bf4739b897d4aa589c307395aa15ceae.ppt

- Количество слайдов: 33

How Competitive is the Canadian Residential Broadband Market? A Study of Canadian Internet Service Providers and Their Regulatory Environment Catherine Middleton Annemijn van Gorp Research conducted in Summer 2009 Ted Rogers School of Management Ryerson University , Toronto, Ontario

Broadband competition in Canada • Facilities-based competition – battle for the broadband home – cableco vs. telco – fierce competition • Services-based competition – third party access to existing infrastructure – idea is to increase competition – local loop unbundling on copper – TPIA – third party internet access – on cable

Effective Benefits of ^ Competition “The fastest connections, lowest prices and most innovative services are in areas where there is a range of consumer choices for broadband. ”

–")

What has changed since 2009? • more use of TPIA (reselling of cable) – Why? CRTC mandate • speed matching is required – but incumbents are explicitly not required to provide IPTV capacity • new pricing regime – but Review & Vary applications in process

What hasn’t changed? • • Market share of independent ISPs Lack of innovation among ISP offerings Pricing Difficulty of running small ISP

CRTC data – residential internet 2006 2007 2008 2009 2010 Canadian Radio-television and Telecommunications Commission (2011). Communications Monitoring Report. CAGR 06 -10

. Residential and Business Broadband Prices")

Broadband pricing Wallsten, S. , & Riso, J. (2010). Residential and Business Broadband Prices Part 2: International Comparisons. Washington, DC: Technology Policy Institute. – “while residential prices have remained unchanged in the U. S. , they have been falling in most other OECD countries” (p. 2)

. OECD Communications Outlook 2011. Paris:")

Broadband pricing Organisation for Economic Co-operation and Development (2011). OECD Communications Outlook 2011. Paris: OECD. – “Broadband prices have been continuously declining over the past decade across the OECD area, while connection speeds have increased” (p. 264) – 2010 data “the average download speed was 36 mbps and the average upload speed 16 mbps. ” (p. 265)

