Instructor: Yulia Ilina, Associate Professor [email protected] Teaching Assistant:

are open-book assignments that combine open questions, multiple")

Final evaluation is exercised by written open-book exam (100 min).")

Net operating profit after")

NOPAT = EBIT(1 -")

What are operating current assets? Operating current assets")

What are operating current liabilities? Operating current liabilities")

")

Operating Capital= NOWC + Net")

for 2010 FCF = NOPAT - Net investment in")

Net operating profit after")

MVA = Market Value of the Firm - Book Value")

a. Calculate net operating working capital,")

?")

Governments: U.S. governments are net borrowers,")

14338-topic_1.ppt

- Количество слайдов: 69

Instructor: Yulia Ilina, Associate Professor [email protected] Teaching Assistant: Kristina Lochakova, Assistant professor [email protected]

Topic 1 Introduction to Corporate Finance

Financial management: goals, primary issues, company’s value and cash flows Introduction to the course Free cash flow and company’s value Accounting and market-based performance results Capital allocation process and financial markets Topic 1

Objectives To understand the corporate finance framework, financial environment To identify goals and objectives of financial management and its focus on … Explain the main goal of financial management, the concept of the free cash flow, the relationship between company’s value and cash flows Understand the capital allocation process and the role of financial markets

The goal of financial management and investment decisions Maximizing shareholders wealth High return on investments Choosing effective investment proposals

The goal of financial management and Financing decisions Maximizing shareholders wealth Sufficient financing at the low cost Choosing among sources of finance

Organizational forms of companies What are companies organizational forms? Which organizational form is mostly hard (challenging) to manage in terms of finance?

Organizational forms of companies What could be motives for the company to become chartered as a corporation? Explore more financing and investment opportunities (for. ex. raising capital from financial markets) Enhancing opportunities for growth

Organizational forms of companies Is it true: the majority of companies are chartered as corporations? Is it true: - the major part of GNP is produced by corporations? - the largest cash flows are generated by corporations? - corporations are main users of funds in financial markets (among other forms of business)?

Corporate Finance The issues studied in Corporate Finance course are primarily relevant for corporations (public companies)

!!! Corporate finance is today the discipline not simply supporting the managerial decisions on various aspects of company’s activities (assets valuation, policy of debt financing, dividends payments etc.), but is the advanced section of strategic management in which the focus is more and more transferred from purely quantitative methods of valuation on qualitative methods of decision making, however, necessarily based on mathematical models. Corporate Finance

What is a successful company and how finance fits in it? Successful companies should have enough funding – be able to raise capital externally Successful companies should make effective investments that add value to the firm

Largest and fastest-Growing Largest companies Fastest-growing companies

Corporate finance provides the skills managers need to: Identify and select the corporate strategies and individual projects that add value to their firm. Forecast the funding requirements of their company, and devise strategies for acquiring those funds. Why is corporate finance important to all managers?

Maximizing shareholders' wealth What does this mean: maximizing company’s value? Market value or …. Fundamental value?

Price and Value: Difference Price is what you pay, Value is what you get. Warren Buffet

Corporate scandals and shareholders value maximization What lessons could be learned from the corporate failures? Didn’t managers strive for a company’s value maximization? Fundamental value vs. Market price

Shareholders value maximization How the corporate form of business could come into conflict with this goal? Separation of ownership and control Agency problem

Which sources of financing are to be used? How we should estimate the cost of each of sources? How to choose the most effective capital structure? Which investment opportunities to accept? How corporate governance mechanisms could be used to avoid the conflict of interests? How to increase company’s value?

Corporate Finance Course content Topic 1. Introduction to Corporate Finance. Topic 2. Valuing Debt Securities. Bonds Valuation and Interest Rates. Topic 3. Stocks Valuation. Topic 4. Risk and Return. Capital Asset Pricing Model. Topic 5. Cost of Capital. Topic 6. Long-term Financial Decisions: Capital Budgeting and Investment Valuation. Topic 7. Capital Structure Decisions. Topic 8. Financial Statements Analysis and Corporate Valuation. Topic 9. Corporate Governance. IPO.

Textbooks Required textbook E. Brigham, M. Ehrhardt. Financial Management: Theory & Practice. 13th ed. Thomson-South Western. 2010 (http://www.cengage.com/brigham) Additional recommended textbook (available at GSOM library) S. A. Ross, R. W. Westerfield, B. D. Jordan. Essentials of Corporate Finance. 6-th ed. McGraw Hill. 2008.

