edc4e11608ffb21352e2f46a84c49577.ppt

- Количество слайдов: 85

INTERNATIONAL FINANCIAL MARKET & INTERNATIONAL MONETARY SYSTEM

INTERNATIONAL FINANCIAL MARKET & INTERNATIONAL MONETARY SYSTEM

Introduction • Fundamental difference between payment transactions • Domestic transaction—use only one curency • Foreign transaction—use two or more currencies • Foreign exchange— money denominated in the currency of another group of nations • Exchange rate—price of a currency • Number of units of one currency that buys one unit of another currency • Exchange rate can change daily 2

Introduction • Fundamental difference between payment transactions • Domestic transaction—use only one curency • Foreign transaction—use two or more currencies • Foreign exchange— money denominated in the currency of another group of nations • Exchange rate—price of a currency • Number of units of one currency that buys one unit of another currency • Exchange rate can change daily 2

• International financial market comprise of: – International Capital Market • Obtaining external financing. • Main purpose is to provide a mechanism through which those who wish to borrow or invest money can do so efficiently. – Foreign-Exchange Market—made up of: – over-the-counter (OTC) » commercial and investment banks » majority of foreign-exchange activity – security exchanges » trade certain types of foreign-exchange instruments

• International financial market comprise of: – International Capital Market • Obtaining external financing. • Main purpose is to provide a mechanism through which those who wish to borrow or invest money can do so efficiently. – Foreign-Exchange Market—made up of: – over-the-counter (OTC) » commercial and investment banks » majority of foreign-exchange activity – security exchanges » trade certain types of foreign-exchange instruments

Essential Terms • Security - a contract that can be assigned a value and traded (stocks, bonds, derivatives and other financial assets) • Stocks – A instrument representing ownership • Bonds - a debt agreement • Derivatives - the rights to ownership (financial instruments; futures, forwards, options, swaps)

Essential Terms • Security - a contract that can be assigned a value and traded (stocks, bonds, derivatives and other financial assets) • Stocks – A instrument representing ownership • Bonds - a debt agreement • Derivatives - the rights to ownership (financial instruments; futures, forwards, options, swaps)

Essential Terms II • Stock exchange, share market or bourse - is a corporation or mutual organization which provides facilities for stock brokers and traders, to trade company stocks and other securities • Over-the-counter (OTC) trading - is to trade financial instruments such as stocks, bonds, commodities or derivatives directly between two parties. It is contrasted with exchange trading, which occurs via corporate-owned facilities constructed for the purpose of trading (i. e. , exchanges), such as futures exchanges or stock exchanges.

Essential Terms II • Stock exchange, share market or bourse - is a corporation or mutual organization which provides facilities for stock brokers and traders, to trade company stocks and other securities • Over-the-counter (OTC) trading - is to trade financial instruments such as stocks, bonds, commodities or derivatives directly between two parties. It is contrasted with exchange trading, which occurs via corporate-owned facilities constructed for the purpose of trading (i. e. , exchanges), such as futures exchanges or stock exchanges.

Capital Market • System that allocates financial resources according to their most efficient uses • Common capital market intermediaries: • Commercial Banks • Investment Banks Debt: Repay principal plus interest Ø Bond has timed principal & interest payments Equity: Part ownership of a company Ø Stock shares in financial gains or losses

Capital Market • System that allocates financial resources according to their most efficient uses • Common capital market intermediaries: • Commercial Banks • Investment Banks Debt: Repay principal plus interest Ø Bond has timed principal & interest payments Equity: Part ownership of a company Ø Stock shares in financial gains or losses

Network of people, firms, financial institutions and governments borrowing and") International Capital Market (ICM) Network of people, firms, financial institutions and governments borrowing and investing internationally Purposes Borrowers Ø Expands money supply Ø Reduces cost of money Lenders Ø Spread / reduce risk Ø Offset gains / losses

International Capital Market (ICM) Network of people, firms, financial institutions and governments borrowing and investing internationally Purposes Borrowers Ø Expands money supply Ø Reduces cost of money Lenders Ø Spread / reduce risk Ø Offset gains / losses

") International Capital Market Drivers Information technology Deregulation Financial instruments (securitization)

International Capital Market Drivers Information technology Deregulation Financial instruments (securitization)

World Financial Centers • At present, the three main financial centers are London, New York and Tokyo • London is one of the three leading world financial centres. It is famous for its banks and Europe's largest stock exchange, that have been established over hundreds of years (e. g. Lloyd's of London, London Stock Exchange). The financial market of London is also commonly referred to as the City. It has historically been situated around the part of London called Square Mile, but in the 1980's and 1990's a large part of the City of London's wholesale financial services relocated to Canary Wharf.

World Financial Centers • At present, the three main financial centers are London, New York and Tokyo • London is one of the three leading world financial centres. It is famous for its banks and Europe's largest stock exchange, that have been established over hundreds of years (e. g. Lloyd's of London, London Stock Exchange). The financial market of London is also commonly referred to as the City. It has historically been situated around the part of London called Square Mile, but in the 1980's and 1990's a large part of the City of London's wholesale financial services relocated to Canary Wharf.

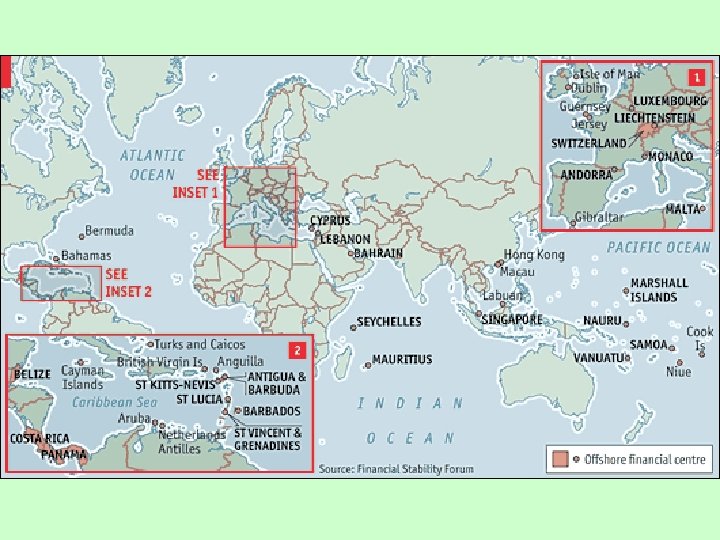

Offshore Financial Centers Operational center Extensive financial activity and currency trading Country or territory whose financial sector features few regulations and few, if any, taxes Booking center Mostly for bookkeeping and tax purposes

Offshore Financial Centers Operational center Extensive financial activity and currency trading Country or territory whose financial sector features few regulations and few, if any, taxes Booking center Mostly for bookkeeping and tax purposes

IMF defines OFC as: • Jurisdictions that have relatively large numbers of financial institutions engaged primarily in business with non-residents; • Financial systems with external assets and liabilities out of proportion to domestic financial intermediation designed to finance domestic economies; and • More popularly, centers which provide some or all of the following services: low or zero taxation; moderate or light financial regulation; banking secrecy and anonymity.

