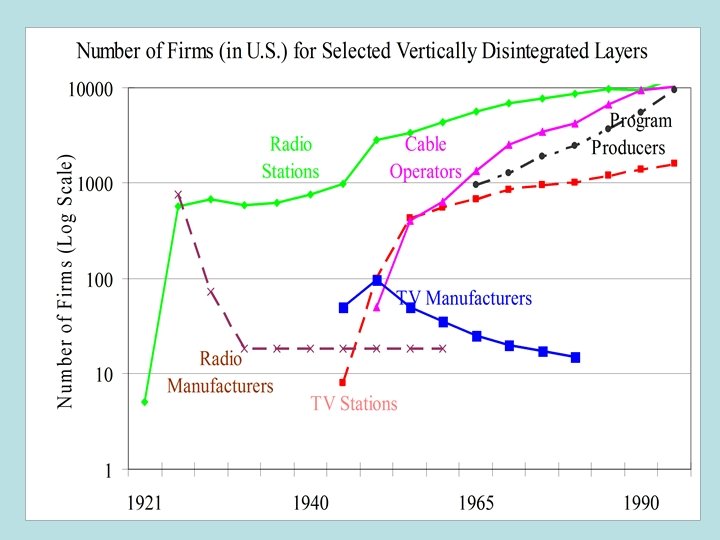

Results: Different Industry Architectures Most of World Thousands of local broadcasters Delivery of Programs Distribution of Programs Production of Programs Financing of Programs Evaluation of Programs United States One firm (e. g. , BBC) did most everything until recently 3 network broadcasters distributed programs to local broadcasters via AT&T’s telephone lines and later satellite and Internet firms As many as 10, 000 firms produce programs for broadcasters Many firms finance programs through advertisements Many rating and research agencies evaluate public response

Results • Greater number of firms were able to participate in radio and television industries • Greater variety of programs were available to citizens • More local programs that addressed local needs

Example 2: Computers in U. S. • Similarities between different computers – vertical disintegration emerged for most computer systems in for example, computer design, operating systems, electronic components, and peripherals • Differences between computers: – Mainframe vs. personal computers: independent suppliers of operating systems emerged for personal computers (and subsequent ones) – U. S. Justice Department’s anti-trust suit in late 1960 s against IBM caused IBM to unbundle hardware and application software. There was a different outcome in anti-trust suit against Microsoft in mid-1990 s

Results • Strong anti-trust suit in late 1960 s against IBM led to emergence of many industry-specific (1, 229) and cross-industry (777) application software products by 1974 (ICP Quarterly, 1974; Campbell -Kelly, 2003, A History of the Software Industry) • U. S. Justice Department’s weak anti-trust suit in mid-1990 s against Microsoft had a different result – initially successful software from Word. Perfect (word processing), Lotus (spreadsheet), and Borland (database) were largely replaced by software from Microsoft in 1990 s (Campbell-Kelly, 2003) – only two PC application software providers, Adobe and Novell, remained in the top 50 software firms by 2002 (Cusumano, 2004).

Example 3: Mobile Internet • Similarities between countries – Most countries defined frequencies and standards for interface between base stations and phones • Differences between countries: – Greater historical control of phone specifications by Japanese service providers enabled them to define standards for services such that services worked better in Japan (also in Korea) than in Western countries (Fransman, 2002; Funk, 2007) – Partly by accident, Japanese service providers • took smaller percentage of mobile commerce revenues • made simple form of electronic mail a standard function on all phones by 2000. This can be interpreted as greater openness between mobile and PC devices (Funk, 2007) • Western governments could have required open interface just as U. S. government required IBM to do so in mainframe computers

Results as of 2007 • Japan – Tens of thousands of profitable content providers – Mobile commerce exceeded 1. 15 trillion Yen (about 11. 5 B$ at 100 Yen/$) in 2007 of which fastest growing segment was non-entertainment commerce (represented 63% of mobile commerce) (MIAC, 2009) • Rest of World – Service providers take majority of revenues – Fact that m-commerce revenues for non-entertainment content are not reported in Western press or in analyses of Western mobile Internet markets (Tilson and Lyytinen, 2006; Hibberd, 2007, Sharma, 2009) suggest that they are very small or do not exist at all – These markets are finally growing (as i. Phone diffuses)

