fea3235fb0ac2c99324ab25a0dbe9dca.ppt

- Количество слайдов: 23

Fraud Investigation-Latest trends and novel Methods National Housing Bank March 17 2010

Fraud Investigation-Latest trends and novel Methods National Housing Bank March 17 2010

Discussion in this session n Business scenario : home loan fraud Types and categories of fraud and common Causes and illustrations Novel and uncharted methods for fraud detection and prevention

Discussion in this session n Business scenario : home loan fraud Types and categories of fraud and common Causes and illustrations Novel and uncharted methods for fraud detection and prevention

Growth of housing loans n Housing loans grew from a level of Rs 16, 000 crore in 2001 to a level of Rs 1, 86, 000 crore in 2006

Growth of housing loans n Housing loans grew from a level of Rs 16, 000 crore in 2001 to a level of Rs 1, 86, 000 crore in 2006

What is more alarming is n n n Brazenly Big numbers: In a nationalised bank in Wadala Mumbai- there were 102 fraud HL between 2004 and 2006 from out of just 150 accounts Detected late – more than 4 – 5 years

What is more alarming is n n n Brazenly Big numbers: In a nationalised bank in Wadala Mumbai- there were 102 fraud HL between 2004 and 2006 from out of just 150 accounts Detected late – more than 4 – 5 years

Types and Categories of fraud n n Fraud purely from forces outside the entity Fraud with collusion from within

Types and Categories of fraud n n Fraud purely from forces outside the entity Fraud with collusion from within

Causative factors for purely external fraud n n n Derelection of duty or lackadaisical approach Intellectual capabilities of fraudsters and awareness of loopholes Systems have been evolving and dynamic, giving an atmosphere or uncertainty and inconsistency of policy and procedures

Causative factors for purely external fraud n n n Derelection of duty or lackadaisical approach Intellectual capabilities of fraudsters and awareness of loopholes Systems have been evolving and dynamic, giving an atmosphere or uncertainty and inconsistency of policy and procedures

Causative Factors for fraud with internal collusion n Awareness of gaps in procedures etc Non accountability Existence of Organised Crime

Causative Factors for fraud with internal collusion n Awareness of gaps in procedures etc Non accountability Existence of Organised Crime

Standard Procedure for Housing Loans POTENTIAL BORROWER APPROACHES BANKS / INSTITUTIONS- BASIC ELIGIBILITY 2. SUBMISSION OF APPLICATION 3. SUBMISSION OF TITLE DOCUMENT 4. INSPECTION OF SITE/PLACE 5. VALUATION 6. SUBMISSION OF FINANCIAL DOCUMENTS 7. APPRAISAL OF FINANCIAL DOCUMENTS 8. APPRAISAL OF TITLE DOCUMENT 9. VALUATION OF PROPERTY AND ASSETS. 10. OBTAINING INSURANCE POLICY OF BORROWERS 11. GETTING NOC FROM BUILDER/SOCIETY AS RELEVANT AND BANK’S CHARGE CONFIRMATION FROM THE SCOIETY 12. GETTING ORIGINAL SHARE CERTIFICATE 13. POST DATED CHEQUES FOR MONTHLY EMIS 1.

Standard Procedure for Housing Loans POTENTIAL BORROWER APPROACHES BANKS / INSTITUTIONS- BASIC ELIGIBILITY 2. SUBMISSION OF APPLICATION 3. SUBMISSION OF TITLE DOCUMENT 4. INSPECTION OF SITE/PLACE 5. VALUATION 6. SUBMISSION OF FINANCIAL DOCUMENTS 7. APPRAISAL OF FINANCIAL DOCUMENTS 8. APPRAISAL OF TITLE DOCUMENT 9. VALUATION OF PROPERTY AND ASSETS. 10. OBTAINING INSURANCE POLICY OF BORROWERS 11. GETTING NOC FROM BUILDER/SOCIETY AS RELEVANT AND BANK’S CHARGE CONFIRMATION FROM THE SCOIETY 12. GETTING ORIGINAL SHARE CERTIFICATE 13. POST DATED CHEQUES FOR MONTHLY EMIS 1.