IMF defines OFC as: • Jurisdictions that have relatively large numbers of financial institutions engaged primarily in business with non-residents; • Financial systems with external assets and liabilities out of proportion to domestic financial intermediation designed to finance domestic economies; and • More popularly, centers which provide some or all of the following services: low or zero taxation; moderate or light financial regulation; banking secrecy and anonymity.

Main Components of ICM: International Bond Market of bonds sold by issuing companies, governments and others outside their own countries Eurobond Foreign bond Interest rates Bond that is issued outside the country in whose currency the bond is denominated Bond sold outside a borrower’s country and denominated in the currency of the country in which it is sold Driving growth are differential interest rates between developed and developing nations

Main Components of ICM: International Bond Market of bonds sold by issuing companies, governments and others outside their own countries Eurobond Foreign bond Interest rates Bond that is issued outside the country in whose currency the bond is denominated Bond sold outside a borrower’s country and denominated in the currency of the country in which it is sold Driving growth are differential interest rates between developed and developing nations

International Equity Market of stocks bought and sold outside the issuer’s home country Factors contributing towards growth: • Spread of Privatization • Economic Growth in Developing Countries • Activities of Investment Banks • Advent of Cybermarkets

International Equity Market of stocks bought and sold outside the issuer’s home country Factors contributing towards growth: • Spread of Privatization • Economic Growth in Developing Countries • Activities of Investment Banks • Advent of Cybermarkets

Eurocurrency Market Unregulated market of currencies banked outside their countries of origin Ø Ø Governments Commercial banks International companies Wealthy individuals

Eurocurrency Market Unregulated market of currencies banked outside their countries of origin Ø Ø Governments Commercial banks International companies Wealthy individuals

Foreign Exchange Market Introduction • Foreign exchange market: a market for converting the currency of one country into the currency of another. • Exchange rate: the rate at which one currency is converted into another • Foreign exchange risk: the risk that arises from changes in exchange rates

Foreign Exchange Market Introduction • Foreign exchange market: a market for converting the currency of one country into the currency of another. • Exchange rate: the rate at which one currency is converted into another • Foreign exchange risk: the risk that arises from changes in exchange rates

Foreign Exchange Market in which currencies are bought and sold and their prices are determined ü Conversion: To facilitate sale or purchase, or invest directly abroad ü Hedging: Insure against potential losses from adverse exchange-rate changes ü Arbitrage: Instantaneous purchase and sale of a currency in different markets for profit ü Speculation: Sequential purchase and sale (or vice-versa) of a currency for profit

Foreign Exchange Market in which currencies are bought and sold and their prices are determined ü Conversion: To facilitate sale or purchase, or invest directly abroad ü Hedging: Insure against potential losses from adverse exchange-rate changes ü Arbitrage: Instantaneous purchase and sale of a currency in different markets for profit ü Speculation: Sequential purchase and sale (or vice-versa) of a currency for profit

The Functions of the Foreign Exchange Market • The foreign exchange market serves two main functions: – Convert the currency of one country into the currency of another – Provide some insurance against foreign exchange risk • Foreign exchange risk: the adverse consequences of unpredictable changes in the exchange rates

The Functions of the Foreign Exchange Market • The foreign exchange market serves two main functions: – Convert the currency of one country into the currency of another – Provide some insurance against foreign exchange risk • Foreign exchange risk: the adverse consequences of unpredictable changes in the exchange rates

Currency Conversion • Consumers can compare the relative prices of goods and services in different countries using exchange rates • International business have four main uses of foreign exchange markets • To exchange currency received in the course of doing business abroad back into the currency of its home country • To pay a foreign company for its products or services in its country’s currency • • To invest excess cash for short terms in foreign markets To profit from the short-term movement of funds from one currency to another in the hopes of profiting from shifts in exchange rates, also called currency speculation

Currency Conversion • Consumers can compare the relative prices of goods and services in different countries using exchange rates • International business have four main uses of foreign exchange markets • To exchange currency received in the course of doing business abroad back into the currency of its home country • To pay a foreign company for its products or services in its country’s currency • • To invest excess cash for short terms in foreign markets To profit from the short-term movement of funds from one currency to another in the hopes of profiting from shifts in exchange rates, also called currency speculation

Insuring against Foreign Exchange Risk • A spot exchange occurs when two parties agree to exchange currency and execute the deal immediately • The spot exchange rate is the rate at which a foreign exchange dealer converts one currency into another currency on a particular day – Reported daily – Change continually

Insuring against Foreign Exchange Risk • A spot exchange occurs when two parties agree to exchange currency and execute the deal immediately • The spot exchange rate is the rate at which a foreign exchange dealer converts one currency into another currency on a particular day – Reported daily – Change continually

Insuring against Foreign Exchange Risk • Forward exchanges occur when two parties agree to exchange currency and execute the deal at some specific date in the future – Exchange rates governing such future transactions are referred to as forward exchange rates – For most major currencies, forward exchange rates are quoted for 30 days, 90 days, and 180 days into the future • When a firm enters into a forward exchange contract, it is taking out insurance against the possibility that future exchange rate movements will make a transaction unprofitable by the time that transaction has been executed

Insuring against Foreign Exchange Risk • Forward exchanges occur when two parties agree to exchange currency and execute the deal at some specific date in the future – Exchange rates governing such future transactions are referred to as forward exchange rates – For most major currencies, forward exchange rates are quoted for 30 days, 90 days, and 180 days into the future • When a firm enters into a forward exchange contract, it is taking out insurance against the possibility that future exchange rate movements will make a transaction unprofitable by the time that transaction has been executed

Insuring against Foreign Exchange Risk • Currency swap: the simultaneous purchase and sale of a given amount of foreign exchange for two different value dates • Swaps are transacted between international businesses and their banks, between banks, and between governments when it is desirable to move out of one currency into another for a limited period without incurring foreign exchange risk

Insuring against Foreign Exchange Risk • Currency swap: the simultaneous purchase and sale of a given amount of foreign exchange for two different value dates • Swaps are transacted between international businesses and their banks, between banks, and between governments when it is desirable to move out of one currency into another for a limited period without incurring foreign exchange risk

The Nature of the Foreign Exchange Market • The foreign exchange market is a global network of banks, brokers and foreign exchange dealers connected by electronic communications systems • The most important trading centers include: London, New York, Tokyo, and Singapore • London’s dominance is explained by: – History (capital of the first major industrialized nation) – Geography (between Tokyo/Singapore and New York) • Two major features of the foreign exchange market: – The market never sleeps – Market is highly integrated

The Nature of the Foreign Exchange Market • The foreign exchange market is a global network of banks, brokers and foreign exchange dealers connected by electronic communications systems • The most important trading centers include: London, New York, Tokyo, and Singapore • London’s dominance is explained by: – History (capital of the first major industrialized nation) – Geography (between Tokyo/Singapore and New York) • Two major features of the foreign exchange market: – The market never sleeps – Market is highly integrated

Institutions of Foreign Exchange Market • Interbank Market: market in which the world’s largest banks exchange currencies at spot and forward rates. – “Clearing mechanism” • Securities Exchanges: exchange specializing in currency futures and options transactions. • Over-the-Counter Market: Exchange consisting of a global computer network of foreign exchange traders and other market participants.