Summary • Industry architecture focuses our attention on – economic agents within an economic system – interfaces between economic agents • Industry architecture enables one to look at the public -private interface in terms of interfaces between economic agents • What policies will lead to – greater “openness” between different economic agents? – greater participation by different economic agents? – greater variety and value for end users? • Of course, greater openness does not always lead to greater value for end users (e. g. , mortgage banking and food)

• Appendix

Figure 3. Increasing Vertical Disintegration in Movie and Television Program Production (Number of Firms in Parentheses for 1966, 1974, and 1981) Total Number of Firms 1966: 956 1974: 1281 1981: 2470 1999: 9500 Artists Representatives (242, 359, 344) Rental Studios (13, 24, 67) Properties Firms (66, 33, 184) Market Research (3, 5, 24) Film Companies (563, 709, 1473) Film Processing (43, 76, 55) Editing (4, 31, 113) Recording/ Sound (20, 33, 187) Lighting (2, 16, 23) Source: Storper and Christopherson, 1987 (for 1999 figure: Scott, 2002)

Figure 2. Evolution of Industry Architecture for IT Sector Computer Design System 360 Computer Design Peripherals User (3) Customization Mini. Computers Computer Design IBM Unbundling Peripherals Computer Design User Customization (3) VARs 16 -bit word length Peripherals Computer Design App S/W Personal Computers (PCs) Peripherals Computer Design 1950 App S/W 1960 1970 IBM OS PC Microprocessor 1980 Server (2) Design OS Microprocessor Application S/W Peripherals Client (1) Design Networks OS Microprocessor Contract S/W, Services (4) Systems Software and Systems Integration App/ S/W App S/W Mainframe Computers Contract S/W, Services (4) Client-Server Systems Windows, UNIX, TCP/IP, Ethernet, 1990 S/W: software; App: application; OS: operating system; CPU: central processing unit; VAR: Value-added reseller. (1): Includes PCs and workstations. (2) Mainframe computers and workstations are also used as servers; (3) Includes contract S/W and services; 4) includes facility management, computer leasing, and remote services such as processing or time-sharing.

Figure 1. The Old Structure for the Mobile Phone Industry Batteries Displays Chips Phone Manufacturers Software Interface defined by air-interface standards such as GSM and CDMA Retail Base Stations Switching Equipment Service Providers Network Software Source: Adapted from (Steinbock, 2003; Peppard and Rylander, 2006) Customer

• Falling transaction costs (Jacobides and Winter, 2005) also impacted on architecture")

Interpretation (2) • Falling transaction costs (Jacobides and Winter, 2005) also impacted on architecture of radio industry and created entrepreneurial opportunities – choice of frequency band rudimentary standard reduced costs of matching transmitters and receivers – availability of AT&T’s telephone lines reduced transaction costs associated with different firms providing network and local broadcasting – existing network of entertainment firms reduced transaction costs associated with outsourcing content through advertising agencies • importation of radio programs from existing network of entertainment firms through advertising agencies • 1940 -ruling that playing records on air doesn’t violate copyrights enabled local broadcasters to import content from another existing set of entertainment firms, the music companies – Emergence of rating system reduced transaction costs associated with different firms providing financing and content production/evaluation

• Looking at other technological discontinuities, i. e. , industries in the broadcasting sector – Broadcast television – Cable television – Satellite television – Rental and sale of pre-recorded movies

Vertical Disintegration and Entrepreneurial Opportunities for Broadcast Television • Similar U. S. government policies enabled multiple broadcasters to co-exist • Similar strategies by network broadcasters: brought together local broadcasters, ad agencies, sponsors – used AT&T telephone lines to distribute programs to local broadcasters – created mobility (Jacobides, Knudsen and Augier, 2006) in other capabilities – number of licenses (3 to 4) restricted number of network broadcasters • Large number of submarkets (Klepper, 1997) in local broadcasters (geographical) and programs (genres) • Reductions in transaction costs through standards, AT&Ts telephone lines, rating system, film-chain technique

Vertical Disintegration and Entrepreneurial Opportunities for Other… • Cable television – Enabled television to reach a small niche market of consumers that could not receive broadcasted signal – Satellites enabled cable companies to access and provide new content, i. e. , so-called cable channels, and thus created many entrepreneurial opportunities • Recorded movies – Emergence of standards (Beta and VHS) enabled separation of manufacturers, film/program producers, and rental stores and thus created many entrepreneurial opportunities • Satellite television – Provided an additional way for film/program producers to reach consumers and thus created many entrepreneurial opportunities • Cable, satellite, and recorded movies reduced power of network broadcasters and increased power of program producers

