20e82d384a7aecd6e1048e5766089223.ppt

- Количество слайдов: 22

Forecasting • • • OBJECTIVES 1. Show value of forecasting in business planning. 2. Produce some basic forecasting procedures. 3. Show the limits of a forecast. 4. Illustrate how to use forecasts in business planning.

• I. Introduction • Firms need forecasting to stay abreast of changes in customer demand & market condition for inputs & outputs. • In the era of economic dependence, competition & uncertainty (e. g. , droughts, embargoes, price freezes) the ability to forecast future business conditions accurately is important to agribusinesses. • Forecasting reduces the uncertainty on business decision making & shd lead to increased profits – e. g. firms wld not expand pdn if an economic downturn is forecasted for the next year.

• 11. The Basics • A. Need to forecast basic economic variables (GDP, interest rates, etc. ) & relate these to pricing, pdn, sales, inventory decisions for agribusiness firms. • 1. Forecast Frequently: Forecasts explains past & predicts future customer buying habits, & anything affecting mkt conditions. Failure to forecasts mkt changes can lead business failure. Thus its important to forecast frequently on anything influencing firms • 2. Use Appropriate Forecasting Techniques: Forecasts is made in many ways, from throwing darts, to large, complex mathematical computer models. However, businesses have to use the forecasting techniques appropriate to their situation.

• • • B. The Five Factors of Forecasting The selection of a forecasting procedure is dependent on the ff factors: (1) accuracy desired, (2) time permitted to develop the forecast, (3) the complexity of the situation to be explained, (4) the time period to be projected, & (5) the amount of money available to carry out forecast. All these factors are inter-related – e. g. if time used in forecasting is short, accuracy of the projection cld suffer or if time used is long, accuracy increases, but so will the cost. The key is to determine the proper mix of the 5 factors. As a general rule, the best forecasts are those using the most straightforward, uncomplicated methods.

• • • C. Sources of Forecasts Forecasting can be obtained from private & public sources. 1. Private Firms: Private forecasting firms use sophisticated computer models to make their projections & sell them to other firms for a fee. Some large agribusiness firms operate their own in-house forecasting units 2. Trade Associations: Small firms that cannot buy or forecast on their own cos of cost can & do get forecasts thro their trade associations (e. g. Cattleman's Association) 3. Government: Some forecasting data (e. g. town, retail sales, popn, age, income, # of households) is available, free of charge, from federal, state, & local gov’t agencies – e. g. Census of Retail Trade published by US Deptof Commerce. 4. Business Publications: Include business publications like Fortune, Business Week, Wall Street Journal, Farm Journal, Grain Miller's News, Poultry Times, Supermarket News, etc

• D. Types of Data • 1. Cross‑sectional Data: Used to determine economic forces that influence other variables at a time or place– e. g. qty meat eaten in US, where data is qty of beef eaten in each state last year. Paired with other cross-sectional data - e. g. prices of beef, & barbecue sauce, & income – beef processors can see impact of these data on US beef cnsptn as well as forecast changes of these on future beef sales. • 2. Time Series data: Frequently used in forecasting & involves many observations of same variable over many time periods at the same location -e. g. av. monthly farmlevel cattle price from Jan 1990 to now. It makes it possible to identify reoccurring patterns in cattle prices that cld help predict prices in future months & thus assist beef processors to lower costs by indicating when to buy beef at lowest price in coming months.

• Simple Time Series Analysis • Many economic data – e. g agric pdt prices, company sales etc. exhibit repeating patterns of behavior or regularity when plotted over time. • The simplest approach to examining such data assumes that each observation comprises 4 components: – – (1) trend, (2) seasonal effect, (3) cyclical effect, and (4) an irregular effect or error term. • Y = T x S x C x I • where Y sales, price or other variable under analysis • T the trend component • S the seasonal component • C the cyclical component I/ • I the it-regular component or error term

• Trend Season Cyclical Irregular • Trend: Is the broad long-term growth or decline of the industry or firm. • Season: represents annually recurring forces that affect sales or prices. • Cyclical: Is a measure of forces that act as broad irregular waves. Such cycles may be due to demographic changes, general business cycles, etc. • Irregular: Is simply an error term and represents variations that cannot be attributed to trend, season or cycle.

• E. Forecasting Procedures • There a many forecasting methods that can assist a firm with its planning • 1. Extrapolation: Simplest procedure & assumes that whatever happened in the past will continue to happen in the future – e. g. if corn price rose 10% last year, one expects it to rise by 10% again this year. – Disadvantage: Method has no economic base, & this limits long-run use & may cause a manager to miss quick changes in economic environment. – Advantage: Effective forecasting method in short run (1 yr or less), & ease of application makes it an attractive "first-cut" forecasting procedure as many economic variables are often slow to change.

