34e5ac9b6031cd7f521ddfb5de4af7c3.ppt

- Количество слайдов: 77

Macroeconomic for Social Negotiators Open Economy Gustavo Rinaldi - ITC-ILO Consultant University of Turin - ESCP – Europe Turin, November 2016

Macroeconomic for Social Negotiators Open Economy Gustavo Rinaldi - ITC-ILO Consultant University of Turin - ESCP – Europe Turin, November 2016

") Objective What is: The balance of payments The International Investment Position (IIP or NIIP) Explaining the spread on sovereign bonds The aggregated Demand in an open Economy The Nominal Exchange rate The Real Exchange Rate

Objective What is: The balance of payments The International Investment Position (IIP or NIIP) Explaining the spread on sovereign bonds The aggregated Demand in an open Economy The Nominal Exchange rate The Real Exchange Rate

that flow between any individual country and") Balance of payments measures the payments (flows) that flow between any individual country and all other countries. The International Investment Positions measures the linked stocks.

Balance of payments measures the payments (flows) that flow between any individual country and all other countries. The International Investment Positions measures the linked stocks.

Balance of payments Current Account Capital account Financial account

Balance of payments Current Account Capital account Financial account

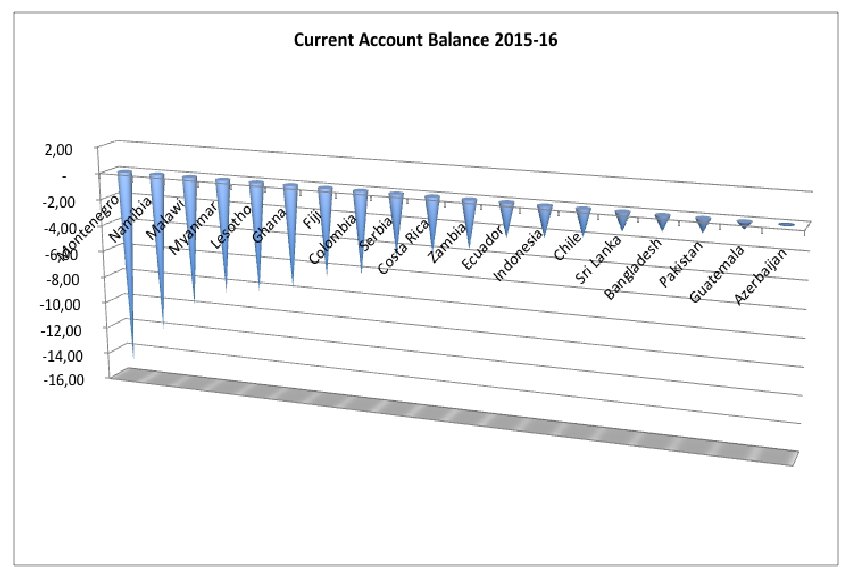

Balance of payments Current Account: its balance indicates a ∆ in the wealth of the nation The Financial account has the same absolute value of the Current account +Capital account. Errors and omissions exist.

Balance of payments Current Account: its balance indicates a ∆ in the wealth of the nation The Financial account has the same absolute value of the Current account +Capital account. Errors and omissions exist.

Current Account + export - import +services sold to foreigners - services bought from foreigners +Net Investment (or capital) Incomes From Abroad +Net Labor Incomes From Abroad +Net Transfers ______________ Current Account Balance

Current Account + export - import +services sold to foreigners - services bought from foreigners +Net Investment (or capital) Incomes From Abroad +Net Labor Incomes From Abroad +Net Transfers ______________ Current Account Balance

Current Account + export - import +services sold to foreigners - services bought from foreigners +Net Investment (or capital) Incomes From Abroad +Net Labor Incomes From Abroad +Net Transfers ______________ Current Account Balance

Current Account + export - import +services sold to foreigners - services bought from foreigners +Net Investment (or capital) Incomes From Abroad +Net Labor Incomes From Abroad +Net Transfers ______________ Current Account Balance

services Transport Trading Insurance Legal Medical Accounting IT Banking Restaurant services Hotelling

services Transport Trading Insurance Legal Medical Accounting IT Banking Restaurant services Hotelling

Net Labour incomes Net Capital Incomes They represent the") Net Incomes From Abroad (NIFA) Net Labour incomes Net Capital Incomes They represent the difference between …. . and …. .

Net Incomes From Abroad (NIFA) Net Labour incomes Net Capital Incomes They represent the difference between …. . and …. .

Net Labor Incomes + Wages of residents in this country temporarily working abroad - Wages of residents abroad temporarily working in this country

Net Labor Incomes + Wages of residents in this country temporarily working abroad - Wages of residents abroad temporarily working in this country

Net Capital Incomes + Incomes of investors who are resident in this country and earn money with their investments abroad (dividends on shares, capital gains and coupons on bonds, rents on foreign properties, profits from direct participation in foreign firms) - Incomes of investors who are resident abroad and earn money with their investment in this country

Net Capital Incomes + Incomes of investors who are resident in this country and earn money with their investments abroad (dividends on shares, capital gains and coupons on bonds, rents on foreign properties, profits from direct participation in foreign firms) - Incomes of investors who are resident abroad and earn money with their investment in this country

Net Transfers + Presents that residents in this country receive from foreign residents + Contributions that international organizations and foreign countries give to this country - Presents that residents in this country give to foreign residents - Contributions that this country gives to international organizations and foreign countries

Net Transfers + Presents that residents in this country receive from foreign residents + Contributions that international organizations and foreign countries give to this country - Presents that residents in this country give to foreign residents - Contributions that this country gives to international organizations and foreign countries

