991ecb9fcdfcf699a1cad6a2bb3e0bba.ppt

- Количество слайдов: 98

Hillsborough County Consumer Protection Agency 8900 N. Armenia Avenue, Suite #226 Tampa, FL 33604 (813) 903 -3430 www. hillsboroughcounty. org/consumerprotection

Who Are We? n The Hillsborough County Consumer Protection Agency was established in 1994. n In 2000, a reorganization plan was approved to rebuild the agency and increase its size.

New Ordinance n In 2006, Commissioners approved a new Consumer Protection Ordinance giving the agency additional enforcement tools.

Florida CPA’s 1. Pinellas County Office of Consumer Protection n 2. Broward County Consumer Affairs Division n 3. New Port Richey, FL Orange County Consumer Fraud Unit n 6. Miami, FL Pasco County Consumer Affairs Division n 5. Fort Lauderdale, FL Miami-Dade County Consumer Services Department n 4. Clearwater, FL Orlando, FL Palm Beach County Division of Consumer Affairs n West Palm Beach, FL

Mission To enforce consumer protection laws To protect and educate Hillsborough County Consumers, in the marketplace and business community, against economic losses resulting from n n • • • Unfair deceptive or illegal business practices.

Who Do We Serve? n All residents and visitors of Hillsborough County. n Anyone who may have experienced a problem with a company or business in Hillsborough County n Jurisdiction

Advise, Information & Assistance n Clearinghouse of information for consumers. n Consumers can call us or visit our website at: www. hillsboroughcounty. org/consumerprotection

Complaints n n CPA intakes approximately 100 formal and many informal complaints per month. The topics and issues of these complaints vary greatly in terms of severity and complexity.

Frequent Complaints n n n Failure to perform Quality of workmanship Lease agreements & security deposits n n n Landlord/tenant issues involving the health, safety and condition of the property should be referred to the County’s Housing & Community Code Enforcement department. Billing & credit disputes Warrantees Criminal theft & fraud Unlicensed activity Advertising

Investigations n Consumers are asked to submit their complaint in writing n n n Provide supporting documentation Include a timeline of events and steps taken to resolve the complaint. Complaints are evaluated by the Chief Investigator to determine if there is reasonable grounds to open an inquiry.

Investigations Investigator assigned the complaint begins a background investigation. n Investigator will make contact with consumer within 5 days of receipt of complaint. n Investigator makes initial contact with the business by sending a letter notifying them of the compliant and requesting a response within 10 days. n

Mediation n Mediation is handled through n Telephone contact n Certified letters n Field visits n Informal office meetings Agency is committed to making consumer whole. n When appropriate, referrals are made to other agencies. n

Criminal Investigations n Criminal conduct involving theft, fraud and some unlicensed activity may lead to arrest and criminal prosecution. n Criminal cases are referred to the appropriate prosecuting agency. n State Attorney’s Office n Statewide Prosecutor n U. S. Attorney General

Statistics n Last year, the agency recovered in excess of $1. 6 Million on behalf of consumers. n Recovery includes: n Cash recovery n Cash savings n Service recovery

Citation Authority n Investigators are now able to directly issue citations that will be processed by the county court system. n Repeat violators and gross conduct can warrant a citation. n Violators can receive a financial penalty of up to $500, and a court appearance.

Outreach & Education n Goal is to educate the public on being a good consumer n Education is the first line of defense in protecting consumers from victimization.

Outreach & Education n Community n n Education Programs Civic Groups & Organizations Senior Groups & Organizations Hispanic Groups & Organizations High School Students

Outreach & Education n CPA participates in Community Health, Financial and Safety Fairs n Active Volunteer Program with 8 Senior volunteers who enhance our efforts.

")

Legal Advocacy Twice a month (2 nd and 4 th Friday of each month) we schedule appointments to meet senior consumers in both the Sun City Center and Plant City areas. n The agency teams up with the HC State Attorney’s Office to provide assistance to seniors that want to speak with someone in person. n

SCAMS, SCHEMES & SCOUNDRELS

Identity Theft – No. 1

ID Theft n. Phishing n. Vishing n. Smishing n. Synthetic ID Theft n. Medical ID Theft

Synthetic ID Fraud vs. True-Name ID Fraud n Synthetic ID Fraud Combine fake & real consumer information n Or all false information to open an account n SS#’s and/or names might be changed to create new identities n n True-Name ID Fraud Consumer’s real identifying information is used without modification n The fraudster poses as the actual consumer n

Synthetic ID Fraud n n n Mainly hurts creditors Consumers end up paying for the fraud losses through fees and higher interest rates. Creates subfiles at the credit bureaus. Additional credit report information tied to a real consumer’s SS#, but someone else’s name. n The negative information gets entered under a subfile that is linked to, but doesn’t belong to you. n

Medical ID Theft

Medical ID Theft n Medical consequences n the medical information and records of the thief become intermingled with your records. n The financial consequences n unpaid bills n serious blemishes on credit reports n and harassing calls from collection agencies.

