3dc29c0dab0b57921e2f38a9cf41e5ea.ppt

- Количество слайдов: 35

Futures markets u Today’s price for products to be delivered in the future. u A mechanism of trading promises of future commodity deliveries among traders. u Biological nature of ag production – Prices not known when production decision is made – Processors need year around supply

Futures markets u Today’s price for products to be delivered in the future. u A mechanism of trading promises of future commodity deliveries among traders. u Biological nature of ag production – Prices not known when production decision is made – Processors need year around supply

Futures Market Exchanges u 12 organized exchanges u Two largest – Chicago Board of Trade (CBOT) » Grains, interest rates » http: //www. cbot. com/ – Chicago Mercantile Exchange (CME) » Livestock, financial, currencies » http: //www. cme. com/ – Combined for 75% of futures volume

Futures Market Exchanges u 12 organized exchanges u Two largest – Chicago Board of Trade (CBOT) » Grains, interest rates » http: //www. cbot. com/ – Chicago Mercantile Exchange (CME) » Livestock, financial, currencies » http: //www. cme. com/ – Combined for 75% of futures volume

Futures Market Exchanges u Trading pits u Centralized pricing – Buyers and sellers represented – All information represented u Perfectly competitive market – Open out-cry trading

Futures Market Exchanges u Trading pits u Centralized pricing – Buyers and sellers represented – All information represented u Perfectly competitive market – Open out-cry trading

The futures contract u. A legally binding contract to make or take delivery of the commodity – Form (wt, grade, specifications) – Time (delivery date) – Place (delivery location) – Possession (seller delivers, buyer receives)

The futures contract u. A legally binding contract to make or take delivery of the commodity – Form (wt, grade, specifications) – Time (delivery date) – Place (delivery location) – Possession (seller delivers, buyer receives)

The futures contract u Standardized contract u No physical exchange takes place when the contract is traded. u Deliveries are made when the contract expires (delivery time) u Payment is based on the price established when the contract was initially traded.

The futures contract u Standardized contract u No physical exchange takes place when the contract is traded. u Deliveries are made when the contract expires (delivery time) u Payment is based on the price established when the contract was initially traded.

months u Fixed size of contract – Grains") Standardized contract u Certain delivery (contract) months u Fixed size of contract – Grains 5, 000 bushels – Livestock in pounds » Lean Hogs 40, 000 lbs carcass » Live Cattle 40, 000 lbs live » Feeder Cattle 50, 000 lbs live u Specified delivery points – Relatively few delivery points

Standardized contract u Certain delivery (contract) months u Fixed size of contract – Grains 5, 000 bushels – Livestock in pounds » Lean Hogs 40, 000 lbs carcass » Live Cattle 40, 000 lbs live » Feeder Cattle 50, 000 lbs live u Specified delivery points – Relatively few delivery points

Market position u Objective: Buy low, sell high u You can either buy or sell initially – Sell a December Corn contract initially » Short the market » Buy back at a later date – Buy a February Live Cattle contract initially » Long the market » Sell back at a later date

Market position u Objective: Buy low, sell high u You can either buy or sell initially – Sell a December Corn contract initially » Short the market » Buy back at a later date – Buy a February Live Cattle contract initially » Long the market » Sell back at a later date

Margin account u Highly leveraged trades – Margin is the earnest money that must be maintained in the trader’s account – Often 5 -10% of full value u Margin account settled everyday – Must maintain account balance – Margin call u Calculate as if you had to get out of the market every day.

Margin account u Highly leveraged trades – Margin is the earnest money that must be maintained in the trader’s account – Often 5 -10% of full value u Margin account settled everyday – Must maintain account balance – Margin call u Calculate as if you had to get out of the market every day.

Margin Account u Initial margin: The amount needed to open and account. u Maintenance margin: The minimum amount needed to keep and account open. u “Mark to the Market” at the close of each trading day.

Margin Account u Initial margin: The amount needed to open and account. u Maintenance margin: The minimum amount needed to keep and account open. u “Mark to the Market” at the close of each trading day.