Current Account + export - import +services sold to foreigners - services bought from foreigners +Net Investment (or capital) Incomes From Abroad +Net Labor Incomes From Abroad +Net Transfers (or net secondary income) ______________ Current Account Balance

Current Account + export - import +services sold to foreigners - services bought from foreigners +Net Investment (or capital) Incomes From Abroad +Net Labor Incomes From Abroad +Net Transfers (or net secondary income) ______________ Current Account Balance

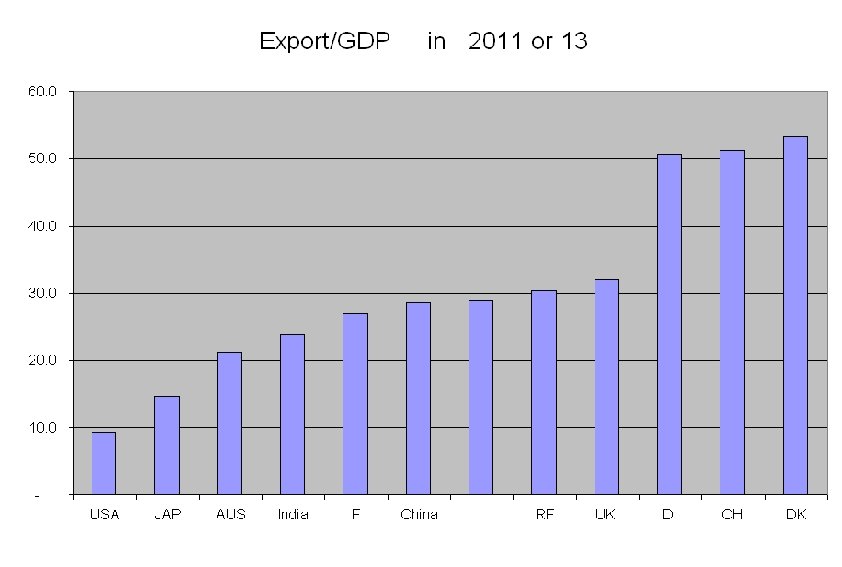

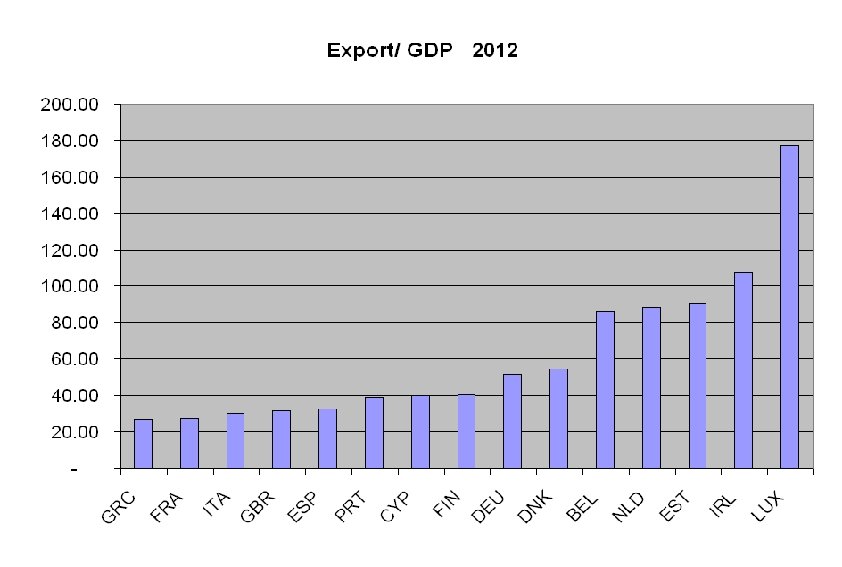

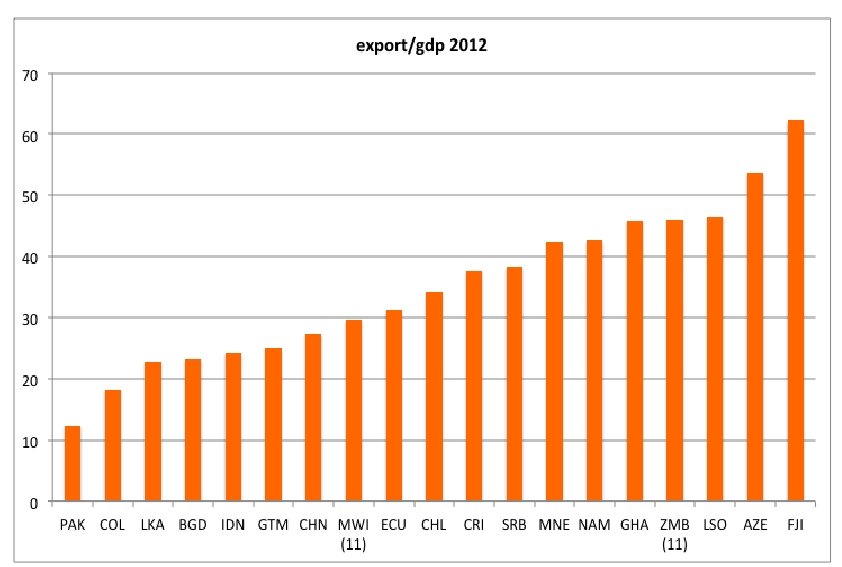

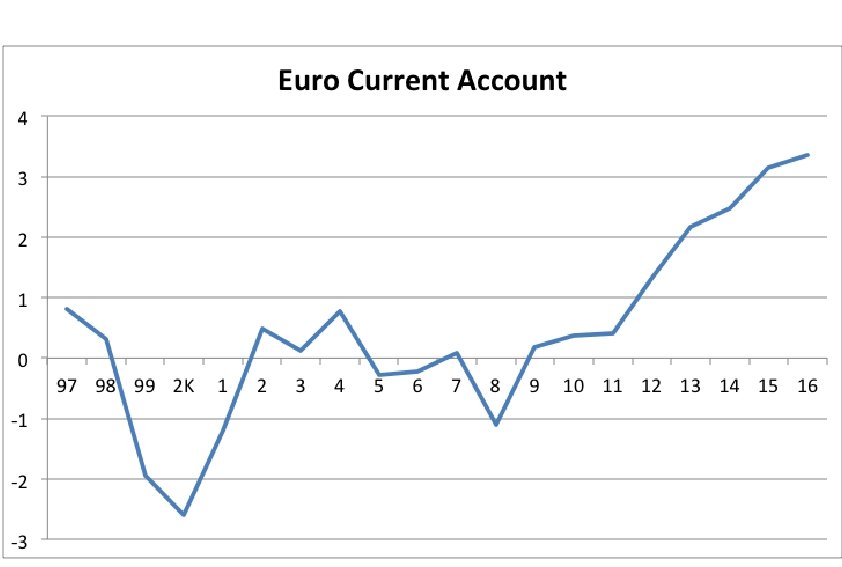

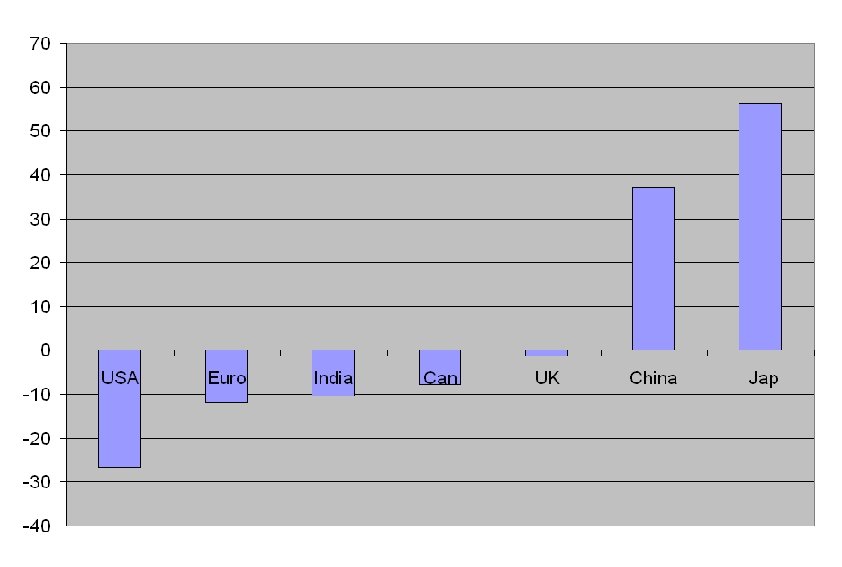

