f0c3bbcfb6c7645dbab1222d7426dd12.ppt

- Количество слайдов: 72

HOUSE COSTS

Cost Object

HOUSE COSTS

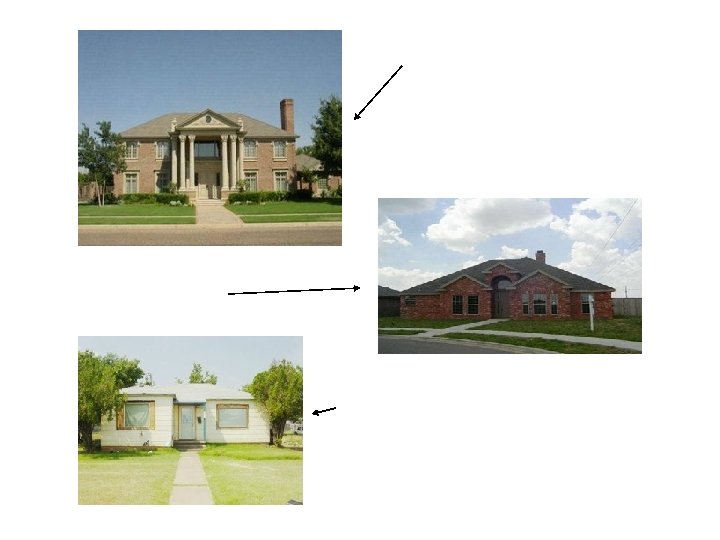

Use of Cost Drivers to Accumulate Costs

Overhead Cost Allocation

COST POOL

Cost Pool Allocation

Estimated Versus Actual Cost

Estimated Versus Actual Cost

Estimated Versus Actual Cost

Identifying Direct Versus Indirect Costs

Identifying Direct Versus Indirect Costs

Identifying Direct Versus Indirect Costs

Identifying Direct Versus Indirect Costs

Allocating Indirect Costs to Departments

Allocating Indirect Costs to Departments

Allocating Indirect Costs to Departments

Allocating Indirect Costs to Departments

Allocating Indirect Costs to Departments

Allocating Indirect Costs to Departments

Allocating Indirect Costs to Departments

Allocating Indirect Costs to Departments

Allocating Indirect Costs to Departments

The Effects of Cost Behavior on Cost Driver Selection

Using Volume Measures to Allocate Variable Overhead Costs

Using Volume Measures to Allocate Variable Overhead Costs

Using Volume Measures to Allocate Variable Overhead Costs

Using Volume Measures to Allocate Variable Overhead Costs

Using Volume Measures to Allocate Variable Overhead Costs

Selecting the Best Cost Driver

Allocating Fixed Overhead Costs

Allocating Fixed Overhead Costs

Allocating Fixed Overhead Costs

Allocating Costs to Solve Timing Problems

Allocating Costs to Solve Timing Problems

Establishing Cost Pools

Establishing Cost Pools

Allocating Joint Costs Product

Allocating Joint Costs

Allocating Joint Costs Consider the following example of an oil refinery. We will assume only two products, gasoline and oil.

Allocating Joint Costs

Joint Cost Allocation Methods

Joint Cost Allocation Methods Let’s look at an example illustrating the joint cost allocation methods.

Physical Quantities Method

Physical Quantities Method

Physical Quantities Method

Physical Quantities Method

Relative Sales Value Method

Relative Sales Value Method

Relative Sales Value Method

Relative Sales Value Method

By-Products

Joint Costs and the Issue of Relevance

Cost Allocation: The Human Factor

Cost Allocation: The Human Factor

Cost Allocation: The Human Factor Who is happy? Who is unhappy?

Cost Allocation: The Human Factor Now let’s allocate the $36, 000 budget based on the number of faculty in each department.

Cost Allocation: The Human Factor is unhappy? Who is happy? Who

Cost Allocation: The Human Factor Now let’s allocate the $36, 000 budget based on the number of students in each department.

Cost Allocation: The Human Factor is unhappy? Who is happy? Who

End of Chapter Five

f0c3bbcfb6c7645dbab1222d7426dd12.ppt