dd6bdc41637b9840bc425faa42894487.ppt

- Количество слайдов: 70

ICAI’s Pune Branch’s Refresher course on Companies Act, 2013 ICAI-WIRC 17 th April 2016 Oppression and Mismanagement & Class Action Adv. Prachi Manekar-Wazalwar Corporate Lawyer Please provide your inputs at prachimanekar@gmail. com

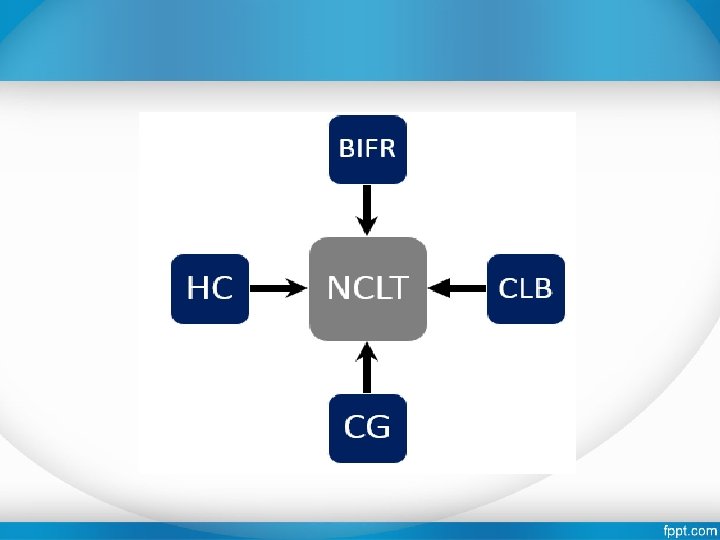

New Enforcement Mechanism Enforcement Machinery Civil NCLT NCLAT Criminal Central Government Special Courts SFIO Investigation officers

New Powers • • Class action; Deregister a company and determine other incidental matters; Remove auditor of a company; Reopen of books of accounts Revise books of accounts Additional powers in case of non-payment of deposits Certain Powers in case of Fast Track Merger

Investor Protection & NCLT

Oppression and Mismanagement • Minority shareholders should be protected from abusive actions by, or in the interest of, controlling shareholders acting either directly or indirectly, and should have effective means of redressal.

Meaning of Oppression Law Lexicon by Ramanatha Aiyer Oppression: • An act or omission may also amount to oppressive conduct if it is designed to achieve an unfair advantage. • The person complaining oppression must show that he was constrained to submit the conduct which is unfair to him and which causes prejudice to him. In the exercise of his legal propriety rights as shareholder. • Oppression means burdensome, harsh and wrongful

(b) of the Companies Act, 2013 reads as under: “(b) the")

Mismanagement • “Section 241(1)(b) of the Companies Act, 2013 reads as under: “(b) the material change, not being a change brought about by, or in the interests of, any creditors, including debenture holders or any class of shareholders of the company, has taken place in the management or control of the company, whether by an alteration in the Board of Directors, or manager, or in the ownership of the company’s shares, or if it has no share capital, in its membership, or in any other manner whatsoever, and that by reason of such change, it is likely that the affairs of the company will be conducted in a manner prejudicial to its interests or its members or any class of members. ….

Meaning of Mismanagement Chander Krishan Gupta v Pannalal Girdhari Lal Pvt. Ltd. and Ors. [MANU/DE/0242/1981, [1984]55 Comp. Cas 702(Delhi), 1982(3)DRJ 295] “(10) Section 398 has two facts. The first is that positive acts are done by the management which results in prejudice being caused to the company. Secondly section 398 may be attracted even where no action at all is taken by the management and such non action results in prejudice being caused to the company”

Acts held to be oppressive • • Pushing a shareholder into hopeless minority Violating statutory rights of a shareholders Legitimate expectations in quasi partnership companies Issue of shares in certain cases Not giving notices Not allowing attendance in general meetings Not permitting inspection of records Disposing of Assets of the company in illegal manner

