581ee966ab8d6d97774f10f6b2fdf484.ppt

- Количество слайдов: 17

June 2, 2008 Detecting Insider Trading MS&E 444 Final Presentation Manabu Kishimoto Xu Tian Li Xu

June 2, 2008 Detecting Insider Trading MS&E 444 Final Presentation Manabu Kishimoto Xu Tian Li Xu

Detecting") Overview • • • Motivation & Focus Litigation Case Study (CNS Inc. ) Detecting Strategy Automation and Optimization Performance Evaluation Conclusion

Overview • • • Motivation & Focus Litigation Case Study (CNS Inc. ) Detecting Strategy Automation and Optimization Performance Evaluation Conclusion

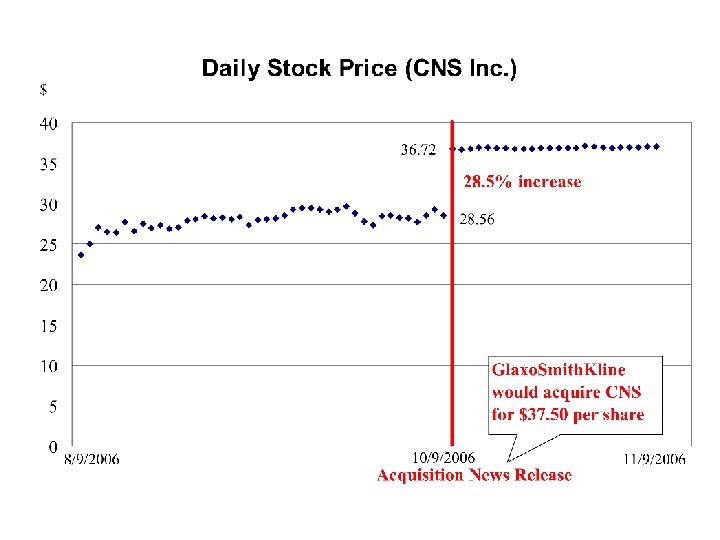

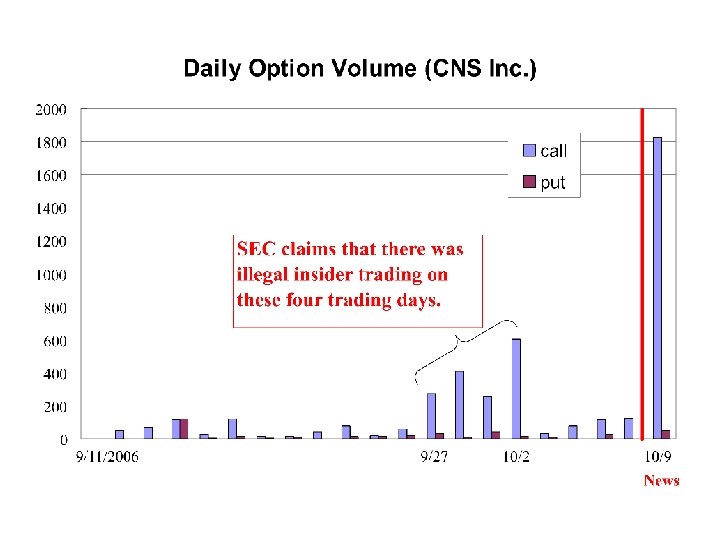

Motivation & Focus • If we can detect insider trading before the news release, we can generate excess returns. • In our project, we focus on the option market because – It gives leveraged return for insiders; – It is more thinly traded than the stock market; – It is more informative than the stock market. • We also focus on good news (e. g. Acquisition).

Motivation & Focus • If we can detect insider trading before the news release, we can generate excess returns. • In our project, we focus on the option market because – It gives leveraged return for insiders; – It is more thinly traded than the stock market; – It is more informative than the stock market. • We also focus on good news (e. g. Acquisition).

