794ddabfd5edd0c60ca6ae8edd6986f5.ppt

- Количество слайдов: 102

History of Beer • Historians think pre-historic people made beer well before they made bread. • Babylonian clay tablets from 4300 BC include detailed recipes for beer. • Beer was brewed in Babylonian, Assyrian, Egyptian, Hebrew, Chinese and Inca cultures. • 1200 AD – Beer making commercialized in England, Germany and Austria. • 1420 – German brewers develop the lager method of brewing • 1490’s – Columbus discovered Indians making beer from corn and black-birch sap • 1516 – Bavarian brewers guilds push the Reinheitsgeobot Purity Laws, outlawing the use of anything but water, barley and hops in beer making. Source: www. beermachine. com

How Beer is made 1. 2. 3. 4. 5. 6. 7. 8. 9. Milling Mashing Boiling Cooling Fermenting Filtering Conditioning Pasteurizing Packaging Main Ingredients: • Malt • Hops • Yeast • Water

Aging and Alcohol Consumption • Aging and alcohol consumption are inversely related. • A person drinks most in their 20 s than in 30 s or later. • As people age, they tend to drink more wine and spirits.

Threat of New Entrants • Threats of new entrants: – Barriers to entry: • • Capital Intensive Distribution networks and agreements Regulations and Taxes Microbrewers are subsidized in Canada – Economies of scale in marketing, production and distribution.

Rivalry • Price competition – Increasing in Canada, particularly Eastern Canada – Increasing competition from imported beers (however, national brewers own part of these breweries). – 2, 200 wholesalers. – 560, 000 retail establishments. – Growing popularity of micro-breweries and other craftbeers. – Alternative: expansion to super-premium beers and other segments with lower demand elasticity.

: – Growth in: • • Wine increasing in")

Threat of Substitutes • Substitutes (Growing): – Growth in: • • Wine increasing in popularity Spirits and Premixed drinks. Alternative malt beverage. Alternative non-alcoholic drinks (from juices to mineral water). – However, beer remains the most consumed alcoholic beverage in the world.

Beer – losing ground to Wine & Spirits

Buyers Bargaining Power • Varies between market segments and demographics, but in general: • Low switching costs • Price competition • Increasing health conscience. • Craft-beers and Microbrewers: which are perceived as having higher quality, these characteristics may not always hold.

Supplier Bargaining Power • Low • Beer uses only a few ingredients – plentiful sources. • Supplies come from competitive industries which are more fragmented than the beer industry: – Farmers. – Labor (the case of unionized labor). • The more consolidated supplier is that one supplying bottles/cans.

Global Industry

US Industry

US Industry

China

Europe Western Europe The Western European beer market is one of the most profitable in the world. In 2004, the beer market declined slightly as a result of the relatively poor summer, weaker European economies and unfavorable demographics. The combination of these elements caused a general decline in the on-trade. In overall volume terms, the offtrade grew but was dominated by increasing competition on price at a retail level as supermarkets fought to win and retain customers.

Europe Central and Eastern Europe is one of the world’s largest beer markets by region. Many markets have belowaverage per-capita consumption and countries are preparing to join the European Union. These elements are forecast to deliver an acceleration in growth of purchasing power, beer consumption and to expand the market for premium beer.

Europe & the World 1997 2003

Price Mix – Canadian Market

Western Canada • Q 2 2004: Growth up due to strike at Labatt's & Molson. • Q 2 2005: Poor spring and summer weather.

Eastern Canada Q 3 2003: Production failure at Guelph plant Q 3 2004: Buck a beer pricing begins in Ontario and Quebec. Q 2 2005: Poor weather conditions.

Business Description • Established in 1864 • Currently control by 5 th generation of Busch Family August A. Busch III – Chairman August A. Busch IV – Group Executive • • Principle business: Production/Distribution of Beer Packaging Entertainment 50. 2% Domestic Market Share

Business Description 2001 2004

Domestic Beer Products Value Priced Premium Priced 4 8 Busch Light/Ice Natural Light/Ice Budweiser/Light/Dry/Ice Light/Select Michelob Golden Draft/Light Michelob Amber Bock/Honey Lager/Marzen/ULTRA Kirin Light/Ichiban Tequiza Ziegen. Bock Amber/Light Bacardi Silver/03/Raz/Limon/Black Cherry/Green Apple BE Anheuser World Select Bare Knuckle Stout Redhook Products Widmer Above Premium 22 Malt Liquor 3 King Cobra Hurricane Malt Liquor Hurricane Ice 3 O’Douls/Amber Busch NA Non-Alcoholic

