f7d5c048d13be6559bd0e8e8ed4ba2c7.ppt

- Количество слайдов: 33

FINANCIAL PLANNING

FINANCIAL PLANNING

WHAT IS FINANCIAL PLANNING ? Financial planning is the process of making advance provision for Financial needs that will arise in the future. The objective is to ensure that the right amount of money is available in the right hands at the right points in the future to achieve the financial objectives of an individual – Examples: • Provision for family in case of death/ disability • Creation of wealth for various needs • Tax saving in a lawful way

WHAT IS FINANCIAL PLANNING ? Financial planning is the process of making advance provision for Financial needs that will arise in the future. The objective is to ensure that the right amount of money is available in the right hands at the right points in the future to achieve the financial objectives of an individual – Examples: • Provision for family in case of death/ disability • Creation of wealth for various needs • Tax saving in a lawful way

PREDICTABLE EVENTS • Emergency funds for medical expenses • Repayment of debts-personal loans/vehicle loans • Capital for purchase of a house/flat • Marriage expenses of children • Capital to start their own business • Income they need in retirement • Children’s education at different stages • Inflation

PREDICTABLE EVENTS • Emergency funds for medical expenses • Repayment of debts-personal loans/vehicle loans • Capital for purchase of a house/flat • Marriage expenses of children • Capital to start their own business • Income they need in retirement • Children’s education at different stages • Inflation

UNPREDICTABLE EVENTS • Long term sickness/disability • The onset of a critical illness • Unemployment • The death of income provider before the children have grown up • Provision for visiting the settled children at abroad

UNPREDICTABLE EVENTS • Long term sickness/disability • The onset of a critical illness • Unemployment • The death of income provider before the children have grown up • Provision for visiting the settled children at abroad

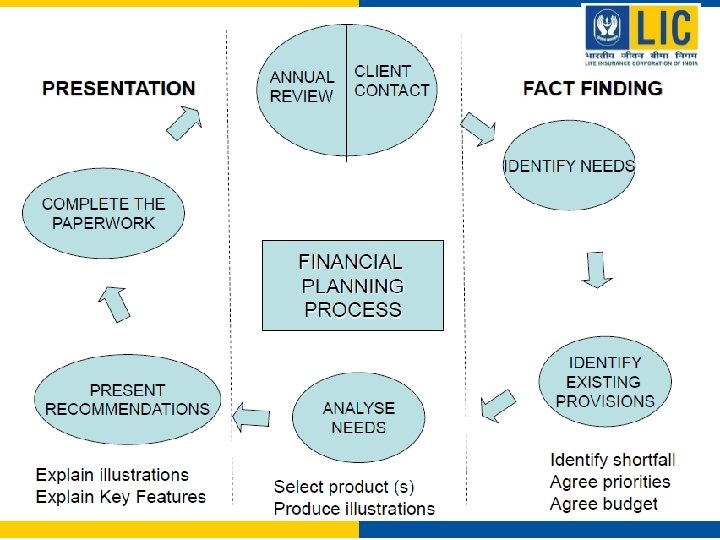

Financial Planning Strategy A six-step process : Step 1: Setting goals with the client Step 2: Gathering relevant information on the client Step 3: Analyzing the information Step 4: Constructing a financial plan Step 5: Implementing the strategies in the plan Step 6: Monitoring implementation and reviewing the plan

Financial Planning Strategy A six-step process : Step 1: Setting goals with the client Step 2: Gathering relevant information on the client Step 3: Analyzing the information Step 4: Constructing a financial plan Step 5: Implementing the strategies in the plan Step 6: Monitoring implementation and reviewing the plan

THE LIFE CYCLE Income Post-family/ pre-retirement Retirement Married with older children Young married with children Young married Unmarried Childhood Birth Age Death

THE LIFE CYCLE Income Post-family/ pre-retirement Retirement Married with older children Young married with children Young married Unmarried Childhood Birth Age Death

PRIORITIES in FINANCIAL PLANNING • Emergency Fund • Life Insurance • Mediclaim / Health Insurance / Critical Insurance • Investment Needs • Pension

PRIORITIES in FINANCIAL PLANNING • Emergency Fund • Life Insurance • Mediclaim / Health Insurance / Critical Insurance • Investment Needs • Pension

Exposure Draft - IRDA • Prescribe Standards & Procedures for Needs Analysis for sale of Insurance policies • Purpose – Ensuring that the product proposed to be sold is suitable for the prospect and meets his/her needs.

Exposure Draft - IRDA • Prescribe Standards & Procedures for Needs Analysis for sale of Insurance policies • Purpose – Ensuring that the product proposed to be sold is suitable for the prospect and meets his/her needs.

