c6dc30a2d3610d9165a97eed6d88b6b2.ppt

- Количество слайдов: 76

FOCUS: Financing a Business

OBJECTIVES: Find out • How FINANCIAL MARKETS help businesses obtain CAPITAL RESOURCES • How businesses BORROW • What EQUITY is and how it’s used to finance business growth • How businesses SAVE

OBJECTIVES: Find out • What the STOCK MARKET is & why it’s important • How to read a STOCK TABLE • What a BALANCE SHEET is & how to use it • What an INCOME STATEMENT is & how to use it

INVESTMENT is the purchase of CAPITAL RESOURCES used to produce goods & services

FINANCIAL MARKETS are where SAVERS exchange with BORROWERS and others who are willing to pay for the use of the money

SAVERS BUSINESSES

KEY POINT: • Every DOLLAR of INVESTMENT = one less DOLLAR of CONSUMPTION

Business Accounting: • ASSETS: what a company OWNS • LIABILITIES: what a company OWES

")

How do BUSINESSES use the FINANCIAL MARKETS to obtain money? • BORROW (debt financing) • Sell SHARES of ownership (EQUITY financing) • SAVE the money themselves (RETAINED EARNINGS – save and plow back into business!)

3 KINDS OF FINANCING • SHORT-TERM FINANCING • INTERMEDIATE-TERM FINANCING • LONG-TERM FINANCING

SHORT-TERM FINANCING: • Trade credit • Unsecured loans • Secured loans • Line of credit pp. 266 -7

• WHOLESALER")

TYPES OF SELLERS: • RETAILER – sells directly to the public (consumers) • WHOLESALER – supplies businesses which sell directly to consumers; does NOT sell to the public – sells to businesses! pp. 266 -7

• Business’s CAPITAL is")

TRADE CREDIT: • BUY NOW, PAY LATER (30 -90 days) • Business’s CAPITAL is not tied up in INVENTORY • Extended by supplier because it increases sales & profits (interest) • DISCOUNT for quick-pay! pp. 266 -7

UNSECURED LOANS: • No COLLATERAL • Guarantees with a PROMISSORY NOTE (specified time & interest rate) pp. 266 -7

SECURED LOANS: • Backed by COLLATERAL --machinery --inventories --ACCOUNTS RECEIVABLE (money owed business by its customers) pp. 266 -7

LINE OF CREDIT: • Maximum amt. of $ a company can borrow from a bank during a period of time (1 yr. ) • No new loan application; auto OK up to amt. specified pp. 266 -7

SHORT-TERM FINANCING: • Trade credit • Unsecured loans • Secured loans • Line of credit pp. 266 -7

• Leasing (renting rather than")

INTERMEDIATE-TERM FINANCING: • Loans (1 to 10 yrs. ) • Leasing (renting rather than buying) pp. 266 -7

LOANS: • 1 -10 years • COLLATERAL: stocks, bonds, equipment, machinery • MORTGAGE if secured by property pp. 266 -7

LEASING: • Renting rather than buying • + low cost service • + income tax deduction • - often more expensive than buying pp. 266 -7

• Leasing (renting rather than")

INTERMEDIATE-TERM FINANCING: • Loans (1 to 10 yrs. ) • Leasing (renting rather than buying) pp. 266 -7

LONG-TERM FINANCING: • BONDS • STOCKS pp. 266 -7

PLEASE NOTE the DIRECT RELATIONSHIP between RISK and SIZE of REWARD!

PLEASE NOTE the INVERSE RELATIONSHIP between RISK and LIKELIHOOD of REWARD!