International Beer Products Anheuser Busch ABEL U. K. Italy Spain Ireland Stag Brewery Budweiser/Ice Michelob/ULTRA Heinekan Italia Budweiser Sociedad Anonima Damm Budweiser Guiness Ireland Budweiser Imported Anheuser World Imported O’Douls Imported Anheuser World

International Beer Products Anheuser Busch Mexico Korea Japan Canada Imported Groupo Modelo Oriental Brewing Budweiser Kirin Brewery Co Budweiser Labatt Brewing Budweiser/Light Busch/Light Budweiser/Light O’Douls Argentina (Chile/Uruguay) Compania Cervecerias Unidas – 10. 8% Budweiser Imported O’Douls

International Beer Products Anheuser Busch China Wuhan International Brewing 97% Tsingtao Harbin Brewery Current – 9. 9% Group $694 M, 2004 In 5 Years– 27% $182 Million

Packaging Metal Container Corporation • Manufactures beverage cans at eight plants and beverage can lids at three plants for sale to ABI and U. S. soft drink customers Anheuser-Busch Recycling Corporation • Buys and sells used aluminum beverage containers • Recycles aluminum containers at its plant in Hayward, California Precision Printing and Packaging, Inc • Manufactures pressure sensitive, metalized and paper labels at its plant in Clarksville, Tennessee Longhorn Glass Manufacturing, L. P. , Eagle Packaging, Inc. • Owns and operates a glass manufacturing plant in Jacinto City, Texas, which manufactures glass bottles for the Company's nearby Houston brewery • Manufactures crown and closure liner materials for ABI at its plant in Bridgeton, Missouri

Family Entertainment

Growth – Domestic Beer 2001 $12. 9 Billion 2004 $14. 9 Billion

")

Growth – International Beer Barrels (Millions)

Growth – Packaging

Growth – Family Entertainment • Third Largest Amusement Park Operator in US • Approximately 20 Million Visitors Annually • Growth Due to Higher Admission Prices & In Park Spending • Adversely Effected by Florida Hurricanes in Q 3 & Q 4, 2004 • Adventure Island, FLA • Sea World, FLA

Q 3 YOY • Domestic Volume down 2. 1% Mgmt Sights: 1. Deferred price increase 2. Hurricane Katrina • International Volume up 70%. • Up 3. 4% excluding Harbin due to increased volume in U. K. , Canada & Mexico, and higher Budweiser sales in China

Profitability

Management Short Term Long Term

Income Statement

Income Statement: Key Figures

Balance Sheet

Balance Sheet

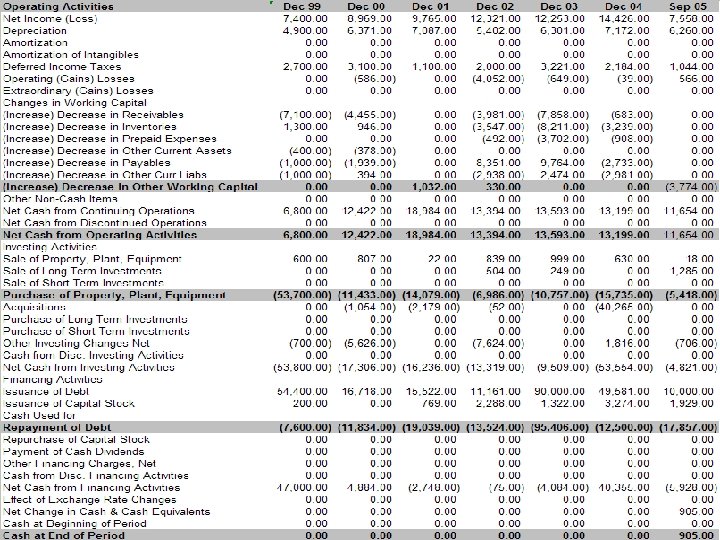

Cash Flow Statement

Stock Price

Actual Dividend Growth (2000")

Valuation Dividend Discount Model K Actual Dividend Growth (1984 -2005) Actual Dividend Growth (2000 -2005) 2005 Dividend Implied Stock Price Actual Stock Price (Feb 13, 2006) Implied Growth Rate Implied K at g = 10. 33% 9. 44% 10. 71% 10. 33% $1. 03 N/A $40. 57 6. 90% 12. 87% β (SP & BUD 04/83 – 02/06) Market Risk Premium (10 yr, SP 1953 -2005) Rf (10 Yr 1953 -2005) 0. 609 8. 9% 4. 02%

Valuation II

Heineken N. V.