Institutions of Foreign Exchange Market • Interbank Market: market in which the world’s largest banks exchange currencies at spot and forward rates. – “Clearing mechanism” • Securities Exchanges: exchange specializing in currency futures and options transactions. • Over-the-Counter Market: Exchange consisting of a global computer network of foreign exchange traders and other market participants.

The Foreign-Exchange Market Size of foreign-exchange market $600 billion spot $1. 3 trillion in derivatives, ie $200 billion in outright forwards $1 trillion in forex swaps $100 billion in FX options. (2004) U. S. dollar is the most important currency because it is: • An investment currency in many capital markets • A reserve currency held by many central banks • A transaction currency in many international commodity markets • An invoice currency in many contracts • An intervention currency employed by monetary authorities to influence their exchange rates 25

The Foreign-Exchange Market Size of foreign-exchange market $600 billion spot $1. 3 trillion in derivatives, ie $200 billion in outright forwards $1 trillion in forex swaps $100 billion in FX options. (2004) U. S. dollar is the most important currency because it is: • An investment currency in many capital markets • A reserve currency held by many central banks • A transaction currency in many international commodity markets • An invoice currency in many contracts • An intervention currency employed by monetary authorities to influence their exchange rates 25

Trends in Foreign-Exchange Trading 9 -7

Trends in Foreign-Exchange Trading 9 -7

= Japanese yen") Quoting Currencies Quoted currency = numerator Base currency = denominator (¥/$) = Japanese yen needed to buy one U. S. dollar Yen is quoted currency, dollar is base currency

Quoting Currencies Quoted currency = numerator Base currency = denominator (¥/$) = Japanese yen needed to buy one U. S. dollar Yen is quoted currency, dollar is base currency

Currency Values Change in US dollar against Polish zloty Change in Polish zloty against US dollar February 1: PLZ 5/$ March 1: PLZ 4/$ Make zloty base currency (1÷ PLZ/$) February 1: $. 20/PLZ March 1: $. 25/PLZ %change = [(4 -5)/5] x 100 = -20% %change = [(. 25 -. 20)/. 20] x 100 = 25% US dollar fell 20% Polish zloty rose 25%

Currency Values Change in US dollar against Polish zloty Change in Polish zloty against US dollar February 1: PLZ 5/$ March 1: PLZ 4/$ Make zloty base currency (1÷ PLZ/$) February 1: $. 20/PLZ March 1: $. 25/PLZ %change = [(4 -5)/5] x 100 = -20% %change = [(. 25 -. 20)/. 20] x 100 = 25% US dollar fell 20% Polish zloty rose 25%

Cross Rate • Exchange rate calculated using two other exchange rates • Use direct or indirect exchange rates against a third currency

Cross Rate • Exchange rate calculated using two other exchange rates • Use direct or indirect exchange rates against a third currency

2) 3) 4) Quote on euro =") Cross Rate Example Direct quote method 1) 2) 3) 4) Quote on euro = € 0. 8461/$ Quote on yen = ¥ 114. 50/$ € 0. 8461/$ ÷ ¥ 114. 50/$ = € 0. 0074/¥ Costs 0. 0074 euros to buy 1 yen Indirect quote method 1) 2) 3) 4) 5) Quote on euro = $ 1. 1819/€ Quote on yen = $ 0. 008734/¥ $ 1. 1819/€ ÷ $ 0. 008734/¥ = € 135. 32/¥ Final step: 1 ÷ € 135. 32/¥ = € 0. 0074/¥ Costs 0. 0074 euros to buy 1 yen

Cross Rate Example Direct quote method 1) 2) 3) 4) Quote on euro = € 0. 8461/$ Quote on yen = ¥ 114. 50/$ € 0. 8461/$ ÷ ¥ 114. 50/$ = € 0. 0074/¥ Costs 0. 0074 euros to buy 1 yen Indirect quote method 1) 2) 3) 4) 5) Quote on euro = $ 1. 1819/€ Quote on yen = $ 0. 008734/¥ $ 1. 1819/€ ÷ $ 0. 008734/¥ = € 135. 32/¥ Final step: 1 ÷ € 135. 32/¥ = € 0. 0074/¥ Costs 0. 0074 euros to buy 1 yen

Currency Convertibility • Governments can place restrictions on the convertibility of currency – A country’s currency is said to be freely convertible when the country’s government allows both residents and nonresidents to purchase unlimited amounts of a foreign currency with it – A currency is said to be externally convertible when only nonresidents may convert it into a foreign currency without any limitations – A currency is nonconvertible when neither residents nor nonresidents are allowed to convert it into a foreign currency

Currency Convertibility • Governments can place restrictions on the convertibility of currency – A country’s currency is said to be freely convertible when the country’s government allows both residents and nonresidents to purchase unlimited amounts of a foreign currency with it – A currency is said to be externally convertible when only nonresidents may convert it into a foreign currency without any limitations – A currency is nonconvertible when neither residents nor nonresidents are allowed to convert it into a foreign currency

• Government restrictions can include – A restriction on residents’ ability to convert the domestic currency into a foreign currency – Restricting domestic businesses’ ability to take foreign currency out of the country • Governments will limit or restrict convertibility for a number of reasons that include: – Preserving foreign exchange reserves – A fear that free convertibility will lead to a run on their foreign exchange reserves – known as capital flight

• Government restrictions can include – A restriction on residents’ ability to convert the domestic currency into a foreign currency – Restricting domestic businesses’ ability to take foreign currency out of the country • Governments will limit or restrict convertibility for a number of reasons that include: – Preserving foreign exchange reserves – A fear that free convertibility will lead to a run on their foreign exchange reserves – known as capital flight

Governmental Restrictions on Foreign-Exchange Convertibility Restrictions used to conserve scarce foreign exchange • Licensing—government regulates all foreign-exchange transactions – those who receive foreign currency required to sell it to its central bank at the official buying rate – central bank rations foreign currency • Multiple exchange-rate system—different exchange rates set for different transactions • Advance import deposit—requires importers to make a deposit with central bank covering price of goods they would purchase from abroad • Quantity controls—limit the amount of currency that resident can purchase foreign travel Currency controls increase the cost of international business and reduce overall international trade 33

