70f1db77cc1a426032e598b37293f6fa.ppt

- Количество слайдов: 72

Macroeconomic Policy Fundamentals Chapter 13

Macroeconomic Policy Fundamentals Chapter 13

Discussion Topics üCharacteristics of money üFederal Reserve System üChanging the money supply üMoney market equilibrium üEffects of monetary policy on economy üThe federal budget deficit üThe national debt üFiscal policy options

Discussion Topics üCharacteristics of money üFederal Reserve System üChanging the money supply üMoney market equilibrium üEffects of monetary policy on economy üThe federal budget deficit üThe national debt üFiscal policy options

Functions of Money 1. Medium of exchange – facilitates payment to others for goods and services 2. Unit of accounting – assessing profitability of businesses, household budgets and aggregate variables like GDP 3. Store of value – money is a liquid asset which has value in investment portfolios and cash flow decisions of businesses and households Page 299

Functions of Money 1. Medium of exchange – facilitates payment to others for goods and services 2. Unit of accounting – assessing profitability of businesses, household budgets and aggregate variables like GDP 3. Store of value – money is a liquid asset which has value in investment portfolios and cash flow decisions of businesses and households Page 299

Functions of the Fed 1. 2. 3. 4. Supply the economy with paper currency Supervise member banks Provide check collection and clearing services Maintain the reserve balances of depository institutions 5. Lend to depository institutions 6. Act at the federal government’s banker and fiscal agent 7. Regulate the money supply Page 302 -303

Functions of the Fed 1. 2. 3. 4. Supply the economy with paper currency Supervise member banks Provide check collection and clearing services Maintain the reserve balances of depository institutions 5. Lend to depository institutions 6. Act at the federal government’s banker and fiscal agent 7. Regulate the money supply Page 302 -303

Location of the 12 District Federal Reserve Banks Page 301

Location of the 12 District Federal Reserve Banks Page 301

Changing of the Guard Alan Greenspan Bernanke

Changing of the Guard Alan Greenspan Bernanke

The Fed’s Policy Tools ü Reserve requirements – depository institutions are required to maintain a specific fraction of their customers’ deposits as reserves. ü Discount rate – rate depository institutions pay when they borrow from the Fed ü Open market operations – Fed can buy or sell government securities to alter the money supply Page 304 – 305

The Fed’s Policy Tools ü Reserve requirements – depository institutions are required to maintain a specific fraction of their customers’ deposits as reserves. ü Discount rate – rate depository institutions pay when they borrow from the Fed ü Open market operations – Fed can buy or sell government securities to alter the money supply Page 304 – 305

Role of the Board of Governors of the Federal Reserve System Page 303

Role of the Board of Governors of the Federal Reserve System Page 303

Role of the Board of Governors of the Federal Reserve System Page 303

Role of the Board of Governors of the Federal Reserve System Page 303

Role of the Board of Governors of the Federal Reserve System Page 303

Role of the Board of Governors of the Federal Reserve System Page 303

Key role played by the Federal Open Market Committee or FOMC Page 303

Key role played by the Federal Open Market Committee or FOMC Page 303

Recent Fed Rate Actions

Recent Fed Rate Actions

Role of the 12 District Federal Reserve Banks located throughout the country Page 303

Role of the 12 District Federal Reserve Banks located throughout the country Page 303

Determinants of the Money Supply

Determinants of the Money Supply

Existing money supply curve. Note it is perpendicular to the quantity axis, implying it is unaffected by the interest rate. Page 309

Existing money supply curve. Note it is perpendicular to the quantity axis, implying it is unaffected by the interest rate. Page 309

Expansionary monetary policy actions will shift the MS curve to the right over a period of 12 months or so. Page 309

Expansionary monetary policy actions will shift the MS curve to the right over a period of 12 months or so. Page 309

Contractionary monetary policy actions, on the other hand, will shift the money supply curve to left over a similar time period. Page 309

Contractionary monetary policy actions, on the other hand, will shift the money supply curve to left over a similar time period. Page 309

