c9ca46d13543f48bcc78c9a73ef2c52c.ppt

- Количество слайдов: 31

Macro Review: BOP, Exchange Rates Jeffrey H. Nilsen http: //thedailyshow. cc. com/videos/zjr 96 n/julian-castro

assume BNB buys")

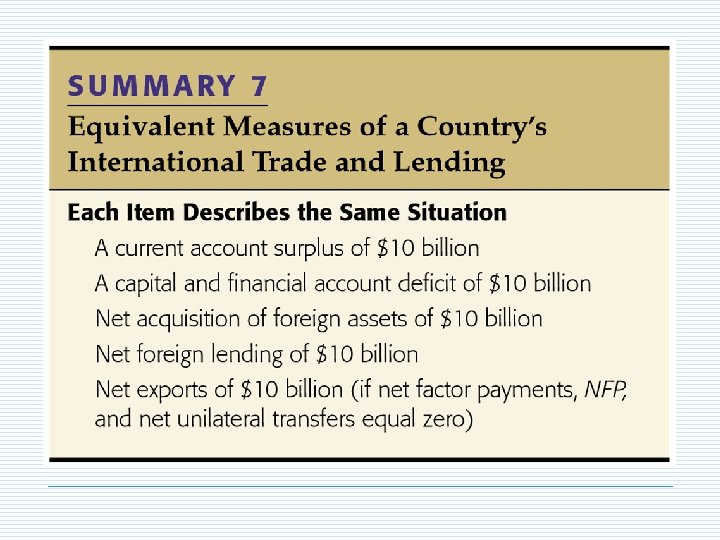

Balance of Payments Accounting (part of N. I. P. A. ) assume BNB buys & sells $ to ensure Lev won’t change (exchange rate “peg”) Count transaction as: CREDIT: in-flow of funds, + DEBIT: out-flow of funds, - Sell good to foreigners => credit (CA) Sell asset to foreigners => credit (private KFA) Sell ORA to foreigners => credit (public KFA, i. e. OSB)

Current Account o Accounts for trade in currently produced goods & services, includes n Net Exports n Net Factor Payments n Net unilateral transfers

CAUS as percentage of GDP

- 553. 5")

Table 5. 1 US BOP Accounts 2008 ($ Billions) - 553. 5

1998 -01 1998 -05 1998 -09 1999 -01 1999 -05 1999 -09 2000 -01 2000 -05 2000 -09 2001 -01 2001 -05 2001 -09 2002 -01 2002 -05 2002 -09 2003 -01 2003 -05 2003 -09 2004 -01 2004 -05 2004 -09 2005 -01 2005 -05 2005 -09 2006 -01 2006 -05 2006 -09 2007 -01 2007 -05 2007 -09 2008 -01 2008 -05 2008 -09 2009 -01 2009 -05 2009 -09 2010 -01 2010 -05 2010 -09 2011 -01 2011 -05 2011 -09 2012 -01 2012 -05 2012 -09 2013 -01 2013 -05 2013 -09 2014 -01 Current Account of Bulgaria (to 2014 Jan) 1000 500 0 Series 1 1998 -01 -57. 9 -500 -1000 -1500

KFA accounts for trade in existing real & financial")

Capital & Financial Account (KFA) KFA accounts for trade in existing real & financial assets, including ORA (official reserve assets) If sell domestic house, inflow => KFA credit If buy Boeing shares, outflow => KFA debit KFA Surplus if BG sells more assets to foreigners than they do to BG

Official Settlements Balance OSB = 0 if no intervention o OSB accounts for official purchase/sales of ORA ($, €, Yen, Renimbi, gold, special drawing rights) n Officials: BOK, Fed, ECB o NO intervention => BNB, Fed don’t buy/sell ORA n (the reason to intervene is to try to influence the exchange rate)

The OSB non-zero if Intervention BNB buys/sells ORA to influence euro per lev exchange rate If tends to appreciate : e. g. CA, private KFA > 0 (Germans want many Leva; BNB buys euro (ORA), selling leva (outflows) OSB DEBIT offsets CA + (private KFA credit) so finally CA + KFA = 0

Sell asset to")

US KFA . . Sell good to foreigners => credit (CA) Sell asset to foreigners => credit (KFA) Sell ORA to foreigners => credit (KFA) Fed buys ORA OSB, 2 parts (on net positive) SNB buys $ Swiss buy US houses KFA surplus CA deficit When the SNB buys $ from a Swiss person or bank : Private Swiss had bought US asset (US sold asset [Bo. PUS inflow]) So transfer to official account OSB (OSBUS inflow) 11

Emerging Market Volatility in early 2014 http: //video. ft. com/3111207196001/ Emerging-market-sell-off-spreadsacross-Asia/Markets

Media Attention on Possible Argentine Currency Crisis In 2014, many investors withdrew funds from emerging markets since expected higher US r; (have pesos want $ assets). Private outflows. To prevent peso from depreciating, Bank of Argentina sells $ for investors’ pesos BUT : continuing private KFA deficit may deplete BOA’s $ ORA (FX reserves) All nations are concerned with exchange rate, but those with pegs are more prone to problems; often Have CA, KFA deficits How much depreciation should central bank allow? ?