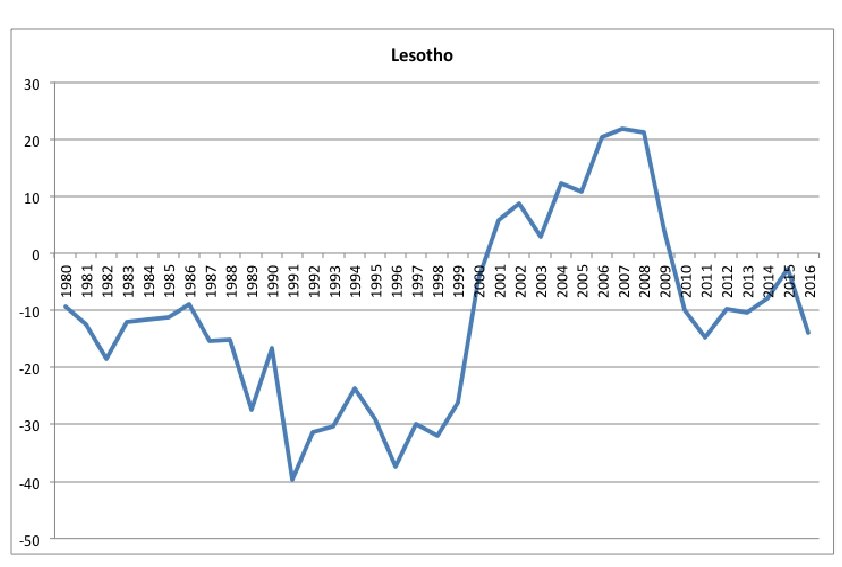

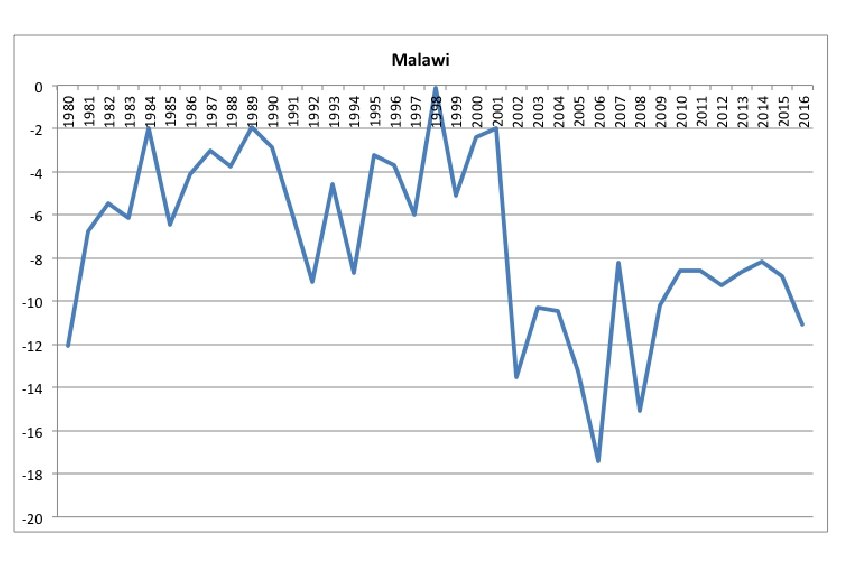

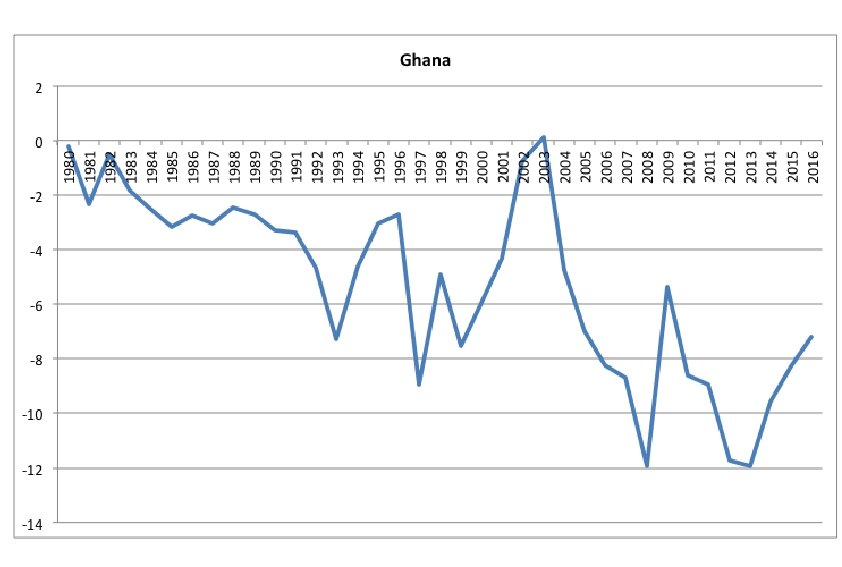

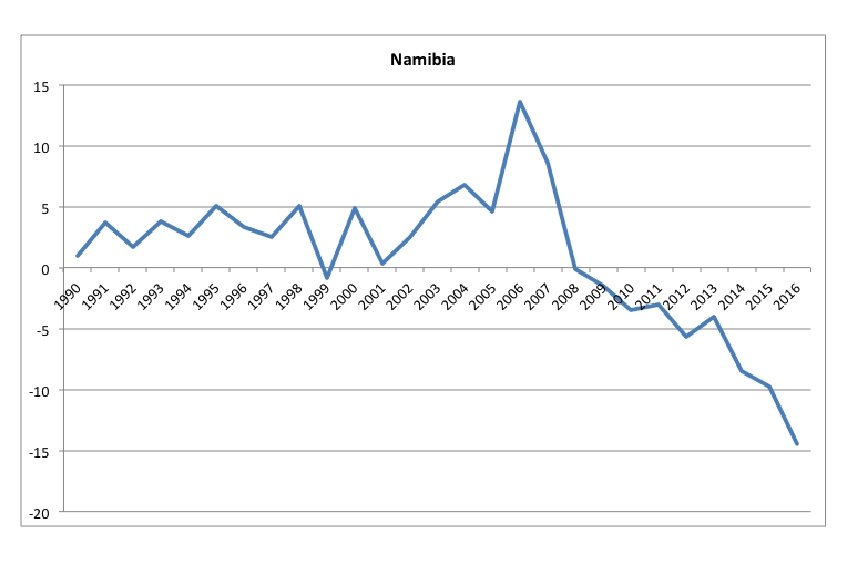

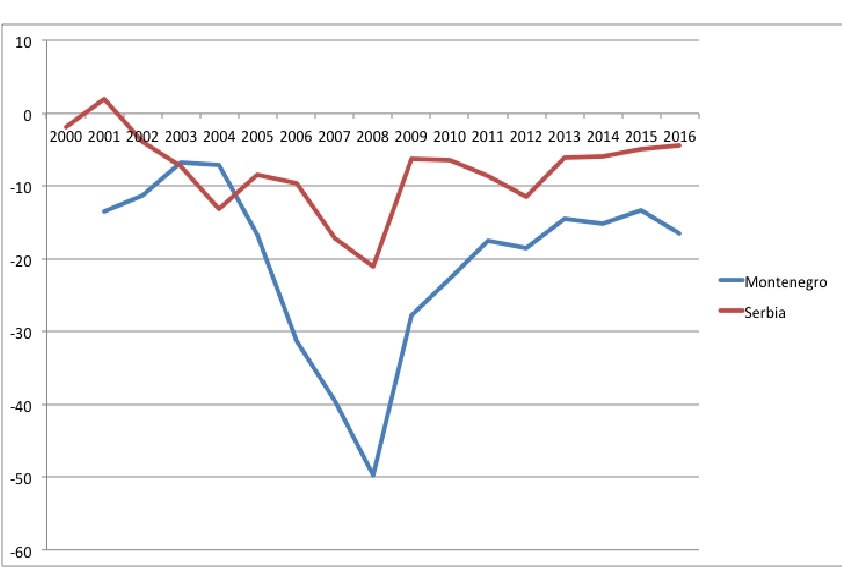

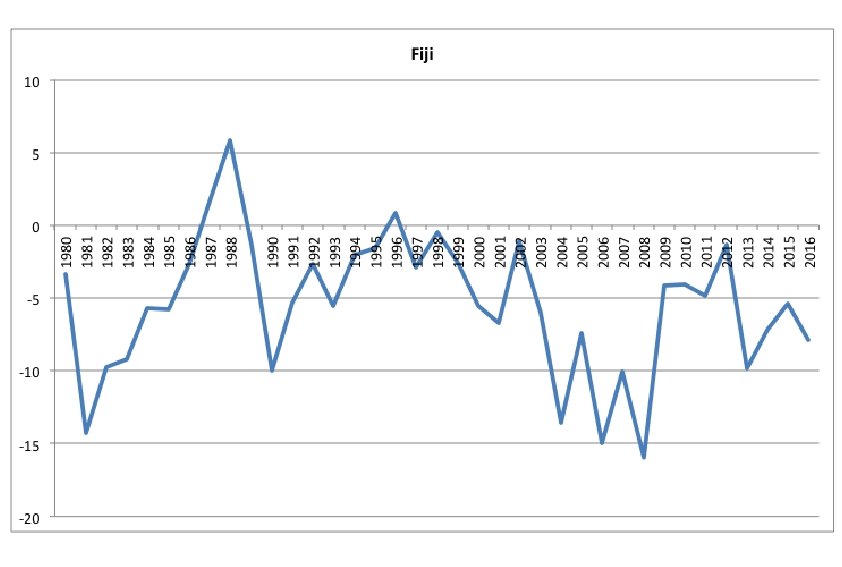

CURRENT ACCOUNT / GDP

CURRENT ACCOUNT / GDP

CURRENT ACCOUNT / GDP

CURRENT ACCOUNT / GDP

Current Account / GDP

Current Account / GDP

+ non financial and non produced") Capital Account + transfers of capital (debt forgiveness) + non financial and non produced assets (land, leases and licenses, and marketing assets such as brands) +Assets of people leaving or entering the country ______________ Capital Account Balance