Not held to be oppressive • • Non-holding of the meeting of the director (Chander Krishan Gupta v. Pannalal Girdhari lal (P. ) Ltd. [1984] 55 Comp. Cas. 702 (Delhi). ) Denial of inspection of books to a shareholder (Maharani Lalita Rajya Lakshmi v. Indian Motor Company (Hazaribagh) ltd. ) Lack of details in notice of a meeting. Non-maintenance of records at registered office in accordance with the provisions of the law (Chander Krishan Gupta v. Pannalal Girdhari lal (P. ) ltd. ) Manipulation in the filing of balance sheet with the ‘Registrar without the signatures of the auditors by itself does not amount to an act of oppression on the minority of shareholders. Drawing of remuneration by a director to which he is not legally entitled. Negligence and inefficiency in managing the affairs of a company. Increasing the voting rights of the shares held by the management.

• • • The majority group sold its shares. As a result of such sale, the such majority group called an EGM wherein it authorized the Board of directors to appoint nominees of the proposed acquirer in the Board. In this case, it was held that as on the date of the petition no such appointment was made and accordingly allegations were premature. In the context of allegations of transfer of shares to an outsider to the hitherto composition of shareholding and inducting the outsider as a director in violation of articles of association and in not sending the notice of EOGM to the petitioner, the CLB found that while the allegation of violating the provisions of the articles could not be substantiated, the irregularity in holding the EOGM was there. This in itself cannot be taken as oppression as in the EOGM majority of shareholders took the decision on transfer as oppression, as in the best interest of the company. However, having regard to prejudice caused to the interest of the Petitioner as shareholder, the respondent was directed to buy out the shares of the Petitioner (Cine & Supply Corpn. (P. ) Ltd. , In re [2002] 35 SCL 683. ) In case where allegation of minority oppressing majority was brought before it, CLB ruled that mere expression of desire to gain control over the company by the minority is not an act of oppression (Ultrafilter (India) Pvt. Ltd. V. Ultrafilter Gmb. H [2002] 38 SCL 573. )

Who can apply • Members • Central Government

Who can apply Eligibility Criteria: Company having share capital: • 100 hundred members or one-tenth of the total number of its members whichever is less, or • Any member or members holding not less than one tenth of the issued share capital of the company. Company not having share capital • One-fifth of the total number of its members: A representative suit can also be filed by a member or members with the written consent from other members.

Wide Powers to pass Orders • The Tribunal is given complete freedom to bring an end to the oppression and mismanagement. Section 242, like the powers conferred under sec 397 and sec 398 of the Companies Act, 1956 provides “the Tribunal may, with a view to bringing to an end the matters complained of, make such order as it thinks fit. ” • Section 242(2) also begins with the words “Without prejudice to the generality of the powers under subsection (1), an order under that sub-section may provide for—…. ”. Thus, the wide powers of the Tribunal is not curtailed by sec 242(2) and the Tribunal can exercise the wide powers. The nature and extent of powers of CLB was discussed in many cases.

Existing Powers • • The regulation of conduct of affairs of the company in future. The purchase of shares or interests of any members of the company by other members thereof or by the company and reduction of capital if the shares are acquired by the company. The termination, setting aside or modification, of any agreement, between the company and its MD/Director/Manager. The setting aside of any transfer, delivery of goods, payment, execution or other act relating to property made or done by or against the company within three months before the date of the application under this section, which would, if made or done by or against an individual, be deemed in his insolvency to be a fraudulent preference.

• • • New/Modified Powers: The termination, setting aside or modification of any agreement between the company and any person other than MD/Director/Manager. This can be done after obtaining the consent of the party concerned. Earlier for termination, the consent of the other party was not required. Restrictions on the transfer or allotment of the shares of the company. Removal of the MD/manager/ Director of the company. Recovery of undue gains made by any MD/Manager/Director during the period of his appointment. Determine the manner in which the amount said so recovered shall be utilised. It can be transferred to IEPF or may be repaid to identifiable victims. The manner in which the MD/Manager of the company may be appointed subsequent to an order removing of the existing managing director or manager. Appointment of such number of persons as directors, who may be required by the Tribunal to report to the Tribunal on such matters as the Tribunal may direct. Imposition of costs as may be deemed fit by the Tribunal. Any other matter for which, in the opinion of the Tribunal, it is just and equitable that provision should be made.