Grading system

Current evaluation In-class tests (40 min) are open-book assignments that combine open questions, multiple choice questions and problems (сalculus). In case of missing (failure) the test, missing other in-class assignments they are not to be repeated or substituted by other types of activities. Group home assignments, based on in-class group discussions, are assigned only for those students, who participated in group class work. Group project: A comprehensive group assignment based on application of corporate finance concepts to particular company case. Students should be able to demonstrate their skills in valuing company’s securities, based on various methods, to estimate the cost of capital and capital structure, to value a company and make financial statements analysis.

Final evaluation (exam) Final evaluation is exercised by written open-book exam (100 min). Exam includes mini-tests, problems, and essay questions. See Course Syllabus for other details.

What determines a firm’s value? The ability to generate cash flows in the long run. Free cash flow – cash flow available for distribution to company’s investors; cash flow available to all providers of the firm’s capital after the firm’s investment decisions have been made. FCF = Sales revenues – Operating costs – Operating taxes – Required investments in operating capital

Free cash flow Revenue Cost of goods sold Depreciation Selling, General and Administrative =Operating profit (EBIT) - Tax on operating profit = Net operating profit after tax (NOPAT) + Depreciation Capital expenditures Investment in Working capital = Cash flow from operations (FCF)

FCF is the amount of cash available from operations for distribution to all investors!!! (including stockholders and debtholders) after making the necessary investments to support operations. A company’s value depends on the amount of FCF it can generate. Free cash flow

How the firm’s fundamental value is related to the FCF and the cost of capital? The value of the firm is determined by the present value of its free cash flows (FCF) discounted at the weighted average cost of capital (WACC)

Cost of capital Rate of return for suppliers of capital Cost of money for users of capital

30 Value = + + + FCF1 FCF2 FCF∞ (1 + WACC)1 (1 + WACC)∞ (1 + WACC)2 Free cash flow (FCF) Market interest rates Firm’s business risk Market risk aversion Firm’s debt/equity mix Cost of debt Cost of equity Weighted average cost of capital (WACC) Sales revenues Operating costs and taxes Required investments in operating capital − − = Determinants of Intrinsic Value: Calculating FCF ...

Is it true? Financial managers generate company’s cash flows. - No! Financial managers function is to make financial decisions (financing – raising capital, investing) to increase company’s value.

Free cash flow – what to know Company with high growth opportunities might have negative free cash flow even if the company is profitable When the growth slows, FCF of the profitable company could be positive and large

Free cash flow Revenue Cost of goods sold Depreciation Selling, General and Administrative =Operating profit (EBIT) - Tax on operating profit = Net operating profit after tax (NOPAT) + Depreciation Capital expenditures Investment in Working capital = Cash flow from operations (FCF)