Governmental Restrictions on Foreign-Exchange Convertibility Restrictions used to conserve scarce foreign exchange • Licensing—government regulates all foreign-exchange transactions – those who receive foreign currency required to sell it to its central bank at the official buying rate – central bank rations foreign currency • Multiple exchange-rate system—different exchange rates set for different transactions • Advance import deposit—requires importers to make a deposit with central bank covering price of goods they would purchase from abroad • Quantity controls—limit the amount of currency that resident can purchase foreign travel Currency controls increase the cost of international business and reduce overall international trade 33

How Companies Use Foreign Exchange Most foreign-exchange transactions involve international departments of commercial banks • Banks buy and sell foreign currency; banks collect and pay money in transaction with foreign buyers and sellers • Banks lend money in foreign currency Companies use foreign-exchange market for: • Import and export transactions • Financial transactions such as FDI Arbitrage—purchase of foreign currency on one market for immediate resale on another market • Arbitragers hope to profit from price discrepancy • Interest arbitrage—investing in debt instruments in different countries Speculation—buying or selling foreign currency has both risk and high profit potential 34

How Companies Use Foreign Exchange Most foreign-exchange transactions involve international departments of commercial banks • Banks buy and sell foreign currency; banks collect and pay money in transaction with foreign buyers and sellers • Banks lend money in foreign currency Companies use foreign-exchange market for: • Import and export transactions • Financial transactions such as FDI Arbitrage—purchase of foreign currency on one market for immediate resale on another market • Arbitragers hope to profit from price discrepancy • Interest arbitrage—investing in debt instruments in different countries Speculation—buying or selling foreign currency has both risk and high profit potential 34

Foreign-Exchange Trading Process Companies work through their local banks to settle foreign-exchange balances • Commercial banks in major money centers became intermediaries for small banks Most foreign-exchange activity takes place in traditional instruments • Commercial and investment banks and other financial institutions handle spot, outright forward, and FX swaps • Foreign-exchange market made up of about 2, 000 dealer institutions worldwide • Most foreign-exchange takes place in OTC market Dealers can trade foreign exchange: • Directly with other dealers • Through voice brokers • Through electronic brokerage systems – Internet trades of currency are more popular 35

Foreign-Exchange Trading Process Companies work through their local banks to settle foreign-exchange balances • Commercial banks in major money centers became intermediaries for small banks Most foreign-exchange activity takes place in traditional instruments • Commercial and investment banks and other financial institutions handle spot, outright forward, and FX swaps • Foreign-exchange market made up of about 2, 000 dealer institutions worldwide • Most foreign-exchange takes place in OTC market Dealers can trade foreign exchange: • Directly with other dealers • Through voice brokers • Through electronic brokerage systems – Internet trades of currency are more popular 35

Commercial and Investment Banks Greatest volume of foreign-exchange activity takes place with the big banks • Top banks in the interbank market in foreign exchange are so ranked because of their ability to: – trade in specific market locations – engage in major currencies and cross-trades – deal in specific currencies – handle derivatives » forwards, options, future swaps – conduct key market research • Banks may specialize in geographic areas, instruments, or currencies – exotic currency—currency of a developing country » often unstable, weak, and unpredictable 36

Commercial and Investment Banks Greatest volume of foreign-exchange activity takes place with the big banks • Top banks in the interbank market in foreign exchange are so ranked because of their ability to: – trade in specific market locations – engage in major currencies and cross-trades – deal in specific currencies – handle derivatives » forwards, options, future swaps – conduct key market research • Banks may specialize in geographic areas, instruments, or currencies – exotic currency—currency of a developing country » often unstable, weak, and unpredictable 36

Rank 1 2") Top 10 Currency Traders (% of overall volume, May 2005 ) Rank 1 2 3 Name Deutsche Bank UBS Citigroup % of volume 17. 0 12. 5 7. 5 4 5 6 7 8 9 10 HSBC Barclays Merrill Lynch J. P. Morgan Chase Goldman Sachs ABN AMRO Morgan Stanley 6. 4 5. 9 5. 7 5. 3 4. 4 4. 2 3. 9

Top 10 Currency Traders (% of overall volume, May 2005 ) Rank 1 2 3 Name Deutsche Bank UBS Citigroup % of volume 17. 0 12. 5 7. 5 4 5 6 7 8 9 10 HSBC Barclays Merrill Lynch J. P. Morgan Chase Goldman Sachs ABN AMRO Morgan Stanley 6. 4 5. 9 5. 7 5. 3 4. 4 4. 2 3. 9

International Monetary System • Rules and procedures by which different national currencies are exchanged for each other in world trade. • Such a system is necessary to define a common standard of value for the world's currencies. • Refer to the institutional arrangements that countries adopt to govern exchange rates – – Floating Pegged exchange rate Dirty float Fixed exchange rate

International Monetary System • Rules and procedures by which different national currencies are exchanged for each other in world trade. • Such a system is necessary to define a common standard of value for the world's currencies. • Refer to the institutional arrangements that countries adopt to govern exchange rates – – Floating Pegged exchange rate Dirty float Fixed exchange rate

• Floating exchange rates occur when the foreign exchange market determines the relative value of a currency • The world’s four major currencies – dollar, euro, yen, and pound – are all free to float against each other • Pegged exchange rates occur when the value of a currency is fixed relative to a reference currency

• Floating exchange rates occur when the foreign exchange market determines the relative value of a currency • The world’s four major currencies – dollar, euro, yen, and pound – are all free to float against each other • Pegged exchange rates occur when the value of a currency is fixed relative to a reference currency

• Dirty float occurs when countries hold the value of their currency within a range of a reference currency • Fixed exchange rate occurs when a set of currencies are fixed against each other at some mutually agreed upon exchange rate • Pegged exchange rates, dirty floats and fixed exchange rates all require some degree of government intervention

• Dirty float occurs when countries hold the value of their currency within a range of a reference currency • Fixed exchange rate occurs when a set of currencies are fixed against each other at some mutually agreed upon exchange rate • Pegged exchange rates, dirty floats and fixed exchange rates all require some degree of government intervention

Evolution of International Monetary System The Gold Standard - In place from 1700 s to 1939 - a monetary standard that pegs currencies to gold and guarantees convertibility to gold - It was thought that gold standard contained an automatic mechanism that contributed to the simultaneous achievement of a balance-ofpayments equilibrium by all countries. - The gold standard broke down during the 1930 s as countries engaged in competitive devaluations

Evolution of International Monetary System The Gold Standard - In place from 1700 s to 1939 - a monetary standard that pegs currencies to gold and guarantees convertibility to gold - It was thought that gold standard contained an automatic mechanism that contributed to the simultaneous achievement of a balance-ofpayments equilibrium by all countries. - The gold standard broke down during the 1930 s as countries engaged in competitive devaluations

The Gold Standard e ad Tr • Roots in old mercantile trade • Inconvenient to ship gold, changed to paper- redeemable for gold • Want to achieve ‘balance-of-trade equilibrium Japan Go ld USA

The Gold Standard e ad Tr • Roots in old mercantile trade • Inconvenient to ship gold, changed to paper- redeemable for gold • Want to achieve ‘balance-of-trade equilibrium Japan Go ld USA

Balance of Trade Equilibrium Decreased money supply = price decline. Trade Surplus As prices decline, exports increase and trade goes into equilibrium. Gold Increased money supply = price inflation.