Origins • The Heineken family entered the beer business in 1864, when Gerard Adriaan Heineken bought a brewery in Amsterdam. • Over the past 140 years, under the leadership of four generations of the Heineken family and pursuing a policy of measured expansion and consistent brand development, Heineken has grown into one of the world’s leading brewing groups.

Profile • Heineken is on of the world’s leading brewers in terms of sales volume and profitability; it has presence worldwide through a global network of distributors • In volume terms it is the largest brewer and beverage distributor in Europe where they realize more than half of their sales • The Heineken brand, available in almost every country on the planet, is the world’s most valuable international premium beer brand.

Goal and Strategy • Heineken’s goal is to grow the business in a sustainable and consistent manner, while constantly improving profitability. Its strategy has four elements: – Strive to reach a leading position in attractive markets – Focus on capturing an ever-growing share of the premium and specialty beer market segment – Work to improve efficiency and cut costs in operations – Grow through selective acquisitions, so long as they create shareholder value • Heineken can therefore benefit from other company’s infrastructure and combine its sales and distribution of the Heineken brand with other strong local brands

Company ownership structure

Company ownership structure • 50. 005% of the shares of Heineken N. V. , is held by Heineken Holding N. V. , this company has no operational activities and is concerned with safeguarding the longterm continuity, independence and stability of Heineken N. V. ’s activities. • Heineken N. V. is responsible for all the operational activities and the company’s goal and business strategy • L’Arche Holding S. A. , a Swiss Company, is fully owned by the Heineken family. This company holds 50. 005% of the Heineken Holding N. V. shares • The net asset value and dividend policy of Heineken N. V. and Heineken Holding N. V. are identical. However, Heineken Holding N. V. trades at a discount

Executive Board • Tony Ruys: Chairman since 2002. Joined Heineken in 1993 after a career with Unilever NV in the Netherlands and abroad • Marc Bolland: Director since 2001. Joined Heineken in 1986 and has held various positions in the Netherlands and abroad • Jean-Francois van Boxmeer: Director since 2001. Joined Heineken in 1984 and has held various positions in the Netherlands and abroad • René Hooft Graafland: Director since 2002. Joined Heineken in 1981 and has held various positions in the Netherlands and abroad • Karl Büche: Director since 2004. Joined Heineken in 2004. Since 1972 he has held various positions in Brau Union AG

Executive Board Remuneration • As of 2005, the remuneration package of the Executive Board will include a base salary, an annual bonus and a long-term incentive • The fixed salary will account for 45% of the total remuneration package • The variable remuneration is divided equally between short-term and long-term • This will ensure a balanced focus, on both short-term and long-term performance

Executive Board Remuneration Base salary: • The base salary for the Chairman will be set 30% above the base salary for the members of the Executive Board Short-term incentive: • The emphasis of the short-term incentive will be on annual operational performance. • “Organic net profit growth” will be the measure to asses the operational performance • Organic net profit growth is identified as growth in net profit excluding exchange rate effects, changes in consolidation, amortization of goodwill, exceptional items and changes in accounting policies

Executive Board Remuneration Long-term incentive: • This long-term incentive will be a performance based share plan • Each year a number of shares will be conditionally awarded. The value of shares equals € 325, 000 for the members of the Executive Board and € 422, 500 for the Chairman • The performance condition will be total shareholder return, measured over a three year period relative to a performance peer group. If, over a three year period, Heineken performs better than the median of the peer group the Executive Board will be rewarded with shares • The shares will be subject to a holding restriction of two years