Results: Number of Firms Pre-recorded videos Standard set in mid 1970 s Number of retail outlets was 25 -30, 000 by 1995 Number of manufacturers increased 5 X from 1975 to 1985 Also large numbers of advertising agencies research agencies rating services

• Vertical disintegration created many entrepreneurial opportunities • Understanding emergence of vertical")

Conclusions (1) • Vertical disintegration created many entrepreneurial opportunities • Understanding emergence of vertical disintegration is critical issue for entrepreneurs • Types of events that led to emergence of vertical disintegration – Emergence of open standards including ones that are often defined as dominant designs – Regulatory decisions: restrictions on ownership of local broadcasters – Legal decisions: allowed play of records on air, AT&T excluded from industry – Strategic decisions: network broadcasters outsourced many activities and create mobility in them

• Consistent with Klepper (1997), following factors may explain numbers of firms")

Conclusions (2) • Consistent with Klepper (1997), following factors may explain numbers of firms in each vertically disintegrated layer • Large economies of scale reduced number of: network broadcasters, telephone and satellite companies, manufactures of radios, TVs, video playback equipment • Submarkets – Many: local broadcasters, cable companies, and video rental stores; and program producers – Few: manufacturers of radio and TV receivers, and video playback equipment • Emergence of new vertically disintegrated layer facilitated increases in number of firms in another existing layer – Emergence of music as free source of content facilitated growth in number of local radio broadcasters – Ability of cable companies to access programs from satellites facilitated increases in the number of them and program producers

• Appendix

Examples of Sub-Markets in Programming for Discontinuities Discontinuity Sub-markets AM Radio Initially music (played by live bands), drama, talk, and variety shows Later recorded music FM Radio Various types of music styles such as country, rock-and roll, classical, jazz, easy listening Broadcast Television Comedies, country and westerns, detective dramas, news, cartoons, other program types Cable and Satellite TV Expansion in number of channels increased and changed the types of program types Recorded Movies Many types of movies Sources: (Sterling, 1979 a; Sterling, 1979 b; Sterling and Kittross, 1990, 2001; Leblebici et al, 1991; Lewis, 1991; Gomery, 2000 a; 2000 b, 2000 c)

Events that Led to Vertical Disintegration and Changes in the Industry Architectures in the Broadcasting Sector (1) Discontinuity Events that led to vertical Facilitated Entry or Separation disintegration and changes in industry of: architectures Radio Broadcasting *Choice of AM (1910 s) and FM (1950 s) frequency bands and standards Separation of broadcasters and radio manufacturers Advertising as business model and rating system Separation of content financing (advertising agencies and sponsors) from content production Regulatory support for local ownership Separation of local and network broadcasters AT&T makes network available Strategic entry by network broadcasters Ruling that playing records on air doesn’t violate copyrights Further entry of local broadcasters

Events that Led to Vertical Disintegration and Changes in the Industry Architectures in the Broadcasting Sector (2) Discontinuity Events that led to vertical disintegration and changes in industry architectures Facilitated Entry or Separation of: Television *Choice of black and white (1940) and Separation of broadcasters and Broadlater color (1954) standards radio manufacturers casting Advertising as business model and rating Separation of content financing system from content production Regulatory support for local ownership AT&T introduces coaxial cable Separation of local and network broadcasters Strategic entry by network broadcasters “Film chain” and video tape (Ampex) standards Entry of film and other independent program producers

Events that Led to Vertical Disintegration and Changes in the Industry Architectures in the Broadcasting Sector (3) Discontinuity Events that led to vertical disintegration and changes in industry architectures Facilitated Entry or Separation of: Cable Television *Distribution of programs to local cable companies via satellite (1975) Entry of new program producers and cable companies Recorded Movies *Beta (1975) and VHS (1976) standards, later DVD (Digital Video Disk) Separation of manufacturers, film producers and video rental stores Satellite Television *Direct broadcast satellite standard (1994) Separation of satellite operators and receiver sales

Key Design")

Examples of Key Design Decisions for Radio Broadcasting (* Represents Dominant Design) Key Design Decisions Type of Design Decision Facilitated Entry/ Separation of: Vacuum tubes, superheterodyne circuits Alternative technologies Not applicable AM (1920 s) and FM frequency Modular bands and broadcasting standards * designs Broadcasters and radio manufacturers Regulatory support for local ownership Local broadcasters Advertising as business model and ratings system Network providers and advertisers/sponsors, later rating agencies AT&T’s network for distribution of program Ruling that playing records on air doesn’t violate copyrights Record companies