Victims of Medical ID Theft As medical-record-keeping systems evolve toward electronically based interconnected systems, the potential for catastrophic errors is on the rise. n Victims find it difficult to get their health care and insurance records corrected. n Victims are many times forced to sue their health care providers. n

How Does It Happen? There is a huge black market for medical records. n Medical records sell for $50 each on the street verses Social Security numbers that go for $1 or $2. n Health care provider employees are many times paid by criminals or criminal organizations to obtain medical information in bulk. n

How Does It Happen? n Stolen records are then sold to individuals without insurance who are in need of n elective surgeries n or other expensive treatments. n The World Privacy Forum estimates that as many as 250, 000 to 500, 000 consumers have been victims of medical ID theft as of mid-2006.

Prescription For Disaster n Less than half of the health care facilities encrypt their data before transmission. n This lack of data security is potentially disastrous n HIPPA protections are riddled with loopholes.

Protection Tips n View your medical records. n n HIPPA requires health care providers to either supply you with the requested records within 30 days or ask for more time. World Privacy Forum’s website www. worldprivacyforum. org Contains several sample letters to use to request copies of your medical records. n Steps you can take to try to get your records corrected and amended. n n Keep a medical journal

SECURITY FREEZE LAW

What does a security freeze mean? u. Your file cannot be shared with potential creditors. u. If your credit files are frozen, even someone who has your name and Social Security number probably would not be able to obtain

How do I place a freeze? u Write to each credit bureau. u Credit bureaus charge $10 to place or remove a security freeze, unless you are age 65 or older or a victim of ID Theft. u Victims will be expected to provide – A copy of the police report – Investigative report or complaint

When will the freeze take effect? u 5 business days from receipt of your letter. u. You will receive a confirmation letter in 10 days with a PIN or password. u. Keep your PIN or password in a safe place.

Can I lift the freeze? u Yes. u There is no charge for seniors over 65 or victims. u Everyone else will be charged $10 for a temporary lift. u Credit bureaus must lift the freeze no later than 3 business days from receipt of your

Can I order my own credit report if it is frozen? u Yes. u Consumers can continue to receive their free annual credit reports. u There is only one Federal website, www. annualcreditreport. com u By phone call toll free at 1 -877 -322 -8228. u Do not contact the credit bureaus

Security Freeze u If a creditor requests your file, they will see a message or code indicating the file is frozen. u They will not be able to obtain your score. u You must freeze with all three credit bureaus. u The freeze will NOT lower your credit score.

Exceptions u. Certain entities still have access –Existing creditors –Collection agencies –Offers of credit –Government agencies