Suppose a depositor in Bank Ag sells $1 million in government securities to the Fed. He then deposits the proceeds from the sale in his bank. If the fractional reserve requirement ratio is 20 percent, Bank Ag can increase the volume of its loans by $800, 000. Suppose the proceeds of these loans are deposited in Bank B. Follow the trail to the Total line. Page 307

Suppose a depositor in Bank Ag sells $1 million in government securities to the Fed. He then deposits the proceeds from the sale in his bank. If the fractional reserve requirement ratio is 20 percent, Bank Ag can increase the volume of its loans by $800, 000. Suppose the proceeds of these loans are deposited in Bank B. Follow the trail to the Total line. Page 307

Change in the Money Supply We can skip tracing deposits through the economy by using the following money supply (MS) equation: MS = (1. 0 ÷ RR) × TR = MM × TR where TR represents total reserves and RR is the reserve requirement ratio. The expression with the brackets is known as the money multiplier. We can restate this equation in terms of the change in the money supply as follows: MS = (1. 0 ÷ RR) × TR = MM × TR Page 307 – 308

Change in the Money Supply We can skip tracing deposits through the economy by using the following money supply (MS) equation: MS = (1. 0 ÷ RR) × TR = MM × TR where TR represents total reserves and RR is the reserve requirement ratio. The expression with the brackets is known as the money multiplier. We can restate this equation in terms of the change in the money supply as follows: MS = (1. 0 ÷ RR) × TR = MM × TR Page 307 – 308

Change in the Money Supply Using the example in Table 13. 3 of the $1 million deposit on page 307 and 20% reserve requirements ratio, we see that the change in the money supply is: MS = (1. 0 ÷. 20) x TR = 5. 0 x $1 million = $5 million This results in a change in loans of loans = MS - TR = $5 million - $1 million = $4 million See bottom line in Table 13. 3 Page 307 – 308

Change in the Money Supply Using the example in Table 13. 3 of the $1 million deposit on page 307 and 20% reserve requirements ratio, we see that the change in the money supply is: MS = (1. 0 ÷. 20) x TR = 5. 0 x $1 million = $5 million This results in a change in loans of loans = MS - TR = $5 million - $1 million = $4 million See bottom line in Table 13. 3 Page 307 – 308

Change in money supply Change in = loan volume Initial + infusion Page 307

Change in money supply Change in = loan volume Initial + infusion Page 307

Impacts of Policy Tools Expansionary actions: Fed buys securities Fed lowers the discount rate Fed lowers required reserve ratio Effects of action: Total reserves increase Money multiplier increases Greenspan Page 308 - 309

Impacts of Policy Tools Expansionary actions: Fed buys securities Fed lowers the discount rate Fed lowers required reserve ratio Effects of action: Total reserves increase Money multiplier increases Greenspan Page 308 - 309

Impacts of Policy Tools Expansionary actions: Fed buys securities Fed lowers the discount rate Fed lowers required reserve ratio Effects of action: Total reserves increase Money multiplier increases Contractionary actions: Fed sells securities Fed raises the discount rate Fed raises required reserve ratio Effects of action: Total reserves decrease Money multiplier decreases Greenspan Page 308 - 309

Impacts of Policy Tools Expansionary actions: Fed buys securities Fed lowers the discount rate Fed lowers required reserve ratio Effects of action: Total reserves increase Money multiplier increases Contractionary actions: Fed sells securities Fed raises the discount rate Fed raises required reserve ratio Effects of action: Total reserves decrease Money multiplier decreases Greenspan Page 308 - 309

Determinants of the Money Demand

Determinants of the Money Demand

Demand for Money üTransactions demand for money – carry cash to pay for normal expenditures üPrecautionary demand for money – carry cash to cover unexpected expenditures üSpeculative demand for money – hold cash as an asset in investment portfolios since the value of cash does not decline during periods of falling asset prices. Page 310 - 311

Demand for Money üTransactions demand for money – carry cash to pay for normal expenditures üPrecautionary demand for money – carry cash to cover unexpected expenditures üSpeculative demand for money – hold cash as an asset in investment portfolios since the value of cash does not decline during periods of falling asset prices. Page 310 - 311