OVERVIEW OF CHANGES Reducing the bar set for oppression The Companies Act, 2013 has reset the bar for oppression to a lower level to include even those oppressive acts that may be prejudicial to members. It also seeks to include not only continuing oppressive actions but also those actions that have continued till recent times. Increasing the bar for mismanagement Now the test “winding up on just and equitable grounds” is made applicable even for mismanagement. Thus, to establish a case for mismanagement, the petition will have to show that the mismanagement is of such nature that it is just and equitable to winding up the company but winding up will unfairly prejudice the petitioner. This test was earlier not applicable to mismanagement matters. Mismanagement resulting in prejudice to public interest is removed as a ground for mismanagement but material change resulting in prejudice to members or class of members is included as a ground for initiating mismanagement.

• • Composite petition The Act does not bar seeking multiple reliefs by way of one application. Thus, reliefs like reopening etc. can be filed simultaneously with oppression and mismanagement to get a holistic relief. Dilution of eligibility criteria Earlier, if a member did not meet the eligibility criteria, he had to apply to the Central Government to seek permission to file a case for oppression and mismanagement. Now, the Tribunal is empowered to decide whether a member below the eligibility criteria can apply.

Impact and interplay of other remedies • The Act has inserted various remedies that are available to the member which can be: • Deregistration 7(7) • Class Action (section 145) • Investigation (sections 210 & 213) • Reopening of books of accounts (section 130) • Seeking compensation from auditors (section 147(3)) • Directions in case of refusal to Transfer and Transmit securities • Right to take exit route in select cases, where Act provides for the same • Some of these remedies can be used along-with the remedy for oppression and mismanagement and some cannot.

CLB vs. NCLT • • • Jurisdiction Scope of powers Nature of general powers Matters that can be taken up Nature of authority Limitation period

General Powers of Tribunals • • Contempt of Court Execution of orders Assistance of Magistrate or Collecctor Powers of Civil Court Power to Determine Procedure Inherent Power to dispense with procedure

Remedies for Person Aggrieved by Order NCLT Appeal any order on Questions of law and fact NCLAT Supreme Court Appeal on Questions of law

Powers of Civil Court • • summoning and enforcing the attendance of any person requiring the discovery and production of documents; receiving evidence on affidavits; subject to the provisions of sections 123 and 124 of the Indian Evidence Act, 1872, requisitioning any public record or document or a copy of such record or document • issuing commissions for the examination of witnesses or documents. • dismissing a representation for default or deciding it ex parte. • setting aside any order of dismissal of any representation

Powers of Civil Courts continued • • granting stay or order status quo; ordering injunction or cease and desist; appointing commissioner (s) for the purpose under the Act; exercising limited power to review its decision to the extent of correcting clerical or arithmetical mistakes or any accidental slip or omission as provided in rule 189 of these rules; • passing such order or orders as it may deem fit and proper in the interest of justice.

Representation before NCLT/NCLAT • A party to any proceeding or appeal before the Tribunal or the Appellate Tribunal, as the case may be, may either appear in person or authorise one or more of the following persons to present his case before the Tribunal or Appellate Tribunal: • Chartered accountants; • Company secretaries; • Cost accountants; • Legal practitioners; • Any other person like officer of the company.

Class Action Suits Prachi Manekar, Corporate Legal Consultant Prachi Manekar

Class Action Suit Prachi Manekar

What is Class Action A lawsuit filed or defended by an individual or small group acting on behalf of a large group Prachi Manekar

Do we have the concept of Class action in India • Yes. We already have the concept of class action in India • The class action is a vehicle for securing judicial review in India • Public Interest Litigation Prachi Manekar

Do we have the concept of class action in Companies Act, 1956 O& M is a type of class action Prachi Manekar