• Specified interest")

BONDS: • Corporate or gov’t. I. O. U. (certificate of indebtedness) • Specified interest rate • Specified time • Pd. In full upon MATURITY pp. 266 -7

BONDHOLDER = Company’s creditor

TWO KINDS of BONDS: pp. 266 -7

County & Municipal Bonds: • BOND ISSUE = election in which local government seeks public approval for the sale of BONDS to raise funds usually for SCHOOL or COMMUNITY improvements

underwrites an issue of stocks or")

UNDERWRITING: • When a securities firm (investment bank) underwrites an issue of stocks or bonds, it buys a corporation’s entire issue of stock or bonds and then sells the securities to the public

BONDS =

• By a borrower (THE")

The BOND… • Is given to the lender (BONDHOLDER) • By a borrower (THE BOND SELLER -- the financial intermediary)

•")

TERMS of the LOAN: The BORROWER will pay: • PRINCIPAL (entire amount borrowed) • INTEREST (the profit paid the lender for the use of his or her money)

VOCABULARY TERMS: • FACE VALUE: the purchase price of the bond (PAR value or principal) • MATURITY DATE: the particular day at which time the borrower promises to pay back the loan in full (both principal and interest) • COUPON RATE: the predetermined rate of interest

BOND RATINGS: • RISK is measured by the credit rating of the bond’s issuer. • RATINGS indicate the ability of a corporation of local government to repay its debts. MOODY’S INVESTOR SERVICES rates bonds on a scale from AAA (highest quality) to C (no interest being paid, bankruptcy filed or in default) DDD – veeeeerry risky!

BONDS GOVERNMENT BONDS CORPORATE BONDS • Lower RISK! • Lower RETURNS! • Higher RISK! • Higher RETURNS!

STOCKS: • EQUITY financing • Shares of ownership pp. 266 -7

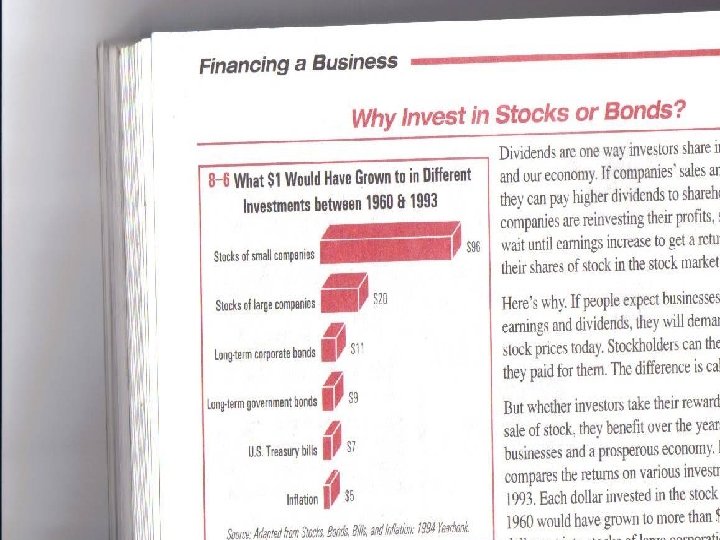

2 Ways to Make Money from Stocks: • DIVIDENDS (share of profits pd. to stockholders) • CAPITAL GAINS (profits from sale of stock)

STOCKHOLDER = Company’s part owner

TWO KINDS of Stock Companies: pp. 266 -7

TWO KINDS of STOCK: pp. 266 -7

Common Stock: • issued by all public corporations • Owners have voting rights; elect board of directors • Pays DIVIDENDS based on performance • Value varies with corp. performance • Last to be pd. If corp. fails pp. 266 -7

Preferred Stock: • not issued by all corps. • No voting rights Value varies with performance • PREFERENTIAL treatment= --pays fixed dividend before common stockholders are pd. --If corp. fails, pd. before common stockholders are pd. pp. 266 -7

SALE of STOCKS & BONDS: • Primary or New Issues Market • Secondary Market (what you think of commonly as the stock market)

PRIMARY MKT: • IPO = initial public offering • Investment bankers sell new shares of stock for corps. • Proceeds go to corps. w/ profit for investment bankers who UNDERWRITE the STOCK ISSUE

underwrites an issue of stocks or")

UNDERWRITING: • When a securities firm (investment bank) underwrites an issue of stocks or bonds, it buys a corporation’s entire issue of stock or bonds and then sells the securities to the public