: MD = c –d(R)") The money demand curve is given by equation (16. 5): MD = c –d(R) + e(NI) where R is the rate of interest and NI is national income. The coefficient d is the slope of the curve and e represents MD÷ NI. Page 311

The money demand curve is given by equation (16. 5): MD = c –d(R) + e(NI) where R is the rate of interest and NI is national income. The coefficient d is the slope of the curve and e represents MD÷ NI. Page 311

+ e(NI) Page") Increase in income increases demand for money MD = c –d(R) + e(NI) Page 311

Increase in income increases demand for money MD = c –d(R) + e(NI) Page 311

Money market interest rate given by intersection of demand supply Page 311

Money market interest rate given by intersection of demand supply Page 311

MS * 0. 06 Expansionary monetary policy lowers interest rates Page 311

MS * 0. 06 Expansionary monetary policy lowers interest rates Page 311

MS * 0. 14 Contractionary monetary policy raises interest rates Page 311

MS * 0. 14 Contractionary monetary policy raises interest rates Page 311

The full effects of this change could take 12 months or more to register in bank deposits Page 312

The full effects of this change could take 12 months or more to register in bank deposits Page 312

A change in the money supply will alter the equilibrium interest rate in the money market Page 312

A change in the money supply will alter the equilibrium interest rate in the money market Page 312

We know from Chapter 12 that a change in interest rates will lead to movement along the planned investment function…. increasing or decreasing new investment Page 312

We know from Chapter 12 that a change in interest rates will lead to movement along the planned investment function…. increasing or decreasing new investment Page 312

We also know from Chapter 12 that increased investment expenditures, a component of GDP, increases the demand for labor, lowers unemployment and thus fuels further growth in national income… Page 312

We also know from Chapter 12 that increased investment expenditures, a component of GDP, increases the demand for labor, lowers unemployment and thus fuels further growth in national income… Page 312

Eliminating Recessionary and Inflationary Gaps

Eliminating Recessionary and Inflationary Gaps

What is the magnitude of the recessionary gap? Page 313

What is the magnitude of the recessionary gap? Page 313

What is the magnitude of the recessionary gap? It is YFE – Y 1 Page 313

What is the magnitude of the recessionary gap? It is YFE – Y 1 Page 313

The use of expansionary monetary policy actions to push aggregate demand from AD 1 to AD 3 increases real GDP from Y 1 to Y 3 while only increasing the general price level to P 3. Page 313

The use of expansionary monetary policy actions to push aggregate demand from AD 1 to AD 3 increases real GDP from Y 1 to Y 3 while only increasing the general price level to P 3. Page 313

÷P 0 Recessionary gap of YFE –") Inflation rate (P 3 – P 0) ÷P 0 Recessionary gap of YFE – Y 1 is partially closed to YFE – Y 3 Page 313

Inflation rate (P 3 – P 0) ÷P 0 Recessionary gap of YFE – Y 1 is partially closed to YFE – Y 3 Page 313

The further use of expansionary monetary policy to push aggregate demand from AD 3 to AD 4 increases real GDP from Y 3 to YFE (full employment GDP), but increases the general price level to P 4. Page 313

The further use of expansionary monetary policy to push aggregate demand from AD 3 to AD 4 increases real GDP from Y 3 to YFE (full employment GDP), but increases the general price level to P 4. Page 313

÷P 3 Recessionary gap fully closed Page") Inflation rate (P 4 – P 3) ÷P 3 Recessionary gap fully closed Page 313

Inflation rate (P 4 – P 3) ÷P 3 Recessionary gap fully closed Page 313

The use of expansionary monetary policy to attain YPOT by shifting aggregate demand to AD 5 will increase the general price level to P 5. Inflation rate (P 5 – P 4) ÷P 4 Inflationary gap created…. . Page 313

The use of expansionary monetary policy to attain YPOT by shifting aggregate demand to AD 5 will increase the general price level to P 5. Inflation rate (P 5 – P 4) ÷P 4 Inflationary gap created…. . Page 313