Margin Account Example u Initial margin $1, 000 u Maintenance margin $800 u Corn contract (5000 bushels) – Day 1: Sell at 2. 55

Margin Account Example u Initial margin $1, 000 u Maintenance margin $800 u Corn contract (5000 bushels) – Day 1: Sell at 2. 55

Margin Account Example Day Price. Chg G/L Margin 1 2. 54 +. 01 +50. 00 1050. 00 2 2. 58 -. 04 -200. 00 850. 00 3 2. 61 -. 03 -150. 00 700. 00 Below Maintenance Margin must make $100 margin call 4 2. 52 +. 09 +450. 00 1250. 00 800. 00 Changes reflect the initial “sell” of the contract

Margin Account Example Day Price. Chg G/L Margin 1 2. 54 +. 01 +50. 00 1050. 00 2 2. 58 -. 04 -200. 00 850. 00 3 2. 61 -. 03 -150. 00 700. 00 Below Maintenance Margin must make $100 margin call 4 2. 52 +. 09 +450. 00 1250. 00 800. 00 Changes reflect the initial “sell” of the contract

Margin Account Example Note that you can calculate your margin account if you know the initial margin, any additions or removals and the current closing price.

Margin Account Example Note that you can calculate your margin account if you know the initial margin, any additions or removals and the current closing price.

Market participants u Hedgers are willing to make or take physical delivery because they are producers or users of commodity. u Speculators buy or sell in an attempt to profit from price movements.

Market participants u Hedgers are willing to make or take physical delivery because they are producers or users of commodity. u Speculators buy or sell in an attempt to profit from price movements.

Hedgers u Producers with a commodity to sell at some point in the future u Short hedgers 1 Sell the futures contract first 2 Buy the futures contract (offset) when they sell the physical commodity

Hedgers u Producers with a commodity to sell at some point in the future u Short hedgers 1 Sell the futures contract first 2 Buy the futures contract (offset) when they sell the physical commodity

Hedgers u Processors or feeders that plan to buy a commodity in the future u Long hedgers 1 Buy the futures first 2 Sell the futures contract (offset) when they buy the physical commodity

Hedgers u Processors or feeders that plan to buy a commodity in the future u Long hedgers 1 Buy the futures first 2 Sell the futures contract (offset) when they buy the physical commodity

Futures Speculators u Do not have the commodity nor need the commodity u They try to profit from price change

Futures Speculators u Do not have the commodity nor need the commodity u They try to profit from price change

Price discovery u Must be a buyer and seller for every transaction u Supply and demand still works – more sellers than buyers price falls – more buyers than sellers price rises

Price discovery u Must be a buyer and seller for every transaction u Supply and demand still works – more sellers than buyers price falls – more buyers than sellers price rises

Futures trade on information u Why would buyers buy? – They think that the price at delivery will be higher than it is currently. u Why would sellers sell? – They think that the price at delivery will be lower than it is currently.

Futures trade on information u Why would buyers buy? – They think that the price at delivery will be higher than it is currently. u Why would sellers sell? – They think that the price at delivery will be lower than it is currently.

corn price is") Futures Trade Example Day 1: Think that the new crop (Dec) corn price is going to decline Step 1: Decide to Sell a December corn futures contract by calculating expected price from hedging Futures bid $2. 34 Adjust for basis -. 31 Subtract commission -. 01 Expected hedge price $2. 02

Futures Trade Example Day 1: Think that the new crop (Dec) corn price is going to decline Step 1: Decide to Sell a December corn futures contract by calculating expected price from hedging Futures bid $2. 34 Adjust for basis -. 31 Subtract commission -. 01 Expected hedge price $2. 02

Futures Trade Example Step 2: Call your broker and place order to sell Dec corn at the market Step 3: Broker forwards order to CBOT where the broker's representative runs the order to the pit and tries to fill the order.

Futures Trade Example Step 2: Call your broker and place order to sell Dec corn at the market Step 3: Broker forwards order to CBOT where the broker's representative runs the order to the pit and tries to fill the order.