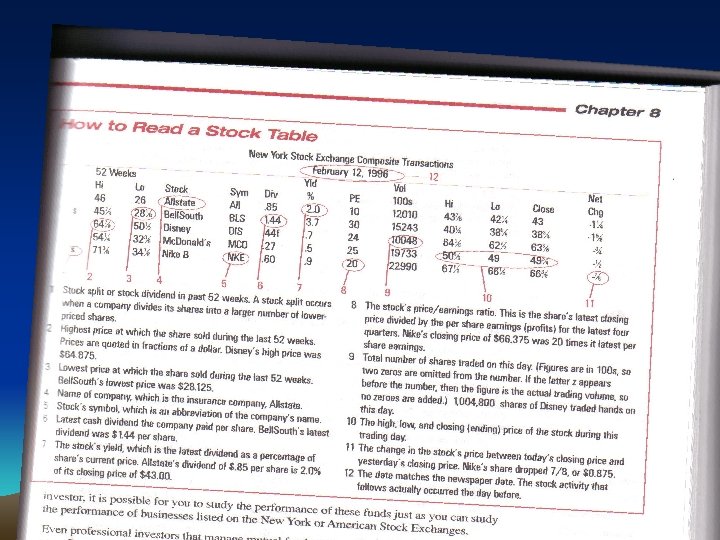

SECONDARY MKT: • Commonly called the STOCK MARKET • Stock sold on EXCHANGES or OTC (over-the-counter) • Proceeds go to stockholder who sells w/ profit to broker NOT to corporation • w/o 2 ndary mkt to trade in, few would buy new issues

2 Ways to Make Money from Stocks: • DIVIDENDS (share of profits pd. to stockholders) • CAPITAL GAINS (profits from sale of stock)

Organized Exchanges: • NYSE: New York Stock Exchange (2000+ of the largest & best-known corps. ) • AMEX: American Stock Exchange (about 1000 midsize corps. w/ strong growth potential) • Regional exchanges: Los Angeles, Chicago, Boston • Foreign exchanges: FTSE, CAC-40

Over-the-Counter Mkt: • Decentralized, computerized markets • NASDAQ: National Assoc. of Securities Dealers Automated Quotation System

Securities Exchange Commission: • Federal governmental agency which regulates sales and protects investors • 5 members appt. by U. S. Pres. • Investigate charges of fraud & violations like insider trading

PROSPECTUS: • SEC requires corps. to provide a PROSPECTUS for any new issue of securities • Contains info. About the company, its stocks or other securities, & risks so you can “check it out” before you buy

SALE of STOCKS & BONDS: • Primary or New Issues Market • Secondary Market (what you think of commonly as the stock market)

2 Ways to Make Money from Stocks: • DIVIDENDS (share of profits pd. to stockholders) • CAPITAL GAINS (profits from sale of stock) --CAPITAL LOSSES don’t make any $$$!

How Things Are Going: • BULL MARKET: Good! Stocks are on the rise. • BEAR MARKET: Bad! Stocks are down!

DO NOW: -Put your name, date, & period on a clean sheet titled “An Interview with Mr. Stock” –Answer questions A-H. Leave space if you don’t know an answer.

FEDERAL BONDS: • Savings Bonds • Treasury Bills

MUTUAL FUNDS: • Corps. that allow individuals to pool money in order to buy and sell stocks, bonds, & other securities • Investors buy SHARES in the FUND instead of shares of stock or bonds

ADVANTAGES of MUTUAL FUNDS: • Professional managers study mkt. & make investments • RISK is spread because a loss in one sec. is likely to be offset by a gain in another • Get better deals because they invest large sums

Mutual Funds • OBJECTIVES vary ---long term growth ---safety & stability ---greatest possible return now ---liquidity

Mutual Funds: • GOAL: Offer • GOAL: higher stability, security, returns or capital liquidity gains • STRATEGY: Invest in short. Invest in term gov’t notes common stocks, and short-term bonds, or a bonds combination (Money Market)