Class actions world wide • Bank of America has agreed to settle a class-action lawsuit brought by investors who claimed they were misled by its Countrywide unit into buying risky mortgage securities. Bank of America acquired Countrywide Financial, a California-based lender, in July 2008 for $2. 5 billion, but analysts have put the effective cost at more than $40 billion, taking into account the post-purchase lawsuits, loan buybacks and write-downs. Prachi Manekar

Companies Act The concept of class action suits has been introduced giving right to a group of shareholders or depositors to move NCLT if they believe that the management or conduct of the affairs of the company are prejudicial to them, such concept is already permitted in the US. Prachi Manekar

Who can sue Shareholders & Depositors Prachi Manekar

What can they claim Compensation © Prachi Manekar

Compensation for What Damages for any fraudulent, unlawful or wrongful act or conduct or any likely act or conduct on his part © Prachi Manekar

Compensation From -Company -Directors -Experts -Advisors © Prachi Manekar

Can investor seek recourse to Section 245 for wrongdoings prior to enactment of new Companies Act © Prachi Manekar

Class Action Suit vs. Arbitration © Prachi Manekar

Biggest Scams Old Scams analysed in new light © Prachi Manekar

Harshan Mehta Scam • He siphoned off funds amounting to Rs 4, 000 crore (Rs 40 billion) from various banks to manipulate stocks in the early 1990 s. The scam was exposed as the markets crashed, and banks and investors lost huge amount of money. He died in 2001. © Prachi Manekar

• How could National Housing Bank give stock broker custody of a Rs. 95. 39 -crore cheque? • The Supreme Court on Wednesday pulled up the Centre for failing to get at the truth of the securities scam indulged in by the late stock broker Harshad Mehta and directed the National Housing Bank to return to the State Bank of India Rs. 95. 39 crore with 19 per cent interest from 1992 (about Rs. 900 crore. )… 15 th August 2013 , The Hindu © Prachi Manekar

Ponzi scheme • Chain Roop Bhansali collected money from the public through mutual funds, fixed deposits and debentures. • He also raised funds through non-existent companies and transferred the money to shell companies or others who invested with him. • The scam came to light when he could not raise more money. The scam resulted in a loss of Rs 1, 100 crore (Rs 11 billion).

Ketan Parekh scam • Ketan Parekh was involved in circular trading and stock manipulation through 1999 -2001 in a host of companies. Like Mehta, he borrowed from banks such as Global Trust Bank and Madhavpura Mercantile Co-operative Bank, and manipulated a host of stocks popularly known as K-10 stocks. Parekh has been banned from the stock market. © Prachi Manekar

Rs 14, 000 crore Satyam scam • Ramalinga Raju confessed he had cooked up the accounts of Satyam Computers and that the cash and bank balances were inflated by Rs 5, 040 crore (Rs 50. 40 billion), after a failed attempt to acquire Maytas. • Satyam Computers has since been acquired by Tech Mahindra. © Prachi Manekar

. Leading")

NSEL • Jignesh Shah, the man behind the crisisridden National Spot Exchange (NSEL). Leading brokers, who rarely antagonise exchange authorities, came on air on Tuesday to openly badmouth Shah and the exchange's alleged failure to safeguard commodity stocks and repay thousands of investors on time. © Prachi Manekar

• More than 12, 000 small investors and farmers in NSEL are now waiting to get back their investments in NSEL. Fraud • artificial liquidity was created • forged warehouse receipts • same stocks pledged with more than one lender. • NSEL is indulging in a cover-up,

• Many public sector units, including MMTC and PEC, have either lost or locked hundreds of crores in the National Spot Exchange Ltd (NSEL) payment crisis, and asked the government to take action against the exchange. Both companies jointly have an exposure of Rs 300 crore to NSEL.

Ponzi Schemes • The Saradha group ran a wide variety of collective investment schemes that collected money from the public. The ponzi scheme collapsed and caused an estimated loss of Rs 4, 000 crore (Rs 40 billion) with 1. 4 million investors affected, mostly small savers. The Union government launched a multiagency probe to investigate the scam. • Sudipta Sen, promoter of Saradha group is the key accused in the scam.