Executive Board Remuneration • • • Below median, no shares will be awarded At 6 th position, 25% of the target amount will vest At 5 th position, 50% of the target amount will vest At 4 th position, 75% of the target amount will vest At 3 rd position, a 100% will be granted • If Heineken is ranked first, the maximum number of shares will vest. This is 1. 5 times the target amount of shares. Heineken is currently ranked eleventh. • The performance peer group includes: Anheuser-Bush, Carlsberg, In. Bev, SABMiller, Scotish & Newcastle, Henkel, L’Oreal, LVMH/PPR, Nestlé, Numico, Unilever

Products and Brands • Heineken owns and manages a portfolio of beer brands. Its main international brands are Heineken and Amstel • The Heineken brand is positioned as a premium beer brand, except for its home market in the Netherlands; it is also the leading brand in Europe and Amstel is the third largest • In Europe, Amstel is positioned in the mid-priced segment, the largest segment of the market, and is available in more than 90 countries around the world • Heineken also owns and manages a strong portfolio of more than 120 top-selling brands that includes Cruzcampo, Zywiec, Birra Moretti, Murphy’s and Star • The company has a limited presence in the low-priced segment of the market

Products and Brands Heineken and Amstel brands

Products and Brands Heineken and Amstel brands • Total Heineken brand volume rose to 11. 4 millions of hectoliters in the first half of 2005. The Heineken brands performed strongly in Central and Eastern Europe, Africa, Asia and Latin America • Amstel sales volume were stable at 5. 3 millions of hectoliters in the first half of 2005, with substantial growth in Africa, offset by lower volumes in some European markets • In 2004, total sales volume was made up as follows: the Heineken brand 18. 7%, Amstel 9. 1% and other beer brands 72. 2%

Sales by Region • Heineken divide the world beer market in five regions as follows: Western Europe • As of June 2005, performance in Western Europe was mixed, with some Southern European markets showing difficult economic environments and low consumer spending

Sales by Region • Despite lower beers sales volume, better prices were achieved in all major Western European countries, in both the on-trade and the off-trade. • Cost savings and efficiency improvements positively contributed to EBIT growth. However, EBIT was negatively affected by € 34 million of exceptional charges relating to production improvements in France • Heineken brand premium volume in the first half grew 0. 8% despite lower sales volume in the declining French market. Growth in other markets remained healthy, particularly in Spain • In the Netherlands, sales volume was low, only partially offset by improved price and sales mix and lower costs

Sales by Region • In Spain, turnover and EBIT increased due to higher sales volume, price and sales mix. The construction of the new brewery in Seville (€ 233 million project) with a capacity of 4. 5 millions hectoliters, will be finished at the end of 2006 and production reaching full capacity in 2008 • In Italy and the UK, volumes were up Central and Eastern Europe • In the first half of 2005, net turnover and group volumes were up, partially as a result of the first-time consolidation of the new breweries in Russia and Germany • Bulgaria, Austria and Slovakia showed lower volumes due to higher excise duties

Sales by Region • In the first half of 2005, net turnover and group volumes were up, partially as a result of the first-time consolidation of the new breweries in Russia and Germany • Bulgaria, Austria and Slovakia showed lower volumes due to higher excise duties • Integration activities at Braun Union, which started in 2004, have been completed. A total of 11 breweries and malteries have been closed so far • In Poland, the restructuring of Group Zywiec distribution system and the closure of breweries in 2004 had a good impact in turnover and EBIT • Russia increased sales volume as a result of the first-time consolidation of acquisitions (4 new companies)

Sales by Region • Russia increased sales volume as a result of the first-time consolidation of acquisitions (4 new companies) • In Austria, due to a real estate divestment, EBIT was low • In Greece, turnover rose slightly despite lower volumes, thanks to cost control and improved pricing The Americas • In the first half of 2005, the performance of the Heineken group was mixed, with the Latin American operations (Chile and Argentina), driving the organic growth in the region and compensating the slower first half in the USA • The joint-venture with Femsa S. A. for the USA started in January 2005. Femsa’s Mexican brands grew in volume

Sales by Region Africa and the Middle East • As of June 2005, the performance varied across the region, with strong results in Nigeria and South Africa and weak results in the Middle East. • Sales volume of Heineken and Amstel grew by 14% and 20% respectively. The Fayrouz brand in Egypt also grew Asia Pacific • In 2004 in China, Heineken and Asia Pacific Breweries merged and created Heineken Asia Pacific Breweries China (HAPBC). In 2005 HAPBC acquired a 40%-stake in Da. Fu. Hao Breweries in Jiangsu, which recently acquired a brewery in Wuijang