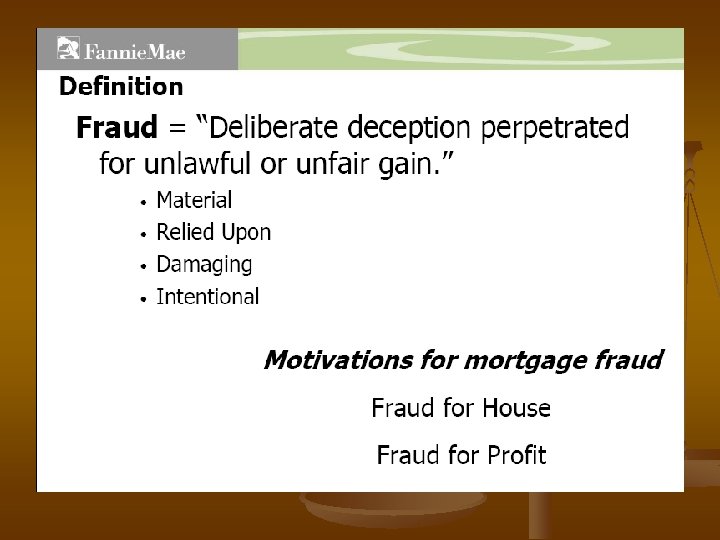

Predatory Lending or Loan Fraud

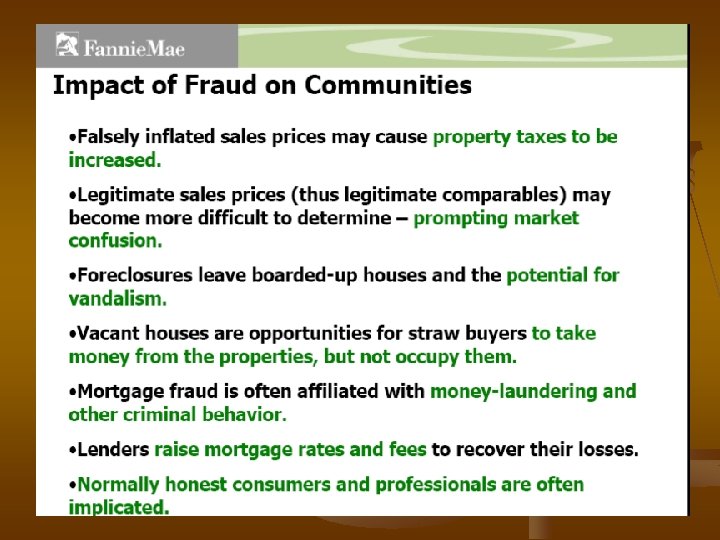

Florida, A Mortgage Fraud “HOT SPOT” Florida No. 1 for mortgage fraud in 2007 for 2 nd straight year. n Predatory Lending or Mortgage Fraud has risen to epidemic proportions in the U. S. n Financial Institutions are sustaining multibillion-dollar losses. n Consumer’s homes, are on the line. n

