4b69539e304ccedc161929901f96820d.ppt

- Количество слайдов: 36

Farmland Values and Leasing Key Questions Chapter 20 § What determines the value of farmland? § What are the advantages and disadvantages of owning vs. leasing? § What are the common types of farm leases? § How can a fair cash rent be determined?

Farmland Values and Leasing Key Questions Chapter 20 § What determines the value of farmland? § What are the advantages and disadvantages of owning vs. leasing? § What are the common types of farm leases? § How can a fair cash rent be determined?

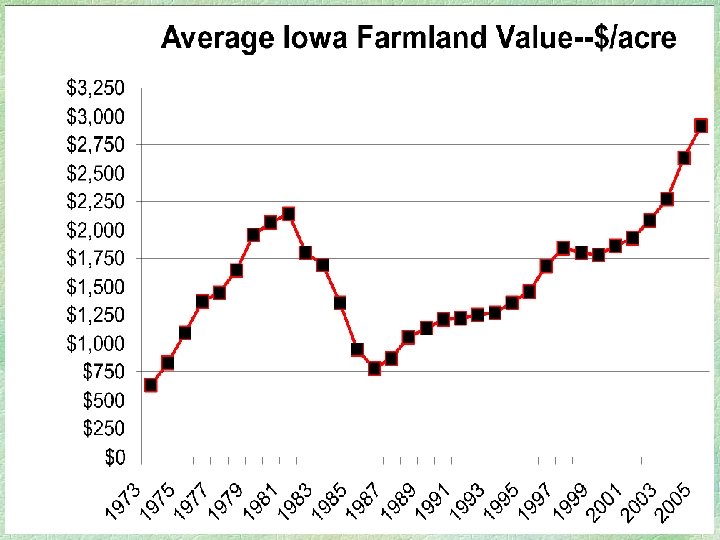

Land Value Trends in Iowa § 1973 -1981 l Increased export demand l High grain prices l Low interest rates l High inflation rate

Land Value Trends in Iowa § 1973 -1981 l Increased export demand l High grain prices l Low interest rates l High inflation rate

§ 1982 -1986 l Higher interest rates l Lower inflation l Weather problems l Forced sales § Since 1986 l Farm economic recovery l Government payments l Higher yields l Lower interest rates

§ 1982 -1986 l Higher interest rates l Lower inflation l Weather problems l Forced sales § Since 1986 l Farm economic recovery l Government payments l Higher yields l Lower interest rates

Who Buys Iowa Farmland?

Who Buys Iowa Farmland?

Farm for Sale § FOR SALE: 80 acres in Hamilton County, 75 acres tillable, Clarion-Webster soil type, CSR of 76 and 84. No buildings. Hard surfaced road. Contract available.

Farm for Sale § FOR SALE: 80 acres in Hamilton County, 75 acres tillable, Clarion-Webster soil type, CSR of 76 and 84. No buildings. Hard surfaced road. Contract available.

Key Questions in Analyzing a Land Purchase § Does it fit in with the operation? l l Labor supply Machinery Livestock Location § Is it worth the asking price? l l Will the potential income support it? How is it priced relative to the market?

Key Questions in Analyzing a Land Purchase § Does it fit in with the operation? l l Labor supply Machinery Livestock Location § Is it worth the asking price? l l Will the potential income support it? How is it priced relative to the market?

Land Valuation: Capitalization of Earnings V=R/d V = value of asset R = expected annual earnings--$ d = discount rate Discount Rate Average cost of capital Minus expected inflation rate Equals discount rate 6 -7% 2 -3% 4%

Land Valuation: Capitalization of Earnings V=R/d V = value of asset R = expected annual earnings--$ d = discount rate Discount Rate Average cost of capital Minus expected inflation rate Equals discount rate 6 -7% 2 -3% 4%

Net Returns to Land Corn Soybeans Yield 165 52 Price $2. 40 $6. 00 Gross income $396 $312 USDA direct payment Seed, fert, pest. Mach. Ownership Mach. Operating Drying Labor Total nonland costs Property taxes, etc. Net return to land 160 40 30 21 25 $276 100 25 20 0 23 $168 Average $354 24 $378 $222 24 $132

Net Returns to Land Corn Soybeans Yield 165 52 Price $2. 40 $6. 00 Gross income $396 $312 USDA direct payment Seed, fert, pest. Mach. Ownership Mach. Operating Drying Labor Total nonland costs Property taxes, etc. Net return to land 160 40 30 21 25 $276 100 25 20 0 23 $168 Average $354 24 $378 $222 24 $132