Sales by Region

Financial Statements

Financial Statements

Financial Statements

Financial Analysis Statement of Income • As of June 2005, net turnover of the company rose by 5. 8% to € 5. 1 billion (€ 4. 9 in June 2004). At the end of 2004 net turnover rose by 8. 1% to € 10. 0 billion. Both increases were due to price/mix improvements and net volume growth

Financial Analysis • In 2004, the operating profit rose 2% to € 1. 25 billion despite the negative impact of exchange rate movements of € 158 million • New acquisitions added € 93 million to operating profit before amortization of goodwill of € 50 million • Income from non-consolidated participating interests declined by € 241 million to € 140 million negative. This decrease was due to the € 190 million impairment charge on Heineken’s 20% participating interest in Cervejerias Kaiser and must be viewed against the exceptional net gain of € 71 million in 2003 on the sale of the 15% interest in Argentinean brewing group Quilmes

Financial Analysis • Net interest charges rose to € 180 million, reflecting the higher interest charges in connection with loans raised to finance acquisitions • Net profit was down 32. 7% to € 537 million and earnings per share declined to € 1. 10 (€ 1. 63 in 2003)

Financial Analysis Balance Sheet and Cash flow statement • As of June 2005, cash flow from operations remained stable at € 566 million compared with € 574 million in the first half of 2004. Lower tax payments were offset by a seasonal increase in net working capital. The sale of real estate assets in Austria also added € 238 million net of tax to the total cash inflow. • In 2004, cash flow from operations decreased to € 1, 520 million from € 1, 637 million in 2003. Net investments in tangible assets added to € 637 million. A total of € 1, 049 million was invested in new acquisitions and expanding existing interests.

Financial Analysis • This refers to the second phase of the Brau Union acquisition in Austria (39. 7%), Shikan Brewery (95. 1%), Volga Brewery (100%) and Sobol Brewery (100%), the increased stake in Dinal (48%) and other acquisitions in Europe

Financial Analysis • The leverage ratio displayed by the company is the result of its continuous process of acquisitions in the industry. This process is also reflected in the increment of its long-term debt throughout time • The profitability of the company has been decreasing over time due to the tight competition in the American market and the downside in many European economies during the last years

Stock Analysis • Heineken’s stock is traded on the U. S. OTC under the symbol HINKY. PK. As of February 17, 2006 HINKY traded at US$35. 20 or € 29. 63 (1€ = US$1. 18789)The following chart shows HINKY’s 5 year stock performance

Stock Analysis Gordon’s Growth Model • This model can be used to valuate a company in a mature industry. Heineken’s dividend growth is likely to be steady, therefore: Value of stock = DPS 1/(k-g) and DPS 1 = DPS 0(1+g) k = (DPS 1/P 0)+g Where: DPS 1 = expected dividend paid out in one year k = required rate of return on investment g = the assumed constant growth rate for dividend P 0 = current stock price

Stock Analysis • In this case g = 0. 05 (the average of the last 5 years dividend growth on the stock) DPS 1 = € 0. 40(1+0. 05) DPS 1 = € 0. 42 k = (DPS 1/P 0) + g k = (€ 0. 42/€ 29. 63) + 0. 05 k = 0. 0641748 • Because Heineken’s k looks small compared to the one showed by its peer Anheuser-Busch (k = 9. 44), we calculate the β for Heineken, (β=0. 276627 ≈ 0. 28) which reflects the lower cost of capital that Heineken shows in Europe, where it displays more than 80% of its revenue

Recommendation • The actual price of the stock is € 29. 63 or US$35. 20 which is in line with the value obtained • Taking into account that the expected growth in the beer industry will be minimum or flat, and given the tight situation in Europe and the continuous process of consolidation in the industry, we recommend to HOLD the stock • Over the last years Heineken’s growth has been determined principally by its continuous process of acquisitions and resulting synergies, (basically a zerosum game) rather than in its presence in other markets

SLEEMAN BREWERIES LTD TSX: ALE

The Company • Established in 1985. • Produces, sells, markets, and distributes Sleeman line of Premium beers, as well as several regional craft-brewed beers. • It is the leading brewer and distributor of premium beer in Canada and the third largest brewing company nationwide (after Molson and Labatt's).