Microeconomic Interest Rate Implications

Microeconomic Interest Rate Implications

Interest Rate Impacts on a 10 Year $150 K Business Loan Inter Annual est total PI rate payment Annual interest payment Total interest payment 8 percent $22, 354. 69 $73, 546. 90 14 percent 28, 757. 67 137, 576. 88 20 percent 35, 782. 44 207, 824. 40 Page 315

Interest Rate Impacts on a 10 Year $150 K Business Loan Inter Annual est total PI rate payment Annual interest payment Total interest payment 8 percent $22, 354. 69 $73, 546. 90 14 percent 28, 757. 67 137, 576. 88 20 percent 35, 782. 44 207, 824. 40 Page 315

Interest Rate Impacts on a 20 Year $100 K Home Mortgage Inter Monthly est rate total PI payment Monthly interest payment Total interest payment 8 percent $848. 78 $432. 08 $103, 707. 46 12 percent 1, 115. 73 699. 06 167, 773. 46 Page 315

Interest Rate Impacts on a 20 Year $100 K Home Mortgage Inter Monthly est rate total PI payment Monthly interest payment Total interest payment 8 percent $848. 78 $432. 08 $103, 707. 46 12 percent 1, 115. 73 699. 06 167, 773. 46 Page 315

What is Fiscal Policy? üTaxation by federal, state and local governments üGovernment spending by federal state and local governments üBudget deficit and the national debt Page 316

What is Fiscal Policy? üTaxation by federal, state and local governments üGovernment spending by federal state and local governments üBudget deficit and the national debt Page 316

States Without Income Tax Eight states do not have a state income tax

States Without Income Tax Eight states do not have a state income tax

State and Local Taxes üAlaska, thanks to oil reserves, has the lowest tax burden üMaine registering the highest has the highest tax burden üMajor sources are sales taxes and property taxes

State and Local Taxes üAlaska, thanks to oil reserves, has the lowest tax burden üMaine registering the highest has the highest tax burden üMajor sources are sales taxes and property taxes

Our focus is on fiscal policy at the federal level….

Our focus is on fiscal policy at the federal level….

Rising spending and tax cuts to spur the economy brought back budget deficits Page 318

Rising spending and tax cuts to spur the economy brought back budget deficits Page 318

Individuals and not businesses pay the Bulk of federal taxes. Page 318

Individuals and not businesses pay the Bulk of federal taxes. Page 318

The effects of 9/11 and increased spending plus tax cuts to stimulate the economy led to record high deficits… A strong economy and controlled spending led to the first budget surplus in more than 20 years… Page 320

The effects of 9/11 and increased spending plus tax cuts to stimulate the economy led to record high deficits… A strong economy and controlled spending led to the first budget surplus in more than 20 years… Page 320

Recent Trends in Deficit • Typically the economy runs a budget deficit at the federal level • 1998 -2001 were the exceptions in recent years • Fueled by growing economy and falling interest rates

Recent Trends in Deficit • Typically the economy runs a budget deficit at the federal level • 1998 -2001 were the exceptions in recent years • Fueled by growing economy and falling interest rates