Futures Trade Example Step 4: The order is filled at $2. 34 Step 5: Broker calls to confirm fill Step 6: Send margin money to broker u Initial margin account level is $750 u Must maintain at least $600 in margin account at end of each day

Futures Trade Example Step 4: The order is filled at $2. 34 Step 5: Broker calls to confirm fill Step 6: Send margin money to broker u Initial margin account level is $750 u Must maintain at least $600 in margin account at end of each day

Futures Trade Example Day 2: Closing price is $2. 38 We sold at $2. 34 Market is $2. 38 We are behind by -$0. 04 On 5, 000 bushels = $200 Send broker $200 on Day 2

Futures Trade Example Day 2: Closing price is $2. 38 We sold at $2. 34 Market is $2. 38 We are behind by -$0. 04 On 5, 000 bushels = $200 Send broker $200 on Day 2

Futures trade example At some later date we decide to offset our position Last Day: Call broker and place order to buy Dec corn at the market Two things could have happened Prices are higher than initially Prices are lower than initially

Futures trade example At some later date we decide to offset our position Last Day: Call broker and place order to buy Dec corn at the market Two things could have happened Prices are higher than initially Prices are lower than initially

Futures trade example u Case 1: Prices are higher => $2. 56 u Calculate returns per bushels Sold on Day 1@ $2. 34 Bought back later @ $2. 56 Gross future return -$0. 22 Commission @ $50/contract -$0. 01 Net return per bushel -$0. 23 Local cash price $2. 25 Net price $2. 25 -. 23=$2. 02

Futures trade example u Case 1: Prices are higher => $2. 56 u Calculate returns per bushels Sold on Day 1@ $2. 34 Bought back later @ $2. 56 Gross future return -$0. 22 Commission @ $50/contract -$0. 01 Net return per bushel -$0. 23 Local cash price $2. 25 Net price $2. 25 -. 23=$2. 02

Futures trade example u Convert to contract returns Gross returns -$0. 23 Contract = 5, 000 bushels -$1, 150 Because we settled the margin account every day the broker has this amount plus at least $600 minimum margin. The remaining margin balance is returned.

Futures trade example u Convert to contract returns Gross returns -$0. 23 Contract = 5, 000 bushels -$1, 150 Because we settled the margin account every day the broker has this amount plus at least $600 minimum margin. The remaining margin balance is returned.

Futures trade example u Case 2: Prices are lower => $2. 20 u Calculate returns per bushels Sold Day 1 @ $2. 34 Bought back later @ $2. 20 Gross return +$0. 14 Commission @ $50/contract -$0. 01 Net return per bushel +$0. 13 Local cash price $1. 89 Net price $1. 89+. 13= $2. 02

Futures trade example u Case 2: Prices are lower => $2. 20 u Calculate returns per bushels Sold Day 1 @ $2. 34 Bought back later @ $2. 20 Gross return +$0. 14 Commission @ $50/contract -$0. 01 Net return per bushel +$0. 13 Local cash price $1. 89 Net price $1. 89+. 13= $2. 02

Futures trade example u Convert to contract returns Gross returns +$0. 13 Contract = 5, 000 bushels +$650 Because the margin account is settled every day the broker has this amount plus the $750 initial margin. We are returned the $1, 400.

Futures trade example u Convert to contract returns Gross returns +$0. 13 Contract = 5, 000 bushels +$650 Because the margin account is settled every day the broker has this amount plus the $750 initial margin. We are returned the $1, 400.