Key Design Decisions")

Examples of Key Design Decisions for TV Broadcasting (*Represents Dominant Design) Key Design Decisions Type of Design Decision Facilitated Entry/ Separation of: Cathode ray tubes (CRTs), iconoscope cameras, etc. Alternative Not applicable technologies Choice of black and white, later color Modular (1954) broadcasting standards * designs Manufacturers and broadcasters Regulatory support for local ownership Local broadcasters Advertising as business model, rating system AT&T introduces coaxial cable Network providers and advertisers, sponsors, programming companies “Film chain, ” video tape (Ampex) standards Film producers, programming companies

Discontinuity Key Design Decisions Cable Connect")

Examples of Other Key Design Decisions (*Dominant Designs) Discontinuity Key Design Decisions Cable Connect homes and Television broadcasters with coaxial cable, later microwave relays Type of Design Decision Facilitated Entry/ Separation of: Alternative technologies Cable providers Distribute programs to local Modular designs New national cable companies via satellite* program producers Recorded Movies Helical Scan Alternative technologies Beta and VHS* standards Modular designs Manufacturers, film producers, video rental stores Digital Video Disk* (DVD) standard Modular designs Manufacturers, film producers, video rental stores Satellite Digital video broadcasting Television (DVB)* Alternative technologies Not applicable Direct broadcast by satellite operators

Number of Firms for Other Layers • Number of manufacturers of video recorders increased from about 10 in 1975 (right before emergence of dominant design) to more than 50 in 1983/84 (Cusumano et al, 1992) • By 1995, there were 25, 000 to 30, 000 stores dealing exclusively in videos and an additional 10, 000 to 12, 000 other stores (e. g. , supermarkets) that rent videos but not as their main business.

• Emergence of standards that are often defined as dominant designs in")

Conclusions (1) • Emergence of standards that are often defined as dominant designs in the broadcasting sector has led to increases in number of firms in broadcasting industry – AM and FM radio standards: local broadcasters, manufacturers – B&W and color standards: local broadcasters, programming companies, and even manufacturers – Linking satellites and cable companies: number of cable companies, programming companies – VHS: number of retail outlets, manufacturers, programming companies • This suggests that – when design decisions lead to modular design and vertical disintegration, emergence of dominant designs leads to entrepreneurial opportunities – important for entrepreneurs to understand systems and how modular design and vertical disintegration emerge in systems

• Vertical disintegration has played an important role in creating entrepreneurial opportunities")

Conclusions (2) • Vertical disintegration has played an important role in creating entrepreneurial opportunities (i. e. , increasing the number of firms) in the broadcasting industry • Without vertical disintegration, the number of firms in the industry would be much fewer • Specific design decisions led to modular design and vertical disintegration – Some were by firms and some were by governments – Some were the result of a top-down decision process and others a bottom-up process – Multiple design decisions were important in a single discontinuity – Many of these decisions are signals to entrepreneurs

• Understanding how modular design and vertical disintegration emerge are important issues")

Conclusions (3) • Understanding how modular design and vertical disintegration emerge are important issues for entrepreneurs (and incumbents) • How can firms identify those design decisions/events that will lead to vertical disintegration? • How can we as universities help our students understand the process by which vertical disintegration emerges? – Existing theory of dominant designs misleads students – Existing emphasis of systems engineering misleads students into a simplistic view of a single designer in a top-down process

Appendix

Radio: 1910 s and 1920 s • Major Issues – Government versus private control: U. S. licensed many private firms and set restrictions on local ownership (most countries only offered government services) – Subscription (most countries) versus advertising (U. S. ) model • Advertising model appeared in early 1920 s – Manufacturers and retailers of radios started radio stations – They transmitted music and advertisements (mostly for radios) on the same program – Many bands played for low wages or even for free in hopes of increased publicity for their music • In 1923, radio stations with known ownership were operated by – Entrepreneurial manufacturers (47%) – Retailers such as department or music stores (20%) • Problems with this “vertical integration” – The number of radio manufacturers quickly declined – Many producers of consumer products wanted to advertise their products on the radio