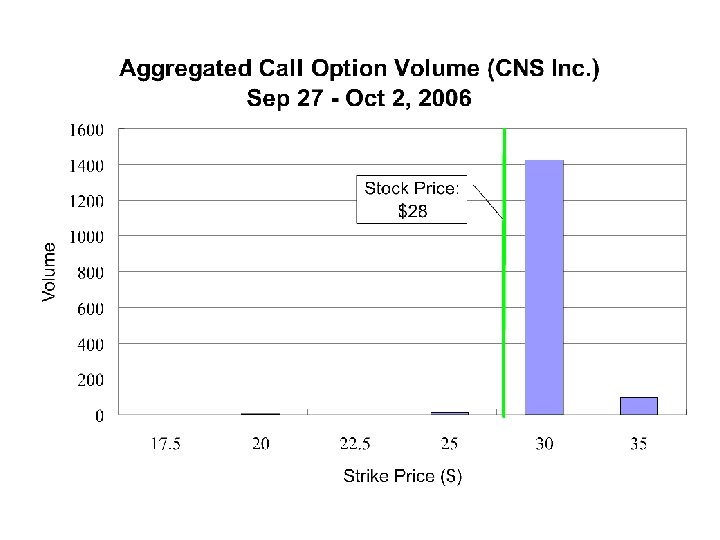

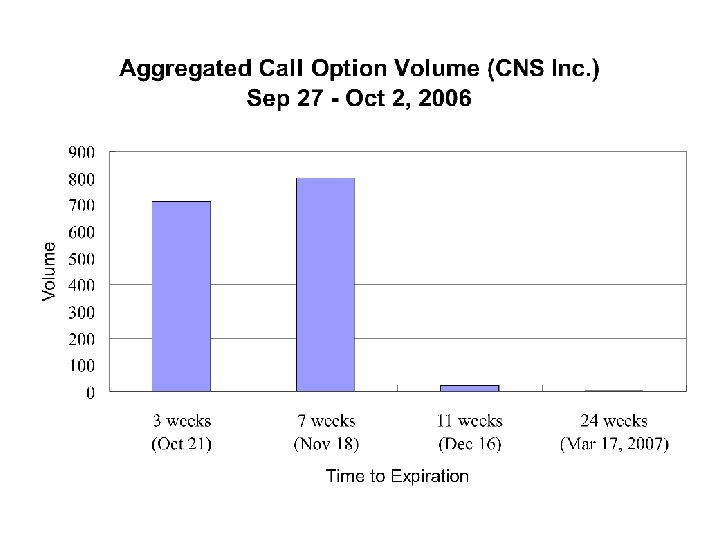

Salient Statistical Patterns 1. Call-put imbalance is large; 2. Total option volume is high; 3. Insiders prefer slightly in-the-money or out-of-the-money option; 4. Near-term option is preferred.

Salient Statistical Patterns 1. Call-put imbalance is large; 2. Total option volume is high; 3. Insiders prefer slightly in-the-money or out-of-the-money option; 4. Near-term option is preferred.

100 days Background • • 10 days Signal News? Insider? Use") Detecting Strategy (1) 100 days Background • • 10 days Signal News? Insider? Use moving windows: take 100 trading days as background data and 10 days as the signal Filter the data: focus on the data which satisfy the following two conditions: 1. Strike Price Filter Criterion Stock price – Strike price < +0. 15 Stock price 2. Expiration Date Filter Criterion Expiration date – Current date < 6 months

Detecting Strategy (1) 100 days Background • • 10 days Signal News? Insider? Use moving windows: take 100 trading days as background data and 10 days as the signal Filter the data: focus on the data which satisfy the following two conditions: 1. Strike Price Filter Criterion Stock price – Strike price < +0. 15 Stock price 2. Expiration Date Filter Criterion Expiration date – Current date < 6 months

100 days Background • 10 days Signal News? Insider? Apply the") Detecting Strategy (2) 100 days Background • 10 days Signal News? Insider? Apply the following criteria: 1. Call Ratio Criterion Call volume + Put volume > 75% 2. Total Volume Criterion Signal daily average volume Background daily average volume >1

Detecting Strategy (2) 100 days Background • 10 days Signal News? Insider? Apply the following criteria: 1. Call Ratio Criterion Call volume + Put volume > 75% 2. Total Volume Criterion Signal daily average volume Background daily average volume >1

• Optimize detection criteria • Use several benchmarks") Automation • Automatic processing script (PERL) • Optimize detection criteria • Use several benchmarks to evaluate the effectiveness of detection strategy Litigation Database CNXS, DJ, INVN Training Database Testing Database Event Database 2007 First Half Option. Metrics Database # of Tickers 3 99 3068 Year 2002/01 -2004/06 2005/01 -2007/06 2005/01/012007/06/30 2007/01/012007/06/30 # of events 15 474 1902