• 73 companies running Ponzi schemes to be shut down, says West Bengal government © Prachi Manekar

2 G Scam

• Corporations accused in 2 G Spectrum Scam and charges against them • A number of companies and firms have been implicated in the 2 G Spectrum scam and they are as follows: • Unitech Wireless • Reliance Telecom • Swan Telecom © Prachi Manekar

Loop Mobile India Ltd Loop Telecom Pvt Ltd Essar (Parent company of Essar Tele Holding) Essar Tele Holding • The criminal charges framed against these companies include the following: • Section 120 B • Section 420 (cheating) • Sections 468 and 471 (forgery) © Prachi Manekar

Possibility of Abuse Frivolous applications, if any, made by the group of shareholders or depositors will be rejected and the applicant can be asked to pay up to Rs 1 lakh to the opposite party © Prachi Manekar

What will the future look like © Prachi Manekar

Leading Class Action Suits in World © Prachi Manekar

AOL Time Warner • Status: Settled 2005 • Amount: $2. 5 billion Investors in AOL Time Warner stock sued the company for fraud under federal securities law. The company was alleged to have improperly accounted for dozens of advertising transactions between 1998 and 2002. The alleged transactions created the appearance that they were generating revenue when, in reality, were just shifting money back and forth. The alleged false earnings statements inflated the company’s value by $1. 7 billion.

Tyco International • Status: Settled 2007 Amount: $3. 2 billion A series of class-action lawsuits were filed against the company. , former officers and directors of Tyco, and Pricewaterhouse Coopers, alleging that these individuals and entities made false and misleading public statements and omitted material information about Tyco's finances in violation of Sections 10(b), 14, 20 A and 20(a) of the Securities Exchange Act of 1934.

World Com • Status: Settled 2005 Amount: $6. 2 billion This class-action lawsuit represented investors who held World Com stock from April 29, 1999 through June 25, 2002. Lawsuits were initiated against World Com, and individual employees Bernard Ebbers (CEO), Scott Sullivan (CFO) David Myers (Controller) and Buford Yates (Accounting Director) for fraud.

World Com The main charges of fraud stemmed from improperly classifying expenses as “capital costs” and inflating revenue statements with false entries. The Securities and Exchange Commission (SEC) later stated that the earnings and assets had been falsely stated by over $11 billion.

Enron Status: Settled 2006 Amount: $7. 2 billion Investors in Enron corporate stock filed lawsuits under both federal and state securities laws against Enron Corporation, individual Enron officers and directors, Enron’s accountant Arthur Anderson, individual Arthur Anderson partners and employees, and Enron’s former law firm Vinson & Elkins. © Prachi Manekar

Enron • The lawsuit’s primary contention was that Enron engaged in fraud by concealing from investors losses by Enron-controlled special purpose entities (the Raptors). Because Enron’s primary corporate losses were attributed to these entities, those losses were not disclosed in annual reports or SEC filings. In total, the $7. 2 billion in settlements reached by Enron to compensate shareholders whose stock became worthless during the company collapse is the largest payout to date in a shareholder securities class action. © Prachi Manekar

Rising Class Action Abroad The sweep of securities class litigation is massive, and is increasing by time. The US Chamber Institute for Legal Reform report above states that since 1996, at least 2, 758 public companies—or 41% of the roughly 6, 000 companies currently listed on the three major stock exchanges—have been named as defendants in at least one federal securities class action. As accounting standards get more complicated, it is possible to find accounting lapses and use them as the handle to file class litigation © Prachi Manekar

Will we face an avalanche of Class Actions © Prachi Manekar

Impact on CA’s

Other Onerous Provisions – Impact on CA’s • CA’s who help in raising Corporate Finance • Recourse for people relying on audit report • Removal of Authority

Queries? © Prachi Manekar

")

For more details NCLT & NCLAT Law, Practice and Procedure (Releasing Shortly)

Thank you Prachi Manekar-Wazalwar 308, Jolly Bhavan No. 1, 10, New Marine Lines, Mumbai-20 prachimanekar@gmail. com

dd6bdc41637b9840bc425faa42894487.ppt