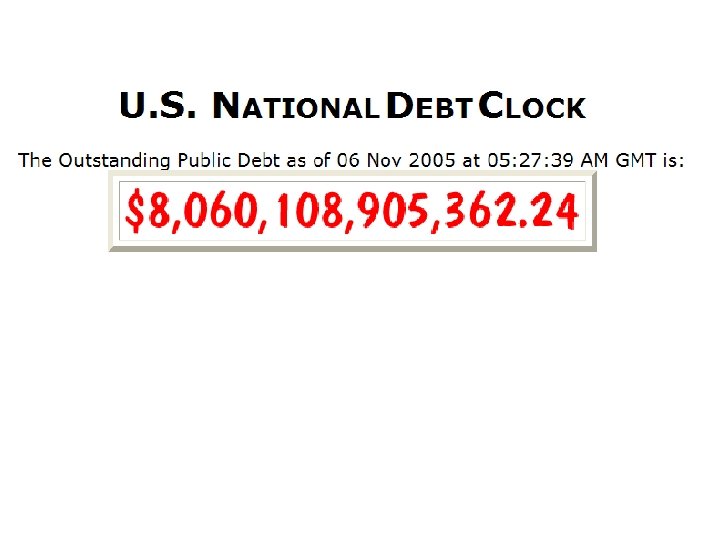

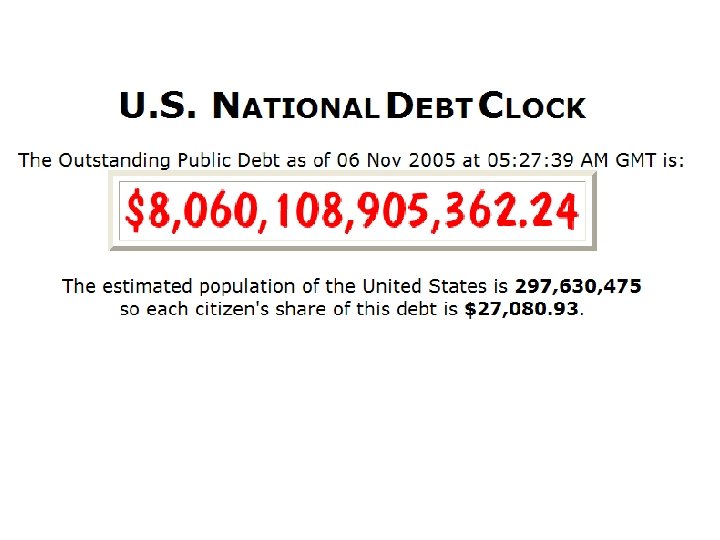

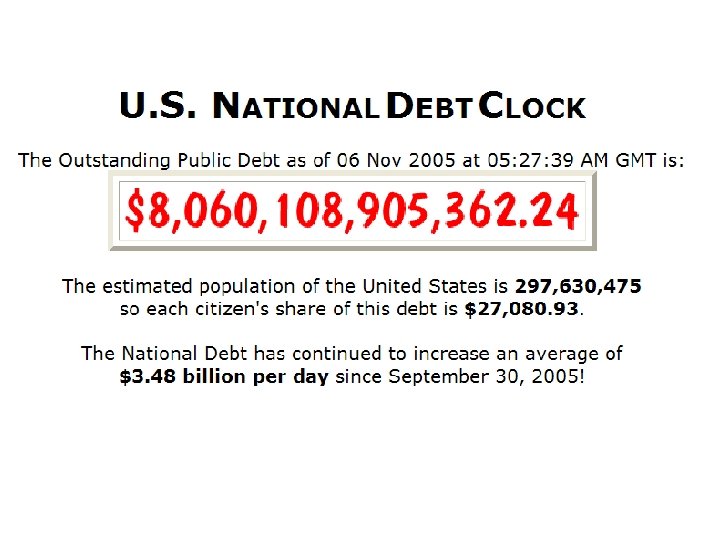

Debt and the Deficit National debt. T = National debt. T-1 + Deficit. T

Debt and the Deficit National debt. T = National debt. T-1 + Deficit. T

The growth in federal spending has grown rapidly over the last 20 years… Page 321

The growth in federal spending has grown rapidly over the last 20 years… Page 321

While the national debt grew as deficit spending dominated the 1980 s and 1990 s, debt as a percent of GDP stayed within post-WW II experience… Page 322

While the national debt grew as deficit spending dominated the 1980 s and 1990 s, debt as a percent of GDP stayed within post-WW II experience… Page 322

Federal government spending on Agriculture programs is the fourth highest on this list of total federal spending.

Federal government spending on Agriculture programs is the fourth highest on this list of total federal spending.