Capital Account + transfers of capital (debt forgiveness) + non financial and non produced assets (land, leases and licenses, and marketing assets such as brands) +Assets of people leaving or entering the country ______________ Capital Account Balance

Portfolio") Financial Account = current acc. + capital acc. Direct Investment (buildings and firms) Portfolio Investment Equity Debt Securities short term and medium long term. + Financial Derivatives + Other Investment Monetary Authorities General Government Monetary and Financial Institutions Other sectors Reserve assets ERRORS AND OMISSIONS

Financial Account = current acc. + capital acc. Direct Investment (buildings and firms) Portfolio Investment Equity Debt Securities short term and medium long term. + Financial Derivatives + Other Investment Monetary Authorities General Government Monetary and Financial Institutions Other sectors Reserve assets ERRORS AND OMISSIONS

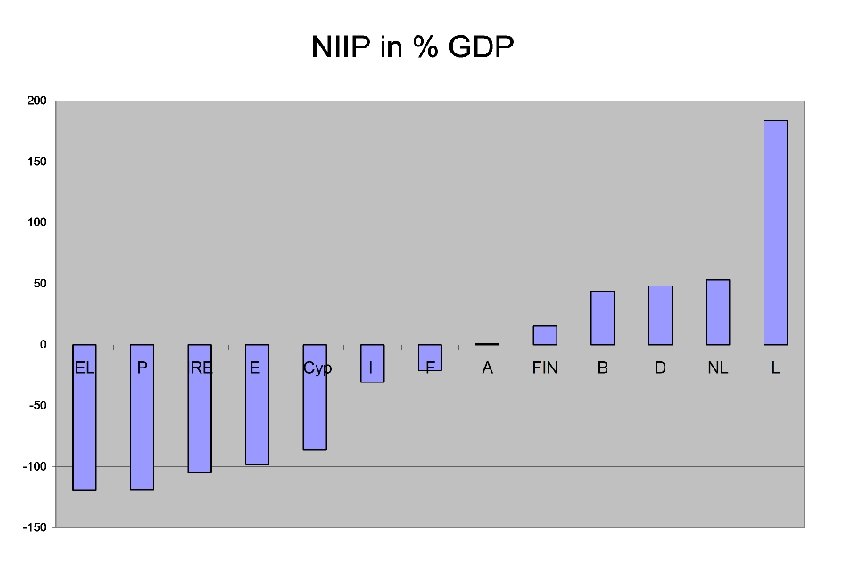

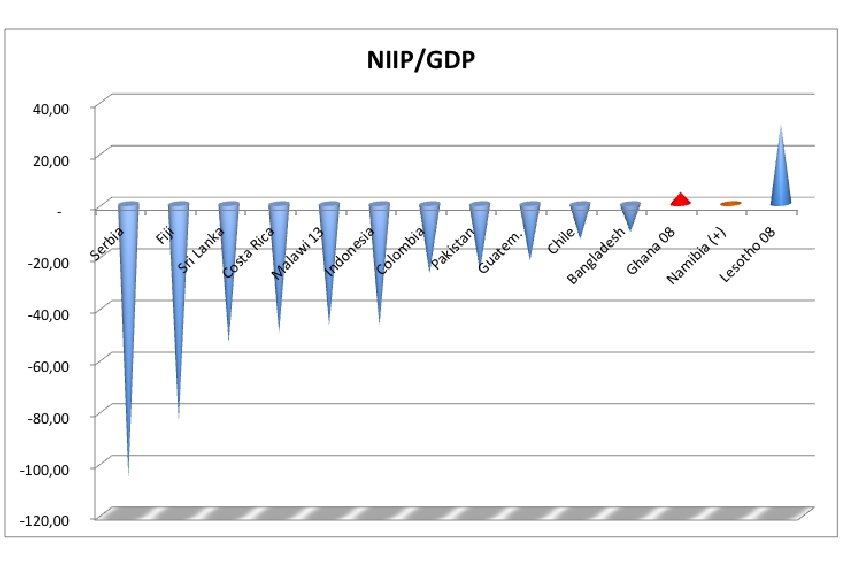

A statistical statement that presents external assets and liabilities,") The International Investment Position (IIP) A statistical statement that presents external assets and liabilities, and net balance of resident sectors at market value. External assets and liabilities are made up of real and financial assets, either tangible or intangible, held by residents in relation to nonresidents and vice versa. http: //www. mecon. gov. ar/cuentas/internacionales/documentos/international_investment_position_methodology. pdf

