9d40f0f20fe068221d27bb78be562953.ppt

- Количество слайдов: 72

Is accounting important to you? Yes, accounting is important in your personal life as well as your career, even though you may not become an accountant. For example, assume that you are the owner or manager of a small restaurant and are considering opening another restaurant in a neighboring town. Accounting information about the restaurant will be a major factor in your deciding whether to open the new restaurant and the bank’s deciding whether to finance the expansion. So our primary objective in this text is to illustrate basic accounting concepts that will help you to make good personal and business decision.

Is accounting important to you? Yes, accounting is important in your personal life as well as your career, even though you may not become an accountant. For example, assume that you are the owner or manager of a small restaurant and are considering opening another restaurant in a neighboring town. Accounting information about the restaurant will be a major factor in your deciding whether to open the new restaurant and the bank’s deciding whether to finance the expansion. So our primary objective in this text is to illustrate basic accounting concepts that will help you to make good personal and business decision.

Assets=Liabilities+Owner’s Equity +Revenues -Expenses

Assets=Liabilities+Owner’s Equity +Revenues -Expenses

This equation shows assets are equal to equities. Equities are divided into liabilities and capital (owner’s equity). When the amounts of any two of these elements (assets, liabilities or owner’s equity) are known, the third can be calculated. The followling are variations of the accounting equation: owner’s equity = assets - liabilities = assets - owner’s equity liabilities + owner’s equity = assets

This equation shows assets are equal to equities. Equities are divided into liabilities and capital (owner’s equity). When the amounts of any two of these elements (assets, liabilities or owner’s equity) are known, the third can be calculated. The followling are variations of the accounting equation: owner’s equity = assets - liabilities = assets - owner’s equity liabilities + owner’s equity = assets

Example 1

Example 1

The T-account form of an account is often very useful for illustration and analysis purposes because T accounts can be drawn so quickly. However, in practice, the account forms are much more structured. A form widely used in a manual system is illustrated below, using assumed data from the cash account of a certain company.

The T-account form of an account is often very useful for illustration and analysis purposes because T accounts can be drawn so quickly. However, in practice, the account forms are much more structured. A form widely used in a manual system is illustrated below, using assumed data from the cash account of a certain company.

5. 2 Journalizing The recording of transactions in the journal using the double-entry system is called journalizing. That is to record the entire business transaction in chronological order in the journal and embody all the necessary information and effects. Procedure of Journalizing Recording a business transaction in a journal (journalizing) includes two steps: (1) Analyze transactions form source documents. Source documents are the business papers that support the existence of business transactions. Source documents take the form of checks, invoices, bills etc. They are used as the basis of recording transactions. All information used in accounting must be evidenced by a source document that identifies the actual cost agreed upon by the buyer and the seller at the time of the transaction.

5. 2 Journalizing The recording of transactions in the journal using the double-entry system is called journalizing. That is to record the entire business transaction in chronological order in the journal and embody all the necessary information and effects. Procedure of Journalizing Recording a business transaction in a journal (journalizing) includes two steps: (1) Analyze transactions form source documents. Source documents are the business papers that support the existence of business transactions. Source documents take the form of checks, invoices, bills etc. They are used as the basis of recording transactions. All information used in accounting must be evidenced by a source document that identifies the actual cost agreed upon by the buyer and the seller at the time of the transaction.

Record transactions in a journal under the double-entry system. Business transactions will be") (2) Record transactions in a journal under the double-entry system. Business transactions will be recorded in the journal in chronological order. Here, we use the general journal. As is shown in the first table in 3. 1, the general journal consists of seven parts, which the recording or journalizing should fulfill: date; the account to be debited and the amount; the account to be credited and the amount; the posting reference to the General Ledger and page number. It is to notice that for each transaction, the debit account and its amount are entered first; the credit account and its amount are written below the debit portion.

(2) Record transactions in a journal under the double-entry system. Business transactions will be recorded in the journal in chronological order. Here, we use the general journal. As is shown in the first table in 3. 1, the general journal consists of seven parts, which the recording or journalizing should fulfill: date; the account to be debited and the amount; the account to be credited and the amount; the posting reference to the General Ledger and page number. It is to notice that for each transaction, the debit account and its amount are entered first; the credit account and its amount are written below the debit portion.

The following example, which shows how transactions are recorded, can help in understanding the operation of the general journal. Example 1 Journalize the transactions described for Mr. Drew`s law practice. During the month of January, Ted Drew, Lawyer Jan. 1 Invested $4, 000 to open his practice. 4 Bought supplies (stationery, forms, pencils, and so on) for cash, $300. 5 Bought office furniture from Robinson Furniture Company on account, $2, 000. 15 Received $2, 500 in fees earned during the mouth. 30 Paid office rent for January, $500.