Exposure Draft - IRDA • Standard Proposal-cum-Needs Analysis Form • Prospect Product Matrix

Exposure Draft - IRDA • Standard Proposal-cum-Needs Analysis Form • Prospect Product Matrix

Standard Proposal-cum-Needs Analysis Form § Shall be the heart of the sales process § It helps in getting all of the important input information needed for basic to comprehensive financial planning § Also works as support during conflicts between client and financial planner

Standard Proposal-cum-Needs Analysis Form § Shall be the heart of the sales process § It helps in getting all of the important input information needed for basic to comprehensive financial planning § Also works as support during conflicts between client and financial planner

THE LIFE CYCLE AND ITS IMPLICATION FOR FINANCIAL PLANNING 1. Childhood: 2. 3. 4. Dependency: Education/ Higher Edn. /Food/Clothing/Pocket money/Social Activities Needs: No protection needs for children. However, when financial assistance availed then protection needs are needed to the extent of loan.

THE LIFE CYCLE AND ITS IMPLICATION FOR FINANCIAL PLANNING 1. Childhood: 2. 3. 4. Dependency: Education/ Higher Edn. /Food/Clothing/Pocket money/Social Activities Needs: No protection needs for children. However, when financial assistance availed then protection needs are needed to the extent of loan.

THE LIFE CYCLE AND ITS IMPLICATION FOR FINANCIAL PLANNING 2. Young/Unmarried: *Disability & incurable illness *Investment needs *Long/Short term savings *Establish Home Young Unmarried – With Dependents

THE LIFE CYCLE AND ITS IMPLICATION FOR FINANCIAL PLANNING 2. Young/Unmarried: *Disability & incurable illness *Investment needs *Long/Short term savings *Establish Home Young Unmarried – With Dependents

Both partners working * Accumulate capital for future needs *") 3. Young Married: (a) Both partners working * Accumulate capital for future needs * Retirement * Emergency Fund * Need protection against disability (injuries & long term sickness) and incurable diseases. * cover against housing loan * Short term savings needs (car, tour etc. ) (b) Single Partner Working *Life Insurance *Pension Provision The points in (b) is applicable to both the above categories

3. Young Married: (a) Both partners working * Accumulate capital for future needs * Retirement * Emergency Fund * Need protection against disability (injuries & long term sickness) and incurable diseases. * cover against housing loan * Short term savings needs (car, tour etc. ) (b) Single Partner Working *Life Insurance *Pension Provision The points in (b) is applicable to both the above categories

• • • Financial Needs Are Immediate & Short Term May still have some support from parents May be saving towards future family needs - say buying home May be paying off education loans Likes to spend money Ability to Invest : Limited due to higher spending Choice Of Investments : Liquid plans & short term investments. Some exposure to equity and pension products, Term Insurance plan

• • • Financial Needs Are Immediate & Short Term May still have some support from parents May be saving towards future family needs - say buying home May be paying off education loans Likes to spend money Ability to Invest : Limited due to higher spending Choice Of Investments : Liquid plans & short term investments. Some exposure to equity and pension products, Term Insurance plan

4. Young Married with children * If mother gives up work -Loss of Earnings -Substantial insurance required -Money availability reduced * If mother returns to work -Life insurance on both lives to be divided proportionately -Injury/long term illness -Increased investment needs * School/Higher education costs * Marriage/Dowry/Bride prices * Investment needs-better house, better cars * Retirement Protection needs priority over investment

4. Young Married with children * If mother gives up work -Loss of Earnings -Substantial insurance required -Money availability reduced * If mother returns to work -Life insurance on both lives to be divided proportionately -Injury/long term illness -Increased investment needs * School/Higher education costs * Marriage/Dowry/Bride prices * Investment needs-better house, better cars * Retirement Protection needs priority over investment

• High expenditure through installment repayments for house, car etc. • Worried about protecting dependants in case of death or prolonged illness or disability • Need to save for children for their education, marriage etc. • Need to support elderly parents • Need for planning a comfortable retirement phase • Maximum Insurance Protection required due to • High debt, high expenditure phase –Family’s dependency on your income • Low accumulated wealth • Need for planning retirement

• High expenditure through installment repayments for house, car etc. • Worried about protecting dependants in case of death or prolonged illness or disability • Need to save for children for their education, marriage etc. • Need to support elderly parents • Need for planning a comfortable retirement phase • Maximum Insurance Protection required due to • High debt, high expenditure phase –Family’s dependency on your income • Low accumulated wealth • Need for planning retirement