• • • History 1834 - John H. Sleeman establishes himself as a brewer and malter. 1851 - JHS purchases property in Guelph for the Silver Creek Brewery. 1898 - Recipe for Sleeman Cream Ale is brewed. 1900 - Sleeman Brewing and Malting Company is incorporated. 1933 - George A. Sleeman is caught smuggling beer into Detroit. Faced with two choices: 1. Pay the beer taxes and get out of the brewing business. 2. Lose the brewery. He chose to pay the taxes, and sold off the brewery. Sleeman brewery closes.

History – more recent • 1984 - John Sleeman receives the leather bound Sleeman recipe book and an original heritage bottle from his Aunt. He decides to revive the family business. • 1985 - The Sleeman Brewing and Malting Company is incorporated on October 29 th. • 1991 - Sleeman doubles brewing capacity to 200000 HL (60 MM bottles) and has 1% of the Ontario beer market. • 1992 - Sleeman Cream Ale is exported to Detroit, Michigan. • 1997 - Sleeman Honey Brown Lager is launched - most successful product launch in company's history. • 2002 - Sleeman launches Cans in unique "barrel" cans. • 2004 - Sleeman acquires Unibroue

• • Sleeman Brands Sleeman Upper Canada Okanagan Spring Seigneuriale Shaftebury Maritime Beer Unibroue

Distribution Agreements • Imports and distributes well-known international brands. • 2006: Agreement to produce and distribute Sapporo in Canada. • National distribution network.

Sleeman Premium Beers

. • Not a major")

Value Brands • Mainly marketed in the Eastern segments (Ontario). • Not a major focus, but company will Stratify brands, with Pabst at the bottom and Old Milwaukee as sub-premium.

Business strategy • Manage costs and increase efficiency: Cost Control – decreasing cost per Hectoliter. • Grow premium brands. The company recognizes that it won't win by engaging in a price war, and is thus placing itself mainly as a premium beer marketer for its brands, particularly in the Western segments. • Continue to compete with “Buck-a-beers” with its own value line: Pabst, mainly in Eastern segment. • Expand US business, using Sleeman Cream Ale as its lead brand. • Pursue other strategic acquisitions – particularly other premium craft-brewers.

SWOT Analysis TSX: ALE

Strengths • Strong brand name. Has clearly distinguished itself from the two big brands, Labatt’s & Molson. • Unique packaging on both Bottles & Cans. – sets apart from competitors. • National distribution network. • Clear acquisition strategy: Organic growth and to buy other premium microbreweries.

Weaknesses • Debt-ridden company. • No cash. • Not large enough yet to realize real economies of scale or to compete on price. • Susceptible to the seasons – 2004 had poor summer weather across the country. • Susceptible to other factors – NHL Lockout.

Opportunities • U. S. markets: Sleeman & Unibroue brands are the most recognizable Canadian premium beers. • Unibroue has distribution to 34 states. • Oct 2005: Ontario raised floor prices from $24. 00 to $26. 40 (incl. deposit) • New deal with Quebec retailers.

and its market segment has been very")

Threats • “Buck-a-beer” competitors (Lakeport, Brick Brewing) and its market segment has been very successful, and is here to stay. • Molson, Labatt’s have slashed prices to compete. • Other Tax-subsidized Microbreweries • Increasing popularity of wine and spirits for younger demographic.

Financial Analysis TSX: ALE

Income Sheet SOURCE: COREREFERENCE

Income Statement Analysis • Slowdown in Revenue generation, Zero growth since 2003 (but no decline). • Net income estimate for 2005 will be lowest since 2001. • Widening gap between Revenues, EBITDA and Net Income: Inefficiency and lack of cost control.

Sleeman - Efficiency

Balance Sheet

Balance Sheet • Increasing Debt and L/T debt. • No cash until last Qtr Q 3 2005. • Increasing Inventories – reflect no growth in sales • Increasing Receivables • Increasing Intangibles that make up an increasing portion of Total Assets. • General trend of increasing Current Liabilities.

Cash Flow Analysis

Valuation • No dividends given in company’s history • Multiples Valuation Used: • Conservative EPS estimated 2006 at 0. 70 (vs. Q 3 2005 report of $0. 60 -$0. 65)

TSX: ALE

Recommendation HOLD

794ddabfd5edd0c60ca6ae8edd6986f5.ppt