The International Investment Position (IIP) A statistical statement that presents external assets and liabilities, and net balance of resident sectors at market value. External assets and liabilities are made up of real and financial assets, either tangible or intangible, held by residents in relation to nonresidents and vice versa. http: //www. mecon. gov. ar/cuentas/internacionales/documentos/international_investment_position_methodology. pdf

IMF data

IMF data

The Net International Investment Position is more or less the sum of the current account and capital account of the last years.

The Net International Investment Position is more or less the sum of the current account and capital account of the last years.

The interest paid by sovereign bonds in some periods and in some places depends from some external forces (in the euro zone between 1999 and 2009 the idea that there was European solidarity, more recently the “whatever it takes” or the announcement of purchases of bonds by Draghi). In other moments it depends on the credit worthiness of the specific sovereign country. What is the best proxy for the credit worthiness of a sovereign entity? Deficit/ GDP? NO Debt/GDP? Not too much. The IIP or NET IIP (NIIP) is probably the best proxy.

The interest paid by sovereign bonds in some periods and in some places depends from some external forces (in the euro zone between 1999 and 2009 the idea that there was European solidarity, more recently the “whatever it takes” or the announcement of purchases of bonds by Draghi). In other moments it depends on the credit worthiness of the specific sovereign country. What is the best proxy for the credit worthiness of a sovereign entity? Deficit/ GDP? NO Debt/GDP? Not too much. The IIP or NET IIP (NIIP) is probably the best proxy.

NIIP and interest rare

NIIP and interest rare

Interest rate

Interest rate

The NIIP in 2009 -2010 Permits to predict 76% (78% if we omit the USA) of interest variation in march 2012 Any policy, which worsens the NIIP of a country (e. g. Sale of dividend-making firms or properties to foreigners) risks to increase its interest rate. The NIIP is influenced by the balance of payments, but what does influence the balance of payments?

The NIIP in 2009 -2010 Permits to predict 76% (78% if we omit the USA) of interest variation in march 2012 Any policy, which worsens the NIIP of a country (e. g. Sale of dividend-making firms or properties to foreigners) risks to increase its interest rate. The NIIP is influenced by the balance of payments, but what does influence the balance of payments?

+") Open Economy: A New Aggregated Demand Z ≡ co + c 1 (Y-T) + I + G old Z ≡ co + c 1 (Y-T) + I + G + X – IM new Z ≡ co + c 1 Y+ I + ( G- c 1 T) + X – IM …. . . PRIVATE PUBLIC FOREIGN

Open Economy: A New Aggregated Demand Z ≡ co + c 1 (Y-T) + I + G old Z ≡ co + c 1 (Y-T) + I + G + X – IM new Z ≡ co + c 1 Y+ I + ( G- c 1 T) + X – IM …. . . PRIVATE PUBLIC FOREIGN

+ X – IM Trade Balance Trade Deficit, if < 0 Trade Surplus, if > 0

+ X – IM Trade Balance Trade Deficit, if < 0 Trade Surplus, if > 0

What is the price in international business? Price matters Exchange rate matters

What is the price in international business? Price matters Exchange rate matters

Open Economy: A New Aggregated Demand + X – IM when this, the major component of the Balance Of Payments, diminishes too much, the country suffers.

Open Economy: A New Aggregated Demand + X – IM when this, the major component of the Balance Of Payments, diminishes too much, the country suffers.

If residents in foreign countries buy national goods The Aggregated Demand of domestic goods increases Z ≡ co + c 1 (Y-T) + I + G + X – IM

If residents in foreign countries buy national goods The Aggregated Demand of domestic goods increases Z ≡ co + c 1 (Y-T) + I + G + X – IM

Open Economy: A new choice Shall I buy national or foreign goods?

Open Economy: A new choice Shall I buy national or foreign goods?

How much foreign currency should I give to obtain a") Nominale exchange rate A) How much foreign currency should I give to obtain a unit of domestic currency? You paid $1, 48 (29/04/2011) to buy € 1 http: //markets. ft. com/markets/overview. asp B) You can also use the reverse, i. e. the price in national currency of a foreign currency (1/1, 48) $ 1 = € 0, 68 We just have to be consistent WE USE A

Nominale exchange rate A) How much foreign currency should I give to obtain a unit of domestic currency? You paid $1, 48 (29/04/2011) to buy € 1 http: //markets. ft. com/markets/overview. asp B) You can also use the reverse, i. e. the price in national currency of a foreign currency (1/1, 48) $ 1 = € 0, 68 We just have to be consistent WE USE A

How much foreign currency should I give to obtain a") Nominale exchange rate A) How much foreign currency should I give to obtain a unit of domestic currency? You paid $1, 22 (30/12/2014) to buy € 1 http: //markets. ft. com/markets/overview. asp B) You can also use the reverse, i. e. the price in national currency of a foreign currency (1/1, 22) $ 1 = € 0, 82 We just have to be consistent WE USE A

Nominale exchange rate A) How much foreign currency should I give to obtain a unit of domestic currency? You paid $1, 22 (30/12/2014) to buy € 1 http: //markets. ft. com/markets/overview. asp B) You can also use the reverse, i. e. the price in national currency of a foreign currency (1/1, 22) $ 1 = € 0, 82 We just have to be consistent WE USE A