• • • Financial Needs : Short & Intermediated term. Housing & insurance needs. Consumer finance needs, children education and related expenses Ability to Invest : Limited due to higher spending. Cash flow requirments are also limited. Financial planning needs are highest as this state is ideal for disciplining spending & saving regularly Choice Of Investments : Medium to long term investments. Ability to take risks. Fixed income, insurance & Equity products. Long term insurance policies like disability income and death benefit protection i. e. a need for temporary (Term) or Whole Life Insurance products, and long-term disability products

• • • Financial Needs : Short & Intermediated term. Housing & insurance needs. Consumer finance needs, children education and related expenses Ability to Invest : Limited due to higher spending. Cash flow requirments are also limited. Financial planning needs are highest as this state is ideal for disciplining spending & saving regularly Choice Of Investments : Medium to long term investments. Ability to take risks. Fixed income, insurance & Equity products. Long term insurance policies like disability income and death benefit protection i. e. a need for temporary (Term) or Whole Life Insurance products, and long-term disability products

5. Married with Older Children: * Investment needs * Income Protection * Pension funding * Medical Insurance * children higher education loans * Professional & additional courses * Start in life provision

5. Married with Older Children: * Investment needs * Income Protection * Pension funding * Medical Insurance * children higher education loans * Professional & additional courses * Start in life provision

* Maximise income on retirement * Accident/ageing sickness") 6. Post family/Pre-retirement * Pension Products(Maximise) * Maximise income on retirement * Accident/ageing sickness * Inheritance tax planning * Rennovation/ extension of house, new car * Medical insurance

6. Post family/Pre-retirement * Pension Products(Maximise) * Maximise income on retirement * Accident/ageing sickness * Inheritance tax planning * Rennovation/ extension of house, new car * Medical insurance

• Older, may be financially independent children • Reduced debts or repaid loans • Decreased expenditure • Probable period of redundancy Financial Needs • Save for retirement • Enjoy a life time holiday on retirement • Protect dependants financially against your death, prolonged illness or disability • Save for children • Medium term needs for children's education & marriage. Need for pension, insurance & higher medical cover

• Older, may be financially independent children • Reduced debts or repaid loans • Decreased expenditure • Probable period of redundancy Financial Needs • Save for retirement • Enjoy a life time holiday on retirement • Protect dependants financially against your death, prolonged illness or disability • Save for children • Medium term needs for children's education & marriage. Need for pension, insurance & higher medical cover

Ability to invest • Higher saving ratios recommended. Requirement for intermittent cash flows higher. Choice of Investments : • Long term investments with medium return meeting periodical liquidity needs • Portfolio of products including Medium exposure to equity, debt & pension plans. • Provision for your retirement either with-profit or unit-linked endowment assurance or deferred annuities. • For accumulation of wealth to be transferred to the next generation with -profit or unit-linked Whole life insurance products. Single premium with -profit or unit linked products providing a lump sum benefit for the future • High sum insured towards Health Insurance plans for self and dependents

Ability to invest • Higher saving ratios recommended. Requirement for intermittent cash flows higher. Choice of Investments : • Long term investments with medium return meeting periodical liquidity needs • Portfolio of products including Medium exposure to equity, debt & pension plans. • Provision for your retirement either with-profit or unit-linked endowment assurance or deferred annuities. • For accumulation of wealth to be transferred to the next generation with -profit or unit-linked Whole life insurance products. Single premium with -profit or unit linked products providing a lump sum benefit for the future • High sum insured towards Health Insurance plans for self and dependents

• 7. Retirement: Three main categories *Low pension & little capital to supplement *Low pension & accumulated capital *Sufficient income & substantial assets & capital

• 7. Retirement: Three main categories *Low pension & little capital to supplement *Low pension & accumulated capital *Sufficient income & substantial assets & capital

• Older, may have financially independent children • Repaid loans • Decreased expenditure Financial Needs • Income flow to support retirement • Enjoy holiday, entertainment, celebrations, etc. on retirement • Financial security for spouse / dependents in the event of your death, • prolonged illness or disability • Save for children • Need for pension, insurance & higher medical cover

• Older, may have financially independent children • Repaid loans • Decreased expenditure Financial Needs • Income flow to support retirement • Enjoy holiday, entertainment, celebrations, etc. on retirement • Financial security for spouse / dependents in the event of your death, • prolonged illness or disability • Save for children • Need for pension, insurance & higher medical cover

• Ability to invest • Higher saving ratios recommended. Requirement for intermittent cash flows higher. • Choice of Investments : • Medium term investments with high liquidity needs. • Portfolio of products including low equity exposure , more debt exposure & pension plans. • Wealth Transfer or other savings vehicles • emphasis should be on returns on investment - so, withprofit or unit-linked products would be ideal. • For accumulation of wealth to be transferred to the next generation with-profit or unit-linked Whole life insurance products. Single premium with-profit or unit linked products providing a lump sum benefit for the future