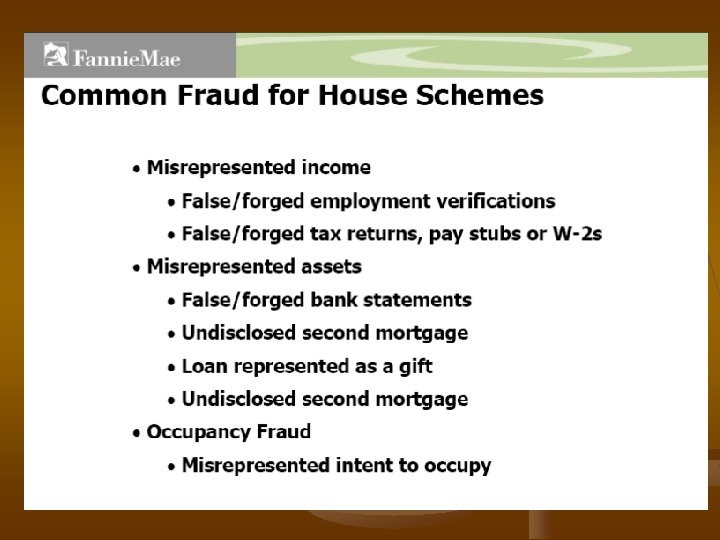

20% of Mortgage Fraud Cases

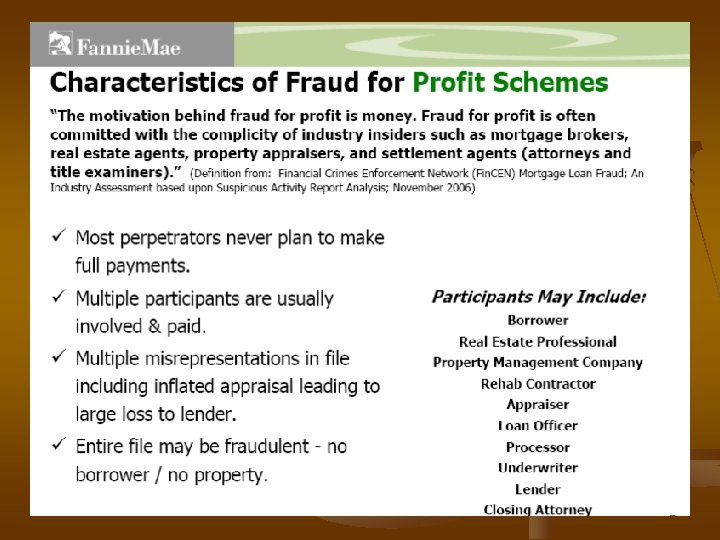

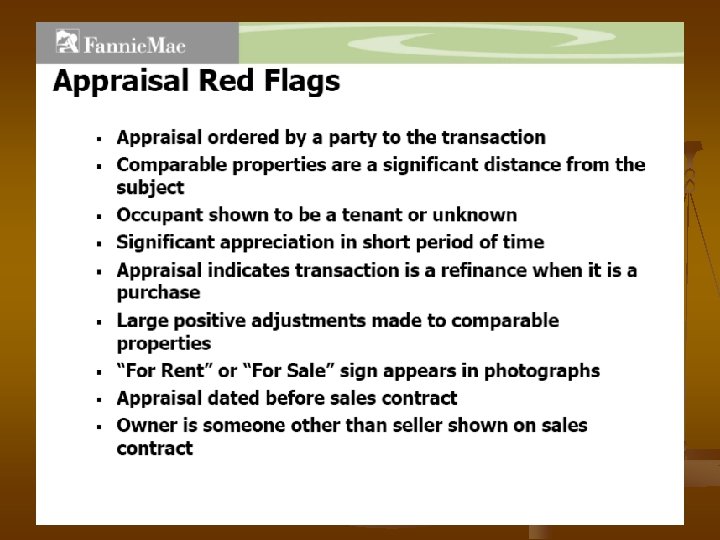

For-Profit Mortgage Fraud n Property Flipping The property is bought, falsely appraised at a higher value and quickly sold, sometimes several times in rapid succession. n Eventually, the mortgage goes into default. n The profits disappear with the criminal. n n Straw buyers n The identity of the borrower is concealed by using the name and credit history of a willing accomplice.

For-Profit Mortgage Fraud n Fake/Stolen Identity n n Inflated appraisals n n Stolen identities - along with credit histories - are used on a loan application. An appraiser agrees to inflate the property of the house. Equity skimming n n An investor uses a straw buyer to get a mortgage. Prior to closing, the straw buyer signs the property over to the investor, who in turn rents the property out without making any mortgage payments.

The Home Repair Scam

The Home Repair Scam n Use high pressure sales tactics to sell home improvements n They just happen to know someone who will finance the project. n Credit problems will not be a problem for them.

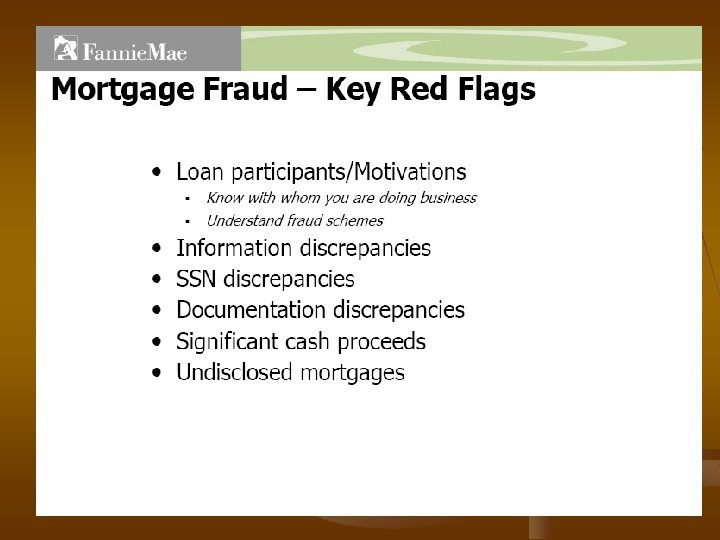

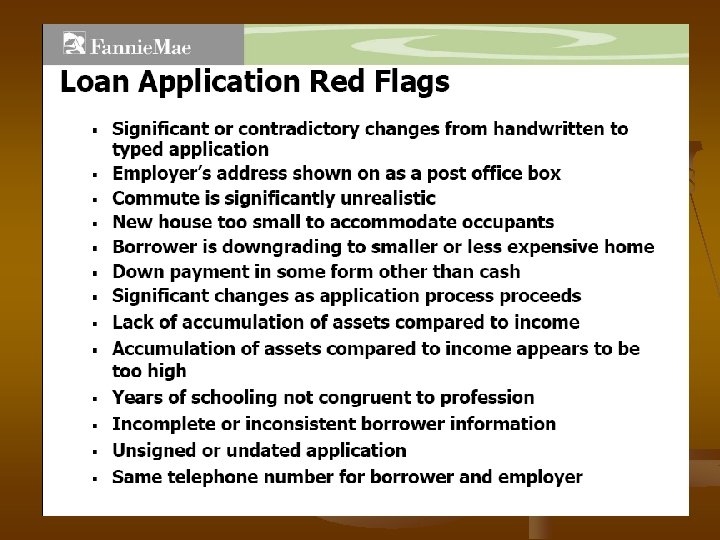

RED FLAGS n. A lender or investor tells the victim they are the only chance of getting a loan. n The victim is asked to sign a sales contract or loan documents that are blank or that contain information which is not true.