Radio: Late 1920 s – 1940 s • Entry of advertising agencies, other firms (vertical disintegration) • Major issue was how to finance the production of programming – Can this be done without economies of scale, i. e. , serving a national audience? – Commerce Department outlawed the playing of records on the radio and restricted the number of stations that could be owned by a single firm • The network provider (NBC, CBS, later ABC) became the solution: They – – developed programs in cooperation with advertising agencies created alliances with local broadcasters delivered programs to the local broadcasters via AT&T’s telephone lines Controlled the design rules in the negotiations with the other vertically disintegrated layers • The emergence of advertising agencies facilitated the emergence of – independent producers of radio programs – talent agents – transcription syndicates

• Complex design rules (contracts between firms)")

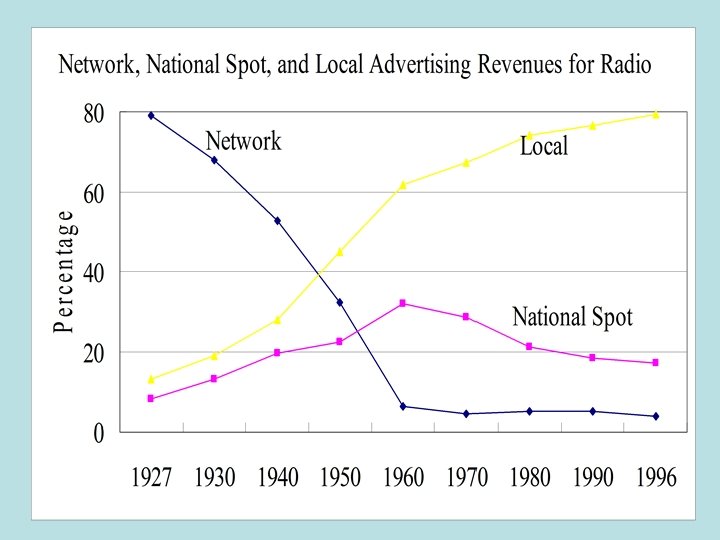

Radio: 1920 s – 1940 s (continued) • Complex design rules (contracts between firms) determined the interactions between the various modules • AT&T only exited the radio business and provided its telephone lines to the networks through legal and regulatory pressure from RCA and the U. S. Government – legal disputes and back room deals continued to determine the conditions under which broadcasters obtained access to AT&T’s network well into the 1940 s • The network and local (not shown in Figure 2) broadcasters produced their own programs partly to counter the power of the advertising agencies – thus advertising agencies only fill half the production layer in the column entitled “Radio: 1920 s to 1940 s” in Figure 2. • Relationship between the networks and local broadcasters – the networks tried various types of contractual relationships with the local broadcasters – the networks’ control of the programs caused the percentage of radio stations that were affiliated with a national network to increase from 6% in 1927 to a peak of 97% in 1947

Radio: Changes in the Early 1950 s that Formed Today’s Industry • Rating services first introduced in 1929 – facilitated a growth in national “spot” advertising – In spot advertising, advertisers purchased “time” as opposed to the rights for an entire national program. – The spread of spot advertising reduced the power of the networks • Phonographs became an accepted form of program content – Ban on playing phonograph records on the radio was rescinded in 1941 – By the early 1950 s most record companies realized that playing records on the radio increased the sales of phonograph records • The start of television reduced the network’s and national manufacturers’ interests in radio • New business model emerged – Local broadcasters played records and local advertisements – FM radio provided the sound quality necessary for rock and roll music – AM radio stations focused on sports and music for older listeners

Television: 1940 s – 1950 s • Similar type of vertical disintegration emerged in television as in radio. Network broadcasters – – developed programs with advertising agencies delivered programs over AT&T’s telephone lines (now using coaxial cable) created alliances with local broadcasters broadcast films using “film chain” technology • More difficult for local broadcasters to be independent from networks in television – Television programs were more expensive to develop than radio programs – Independent local broadcasters typically played “re-runs” that were purchased through “syndicators” • By the late 1950 s, advertising agencies were being replaced in the value chain – There was a limited number of sponsors that could finance a single program – The networks gradual use of multiple sponsors for a single program gradually eliminated the advertising agencies

Television: From 1960 s • Networks took control of programming • Networks outsourced some of the programs to “program packagers” – program packagers combined talent, production facilities, and ideas for specific programs or series under contract to a network – thus they were also vertically disintegrated – by 1960, they produced about 60% of television programs (versus 14% for single sponsored programs) and their role was strengthened by a 1970 FCC (Federal Communications Commission) ruling (this restricted the networks’ ability to be the production source for most of their prime-time programming) – Program packagers also sold their programs to unaffiliated local broadcasters through “syndicators” (videotape facilitated this) • Networks purchased movies from film companies – By the 1970 s, television broadcasting provided film/movie companies with more income than theaters did – Vertical disintegration also occurred in film production following the Paramount antitrust decision in 1948 where a network or “flexible” form of movie production to emerge.