OECD data

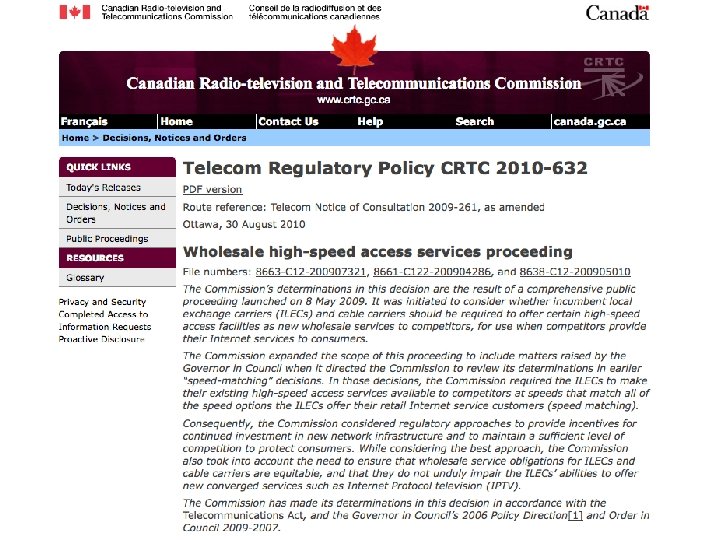

September 2009

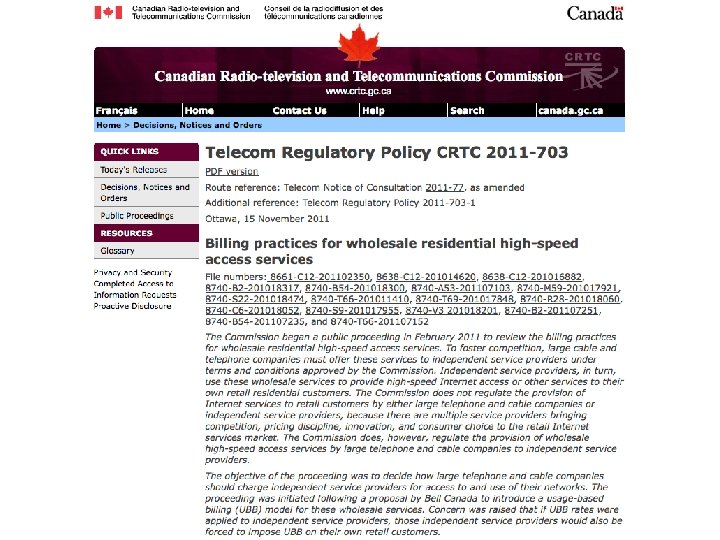

July 2012

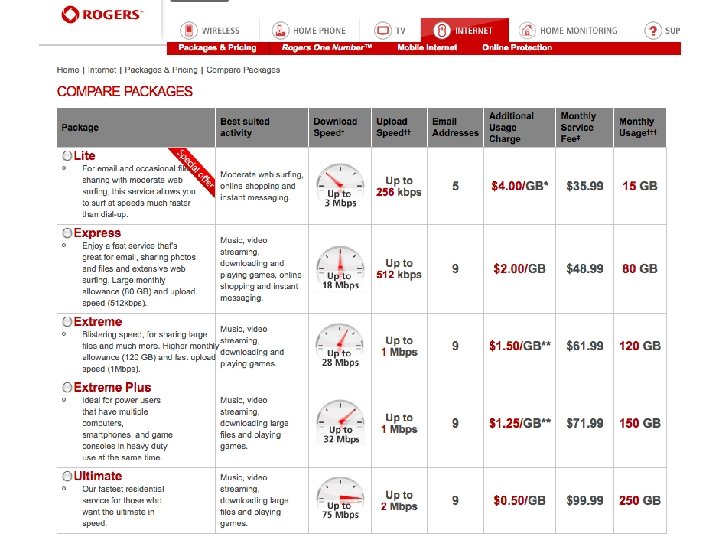

Rogers: 2009

2735 MR. GAUDRAULT: Again, we are actively trying to sell everything we can basically across the country. 2736 COMMISSIONER KATZ: So you were initially selling just DSL. 2737 MR. GAUDRAULT: That's right. 2738 COMMISSIONER KATZ: When you made the decision to upgrade to sell both, what was the -- I don't want to ask you what the cost was, but what was the magnitude of the decision that you had to take and what were thought process and how big a decision was it? 2739 MR. GAUDRAULT: So I guess you guys had a big part to play in it, the uncertainty of that. The fact that we had been selling 5 megabyte for years without any upgrade, the fact that looking -- after doing the 261 proceeding it became pretty obvious that at some point people are just going to want faster speeds period. So the sellability of the product became, "Geez, you know, people are going to start wondering. " 2740 So sure enough a 5 -meg product is less sellable today than when this proceeding first started a couple of years ago. 2741 So all these things, looking into the future saying, "Wow, if we don't do this we won't have anything viable. " They are not giving us the higher speeds. So all this put together. 2742 And then initially we tried looking at TPIA sooner, but it is really expensive. Like on any one connection the ROI is like two or three months. It's tough. So it was a big pill to swallow just to start TPIA the way we did and it's either kind of you have to go big or not go at all with TPIA the way it was set up. 2743 Even now there a lot of problems with it, just it's tough. 2744 COMMISSIONER KATZ: Did you have to build an overlay network or could you use the infrastructure you had and simply adapt it? 2745 MR. GAUDRAULT: So we leveraged whatever we could out of whatever we were doing with DSL, but the input rates just from TPIA themselves were the real barrier. So the gear we had, for sure that helped, there is no doubt you know. So somebody coming in just to do TPIA, it's no mystery to me why there's not a lot of people selling TPIA already, it just doesn't make sense. You are shooting yourself in the foot. 2746 COMMISSIONER KATZ: And the costs are competitive for you to buy TPIA relative to DSL? 2747 MR. GAUDRAULT: Well, let's just say I'm banking that this is all going to work out pretty good. 2748 COMMISSIONER KATZ: But today are you paying a premium? 2749 MR. GAUDRAULT: For. . . ? 2750 COMMISSIONER KATZ: For the same throughput on TPIA as for GAS I guess? 2751 MR. GAUDRAULT: So in the access part? 2752 COMMISSIONER KATZ: Total. Per customer. When you sell to a customer -2753 MR. GAUDRAULT: Well, TPIA costs more, but it's hard to compare apples to apples because they are different speeds. That's the reason we went there.