Money Market Mutual Funds: • GOAL: Offer stability, security, liquidity • STRATEGY: Invest in shortterm gov’t notes and shortterm bonds

MUTUAL FUNDS: • What fees: --buying --selling • When paid: --front load --back load --no load • Performance: --check against objectives

FINANCIAL DECISIONS: • Professionals - FINANCIAL ADVISORS – Trained in business at college/university – Experienced judgment – Spend all day everyday watching and studying the market • Amateurs – hobby = watching the market and managing investments – Individuals – clubs

DO NOW: BUSINESS ACCOUNTING Check out the sheet on your desk. Find out the difference in a A. BALANCE SHEET B. INCOME STATEMENT Explain briefly on a clean sheet.

Business Accounting: • ASSETS: what a company OWNS • LIABILITIES: what a company OWES Assets – Liabilities = NET WORTH or ASSETS = Liabilities + Net Worth

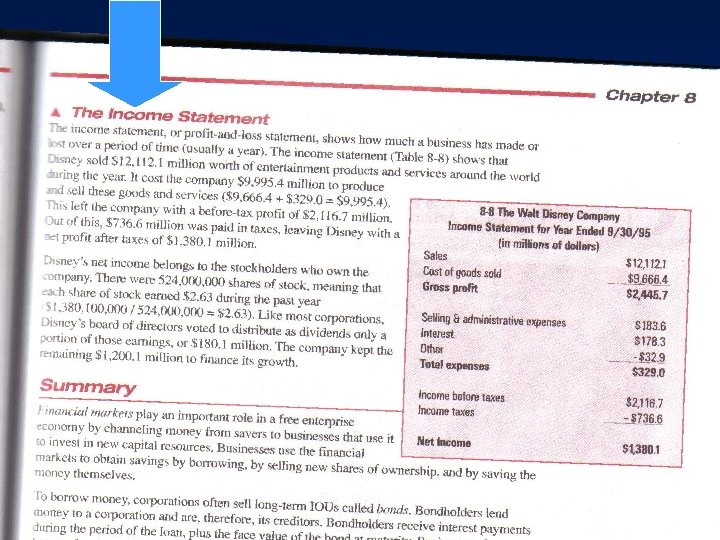

Business Accounting: • BALANCE SHEET • INCOME STATEMENT -- “snapshot” of a business at a given pt. – “video” of business over time (usually 1 in time yr. ) --summarizes a company’s ASSETS, --summarizes a firm’s REVENUES, COSTS, LIABILITIES, and the difference NET WORTH between the two (PROFIT or LOSS)

BALANCE SHEET

4 Factors Affecting a Business’s Loan Choices • INTEREST COSTS • MARKET CLIMATE • CONTROL OF THE CO. • FINANCIAL CONDITION OF THE CO. P. 269

When Businesses Save: • DEPRECIATION: the value lost in assets like tools or machines as they wear out or become obsolete • When cost of DEPRECIATION is included in price of products or services, businesses save P. 269

How Businesses Use Profits: • Pay income taxes to state & federal gov’ts. • Pay dividends to stockholders • RETAINED EARNINGS (undistributed profits) may be “plowed back” into the co. by investing in new CAPITAL RESOURCES P. 269

MERGERS • Occur when 2 or more businesses unite under the same ownership • One can buy the other or they can simply combine • 3 categories: – HORIZONTAL MERGERS – VERTICAL MERGERS – CONGLOMERATE MERGERS

3 Categories of MERGERS: • HORIZONTAL MERGER: – 2 companies at the same stage of production join; eliminates competition – Mc. Donalds & Burger King – VERTICAL MERGER: – 2 companies at different stages of production of the same product merge – Mc. Donalds and a meat processing company • CONGLOMERATE MERGER – 2 totally UNRELATED companies merge

Celler-Kefauver Act • 1950 • Prohibits any type of merger that gives merging firms an unfair advantage in the marketplace (MONOPOLY)

c6dc30a2d3610d9165a97eed6d88b6b2.ppt