RED FLAGS n The cost or loan terms are not what the victim agreed to. n The victim is told that refinancing can solve their credit or money problems.

Mortgage Fraud CRIMINAL INVESTIGATION n n Beginning in 2003 a scheme was devised to solicit mostly minority consumers in poor and depressed residential areas promising to fix up their home for no money down. The defendants and their criminal enterprise submitted loan applications containing false, forged and counterfeit supporting documents without the consumers’ knowledge.

Mortgage Fraud CRIMINAL INVESTIGATION Once the loans were funded , the loans were closed at title companies without the presence of the consumers. n The funds were manipulated and distributed by the defendants with the title companies assistance and cooperation. n Notary fraud and forgeries were common in the closing of the loans. n

Mortgage Fraud CRIMINAL INVESTIGATION Of the 21 home improvement related loans, all of the construction funds were deposited directly into the defendants bank accounts. n Little to no work was done on the victims’ houses. n Some work that had been done was shoddy, incomplete and done by unlicensed contractors. n

Mortgage Fraud CRIMINAL INVESTIGATION n The victims were left with large loan balances due and none of the home improvement projects completed as promised. n Numerous fees were charged to the consumers during the closing process and pocketed by the defendants and others.

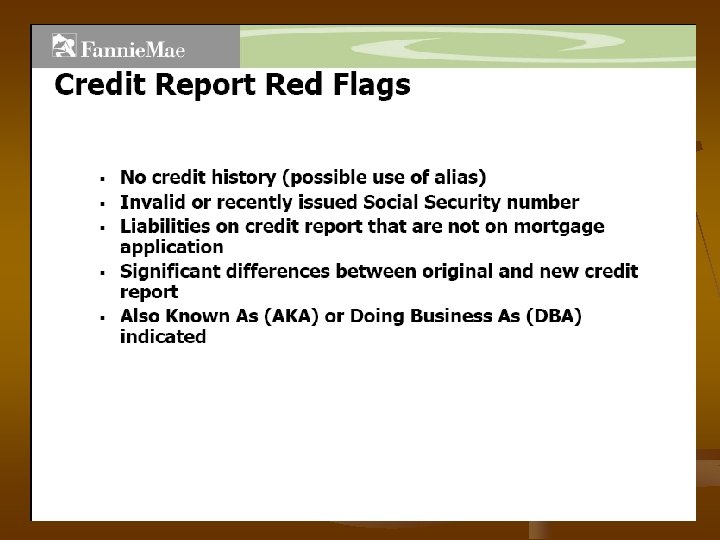

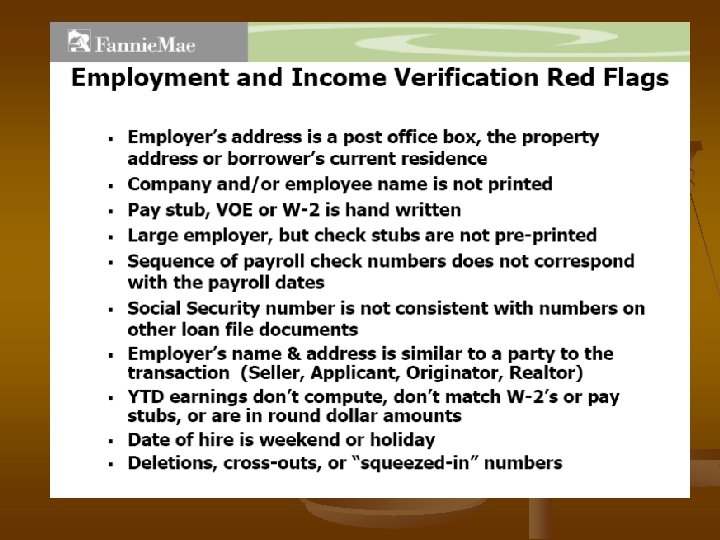

Mortgage Fraud CRIMINAL INVESTIGATION n It was commonplace and routine for each of the loans to contain fraudulent documents created or altered by defendants. Employment history n Income verification n Altered or phony W-2’s n Check stubs n Credit reports n Rental history verification checks n