• 2. Graphical Analysis: Extrapolation can be a good forecaster when combined with graphical analysis. Here, the time-series data are plotted on a graph to permit forecasters to "see" changes to the variable over time covered. A trend line can be fitted to the graph & its slope gives expected future or long-run direction of the change. • Trend Line ___ A rise in Price trend price from $2 in yr 9 to $6 6 in yr 13 i. e. av. Price rise 5 of $1 per yr. If things stay 4 the same we can forecast 3 an increase in price of $1 for 2 next yr 1 1 2 3 4 5 6 7 8 9 10 11 12 13 time • Caution: Method shd be used for short-run forecasting as it has no economic foundation

• • Adjusting for Trend in Time Series Data 1. Adjusting for Inflation Graphical analysis does not provide a realistic picture of the data or impact of inflation – e. g. does trend in graphical analysis show a real increase in price of the pdt or shows a rise in the general level of all prices due to inflation? Deflation: To overcome this it is necessary to deflate or remove from these prices the effects of inflation – i. e. by dividing the price series by an appropriate index of price levels calculated for the same period, such as the Index of Prices Received by Farmers, the Consumer Price Index, or the Producer Price Index. Deflation Procedure: Deflated 99 =$2. 23 Corn price Price Rec’d Real Price 100 = 100/99 x 2. 23 Yr 1 Dec $2. 23 99 $2. 25 102=$2. 27 100=100/102 x 2. 27 Yr 2 Jan $2. 27 102 $2. 22

• Deflated prices can be plotted & new trend line is fitted. If the new trend shows an increase of price of $0. 20 from yr 9 to yr 13 then the average annual real increase in price is $0. 20/4 = $0. 05 - i. e. we can forecast an $0. 05/year real price increase in corn before inflation. This increase could reflect actual shifts in the demand or supply, or both. • 2. Adjusting for Population Growth • Popn can also distort time series data including consmption of agric pdt over time. If cnsmptn of a pdt is rising yearly, it is important to know if its caused by changes in consumer tastes, lower prices, or a rising popn. Popn effects on consmptn is removed by dividing consmptn by popn to get a per capita consumption rate. • If per capita consumption is rising or falling over time, it could indicate a change in consumer tastes, the effects of price shifts, or other variables but not population.

• Procedure for Removing Effect of Population • Yr Meat % chnge Popn % chnge Per Cap % chnge . Csptn sn 1971 ml sn 1971 Csptn sn 1971 40405 - 204. 9 - 197. 2 - 1976 41456 2. 6 216. 0 5. 4 161. 9 - 2. 7 1981 40481 0. 2 227. 9 11. 2 177. 6 - 9. 9 • • Consumption of meat stayed almost the same • But by removing the impact of population it shows that per capita consumption of meat has declined over the yrs & this may be due to change in consumers taste.

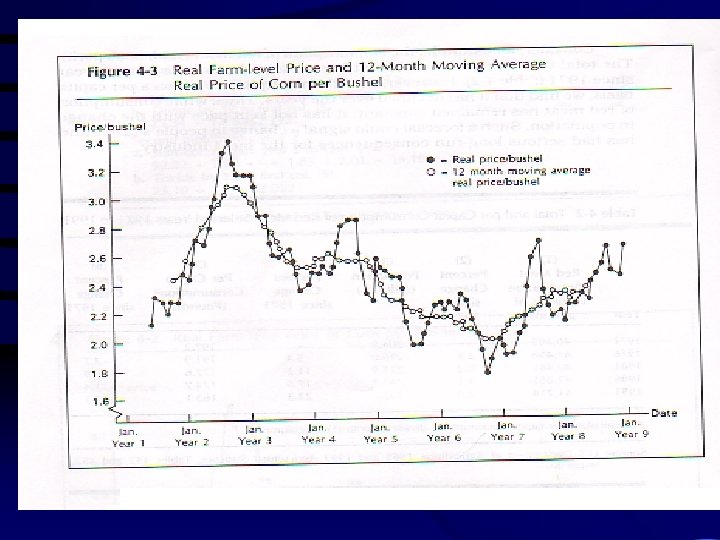

• 3. Adjusting for Short-time Fluctuations • a. Using Moving Averages to Adjust for Fluctuations • Is another way to get a clearer picture of change or trend in the data & it helps to reduce the impact of short-run fluctuations in the data thro the process of "smoothing out“ i. e. by plotting average of several data points. • A 12 -month moving average is calculated by adding the 12 most recent months of prices & dividing by 12. This is repeated each subsequent months, with the oldest month's value being dropped & replaced by the next month's price. • Plotting the moving average for these prices against the monthly prices shows the smoothing effect of the procedure (figure 4 -3).