Instances of lakadaisical approach

Instances of lakadaisical approach

Common Causes- home loans n n n n Borrowers credentials- not examined to identify those who cannot pay Guarantors merely interviewed telephonically, if at all No structured procedure in place to spot fake OR modified documents, title deeds, etc Unreliable, inflated or even fictitious valuation reports, if there is collusion from within the financing bank Field checks- Laxity in field inspections of site, property, flat and other verifiable submissions before sanctioning a loan have contributed to a rise in frauds, Absence of system in place which can detect whether the same property has been mortgaged more than once Perfunctory examination of financial statements, tax returns. No application of mind Title checks through legal advisors- very unreliable

Common Causes- home loans n n n n Borrowers credentials- not examined to identify those who cannot pay Guarantors merely interviewed telephonically, if at all No structured procedure in place to spot fake OR modified documents, title deeds, etc Unreliable, inflated or even fictitious valuation reports, if there is collusion from within the financing bank Field checks- Laxity in field inspections of site, property, flat and other verifiable submissions before sanctioning a loan have contributed to a rise in frauds, Absence of system in place which can detect whether the same property has been mortgaged more than once Perfunctory examination of financial statements, tax returns. No application of mind Title checks through legal advisors- very unreliable

Major Challenges- home loans through collusion n Staff Collusion with borrowers- individual level Organised Fraud : Builder-borrower-staff-advocatechartered accountant nexus is believed to be the root cause of banks falling prey to home loan frauds Agents are available forging and creation of fictitious documents and rubber stamps

Major Challenges- home loans through collusion n Staff Collusion with borrowers- individual level Organised Fraud : Builder-borrower-staff-advocatechartered accountant nexus is believed to be the root cause of banks falling prey to home loan frauds Agents are available forging and creation of fictitious documents and rubber stamps

Staff Collusion helps in fraud being detected years later n n n HL not classified as HL but outsider fraud Teeming and lading of cheque collections EMIs not presented

Staff Collusion helps in fraud being detected years later n n n HL not classified as HL but outsider fraud Teeming and lading of cheque collections EMIs not presented