Mortgage Fraud CRIMINAL INVESTIGATION n After a lengthy 3 year investigation, six defendants were charged with n Racketeering n Conspiracy to Commit Racketeering by fraudulently obtaining mortgages in the names of victims solicited for home improvement projects. n Defendants were also responsible for obtaining fraudulent loans on their own personal properties.

Mortgage Fraud CRIMINAL INVESTIGATION The 150 page arrest affidavit detailed the fraudulent activity in 31 residential mortgage loans totaling nearly $3 million. n The majority of the loans were submitted through and funded by ARGENT MORTGAGE COMPANY n n One of the nation’s largest wholesale “sub -prime” mortgage companies.

Mortgage Fraud CRIMINAL INVESTIGATION n Two defendants were former high ranking employees of ARGENT’S White Plains, NY office. n The two approved fraudulent documents and loan packages submitted by brokers. n They received tens of thousands of dollars in bribes or kickbacks.

ARGENT INSIDERS Orson Benn & Samuel Green

Defendants Scott Almeida, Frank Giffone & Adrienne White

Mortgage Fraud CRIMINAL INVESTIGATION n In addition to ARGENT, fraudulent loans were also approved by n Pinnacle Mortgage Company n Decision One Mortgage Company n Mortgage Lenders Network USA

Mortgage Fraud CRIMINAL INVESTIGATION n The other four defendants are all former owners, principals or employees of Hillsborough County Mortgage broker companies n n Advanced Mortgage Solutions Consumer Lending Resources First Commerce Home Funding In addition to the mortgage brokerage businesses, the defendants operated two phony home improvement companies n n Premier Quality Renovations Florida Beautiful Construction

Mortgage Fraud CRIMINAL INVESTIGATION n n n In total, approximately 180 loans were submitted by various mortgage broker businesses through ARGENT MORTGAGE COMPANY totaling nearly $18 million. At least 129 of those loans were funded in the amount of approximately $13 million. The investigation is ongoing and additional charges are anticipated against other associates related to the six defendants and their criminal enterprise.

Subprime Lenders

Subprime Lenders n Offer credit to individuals who otherwise might never be able to build home equity. n Not all subprime loans are predatory. n But virtually every predatory loan we have seen is a subprime loan.

Subprime Loans Buyer Beware Market! n What constitutes subprime? n n The credit score used to separate prime from subprime varies with the lender and loan. n Typically, below 600 is subprime n FICO n score from 600 to 650 gray area Consumers with scores in the mid-600 range were many times steered into subprime loans when they qualified for prime.

Easy Prey n Shady lenders targeted people with poor credit who had few other options. n Many times put elderly consumers with good credit into subprime loans.

Foreclosure “Rescue” Scam n n The “rescuer” identifies distressed homeowners through public foreclosure notices in newspapers or at government offices. The “rescuer” then contacts the homeowner by phone, personal visit, card or flyer left at the door, or advertising. “Stop foreclosure with just one phone call. ” n “I’d like to $ buy $ your house” n “You have options” n “Do you need instant debt relief and CASH? ” n

How to Spot a “Rescue Scam” n Call itself a “mortgage consultant, ” “foreclosure service, ” or something similar. n Contact or advertises to people whose homes are listed foreclosure, including anyone who sends flyers or solicits door-to-door or by phone.

How to Spot a “Rescue Scam” Collects a fee before providing services. n The victim is instructed to make their mortgage payments directly to the rescuer instead of the lender. n The victim is instructed to transfer their deed or title to the individual or company. n

Initial Visit n Offer a “fresh start. ” n Has “testimonials” n Instructs homeowner to cease contact with the lender and/or lawyers n They will handle all negotiations

Result n Once it is too late… the “rescuer” takes the home or drains the equity n Many homeowners are then evicted by their “rescuer”

Reverse Mortgages n A special type of home loan that allows homeowners who are 62 and older to borrow against their home equity without having to repay the money until the home is sold n or the borrower passes away n or moves out permanently n n These loans are popular options for seniors because they offer a cash source which can help meet unexpected medical expenses, supplement social security and more.