Automation • Automatic processing script (PERL) • Optimize detection criteria • Use several benchmarks to evaluate the effectiveness of detection strategy Litigation Database CNXS, DJ, INVN Training Database Testing Database Event Database 2007 First Half Option. Metrics Database # of Tickers 3 99 3068 Year 2002/01 -2004/06 2005/01 -2007/06 2005/01/012007/06/30 2007/01/012007/06/30 # of events 15 474 1902

Optimize Detection Criteria • Define: – Right Detection: stock price rallies ≥ 10% – Wrong Detection: stock price sinks ≥ 10% • Optimization on Training database – Optimize to maximize Right/Total Ratio – Optimize the criteria to maximize Right/Wrong Ratio • Change only one parameter at a time

Optimize Detection Criteria • Define: – Right Detection: stock price rallies ≥ 10% – Wrong Detection: stock price sinks ≥ 10% • Optimization on Training database – Optimize to maximize Right/Total Ratio – Optimize the criteria to maximize Right/Wrong Ratio • Change only one parameter at a time

Performance Evaluation Benchmark #1: Histogram of Stock Return • If we buy 1 share of stock when the signal suggests insider events, and sell it after holding it for 10 days, we obtained the histogram of the percentage return for all tickers in the database. Litigation Database Training Database Testing Database

Performance Evaluation Benchmark #1: Histogram of Stock Return • If we buy 1 share of stock when the signal suggests insider events, and sell it after holding it for 10 days, we obtained the histogram of the percentage return for all tickers in the database. Litigation Database Training Database Testing Database

Performance Evaluation Benchmark #2: Percentage Return of Non-leveraged Simple Trading Strategy • Non-leveraged Simple Trading Strategy (NSTS): – Allocate $1 for every ticker in the database – Check whethere is possible insider trading just before the market closes Yes: Use all balance allocated to buy shares of stocks and sell it after 10 days. No: Do nothing. – Calculate annualized percentage returns for all the funds allocated at the end of the period – Compare the return with the Buy-and-Hold strategy Litigation Database Training Database Testing Database NSTS Return +15% +5. 7% +7. 47% Buy and hold Return +39% (Acquisition rich) +28% (Acquisition rich) +2. 82%

Performance Evaluation Benchmark #2: Percentage Return of Non-leveraged Simple Trading Strategy • Non-leveraged Simple Trading Strategy (NSTS): – Allocate $1 for every ticker in the database – Check whethere is possible insider trading just before the market closes Yes: Use all balance allocated to buy shares of stocks and sell it after 10 days. No: Do nothing. – Calculate annualized percentage returns for all the funds allocated at the end of the period – Compare the return with the Buy-and-Hold strategy Litigation Database Training Database Testing Database NSTS Return +15% +5. 7% +7. 47% Buy and hold Return +39% (Acquisition rich) +28% (Acquisition rich) +2. 82%

Performance Evaluation Benchmark #3: Histogram of Signal’s Lead Time before the News Announcement Training Database Testing Database

Performance Evaluation Benchmark #3: Histogram of Signal’s Lead Time before the News Announcement Training Database Testing Database

Testing Training Litigation Performance Evaluation Benchmark #4: Prediction Errors # of events Detected? Yes No Yes 4 11 No 55 # of events Detected? Stock jump more than 5%? Yes No Yes 114 360 No 828 # of events Detected? Stock jump more than 5%? Yes No Yes 417 1485 No 18108

Testing Training Litigation Performance Evaluation Benchmark #4: Prediction Errors # of events Detected? Yes No Yes 4 11 No 55 # of events Detected? Stock jump more than 5%? Yes No Yes 114 360 No 828 # of events Detected? Stock jump more than 5%? Yes No Yes 417 1485 No 18108

Conclusion • There are salient statistical patterns of insider trading in the option market. 1. Call-put imbalance is large; 2. Total option volume is high; 3. Slightly in-the-money or out-of-the-money is preferred; 4. Near-term option is preferred. • By detecting insider trading before the news release, excess returns can be generated. - Based on 2007 data, Market return = + 2. 82% Our return = + 7. 47%

Conclusion • There are salient statistical patterns of insider trading in the option market. 1. Call-put imbalance is large; 2. Total option volume is high; 3. Slightly in-the-money or out-of-the-money is preferred; 4. Near-term option is preferred. • By detecting insider trading before the news release, excess returns can be generated. - Based on 2007 data, Market return = + 2. 82% Our return = + 7. 47%