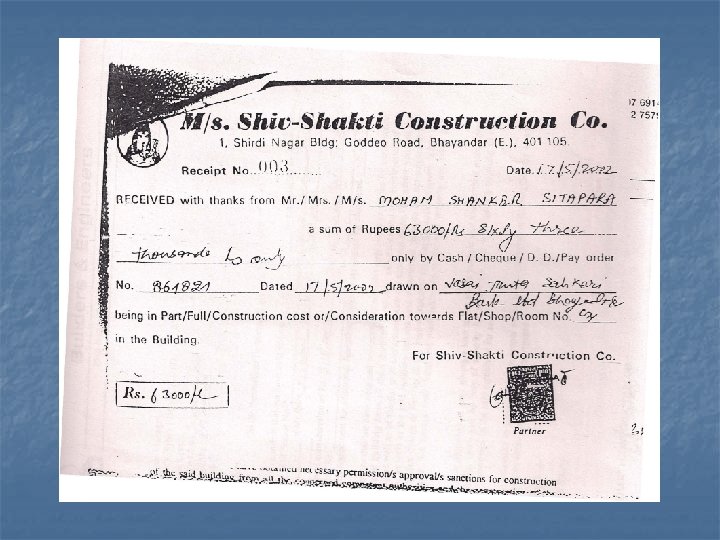

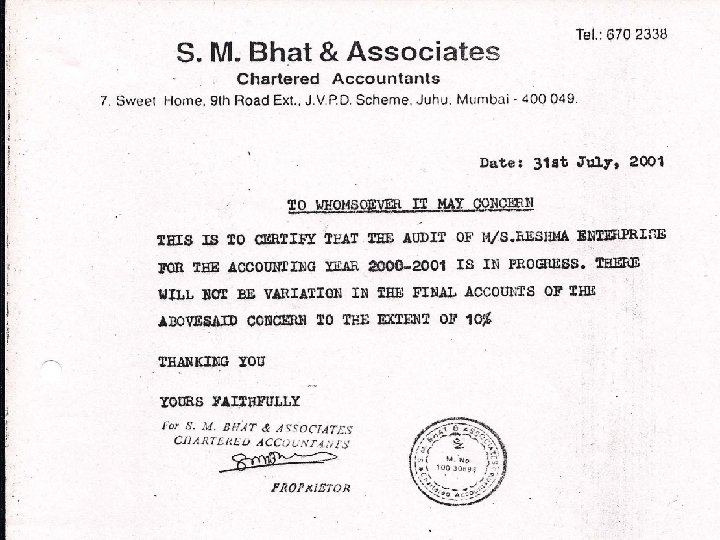

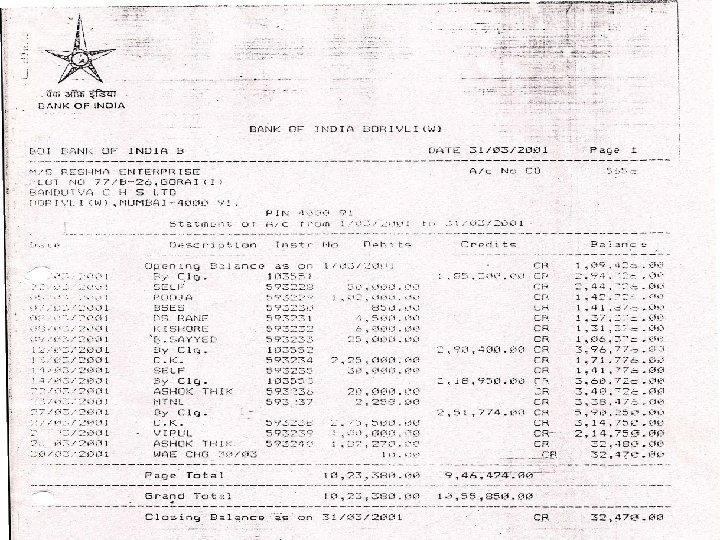

Case We have seen which encompassed every level of collusion n n Property did not exist Borrower was a sweeper staying on the road Borrower was not interviewed Guarantor did not exist Agreement was fictitious Registration receipt fictitious Valuer backed out stating that he had not issued any report Paneladvocate report was not taken No recovery suit was filed Police report conveniently stated borrower was absconding

Case We have seen which encompassed every level of collusion n n Property did not exist Borrower was a sweeper staying on the road Borrower was not interviewed Guarantor did not exist Agreement was fictitious Registration receipt fictitious Valuer backed out stating that he had not issued any report Paneladvocate report was not taken No recovery suit was filed Police report conveniently stated borrower was absconding

Novel Audit Tests for detecting frauds n n n n Other Mathematical tools: Benford’s Law, RSF, Statistical methods such as regression Tiger Team Tests, test packs Sting Operations- decoy purchases/sales, sting interviews Placebo effect Nanoscience approach-data mining Barium Test Repetitive verifications

Novel Audit Tests for detecting frauds n n n n Other Mathematical tools: Benford’s Law, RSF, Statistical methods such as regression Tiger Team Tests, test packs Sting Operations- decoy purchases/sales, sting interviews Placebo effect Nanoscience approach-data mining Barium Test Repetitive verifications

Measures of prevention at early stages- technology based n n Data mining for duplicate names, registration numbers, telephone nos etc Time dates- registration on Sundays/ Holidays Advanced data mining techniques Benford law etc

Measures of prevention at early stages- technology based n n Data mining for duplicate names, registration numbers, telephone nos etc Time dates- registration on Sundays/ Holidays Advanced data mining techniques Benford law etc

General methods n n n Verification of Registration receipt Development of forensic cell Training of staff for better awareness and techniques Use of investigation software Use repetitive valuers Data base of tainted borrowers, builders, consultants

General methods n n n Verification of Registration receipt Development of forensic cell Training of staff for better awareness and techniques Use of investigation software Use repetitive valuers Data base of tainted borrowers, builders, consultants

Benford’s Law

Benford’s Law

Benford’s Law

Benford’s Law

Tiger Team Tests Can be used in Housing Loans

Tiger Team Tests Can be used in Housing Loans

Thank you Chetan Dalal

Thank you Chetan Dalal