")

Reason for recent depreciation does Seems UNrelated to CA (in surplus for a decade)

Review Exchange Rates Plan o Nominal vs. real o PPP: absolute vs. relative o Determination of “fundamental exchange rate” where FX amount supplied = amount demanded o Peg en : over-valued vs. under-valued

Exchange Rates o Nominal: How much foreign currency you receive for 1 unit of home currency, e. g. 0. 50 € per 1 lev o Real (e. R): how many German goods you get for 1 BG good If mavrud costs 12 leva & same wine costs 5 euro in Germany, e. R = 1. 2 (German wine per bottle mavrud) Real exchange rate > 1: Consumers choose 1 Bulgarian vs. > 1 identical German goods

e. R rises")

Nominal depreciation: e. N falls (get fewer € for 1 lev) e. R rises (real appreciation) => Get more German wine for each case mavrud (so more difficult to sell mavrud in D)

o ABSOLUTE PURCHASING POWER PARITY (PPP) => assuming")

Purchasing Power Parity (long run influence) o ABSOLUTE PURCHASING POWER PARITY (PPP) => assuming free trade, identical goods: goods trade 1 -for-1 only => => (same price in $ ) n If doesn’t hold, pressure to return to PPP: o PBG or e. R falls due to unsold BG goods o or PDE rises due to high demand for German goods

")

Express absolute PPP as: PFor / P Pounds per $ (US domestic, UK foreign)

Relative PPP Instead ? o Absolute PPP does NOT hold because: n 1. services (especially) not subject to int’l competition; n 2. trade barriers don’t allow international P to equalize o Relative PPP: instead of er = 1, assume er constant over time o Relative PPP => e. N will appreciate to extent euro π > BG π

experience greater depreciation Lane (1999) What determines the")

Nations with higher inflation (vs. $) experience greater depreciation Lane (1999) What determines the nominal exchange rate, some cross sectional evidence. CJE

Finding Eqbm e. N FX Market o Leva. S: BG public supplies leva to get euro $ to buy Airbus Jets & VW shares High e. N: BG want lots of euro since German Goods are cheap Low e. N: BG wants few euro since German goods high cost o Leva. D: Germans demand Leva to buy Mavrud & real estate Low e. N: Germans want many Leva since Mavrud cheap

Quality of BG goods improves Lev demand")

FX Market Shifts Lev Supply (Lev appreciates) Quality of BG goods improves Lev demand Foreign interest Rate rise ? ?

Floating en & Policy o Float: en set by S & D IN ABSENCE OF central bank intervention o (zero OSB)

o Pure peg: the BNB commits to")

“Fixed” Exchange Rate Regime (e. g. Bulgaria) o Pure peg: the BNB commits to buy/sell € to maintain 0. 5 € per lev rate o Often not pure; even in float, national bank may intervene if believe currency overvalued (tough for exporters) e. g. Switzerland http: //video. ft. com/1145014411001/Swissie-pegdestabilising/Editors-Choice (Switzerland generally allows its Swiss Franc to float)

Important Issue in Pegs o Compare peg value to value that e would have without intervention (at fundamental value, where SFX = DFX ) o Undervalued peg may be strategy to increase exports o Overvalued peg may bring currency crisis Recall: policy changes in exchange rate are “revaluation” & “devalu

Undervalued Peg o e. PEG < efundamental o Low e. PEG => n American public buys many cheap Chinese goods, assets => Chinese CA, KFA both surplus n BUT EDYUAN: To maintain peg, PBo. C must sell yuan & buy $ (ORA) OSB debit Central Bank $ ↑ Y ↑ Result: PBo. C holds 2 trillion $

o e. PEG > e. FUND: CA, KFA deficit")

Overvalued Peg (Bulgaria pre-financial crisis) o e. PEG > e. FUND: CA, KFA deficit o Policy choices: n 1. Devalue to get to e. FUND n 2. e. g. tax IM to cut Lev. S (raising e. FUND) n 3. Soak up ESLEV: sell $, buy lev (must abandon peg if no more $ !!) Germans: Mavrud too costly Central Bank $ ↓ lev ↓ Cheap VW, D. assets

Speculative Attack o Germans fear lev assets lose value if BNB devalues At 0. 5 €/lev, share of Bulgartabak at 100 lev worth 50 € in Germany If BNB devalues to 0. 25€/lev => value drops to 25 € o Sell lev assets => lev. S shifts out o Fear makes ESLEV worse, BNB needs more $ to maintain overvalued peg => peg less sustainable

Compare Peg to Float o Peg cuts volatility and costs to trade. Disciplines M policy (limits BNB ability for discretionary M policy => lower π) o But float allows M policy to stabilize Y

c9ca46d13543f48bcc78c9a73ef2c52c.ppt