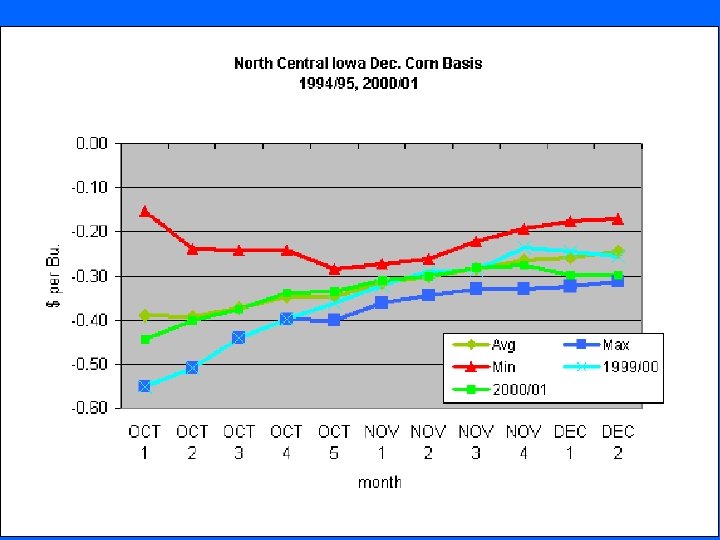

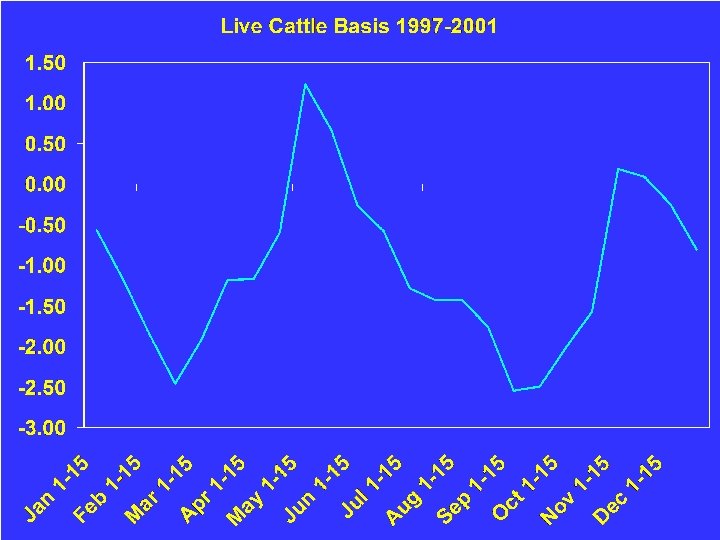

Relationship between futures and cash prices u Difference is call basis Basis = Cash - Futures u Grain Typically quote the absolute value “ 30 cents under” = $. 30 basis Cash is $. 30 less than futures u Livestock The sign is important

Relationship between futures and cash prices u Difference is call basis Basis = Cash - Futures u Grain Typically quote the absolute value “ 30 cents under” = $. 30 basis Cash is $. 30 less than futures u Livestock The sign is important

Basis u Reflects local conditions – Supply and demand » Yields, storage availability, processing capacity, rail cars, local usage u Individual basis impacted by factors that effect the local cash price relative to the delivery point price.

Basis u Reflects local conditions – Supply and demand » Yields, storage availability, processing capacity, rail cars, local usage u Individual basis impacted by factors that effect the local cash price relative to the delivery point price.

Basis u Differs by market – Time, place, and form u Basis includes – Storage to maturity – Transportation to delivery point – Grade differences

Basis u Differs by market – Time, place, and form u Basis includes – Storage to maturity – Transportation to delivery point – Grade differences

Basis generalities u Cash and futures move together u Basis narrows at contact maturity – Cash and futures converge – Arbitrage of delivery u Basis is more predictable than price u Basis generally follows a pattern – Seasonal patterns

Basis generalities u Cash and futures move together u Basis narrows at contact maturity – Cash and futures converge – Arbitrage of delivery u Basis is more predictable than price u Basis generally follows a pattern – Seasonal patterns

Position Diagram u 1. 2. Graph of expected payoff at alternative futures prices at contract expiration Futures prices on horizontal axis Expected net price on vertical axis Adjust for basis and commission if needed 3. 4. Start with current futures price Identify one other futures price Futures, cash, and hedge are linear

Position Diagram u 1. 2. Graph of expected payoff at alternative futures prices at contract expiration Futures prices on horizontal axis Expected net price on vertical axis Adjust for basis and commission if needed 3. 4. Start with current futures price Identify one other futures price Futures, cash, and hedge are linear

Net Price Short Futures = 45 o Long Futures = 45 o Long Cash Adjust for basis Hedge Adjust for basis Current Futures

Net Price Short Futures = 45 o Long Futures = 45 o Long Cash Adjust for basis Hedge Adjust for basis Current Futures