Balance of Trade Equilibrium Decreased money supply = price decline. Trade Surplus As prices decline, exports increase and trade goes into equilibrium. Gold Increased money supply = price inflation.

Between the Wars • Post WWI, war heavy expenditures affected the value of dollars against gold • US raised dollars to gold from $20. 67 to $35 per ounce – Dollar worth less? • Other countries followed suit and devalued their currencies

Between the Wars • Post WWI, war heavy expenditures affected the value of dollars against gold • US raised dollars to gold from $20. 67 to $35 per ounce – Dollar worth less? • Other countries followed suit and devalued their currencies

Bretton Woods • In 1944, 44 countries met in New Hampshire • Countries agreed to peg their currencies to US$ which was convertible to gold at $35/oz • Agreed not to engage in competitive devaluations for trade purposes and defend their currencies • Weak currencies could be devalued up to 10% w/o approval • Created the IMF and World Bank

Bretton Woods • In 1944, 44 countries met in New Hampshire • Countries agreed to peg their currencies to US$ which was convertible to gold at $35/oz • Agreed not to engage in competitive devaluations for trade purposes and defend their currencies • Weak currencies could be devalued up to 10% w/o approval • Created the IMF and World Bank

Articles of Agreement were heavily") International Monetary Fund • The International Monetary Fund (IMF) Articles of Agreement were heavily influenced by the worldwide financial collapse, competitive devaluations, trade wars, high unemployment, hyperinflation in Germany and elsewhere, and general economic disintegration that occurred between the two world wars • The aim of the IMF was to try to avoid a repetition of that chaos through a combination of discipline and flexibility

International Monetary Fund • The International Monetary Fund (IMF) Articles of Agreement were heavily influenced by the worldwide financial collapse, competitive devaluations, trade wars, high unemployment, hyperinflation in Germany and elsewhere, and general economic disintegration that occurred between the two world wars • The aim of the IMF was to try to avoid a repetition of that chaos through a combination of discipline and flexibility

International Monetary Fund • Discipline – Maintaining a fixed exchange rate imposes monetary discipline, curtails inflation – Brake on competitive devaluations and stability to the world trade environment • Flexibility – Lending facility: • Lend foreign currencies to countries having balance-of-payments problems – Adjustable parities: • Allow countries to devalue currencies more than 10% if balance of payments was in “fundamental disequilibrium”

International Monetary Fund • Discipline – Maintaining a fixed exchange rate imposes monetary discipline, curtails inflation – Brake on competitive devaluations and stability to the world trade environment • Flexibility – Lending facility: • Lend foreign currencies to countries having balance-of-payments problems – Adjustable parities: • Allow countries to devalue currencies more than 10% if balance of payments was in “fundamental disequilibrium”

Purposes of IMF • Promoting international monetary cooperation • Facilitating expansion and balanced growth of international trade • Promoting exchange stability, maintaining orderly exchange arrangements, and avoiding competitive exchange devaluation • Making the resources of the Fund temporarily available to members • Shortening the duration and lessening the degree of disequilibrium in the international balance of payments of member nations

Purposes of IMF • Promoting international monetary cooperation • Facilitating expansion and balanced growth of international trade • Promoting exchange stability, maintaining orderly exchange arrangements, and avoiding competitive exchange devaluation • Making the resources of the Fund temporarily available to members • Shortening the duration and lessening the degree of disequilibrium in the international balance of payments of member nations

To serve these purposes, the IMF: • monitors economic and financial developments and policies, in member countries and at the global level, and gives policy advice to its members based on its more than fifty years of experience. • For example: In its annual review of the Japanese economy for 2003, the IMF Executive Board urged Japan to adopt a comprehensive approach to revitalize the corporate and financial sectors of its economy, tackle deflation, and address fiscal imbalances.

To serve these purposes, the IMF: • monitors economic and financial developments and policies, in member countries and at the global level, and gives policy advice to its members based on its more than fifty years of experience. • For example: In its annual review of the Japanese economy for 2003, the IMF Executive Board urged Japan to adopt a comprehensive approach to revitalize the corporate and financial sectors of its economy, tackle deflation, and address fiscal imbalances.

• The IMF commended Mexico in 2003 for good economic management, but said structural reform of the tax system, energy sector, the labor market, and judicial system was needed to help the country compete in the global economy. • In its Spring 2004 World Economic Outlook, the IMF said an orderly resolution of global imbalances, notably the large U. S. current account deficit and surpluses elsewhere, was needed as the global economy recovered and moved toward higher interest rates.

• The IMF commended Mexico in 2003 for good economic management, but said structural reform of the tax system, energy sector, the labor market, and judicial system was needed to help the country compete in the global economy. • In its Spring 2004 World Economic Outlook, the IMF said an orderly resolution of global imbalances, notably the large U. S. current account deficit and surpluses elsewhere, was needed as the global economy recovered and moved toward higher interest rates.

• lends to member countries with balance of payments problems, not just to provide temporary financing but to support adjustment and reform policies aimed at correcting the underlying problems. • For example: During the 1997 -98 Asian financial crisis, the IMF acted swiftly to help Korea bolster its reserves. It pledged $21 billion to assist Korea to reform its economy, restructure its financial and corporate sectors, and recover from recession. Within four years, Korea had recovered sufficiently to repay the loans and, at the same time, rebuild its reserves.

• lends to member countries with balance of payments problems, not just to provide temporary financing but to support adjustment and reform policies aimed at correcting the underlying problems. • For example: During the 1997 -98 Asian financial crisis, the IMF acted swiftly to help Korea bolster its reserves. It pledged $21 billion to assist Korea to reform its economy, restructure its financial and corporate sectors, and recover from recession. Within four years, Korea had recovered sufficiently to repay the loans and, at the same time, rebuild its reserves.

• In October 2000, the IMF approved an additional $52 million loan for Kenya to help it cope with the effects of a severe drought, as part of a three-year $193 million loan under the IMF's Poverty Reduction and Growth Facility, a concessional lending program for low-income countries.