Reverse Mortgages n n Can serve a purpose when financed through legitimate lenders. Homeowners who take out a reverse mortgage can receive payments in A lump sum n One a monthly basis n Or on an occasional bases as a line of credit n n Homeowners whose circumstances change can restructure their payment options.

Reverse Mortgage Scams n n Deceptive practices and allegations of high pressure sales tactics are being more frequently encountered as senior citizens are being taken advantage of under the guise of a helpful and legitimate reverse mortgage. Borrowers also run the risk of being steered into inappropriate loans and annuities by sales agents and insurance brokers who could be working together without disclosing that relationship to the borrower.

Predatory Loan Red Flags n Balloon Payment n n n Borrowers with a balloon payment have a 46% greater chance of foreclosure. Too-large loan Excessive Fees Useless Services Credit card that taps your home equity High Interest Rate

Red Flags n Payday loan n Major Asset as collateral n Mandatory arbitration clause n Prepayment Penalties n Balance Transfer Fees n Lender solicitation n Teaser Rates

Consumer Tips n Shop and compare lenders and costs. n n www. bankrate. com Do not let anyone persuade them to make a false statement on their application, such as: n Overstating their income n The source of their down payment n Failing to disclose the nature and amount of their debts n Length of their employment

Tips n Be suspicious if anyone tries to steer them to just one lender. n Don’t let anyone convince them to borrow more money than they know they can afford to repay.

Tips n Never sign a blank document or a document containing blanks. n If information is inserted by someone else after you have signed, you may still be bound to the terms of the contract. n Insert “N/A” (not applicable) or n Cross through any blanks.

Tips n Read everything carefully and ask questions. n Do not sign anything they don’t understand. n Be suspicious if the cost of a home improvement goes up if they don’t accept the contractor’s financing.

Tip n Never take an unsecured debt like credit card debt and pay it off by securing your home.

Licensing n n n Ask to see a copy of the contractor’s proficiency license. All contractors are regulated by the State Department of Business & Professional Regulations (DPBR). You may call them at (850) 487 -1395 in Tallahassee or on the Web at www. My. Florida. License. com or by mail at Construction Industry Licensing Board, 1940 N. Monroe St. , Tallahassee, FL 32399 -1039

Licensing Visit the Hillsborough County website at www. hillsboroughcounty. org n Click on Contractor Licensing Reports n You can then search by license number, name, firm name or complaint. n Call HC Contractor Licensing Services at (813) 635 -7308 n

Verify Insurance n You may also contact your local Building Dept. n City of Tampa (813) 259 -1770 n Hillsborough County (813) 272 -5600 n Ask to see Certificates of Insurance for General Liability, Worker’s Compensation, and Automobile Insurance n This is crucial! n If your contractor damages your property or experiences injuries on the job, you could be held liable.

Avoiding Foreclosure n Communicate with your lender! If you seem like a good risk the lender will offer to help keep your mortgage afloat. n If you seem like a bad risk, the lender may cut its losses by taking steps to foreclose and evict you as quickly as possible. n n Repayment Plan n If you suffer a short-term financial setback, your lender may provide some breathing room by agreeing to let you pay off your missed payment in two installments of the next two months.

Avoiding Foreclosure n Loan Modification n Mortgage Servicers can adjust the terms of your loan n Lengthening the amortization schedule n Lowering interest rate n Rolling the delinquent amount into the loan and reamortizing the new balance n This will help you bring the loan current.

Avoiding Foreclosure n Short Sale n The lender allows you to sell the house for less than the outstanding loan amount. n The lender takes the proceeds and forgives any remaining debt. n Short n The Refinance lender forgives some of your debt and refinances the rest into a new loan.

HUD Approved Lenders n n n HUD-approved housing counseling agencies are available for free to provide information, counseling and free referral to a list of HUDapproved lenders. HUD 1 -800 -569 -4287 HUD’s reverse mortgage website n n http: //www. hud. gov/buying/rvrsmort. cfm Don’t use estate planning service or any service that charges a fee just for referring a borrower to a lender.

CONSUMER EDUCATION IS VITAL IN REDUCING VICTIMIZATION OF FINANCIAL CRIME.

Consumer Protection Agency THANKS YOU FOR ALLOWING US TO BRING YOU THIS IMPORTANT INFORMATION

991ecb9fcdfcf699a1cad6a2bb3e0bba.ppt