Fiscal Policy Options Ø Automatic fiscal policy instruments: take effect without explicit action by policymakers (e. g. , progressive tax rates) Ø Discretionary fiscal policy instruments: require explicit actions by the president or Congress (e. g. , passing a law) Page 324

Fiscal Policy Options Ø Automatic fiscal policy instruments: take effect without explicit action by policymakers (e. g. , progressive tax rates) Ø Discretionary fiscal policy instruments: require explicit actions by the president or Congress (e. g. , passing a law) Page 324

Impacts of Policy Tools Expansionary actions: Cut taxes Increase government spending Effects of action: Increase disposable income Increase aggregate demand Congress & Bush Page 327

Impacts of Policy Tools Expansionary actions: Cut taxes Increase government spending Effects of action: Increase disposable income Increase aggregate demand Congress & Bush Page 327

Impacts of Policy Tools Expansionary actions: Cut taxes Increase government spending Effects of action: Increase disposable income Increase aggregate demand Contractionary actions: Increase taxes Cut government spending Effects of action: Decrease disposable income Decrease aggregate demand Congress & Bush Page 327

Impacts of Policy Tools Expansionary actions: Cut taxes Increase government spending Effects of action: Increase disposable income Increase aggregate demand Contractionary actions: Increase taxes Cut government spending Effects of action: Decrease disposable income Decrease aggregate demand Congress & Bush Page 327

A federal budget deficit requires the U. S. Treasury to issue more government securities to balance sources and uses of funds… Page 324

A federal budget deficit requires the U. S. Treasury to issue more government securities to balance sources and uses of funds… Page 324

An increase in the sale of government securities reduces the pool of private capital available to finance investment expenditures, raising interest rates… Page 324

An increase in the sale of government securities reduces the pool of private capital available to finance investment expenditures, raising interest rates… Page 324

We know from Chapter 12 that higher interest rates depresses investment expenditures… Page 324

We know from Chapter 12 that higher interest rates depresses investment expenditures… Page 324

The use of expansionary fiscal policy actions to push aggregate demand from AD 1 to AD 3 increases real GDP from Y 1 to Y 3 while only increasing the general price level to P 3. Inflation rate (P 3 – P 0) ÷P 0 Recessionary gap partially closed Page 328

The use of expansionary fiscal policy actions to push aggregate demand from AD 1 to AD 3 increases real GDP from Y 1 to Y 3 while only increasing the general price level to P 3. Inflation rate (P 3 – P 0) ÷P 0 Recessionary gap partially closed Page 328

The use of expansionary fiscal policy to push demand from AD 3 to AD 4 increases real GDP from Y 3 to YFE (full employment GDP), But increases the general price level to P 4. Inflation rate (P 4 – P 3) ÷P 3 Recessionary gap closed…. Page 328

The use of expansionary fiscal policy to push demand from AD 3 to AD 4 increases real GDP from Y 3 to YFE (full employment GDP), But increases the general price level to P 4. Inflation rate (P 4 – P 3) ÷P 3 Recessionary gap closed…. Page 328

The use of expansionary fiscal policy to attain YPOT by shifting aggregate demand to AD 5 will Increase the general price level to P 5. Inflation rate (P 5 – P 4) ÷P 4 Inflationary gap created…. Page 328

The use of expansionary fiscal policy to attain YPOT by shifting aggregate demand to AD 5 will Increase the general price level to P 5. Inflation rate (P 5 – P 4) ÷P 4 Inflationary gap created…. Page 328

Monetary Policy Summary üFunctions of money and the role of the Federal Reserve System in the economy üThe money multiplier and the growth of the money supply üTools of monetary policy üDemand for money and money market equilibrium üPolicy linkages and timing of full effects üElimination of recessionary and inflationary gaps.

Monetary Policy Summary üFunctions of money and the role of the Federal Reserve System in the economy üThe money multiplier and the growth of the money supply üTools of monetary policy üDemand for money and money market equilibrium üPolicy linkages and timing of full effects üElimination of recessionary and inflationary gaps.

Fiscal Policy Summary üDifference between discretionary and automatic fiscal policy tools üExpansionary and contractionary fiscal policy actions üApplication to eliminating recessionary and inflationary gaps üBudget deficits, national debt and concept of “crowding out”

Fiscal Policy Summary üDifference between discretionary and automatic fiscal policy tools üExpansionary and contractionary fiscal policy actions üApplication to eliminating recessionary and inflationary gaps üBudget deficits, national debt and concept of “crowding out”

Chapter 14 focuses on the key consequences of business fluctuations….

Chapter 14 focuses on the key consequences of business fluctuations….