• In October 2000, the IMF approved an additional $52 million loan for Kenya to help it cope with the effects of a severe drought, as part of a three-year $193 million loan under the IMF's Poverty Reduction and Growth Facility, a concessional lending program for low-income countries.

• provides the governments and central banks of its member countries with technical assistance and training in its areas of expertise. • For example: Following the collapse of the Soviet Union, the IMF stepped in to help the Baltic states, Russia, and other former Soviet countries set up treasury systems for their central banks as part of the transition from centrally planned to market-based economic systems.

• provides the governments and central banks of its member countries with technical assistance and training in its areas of expertise. • For example: Following the collapse of the Soviet Union, the IMF stepped in to help the Baltic states, Russia, and other former Soviet countries set up treasury systems for their central banks as part of the transition from centrally planned to market-based economic systems.

IMF Quotas - each member’s monetary contribution • Based on national income, monetary reserves, trade balance, and other economic indicators • Pool of money that can be loaned to members • Basis for how much a country can borrow • Determines voting rights of members Board of Governors - IMF’s highest authority • One representative from each member country • Board of Executive Directors— 24 persons – handles day-to-day operations

IMF Quotas - each member’s monetary contribution • Based on national income, monetary reserves, trade balance, and other economic indicators • Pool of money that can be loaned to members • Basis for how much a country can borrow • Determines voting rights of members Board of Governors - IMF’s highest authority • One representative from each member country • Board of Executive Directors— 24 persons – handles day-to-day operations

IMF Assistance Provides assistance to member countries • Intended to ease balance-of-payment difficulties • Recipient country must adopt policies to stabilize its economy

IMF Assistance Provides assistance to member countries • Intended to ease balance-of-payment difficulties • Recipient country must adopt policies to stabilize its economy

• An international type of monetary reserve currency, created by") Special Drawing Rights (SDRs) • An international type of monetary reserve currency, created by the International Monetary Fund (IMF) in 1969, which operates as a supplement to the existing reserves of member countries. • Created in response to concerns about the limitations of gold and dollars as the sole means of settling international accounts, • SDRs are designed to augment international liquidity by supplementing the standard reserve currencies.

Special Drawing Rights (SDRs) • An international type of monetary reserve currency, created by the International Monetary Fund (IMF) in 1969, which operates as a supplement to the existing reserves of member countries. • Created in response to concerns about the limitations of gold and dollars as the sole means of settling international accounts, • SDRs are designed to augment international liquidity by supplementing the standard reserve currencies.

– Serves as the IMF’s unit of account • unit in which the IMF keeps its records • used for IMF transactions – Some countries pegged their currencies’ value – Based on the weighted average of four currencies • • • 1986– 1990: USD 42%, DEM 19%, JPY 15%, GBP 12%, FRF 12% 1991– 1995: USD 40%, DEM 21%, JPY 17%, GBP 11%, FRF 11% 1996– 2000: USD 39%, DEM 21%, JPY 18%, GBP 11%, FRF 11% 2001– 2005: USD 45%, EUR 29%, JPY 15%, GBP 11% 2006– 2010: USD 44%, EUR 34%, JPY 11%, GBP 11%

– Serves as the IMF’s unit of account • unit in which the IMF keeps its records • used for IMF transactions – Some countries pegged their currencies’ value – Based on the weighted average of four currencies • • • 1986– 1990: USD 42%, DEM 19%, JPY 15%, GBP 12%, FRF 12% 1991– 1995: USD 40%, DEM 21%, JPY 17%, GBP 11%, FRF 11% 1996– 2000: USD 39%, DEM 21%, JPY 18%, GBP 11%, FRF 11% 2001– 2005: USD 45%, EUR 29%, JPY 15%, GBP 11% 2006– 2010: USD 44%, EUR 34%, JPY 11%, GBP 11%

Role of the World Bank • The official name for the world bank is the International Bank for Reconstruction and Development • Purpose: To fund Europe’s reconstruction and help 3 rd world countries. • Overshadowed by Marshall Plan, so it turns towards development – Lending money raised through WB bond sales • • Agriculture Education Population control Urban development

Role of the World Bank • The official name for the world bank is the International Bank for Reconstruction and Development • Purpose: To fund Europe’s reconstruction and help 3 rd world countries. • Overshadowed by Marshall Plan, so it turns towards development – Lending money raised through WB bond sales • • Agriculture Education Population control Urban development

Collapse of the Fixed Exchange System • The system of fixed exchange rates established at Bretton Woods worked well until the late 1960’s – The US dollar was the only currency that could be converted into gold – The US dollar served as the reference point for all other currencies – Any pressure to devalue the dollar would cause problems through out the world

Collapse of the Fixed Exchange System • The system of fixed exchange rates established at Bretton Woods worked well until the late 1960’s – The US dollar was the only currency that could be converted into gold – The US dollar served as the reference point for all other currencies – Any pressure to devalue the dollar would cause problems through out the world

Collapse of the Fixed Exchange System • Factors that led to the collapse of the fixed exchange system include – President Johnson financed both the Great Society and Vietnam by printing money – High inflation and high spending on imports – On August 8, 1971, President Nixon announces dollar no longer convertible into gold – Countries agreed to revalue their currencies against the dollar – On March 19, 1972, Japan and most of Europe floated their currencies – In 1973, Bretton Woods fails because the key currency (dollar) is under speculative attack

Collapse of the Fixed Exchange System • Factors that led to the collapse of the fixed exchange system include – President Johnson financed both the Great Society and Vietnam by printing money – High inflation and high spending on imports – On August 8, 1971, President Nixon announces dollar no longer convertible into gold – Countries agreed to revalue their currencies against the dollar – On March 19, 1972, Japan and most of Europe floated their currencies – In 1973, Bretton Woods fails because the key currency (dollar) is under speculative attack

The Floating Exchange Rate • The Jamaica agreement revised the IMF’s Articles of Agreement to reflect the new reality of floating exchange rates – Floating rates acceptable – Gold abandoned as reserve asset – IMF quotas increased • IMF continues role of helping countries cope with macroeconomic and exchange rate problems

The Floating Exchange Rate • The Jamaica agreement revised the IMF’s Articles of Agreement to reflect the new reality of floating exchange rates – Floating rates acceptable – Gold abandoned as reserve asset – IMF quotas increased • IMF continues role of helping countries cope with macroeconomic and exchange rate problems

Exchange Rates Since 1973 • Exchange rates have been more volatile for a number of reasons including: – Oil crisis -1971 – Loss of confidence in the dollar - 1977 -78 – Oil crisis – 1979, OPEC increases price of oil – Unexpected rise in the dollar - 1980 -85 – Rapid fall of the dollar - 1985 -87 and 1993 -95 – Partial collapse of European Monetary System - 1992 – Asian currency crisis - 1997