Exchange rates regimes: Flexible: authorities (our government and central bank) leave it fluctuate") (Nominal) Exchange rates regimes: Flexible: authorities (our government and central bank) leave it fluctuate freely Fixed : Government and/or the central bank fix an exchange rate between national currency and a foreign currency or a basket of foreign currencies and actively defend it Mixes

(Nominal) Exchange rates regimes: Flexible: authorities (our government and central bank) leave it fluctuate freely Fixed : Government and/or the central bank fix an exchange rate between national currency and a foreign currency or a basket of foreign currencies and actively defend it Mixes

Cadillac CTS Luxury Sedan

Cadillac CTS Luxury Sedan

") 37, 535 $ (nov 2008)

37, 535 $ (nov 2008)

") 63, 465 $ (apr 2011)

63, 465 $ (apr 2011)

Alfa Romeo MITO 1. 6 120 cv

Alfa Romeo MITO 1. 6 120 cv

") € 20, 550 (nov 2008)

€ 20, 550 (nov 2008)

") € 21, 600 (apr 2011)

€ 21, 600 (apr 2011)

How many Cadillac Sedan was I able to buy with one Alfa MITO in 2008?

How many Cadillac Sedan was I able to buy with one Alfa MITO in 2008?

How many Cadillac Sedan was I able to buy with one Alfa MITO in 2008? 1. 3233 * 20. 550 = 37, 535 26, 565 37, 535 = 0, 7

How many Cadillac Sedan was I able to buy with one Alfa MITO in 2008? 1. 3233 * 20. 550 = 37, 535 26, 565 37, 535 = 0, 7

How many Cadillac Sedan can I buy with one Alfa MITO, today? 1. 48 * 21, 600 = 63, 465 31, 968 = 0, 50 63, 465 We should expect an improvement in Alfa Romeo sales

How many Cadillac Sedan can I buy with one Alfa MITO, today? 1. 48 * 21, 600 = 63, 465 31, 968 = 0, 50 63, 465 We should expect an improvement in Alfa Romeo sales

How many Cadillac Sedan can I buy with one Alfa MITO? It Depends on: P price Alfa Mito P* price Cadillac Sedan E Nominale exchange rate (cost in $ of € 1)

How many Cadillac Sedan can I buy with one Alfa MITO? It Depends on: P price Alfa Mito P* price Cadillac Sedan E Nominale exchange rate (cost in $ of € 1)

How many Cadillac Sedan can I buy with one Alfa MITO? It Depends on: = REAL P E P* EXCHANGE RATE

How many Cadillac Sedan can I buy with one Alfa MITO? It Depends on: = REAL P E P* EXCHANGE RATE

We are not just interested in these cars, therefore we shall use the price indexes (GDP deflators). The value of GDP deflators depends on the bases that we use; its absolute value is not very important, but its variation is very important

We are not just interested in these cars, therefore we shall use the price indexes (GDP deflators). The value of GDP deflators depends on the bases that we use; its absolute value is not very important, but its variation is very important

Real Exchange Rate Variations Real Appreciation: goods of this country become more expensive Real Depreciation

Real Exchange Rate Variations Real Appreciation: goods of this country become more expensive Real Depreciation

= f ( Y, Y*)") Real Exchange Rate and Trade Balance (X – IM) = f ( Y, Y*) The trade balance is a negative function of the real exchange rate and of our GDP, Y, finally, is a positive function of the GDP of our trade partners, Y*)

Real Exchange Rate and Trade Balance (X – IM) = f ( Y, Y*) The trade balance is a negative function of the real exchange rate and of our GDP, Y, finally, is a positive function of the GDP of our trade partners, Y*)

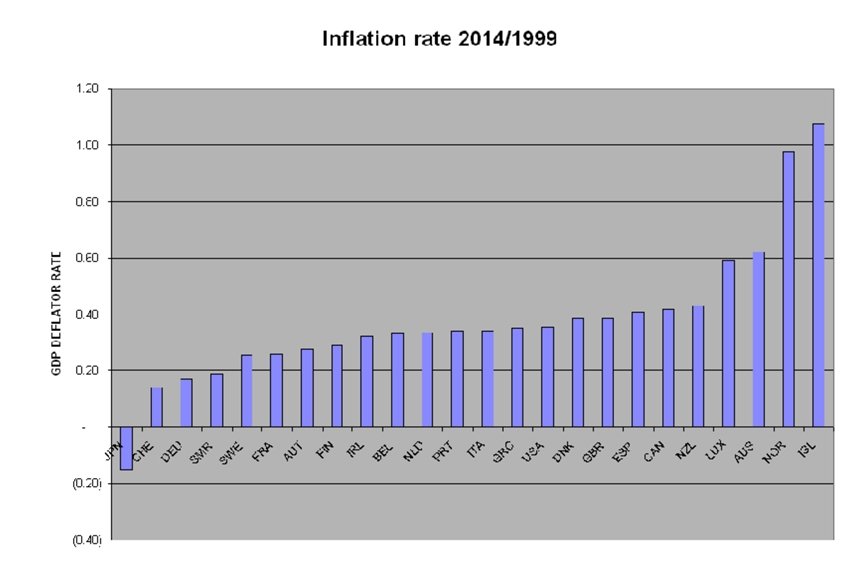

Price variation “Deflation” here indicates how much the 2014 value is smaller than the peak value in the considered period.

Price variation “Deflation” here indicates how much the 2014 value is smaller than the peak value in the considered period.