• Ability to invest • Higher saving ratios recommended. Requirement for intermittent cash flows higher. • Choice of Investments : • Medium term investments with high liquidity needs. • Portfolio of products including low equity exposure , more debt exposure & pension plans. • Wealth Transfer or other savings vehicles • emphasis should be on returns on investment - so, withprofit or unit-linked products would be ideal. • For accumulation of wealth to be transferred to the next generation with-profit or unit-linked Whole life insurance products. Single premium with-profit or unit linked products providing a lump sum benefit for the future

CIRCUMSTANCES AFFECTING FINANCIAL ADVICE There are several constraints on people’s ability to implement the necessary financial plans 1. Available resources-spent or save & invest 2. Health 3. Occupation & leisure activities 4. Tax concessions 5. Time constraints 6. Levels of risks 7. Returns

CIRCUMSTANCES AFFECTING FINANCIAL ADVICE There are several constraints on people’s ability to implement the necessary financial plans 1. Available resources-spent or save & invest 2. Health 3. Occupation & leisure activities 4. Tax concessions 5. Time constraints 6. Levels of risks 7. Returns

Limitations of the Life cycle model Identifying the needs of specific individuals & how these needs can be met now & in the future: 1. 2. Unmarried-Single-Independent Divorce/Separation * Rebuilding his or her career afresh * The terms of the divorce settlement * Remarriage 3. Widows or Widowers: * The self-supporting * Those with adequate provision from a deceased spouse * Those with inadequate provision from a deceased spouse 4. Persons with short earning period ex: broad caster, sportsmen, police & army personnel

Limitations of the Life cycle model Identifying the needs of specific individuals & how these needs can be met now & in the future: 1. 2. Unmarried-Single-Independent Divorce/Separation * Rebuilding his or her career afresh * The terms of the divorce settlement * Remarriage 3. Widows or Widowers: * The self-supporting * Those with adequate provision from a deceased spouse * Those with inadequate provision from a deceased spouse 4. Persons with short earning period ex: broad caster, sportsmen, police & army personnel

Difficulties in identifying financial planning needs and priorities • Awareness for future needs & their present spending (real needs & priorities) • Quantifying each financial needs • Provisioning for short falls • Review of financial needs regularly • Ignorance about real needs • Inability to anticipate certain needs like morbidity

Difficulties in identifying financial planning needs and priorities • Awareness for future needs & their present spending (real needs & priorities) • Quantifying each financial needs • Provisioning for short falls • Review of financial needs regularly • Ignorance about real needs • Inability to anticipate certain needs like morbidity

The role of the financial advisor • Contact the prospects • Identify the clients financial planning needs (real needs) • Understand the client’s risk profile & relate them to the needs of the different people/in different forms of investment • Well trained expert in financial planning products knowledge, technical factors, communication skills • Prepare the viable set of recommendations & make a presentation • Completion of formalities –Paper work, review, keep in touch-provide after sales service

The role of the financial advisor • Contact the prospects • Identify the clients financial planning needs (real needs) • Understand the client’s risk profile & relate them to the needs of the different people/in different forms of investment • Well trained expert in financial planning products knowledge, technical factors, communication skills • Prepare the viable set of recommendations & make a presentation • Completion of formalities –Paper work, review, keep in touch-provide after sales service

Financial Planning • Strategy tailored to a client's specific situation, for meeting a client's specific goals. • Enable a financial analyst to determine what your financial needs are • 3 major components : v. Financial Resources (FR) v. Financial Tools (FT) v. Financial Goals (FG) Financial Planning : FR + FT = FG

Financial Planning • Strategy tailored to a client's specific situation, for meeting a client's specific goals. • Enable a financial analyst to determine what your financial needs are • 3 major components : v. Financial Resources (FR) v. Financial Tools (FT) v. Financial Goals (FG) Financial Planning : FR + FT = FG

Risk Emergency Solution Emergency Fund Quantum Early Death Life Insurance 6 months house hold expenses Limited to HLV Illness/ Injury Mediclaim, health insurance At least up to 3 lacs Long Life Company Pension As per standard plans of living Falling interest/ rising inflation ULIPs, MFs, ETFs As per financial goals

Risk Emergency Solution Emergency Fund Quantum Early Death Life Insurance 6 months house hold expenses Limited to HLV Illness/ Injury Mediclaim, health insurance At least up to 3 lacs Long Life Company Pension As per standard plans of living Falling interest/ rising inflation ULIPs, MFs, ETFs As per financial goals