Financial statements: Income Statement 34

Financial statements. Balance Sheet: Assets 35

Financial statements. Balance Sheet: Liabilities & Equity 36

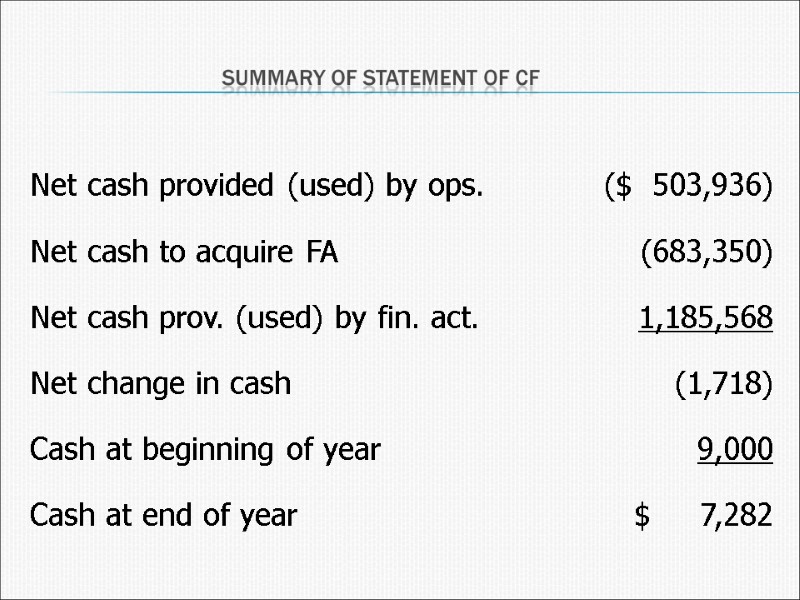

Financial statements. Statement of Cash Flows: 2010 37

38 Financial statements. Statement of Cash Flows: 2010

39 Financial statements. Statement of Cash Flows: 2010

Exercise Calculate a FCF for a given company

42 Earning before interest and taxes (1 − Tax rate) Net operating profit after taxes X Operating current assets Operating current liabilities Net operating working capital − Total net operating capital Operating long-term assets + Net operating working capital Free cash flow − Net investment in operating capital Net operating profit after taxes − Total net operating capital this year Total net operating capital last year Net investment in operating capital Calculating Free Cash Flow in 5 Easy Steps Step 1 Step 2 Step 3 Step 4 Step 5

FCF NOPAT Net operating working capital Total net operating capital Net investment in operating capital Free cash flow.

1. Net Operating Profit after Taxes (NOPAT) NOPAT = EBIT(1 - Tax rate)

2. Net Operating Working Capital (NOWC) What are operating current assets? Operating current assets are the CA needed to support operations. Op CA include: cash, inventory, receivables. Op CA exclude: short-term investments, because these are not a part of operations.

2. Net Operating Working Capital (NOWC) What are operating current liabilities? Operating current liabilities are the CL resulting as a normal part of operations. Op CL include: accounts payable and accruals. Op CL exclude: notes payable, because this is a source of financing, not a part of operations.

2. Net Operating Working Capital (NOWC)

3. Total net operating capital (also called operating capital) Operating Capital= NOWC + Net fixed assets.

4. Net investment in operating capital

Free Cash Flow (FCF) for 2010 FCF = NOPAT - Net investment in operating capital How do you suppose investors reacted?

51 Earning before interest and taxes (1 − Tax rate) Net operating profit after taxes X Operating current assets Operating current liabilities Net operating working capital − Total net operating capital Operating long-term assets + Net operating working capital Free cash flow − Net investment in operating capital Net operating profit after taxes − Total net operating capital this year Total net operating capital last year Net investment in operating capital Calculating Free Cash Flow in 5 Easy Steps Step 1 Step 2 Step 3 Step 4 Step 5

FCF Is it always bad when FCF is negative? What are primary uses of FCF?

1. Pay interest on debt. 2. Pay back principal on debt. 3. Pay dividends. 4. Buy back stock. 5. Buy nonoperating assets (e.g., marketable securities, investments in other companies, etc.).

Stock Price and Other Data

What is a market value of the firm? What is MVA?

Market Value Added (MVA) MVA = Market Value of the Firm - Book Value of the Firm Market Value = (# shares of stock)(price per share) + Value of debt Book Value = Total common equity + Value of debt 56

MVA If the market value of debt is close to the book value of debt, then MVA is: MVA = Market value of equity – book value of equity 57

MVA for our company: what is an assumption? Market Value of Equity 2010: (100,000)($6.00) = $600,000. Book Value of Equity 2010: $557,632.

Main financial performance results: accounting and market-based EBITDA EBIT EBT Net Income Cash flow Free cash flow NOPAT Market value MVA Are directly obtained from financial statements (as they are presented in annual reports) Market-based measures

Using the financial statements (see file-home exercise1.1) a. Calculate net operating working capital, total net operating capital, net operating profit after taxes, free cash flow for the most recent year. b. Assume that there were 15 million shares outstanding at the end of the year, the year-end closing stock price was $65 per share, and the after-tax cost of capital was 8%. Calculate MVA for the most recent year. Exercise (home) ..\home exercise1.1.xlsx Home exercise 1.1

Capital allocation process and financial markets

Capital allocation process and financial markets Who are net savers and net borrowers (investors)? What types of securities are used for providing corporate financing?

Households: Net savers Non-financial corporations: Net users (borrowers) Governments: U.S. governments are net borrowers, some foreign governments are net savers Financial corporations: Slightly net borrowers, but almost breakeven Who are net savers and net borrowers?

Types of financial instruments

Types of financial instruments

Types of financial instruments

Types of financial instruments

For further discussion on the topic 1 read: BE, chapters 1,2.

Required for discussion in class 2: Mortgage securitization and it’s role in financial crisis BE, chapter 1 (pp. 17-18, 36-43) Video tutorial (Mortgage-backed securities I, II, III): http://www.foreclosuresinmass.com/mortgage_securitization.aspx