Capitalized Land Value § Land value = $132 /. 04 = $3, 300 per acre

Capitalized Land Value § Land value = $132 /. 04 = $3, 300 per acre

2. Costs of production 3.") Farmland values depend on: 1. Productivity (supply of crops) 2. Costs of production 3. Crop selling prices (demand) 4. Interest rates 5. Inflation 6. Alternative investments

Farmland values depend on: 1. Productivity (supply of crops) 2. Costs of production 3. Crop selling prices (demand) 4. Interest rates 5. Inflation 6. Alternative investments

Comparative Sales § Recent actual sales § Similar land § Same area

Comparative Sales § Recent actual sales § Similar land § Same area

Comparative Sales Factors to compare: § Productivity + § Location + or § Other uses/income + or § Family sales § Sales contract + § Size of tract + or -

Comparative Sales Factors to compare: § Productivity + § Location + or § Other uses/income + or § Family sales § Sales contract + § Size of tract + or -

Value Based on Productivity CSR Rating X $ per CSR point = Estimated value Example: Comp. sales averaged $50 per CSR point $50/ CSR point x 80 CSR = $4, 000

Value Based on Productivity CSR Rating X $ per CSR point = Estimated value Example: Comp. sales averaged $50 per CSR point $50/ CSR point x 80 CSR = $4, 000

Adjust for % Tillable § Example: § 75 acres tillable out of 80 = 93. 75% § $3, 000 x 93. 75% = $3, 750 per acre

Adjust for % Tillable § Example: § 75 acres tillable out of 80 = 93. 75% § $3, 000 x 93. 75% = $3, 750 per acre

Financial Analysis of a Land Purchase § Where can I obtain financing? l l Equity (savings) Credit Installment contract § Will it cash flow? l l l On its own? With help from other sources?

Financial Analysis of a Land Purchase § Where can I obtain financing? l l Equity (savings) Credit Installment contract § Will it cash flow? l l l On its own? With help from other sources?

Loan amount(2/3) Amortization factor (7%, 25") Cash Flow Analysis Sale price Down payment (1/3) Loan amount(2/3) Amortization factor (7%, 25 yr loan) (p. 418) § Annual payment § Income available § Surplus/deficit § § § $3, 600 -1, 200 = $2, 400 x. 0858 = $206 $120 (86)

Cash Flow Analysis Sale price Down payment (1/3) Loan amount(2/3) Amortization factor (7%, 25 yr loan) (p. 418) § Annual payment § Income available § Surplus/deficit § § § $3, 600 -1, 200 = $2, 400 x. 0858 = $206 $120 (86)

Characteristics of Farmland § Does not depreciate or wear out § Supply is fixed § Each parcel is unique § Values depend on profits from agriculture, other uses § Ownership provides security, pride

Characteristics of Farmland § Does not depreciate or wear out § Supply is fixed § Each parcel is unique § Values depend on profits from agriculture, other uses § Ownership provides security, pride

Farmland Leasing in Iowa Land § Farmed by owner 46% § Farmed by tenant 54% Types of Leases--acres § Cash 69% § Crop Share 30% § Other 1%

Farmland Leasing in Iowa Land § Farmed by owner 46% § Farmed by tenant 54% Types of Leases--acres § Cash 69% § Crop Share 30% § Other 1%

Own vs. Rent § § § Ownership Security Inflation hedge Pride Build equity Loan collateral § § Rental Flexibility Lower cash cost No investment Larger scale

Own vs. Rent § § § Ownership Security Inflation hedge Pride Build equity Loan collateral § § Rental Flexibility Lower cash cost No investment Larger scale

Cash Leases § Tenant pays a fixed rate § Tenant takes all the risk § Rent may be due in advance § Most are one-year agreements § More management freedom § Fewer records to keep

Cash Leases § Tenant pays a fixed rate § Tenant takes all the risk § Rent may be due in advance § Most are one-year agreements § More management freedom § Fewer records to keep

= gross income - nonland") Estimating a Fair Rent Tenant’s Residual (max. to pay) = gross income - nonland costs gross income $378 nonland costs 222 residual $156 Machinery fixed costs? Labor?

Estimating a Fair Rent Tenant’s Residual (max. to pay) = gross income - nonland costs gross income $378 nonland costs 222 residual $156 Machinery fixed costs? Labor?