Cable Television • Delivery – First, local cable companies transmitted broadcasted signals from local antennas to homes via coaxial cables – Second, they imported signals from other broadcasters via microwave relays – Third, they replaced microwave relay systems with satellites – By 1976, improvements in these cable systems had enabled 23% of cable subscribers to receive more than 12 channels and this figure continued to grow in the 1980 s and 1990 s • Services – Used satellites and coaxial cable to increase number of channels and to charge for new channels (called pay cable) – Percentage of subscribers with pay cable increased from less than 1% in 1973 to 21% of all subscribers in 1978 and continued to grow in the 1980 s and 1990 s – Diffusion of pay cable contributed to a growth in the number of program providers

A View of Modern Cable Infrastructure Interfaces to other networks Master Interface Primary Ring Regional Interface Secondary Ring Hub Cluster of about 125 -2000 customers Optical Nodes CATV-Net Source: European Cable Communications Association, Dirk Jaeger

Recorded Movies • Television broadcasters used the first video recording equipment in the 1950 s to: – broadcast programs multiple times in different time zones – sell the rights of the recorded programs (i. e. , syndication) to other broadcasters • By the mid-1970 s, this equipment had become inexpensive enough for some consumers – First in time-shifted recording and later in playback of pre-recorded movies (sales of blank and pre-recorded tapes were about equal by 1980) – About 75% of pre-recorded tapes sold in 1978 -79 were pornographic – The emergence of two (Beta and VHS) and later one standard (VHS) enabled new layers of vertical disintegration • video rental stores (strengthened by DVDs) – 25, 000– 35, 000 exclusive stores, another 10, 000 – 12, 000 other stores in 1995 – Top 50 chains accounted for 49% of the rentals in late 1990 s • independent distributors (later absorbed by film companies)

• Large movie distributors controlled interface between them and video stores")

Recorded Movies (continued) • Large movie distributors controlled interface between them and video stores – rental outlets stocked movies that benefited from the promotions, which accompanied theater release – large movie distributors use video rentals (and sales) as just one more stage in their complex calculation of price discrimination to maximize revenues and thus provide the means to develop blockbuster movies • Large movie distributors keep re-writing the rules to their advantage – Took back control of distribution – Introduced pricing policies that emphasize sales – Replaced sale of tapes to stores with revenue sharing • Facilitated by increasing concentration in rental stores (e. g. , Blockbuster) • Strengthened consolidation in rental stores – Movie distributors make far more money from the sale and rental of DVDs than from movie theater showings

Television • Satellites – first used to distribute programs to")

Direct Broadcast Satellite (DBS) Television • Satellites – first used to distribute programs to local cable companies – satellite dishes had become cheap enough for consumer and digital compression enabled households to receive up to 200 channels by the 1990 s • Hughes was the first firm to offer DBS with digital compression – it used small cable franchises to signup subscribers and to install the satellite dishes, which were initially the biggest bottlenecks to satellite diffusion – Hughes’ first mover advantage enabled it to strike better deals with programming companies and have forced its largest competitor, Echo. Star to set prices that were (as of 2004) 1/3 lower than Hughes’ prices – The real competition for Hughes Direc. TV has been the cable television MSOs. Few entrepreneurial opportunities have emerged for satellite television.

Examples of Sub-Markets in Programming for Discontinuities Discontinuity Sub-markets AM Radio Initially music (played by live bands), drama, talk, and variety shows Later recorded music FM Radio Various types of music styles such as country, rock-and roll, classical, jazz, easy listening Broadcast Television Comedies, country and westerns, detective dramas, news, cartoons, other program types Cable and Satellite TV Expansion in number of channels increased and changed the types of program types Recorded Movies Many types of movies Sources: (Sterling, 1979 a; Sterling, 1979 b; Sterling and Kittross, 1990, 2001; Leblebici et al, 1991; Lewis, 1991; Gomery, 2000 a; 2000 b, 2000 c)

7ad18e8bdd8c72240f694d145f91cc22.ppt