Exchange Rates Since 1973 • Exchange rates have been more volatile for a number of reasons including: – Oil crisis -1971 – Loss of confidence in the dollar - 1977 -78 – Oil crisis – 1979, OPEC increases price of oil – Unexpected rise in the dollar - 1980 -85 – Rapid fall of the dollar - 1985 -87 and 1993 -95 – Partial collapse of European Monetary System - 1992 – Asian currency crisis - 1997

Fixed Versus Floating Exchange Rates • Floating: – Monetary policy autonomy • Restores control to government – Trade balance adjustments • Adjust currency to correct trade imbalances • Fixed: – – – Monetary discipline. Speculation Limits speculators Uncertainty Predictable rate movements – Trade balance adjustments – Argue no link between exchange rates and trade • Link between savings and investment

Fixed Versus Floating Exchange Rates • Floating: – Monetary policy autonomy • Restores control to government – Trade balance adjustments • Adjust currency to correct trade imbalances • Fixed: – – – Monetary discipline. Speculation Limits speculators Uncertainty Predictable rate movements – Trade balance adjustments – Argue no link between exchange rates and trade • Link between savings and investment

Exchange Rate Regimes • Pegged Exchange Rates – Peg own currency to a major currency ($) – Popular among smaller nations – Evidence of moderation of inflation • Currency Boards – Country commits to converting domestic currency on demand into another currency at a fixed exchange rate – Country holds foreign currency reserves equal to 100% of domestic currency issued

Exchange Rate Regimes • Pegged Exchange Rates – Peg own currency to a major currency ($) – Popular among smaller nations – Evidence of moderation of inflation • Currency Boards – Country commits to converting domestic currency on demand into another currency at a fixed exchange rate – Country holds foreign currency reserves equal to 100% of domestic currency issued

Exchange-Rate Arrangements IMF permitted countries to select and maintain an exchange-rate arrangement of their choice • IMF surveillance and consultation programs – designed to monitor exchange-rate policies – determine whether countries were acting openly and responsibly in exchange-rate policy

Exchange-Rate Arrangements IMF permitted countries to select and maintain an exchange-rate arrangement of their choice • IMF surveillance and consultation programs – designed to monitor exchange-rate policies – determine whether countries were acting openly and responsibly in exchange-rate policy

From pegged to floating currencies • Broad IMF categories for exchange-rate regimes – peg exchange rate to another currency or basket of currencies with only a maximum 1% fluctuation in value – peg exchange rate to another currency or basket of currencies with a maximum of 2 ¼% fluctuation – allow the currency to float in value against other currencies • Countries may change their exchange-rate regime

From pegged to floating currencies • Broad IMF categories for exchange-rate regimes – peg exchange rate to another currency or basket of currencies with only a maximum 1% fluctuation in value – peg exchange rate to another currency or basket of currencies with a maximum of 2 ¼% fluctuation – allow the currency to float in value against other currencies • Countries may change their exchange-rate regime

Exchange Rate Policies for IMF Members 2004

Exchange Rate Policies for IMF Members 2004

Crisis Management by the IMF • The IMF’s activities have expanded because periodic financial crises have continued to hit many economies – Currency crisis • When a speculative attack on a currency’s exchange value results in a sharp depreciation of the currency’s value or forces authorities to defend the currency – Banking crisis • Loss of confidence in the banking system leading to a run on the banks – Foreign debt crisis • When a country cannot service its foreign debt obligations

Crisis Management by the IMF • The IMF’s activities have expanded because periodic financial crises have continued to hit many economies – Currency crisis • When a speculative attack on a currency’s exchange value results in a sharp depreciation of the currency’s value or forces authorities to defend the currency – Banking crisis • Loss of confidence in the banking system leading to a run on the banks – Foreign debt crisis • When a country cannot service its foreign debt obligations

Determination of Exchange Rates Floating rate regimes—allow changes in the exchange rates between two currencies to occur for currencies to reach a new exchange-rate equilibrium • Currencies that float freely respond to supply and demand conditions • No government intervention to influence the price of the currency

Determination of Exchange Rates Floating rate regimes—allow changes in the exchange rates between two currencies to occur for currencies to reach a new exchange-rate equilibrium • Currencies that float freely respond to supply and demand conditions • No government intervention to influence the price of the currency

Economic Theories of Exchange Rate Determination • Exchange rates are determined by the demand supply of one currency relative to the demand supply of another • Price and exchange rates: – Law of One Price – Purchasing Power Parity (PPP) – Money supply and price inflation • Interest rates and exchange rates

Economic Theories of Exchange Rate Determination • Exchange rates are determined by the demand supply of one currency relative to the demand supply of another • Price and exchange rates: – Law of One Price – Purchasing Power Parity (PPP) – Money supply and price inflation • Interest rates and exchange rates

Law of One Price • In competitive markets free of transportation costs and trade barriers, identical products sold in different countries must sell for the same price when their price is expressed in terms of the same currency • Example: US/French exchange rate: $1 =. 78 Eur A jacket selling for $50 in New York should retail for 39. 24 Eur in Paris (50 x. 78)

Law of One Price • In competitive markets free of transportation costs and trade barriers, identical products sold in different countries must sell for the same price when their price is expressed in terms of the same currency • Example: US/French exchange rate: $1 =. 78 Eur A jacket selling for $50 in New York should retail for 39. 24 Eur in Paris (50 x. 78)

Purchasing Power Parity • By comparing the prices of identical products in different currencies, it should be possible to determine the ‘real’ or PPP exchange rate - if markets were efficient • In relatively efficient markets (few impediments to trade and investment) then a ‘basket of goods’ should be roughly equivalent in each country

Purchasing Power Parity • By comparing the prices of identical products in different currencies, it should be possible to determine the ‘real’ or PPP exchange rate - if markets were efficient • In relatively efficient markets (few impediments to trade and investment) then a ‘basket of goods’ should be roughly equivalent in each country

Big Mac Index

Big Mac Index

Money Supply and Inflation • PPP theory predicts that changes in relative prices will result in a change in exchange rates – A country with high inflation should expect its currency to depreciate against the currency of a country with a lower inflation rate – Inflation occurs when the money supply increases faster than output increases

Money Supply and Inflation • PPP theory predicts that changes in relative prices will result in a change in exchange rates – A country with high inflation should expect its currency to depreciate against the currency of a country with a lower inflation rate – Inflation occurs when the money supply increases faster than output increases

• Fisher Effect - links inflation and interest") Determination of Exchange Rates (cont. ) • Fisher Effect - links inflation and interest rates –nominal interest rate in a country is the real interest rate plus inflation –because the real interest rate should be the same in every country, the country with the higher interest rate should have higher inflation • International Fisher Effect (IFE) - links interest rates and exchange rates –the interest-rate differential is a predictor of future changes in the spot exchange rate » interest-rate differential based on differences in interest rates –currency of the country with the lower interest rate will strengthen in the future