• Farm-level Average Corn Prices, the Index of Prices Received by Farms, & Real Prices Deflated • • • (1) (2) (3) (4) PRICE PER INDEX OF REAL PRICE DATE BUSHEL PRICES RECVD PER BUSHEL Yr 1 Dec. $2. 23 99 $2. 25 Y 2 Jan. 2. 27 102 2. 22 Feb. 2. 29 105 2. 18 Mar. 2. 43 109 2. 23 Apr. 2. 51 114 2. 20 May 2. 72 118 2. 30 June 2. 68 118 2. 27 July 2. 49 117 2. 13 Aug. • • 2. 35 116 Sept. 2. 27 118 Oct. 2. 20 125 Nov. 2. 20 119 Dec. 2. 45 122 Year 3 Jan. 2. 48 127 Feb. 2. 46 132 Mar. 2. 54 134 To calculate 12 -month Moving Average (5) MOVING-AV PRICE/ BUSHEL $2. 11 2. 09 2. 07 2. 03 2. 04 1. 92 1. 76 1. 85 2. 01 1. 95 1. 86 1. 90 2. 01 2. 00 1. 98 1. 99 2. 03 2. 08 2. 11 • 1. Using price index calculate deflated or real prices ( i. e. to obtain column 4) • Sum 1 st twelve month prices in col. 4 (2. 25 +2. 18. . +1. 76+1. 85 = 25. 34) • Divide by 12 to find column 5 (25. 34/12)

• • • Futures Markets Agribusinesses face many risks in working with future agric prices to make pdn & mktg decisions. Futures mkts were developed as a way to reduce this price risk. The risk reduction is done through futures contract, where buyers & sellers meet & agree on a price/qty to be traded at some time in the future. • Importance of Futures Markets 1. Facilitates Carrying of Inventories: For storable pdt (corn, soybeans, wheat etc) whose supply is limited to one harvest a year, futures contract allows spreading out supply over the year through storage or return from storage.

• e. g. Oct 15, corn cash price = $3. 00/bushel next May's futures price = $3. 14/bushel, Incentive to store not to sell = $0. 14/bushel (or $0. 02/bushel/month return to storage). • Producers who can store for less than $0. 02/bus/mth shld store & vice versa. • 2. Predict or Provide Future Price info: - forecasting of future prices for inputs/outputs. Info assist producers in their pdn decisions & protect processors from shifts in input prices. • Nearest future prices provide better predictions of future price levels & can be of greatest value to producers decisions of agric commodities.

• Provide Forward Contracting and Price-risk Aversion. Producer or processor can lock in futures prices through Forward-contract or Hedging where one takes equal & opposite positions in the cash & futures markets. • Hedging: Permits users to gain the price protection benefits of using the futures market without actually shipping to or receiving the pdt from some distant point. They do this by "netting out“ (liquidating) their position (i. e. , taking equal but opposite futures mkt positions for the same commodity).

• Hedging works cos price difference in cash & futures mkts reflect only storage cost over the life of the futures contract. • e. g. If on July 1, a buyer for breakfast firm looks at the harvest price of wheat ($3. 90/bus) & estimates that it will cost the firm $0. 16/bushel to store the wheat until it is needed on March 1. • July 1 Cost of wheat $3. 90/bushel • Storage cost + $0. 16/bushel • Total cost $4. 06/bushel • March 1 wheat future price= $4. 10 per bushel. • Margin = $0. 04/bushel ($4. 10 - $4. 06) can be made by buying wheat now & storing until March 1. • To protect the firm against adverse price changes, a futures contract is sold to deliver wheat in March at $4. 10/bushel.

• If on March I both futures price & cash price are $4. 30/bushel, the return in the cash mkt will be a savings of $0. 24/bushel ($430 - $4. 06) from purchasing at harvest. • The return in the futures market after buying a contract & "netting out" of the mkt will be a loss of $0. 20/bushel ($4. 10 - $4. 30). • Combining the two yields a margin of + $0. 04/bushel ($0. 24 - $0. 20). • Cash Mkt Futures Mkt • July 1 Buy $4. 06 Sell $4. 10 • March 1 Sell $4. 30 Buy $4. 30 • Gain/Loss $0. 24 -$0. 20 • Net Gain/Loss = $0. 24 -$0. 20 = $0. 04 • Thus, thro hedging, the firm can reduce its price risk for agric pdts

• Benefit of Futures markets • To Producers: It allows producers to be sure of a selling price for their output. • To Processors: It assures processors of adequate supplies of inputs at predetermined prices so they can operate their plants more efficiently. • To Agribusiness System: It benefits the entire, system by giving good forecasts of future price levels that should lead to better prodn decisions.

20e82d384a7aecd6e1048e5766089223.ppt