Slides from 2009 conference presentation

Broadband in Canada • • The cableco “doesn’t even Who cares? get out of bed to make an attempt. They don’t Facilities-based competition between want ISPs, they don’t want incumbent cablecos and incumbent telcos, wholesale business” duopoly • Open access provisions for cable in place since 1999, uncommon • Unbundled local loop mandated in 1997 • Is the market competitive? We started talking to ISPs to find out.

Assumptions about Competition • The literature and most OECD governments/policy makers state that the development of broadband infrastructure should be driven by competition • Facilities-based competition (i. e. cable vs. DSL vs. wireless) is preferred • Service-based competition (using existing facilities) is 2 nd best, but may encourage facilities-based competition over time

Benefits of Competition • Rivalry in pricing and services • Low barriers to entry for new providers • Competitors can establish “a reasonably sustainable market position”

Sustainable market position for entrants?

Fastest connections? ~6 Mbps, 25 th/30 in OECD

Lowest prices? 2008 data 12 th most expensive in OECD

So… Is Competition Working? • Incumbent telcos argue that the market is “fiercely competitive”, “vigorous competition” • Starting to see some higher speed services in the big cities • There hasn’t been much competition on prices and speeds. This may be changing, but… – FB competition on ‘soft’ aspects, e. g. bundling, add-ons – Throttling is an issue, also download caps

“I don’t know how competitive I could even say it is today. If you look back in the dial-up days, the independent ISPs made up a very large chunk of the competitive market. It was actually independent ISPs that started dial-up Internet. The ILECs came later to that market. So at one time there were many, many players in that broadband access market. Now it’s almost primarily the cable companies and the phone companies. ”

What about Local Loop Unbundling? What we need to know is “how effective was the unbundling and what were the outcomes? ” (Taylor Reynolds, OECD)

“I might as well have been selling washers and dryers. There are endless things I should have done instead of being an ISP, really there are just a few of us left. ”

• Wholesale aggregated DSL (not")

Degrees of Unbundling • Resale (‘white label’ DSL, ‘rebilling’) • Wholesale aggregated DSL (not quite bitstream) • Line sharing (incumbent still provides voice) • Full unbundling • Ladder of investment suggests that market entrants will increase investment in their own facilities over time, but…

Issues of Concern to Independents Wholesale DSL may be subject to: • Traffic shaping practices Limited possibilities for differentiation of • Usage-based billing services, reduced • Speed restrictions choice for consumers BUT: these would not be problematic if the independents co-located and used their own equipment • No statistics available, but we believe colocation is not very common

Much Uncertainty for Independents • To date, market entrants have had little traction with the regulator • Several hearings regarding the wholesale broadband market underway or upcoming • Independents are now seeking public support for fight against incumbent wholesale practices

http: //www. competitivebroadband. com

ISP Ideas for Improving the Situation • Broadband has ‘fallen off’ the government agenda in Canada, needs attention again • Effective regulation of wholesale broadband is essential, improve accessibility to regulator for non-incumbents • Structural/functional separation • Reduced regulation (let the incumbents and independents figure it out on their own)

Conclusions and Questions • LLU is not a yes/no proposition, need to understand how it works, level of control • Is there a future for the independent ISP in Canada? Should there be? • What should the regulator be doing to ensure competition? (part of its mandate) • What about transitioning to Next Generation Networks? What is needed to ensure competition for higher speed networks?

bf4739b897d4aa589c307395aa15ceae.ppt