Determination of Exchange Rates (cont. ) • Fisher Effect - links inflation and interest rates –nominal interest rate in a country is the real interest rate plus inflation –because the real interest rate should be the same in every country, the country with the higher interest rate should have higher inflation • International Fisher Effect (IFE) - links interest rates and exchange rates –the interest-rate differential is a predictor of future changes in the spot exchange rate » interest-rate differential based on differences in interest rates –currency of the country with the lower interest rate will strengthen in the future

Other factors affecting exchange rate movements • Confidence—safe") Determination of Exchange Rates (cont. ) Other factors affecting exchange rate movements • Confidence—safe currencies considered Confidence attractive in times of turmoil • Technical factors – release of national statistics – seasonal demands for a currency – slight strengthening of a currency following a prolonged weakness

Determination of Exchange Rates (cont. ) Other factors affecting exchange rate movements • Confidence—safe currencies considered Confidence attractive in times of turmoil • Technical factors – release of national statistics – seasonal demands for a currency – slight strengthening of a currency following a prolonged weakness

Currency Values and Business Exchange rates affect activities of both domestic and international firms Devaluation lowers raises Revaluation export prices import prices raises lowers

Currency Values and Business Exchange rates affect activities of both domestic and international firms Devaluation lowers raises Revaluation export prices import prices raises lowers

Forecasting Exchange-Rate Movements Managers should be concerned with the timing, magnitude, and direction of an exchange-rate movement • Prediction is not a precise science Fundamental forecasting - uses trends in economic variables to predict future rates • Use econometric model or more subjective bases Technical forecasting - uses past trends in exchange rates to spot future trends in the rates • Assumes that if current exchange rates reflect all facts in the market, then under similar circumstances future rates will follow the same patterns • Good treasurers and bankers develop their own forecasts • Use fundamental and technical forecasts for corroboration

Forecasting Exchange-Rate Movements Managers should be concerned with the timing, magnitude, and direction of an exchange-rate movement • Prediction is not a precise science Fundamental forecasting - uses trends in economic variables to predict future rates • Use econometric model or more subjective bases Technical forecasting - uses past trends in exchange rates to spot future trends in the rates • Assumes that if current exchange rates reflect all facts in the market, then under similar circumstances future rates will follow the same patterns • Good treasurers and bankers develop their own forecasts • Use fundamental and technical forecasts for corroboration

Factors to monitor—managers can monitor factors used by governments") Forecasting Exchange-Rate Movements (cont. ) Factors to monitor—managers can monitor factors used by governments to manage their currencies • Institutional setting – float or managed? • Fundamental analysis – economics indicator • Confidence factors • Events • Technical analysis

Forecasting Exchange-Rate Movements (cont. ) Factors to monitor—managers can monitor factors used by governments to manage their currencies • Institutional setting – float or managed? • Fundamental analysis – economics indicator • Confidence factors • Events • Technical analysis

Business Implications of Exchange-Rate Changes Marketing decisions - exchange rates affect demand for a company’s products at home and abroad Production decisions - choice of location for production facilities depends on strength of currency Financial decisions - exchange rates influence the sourcing of financial resources, the cross-border remittance of funds, and the reporting of financial results

Business Implications of Exchange-Rate Changes Marketing decisions - exchange rates affect demand for a company’s products at home and abroad Production decisions - choice of location for production facilities depends on strength of currency Financial decisions - exchange rates influence the sourcing of financial resources, the cross-border remittance of funds, and the reporting of financial results

Stability and Predictability Stable exchange rates Predictable exchange rates Improve accuracy of financial planning Reduce surprises of unexpected rate changes

Stability and Predictability Stable exchange rates Predictable exchange rates Improve accuracy of financial planning Reduce surprises of unexpected rate changes

Implications for Managers • It is critical that international businesses understand the influence of exchange rates on the profitability of trade and investment deals – Adverse changes in exchange rates can make apparently profitable deals unprofitable • The risk introduced into international business transactions by changes in exchange rates is referred to as foreign exchange risk – Foreign exchange risk is usually divided into three main categories: transaction exposure, translation exposure, and economic exposure

Implications for Managers • It is critical that international businesses understand the influence of exchange rates on the profitability of trade and investment deals – Adverse changes in exchange rates can make apparently profitable deals unprofitable • The risk introduced into international business transactions by changes in exchange rates is referred to as foreign exchange risk – Foreign exchange risk is usually divided into three main categories: transaction exposure, translation exposure, and economic exposure

Implications for Managers • Transaction exposure: the extent to which the income from individual transactions is affected by fluctuations in foreign exchange values • Translation exposure: the impact of currency exchange rate changes on the reported financial statements of a company • Economic exposure: the extent to which a firm’s future international earning power is affected by changes in exchange rates

Implications for Managers • Transaction exposure: the extent to which the income from individual transactions is affected by fluctuations in foreign exchange values • Translation exposure: the impact of currency exchange rate changes on the reported financial statements of a company • Economic exposure: the extent to which a firm’s future international earning power is affected by changes in exchange rates

Reducing Translation and Transaction Exposure • These tactics are primarily designed to protect short-term cash flows from adverse changes in exchange rates • Companies should use forward exchange rate contracts and buy swaps • Firms can also use a lead strategy – An attempt to collect foreign currency receivables when a foreign currency is expected to depreciate – Paying foreign currency payables before they are due when a currency is expected to appreciate • Firms can also use a lag strategy – An attempt to delay the collection of foreign currency receivables if that currency is expected to appreciate – Delay paying foreign currency payables if the currency is expected to depreciate

Reducing Translation and Transaction Exposure • These tactics are primarily designed to protect short-term cash flows from adverse changes in exchange rates • Companies should use forward exchange rate contracts and buy swaps • Firms can also use a lead strategy – An attempt to collect foreign currency receivables when a foreign currency is expected to depreciate – Paying foreign currency payables before they are due when a currency is expected to appreciate • Firms can also use a lag strategy – An attempt to delay the collection of foreign currency receivables if that currency is expected to appreciate – Delay paying foreign currency payables if the currency is expected to depreciate

Reducing Economic Exposure • Reducing economic exposure requires strategic choices that go beyond the realm of financial management • The key to reducing economic exposure is to distribute the firm’s productive assets to various locations so the firm’s long-term financial wellbeing is not severely affected by adverse changes in exchange rates

Reducing Economic Exposure • Reducing economic exposure requires strategic choices that go beyond the realm of financial management • The key to reducing economic exposure is to distribute the firm’s productive assets to various locations so the firm’s long-term financial wellbeing is not severely affected by adverse changes in exchange rates