The following example, which shows how transactions are recorded, can help in understanding the operation of the general journal. Example 1 Journalize the transactions described for Mr. Drew`s law practice. During the month of January, Ted Drew, Lawyer Jan. 1 Invested $4, 000 to open his practice. 4 Bought supplies (stationery, forms, pencils, and so on) for cash, $300. 5 Bought office furniture from Robinson Furniture Company on account, $2, 000. 15 Received $2, 500 in fees earned during the mouth. 30 Paid office rent for January, $500.

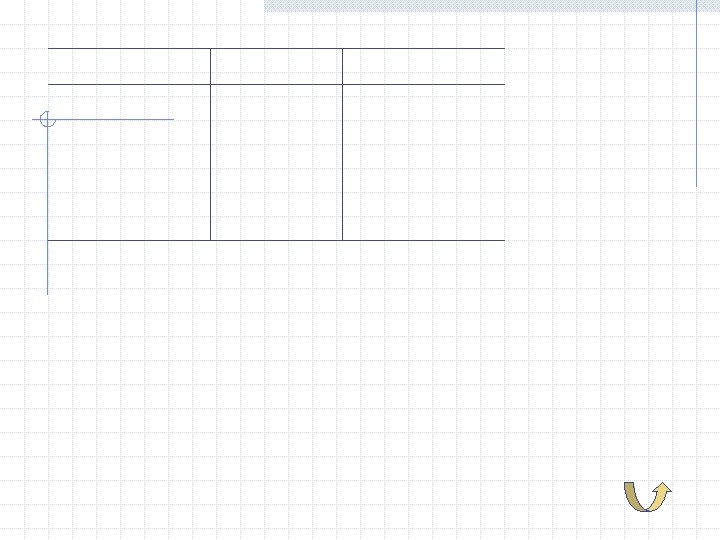

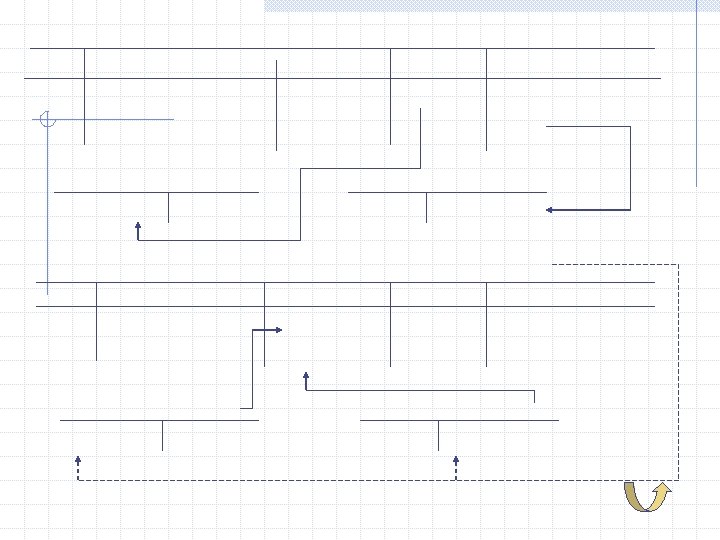

5. 3 Posting The process of transferring information from the journal to the ledger for the purpose of summarizing is called posting. Procedure of Posting is ordinarily carried out in the following steps: (1) Record the amount and date. The date and the amounts of the debits and credits are entered in the appropriate accounts. (2) Record the posting reference in the account. The number of the journal page is entered in the account (broken arrows below). (3) Record the posting in the journal. For crossreferencing, the code number of the account is now entered in the P. R. column of the journal (solid arrows). These numbers are called post reference or folio numbers.

5. 3 Posting The process of transferring information from the journal to the ledger for the purpose of summarizing is called posting. Procedure of Posting is ordinarily carried out in the following steps: (1) Record the amount and date. The date and the amounts of the debits and credits are entered in the appropriate accounts. (2) Record the posting reference in the account. The number of the journal page is entered in the account (broken arrows below). (3) Record the posting in the journal. For crossreferencing, the code number of the account is now entered in the P. R. column of the journal (solid arrows). These numbers are called post reference or folio numbers.

The close relationship of the income statement and the balance sheet is apparent. The net income of $1, 600 for January, shown as the final figure on the income statement of Example 1, is also shown as a separate figure in the balance sheet of Example 2. The income statement is thus the connecting link between two balance sheets. As discussed earlier, the income and expense items art actual a further analysis of the capital account. The balance sheet of Example 2 is arranged in report form, with the liabilities and capital sections shown below the asset section. It may also be arranged in account form, with the liabilities and capital sections to the right of, rather than below, the asset section, as shown in Example 3.

The close relationship of the income statement and the balance sheet is apparent. The net income of $1, 600 for January, shown as the final figure on the income statement of Example 1, is also shown as a separate figure in the balance sheet of Example 2. The income statement is thus the connecting link between two balance sheets. As discussed earlier, the income and expense items art actual a further analysis of the capital account. The balance sheet of Example 2 is arranged in report form, with the liabilities and capital sections shown below the asset section. It may also be arranged in account form, with the liabilities and capital sections to the right of, rather than below, the asset section, as shown in Example 3.