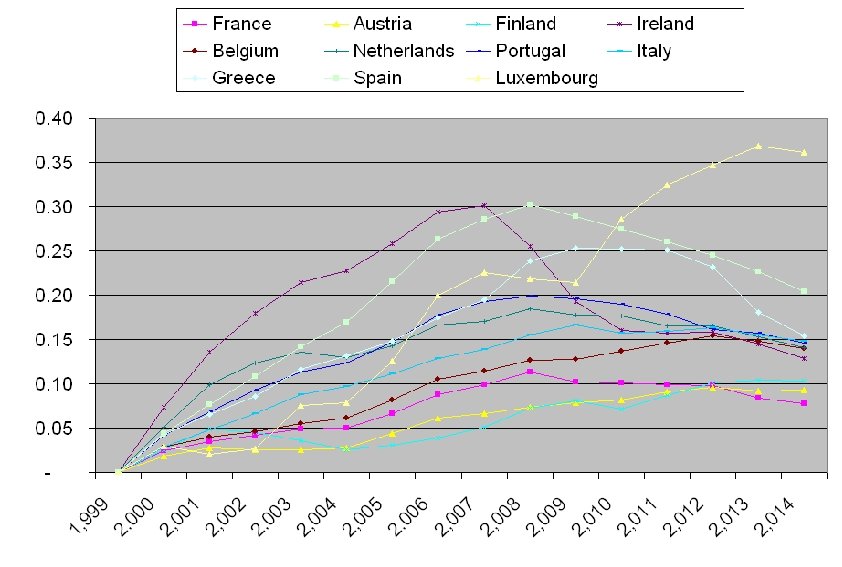

Real Exchange rate with Germany

Real Exchange rate with Germany

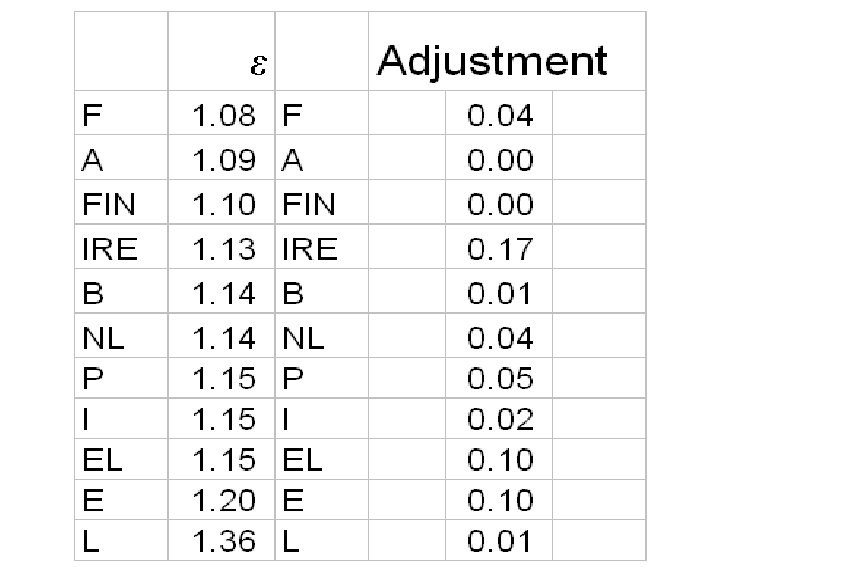

Adjustment: the difference of real exchange rate between peak year and 2014

Adjustment: the difference of real exchange rate between peak year and 2014

GGg Real Exchange Rate in 16 years of euro Percentage growth since 1999

GGg Real Exchange Rate in 16 years of euro Percentage growth since 1999

French Real exchange rate with Germany in 1999 = 1* 1 = 1 1

French Real exchange rate with Germany in 1999 = 1* 1 = 1 1

French Real exchange rate with Germany in 2014 = 1 * 1. 26 1. 17 = 1. 08 On average French goods have worsened their relative position with German goods by 8 % in 15 years

French Real exchange rate with Germany in 2014 = 1 * 1. 26 1. 17 = 1. 08 On average French goods have worsened their relative position with German goods by 8 % in 15 years

Open Economy: Investment, Budget surplus and Trade surplus Y ≡ C + I+ G + – IM + X …. . .

Open Economy: Investment, Budget surplus and Trade surplus Y ≡ C + I+ G + – IM + X …. . .

Open Economy: Investment, Budget surplus and Trade surplus Y ≡ C + I + G + – IM + X …. . . Y- C- T ≡ C –C + I + G –T – IM + X

Open Economy: Investment, Budget surplus and Trade surplus Y ≡ C + I + G + – IM + X …. . . Y- C- T ≡ C –C + I + G –T – IM + X

Open Economy: Investment, Budget surplus and Trade surplus Y ≡ C + I + G + – IM + X …. . . Y- C- T ≡ C –C + I + G –T – IM + X Savings ≡ + I + (G –T) + (– IM+X)

Open Economy: Investment, Budget surplus and Trade surplus Y ≡ C + I + G + – IM + X …. . . Y- C- T ≡ C –C + I + G –T – IM + X Savings ≡ + I + (G –T) + (– IM+X)

Open Economy: Investment, Budget surplus and Trade surplus Savings ≡ + I + (G –T) + (– IM+X) + Private Investment + Budget deficit + Trade Surplus = Domestic Private Savings

Open Economy: Investment, Budget surplus and Trade surplus Savings ≡ + I + (G –T) + (– IM+X) + Private Investment + Budget deficit + Trade Surplus = Domestic Private Savings

Open Economy: Investment, Budget surplus and Trade surplus Domestic Private Savings – = + Budget deficit + Private Investment Trade Surplus =

Open Economy: Investment, Budget surplus and Trade surplus Domestic Private Savings – = + Budget deficit + Private Investment Trade Surplus =

The End Thank You!

The End Thank You!