C:") Estimating a Fair Rent % of gross income (typically 35 to 40 %) C: ($396 + $24) x 35% = $147 SB: ($312 + $24) x 40% = $134

Estimating a Fair Rent % of gross income (typically 35 to 40 %) C: ($396 + $24) x 35% = $147 SB: ($312 + $24) x 40% = $134

Cash Rent Based on Yields § Corn: $. 90 - $1. 00 per bushel § Soybeans: $2. 70 - $3. 00 per bu. § Example: Corn: 165 bu. X $. 90 = $148 Soybeans: 52 bu. X $2. 80 = $146

Cash Rent Based on Yields § Corn: $. 90 - $1. 00 per bushel § Soybeans: $2. 70 - $3. 00 per bu. § Example: Corn: 165 bu. X $. 90 = $148 Soybeans: 52 bu. X $2. 80 = $146

Flexible Cash Leases § Rent is paid in cash § Amount of rent depends on actual prices and/or yields § Tenant pays all crop expenses § Tenant and owner share risks § Must agree on how to calculate rent, and how to determine actual price and yield

Flexible Cash Leases § Rent is paid in cash § Amount of rent depends on actual prices and/or yields § Tenant pays all crop expenses § Tenant and owner share risks § Must agree on how to calculate rent, and how to determine actual price and yield

Flexible Rent Example Rent = % of Gross Revenue Typical: 30 -40% (165 bu. @ $2. 40 + $24) x 35% = $158 (100 bu. @ $2. 80 + $24) x 35% = $106 (200 bu. @ $2. 50 + $24) x 35% = $183 -Usually include government payments. -May set a minimum and maximum rent.

Flexible Rent Example Rent = % of Gross Revenue Typical: 30 -40% (165 bu. @ $2. 40 + $24) x 35% = $158 (100 bu. @ $2. 80 + $24) x 35% = $106 (200 bu. @ $2. 50 + $24) x 35% = $183 -Usually include government payments. -May set a minimum and maximum rent.

Crop Share Leases § Tenant and owner divide crop l 1/2 and 1/2 is typical § Tenant and owner share cost of crop inputs (seed, fertilizer, pesticides, drying, crop insurance) § Tenant supplies labor and machinery § Both price and production risk are shared § Less capital is required from tenant

Crop Share Leases § Tenant and owner divide crop l 1/2 and 1/2 is typical § Tenant and owner share cost of crop inputs (seed, fertilizer, pesticides, drying, crop insurance) § Tenant supplies labor and machinery § Both price and production risk are shared § Less capital is required from tenant

Evaluating a Share Lease Corn Total Seed, fert, pest $160 Machinery $ 70 Drying 21 Labor 25 Management 20 (5% of gross $396) Land $140 Total $436 Share 100% Tenant $80 70 15 25 20 Owner $80 0 6 0 0 0 $210 48% 140 $226 52%

Evaluating a Share Lease Corn Total Seed, fert, pest $160 Machinery $ 70 Drying 21 Labor 25 Management 20 (5% of gross $396) Land $140 Total $436 Share 100% Tenant $80 70 15 25 20 Owner $80 0 6 0 0 0 $210 48% 140 $226 52%

Developing a Good Lease § Discuss details and put it in writing § Treat the land as if it were your own § Communicate frequently § Consider environmental effects § Go the extra mile § The tenant that will pay the most is not always the best

Developing a Good Lease § Discuss details and put it in writing § Treat the land as if it were your own § Communicate frequently § Consider environmental effects § Go the extra mile § The tenant that will pay the most is not always the best

Custom Farming § Operator supplies labor and machinery, only § May buy supplies, choose inputs, etc. § Receives a fixed payment, sometimes a bonus or % of crop § Owner takes all the risk

Custom Farming § Operator supplies labor and machinery, only § May buy supplies, choose inputs, etc. § Receives a fixed payment, sometimes a bonus or % of crop § Owner takes all the risk

Livestock Share Lease § Crop costs split same as crop-share lease § Owner provide buildings, pasture, stationary equipment § Tenant provides movable equipment, labor § Divide livestock, feed, operating costs § Divide income equally § Not very common now

Livestock Share Lease § Crop costs split same as crop-share lease § Owner provide buildings, pasture, stationary equipment § Tenant provides movable equipment, labor § Divide livestock, feed, operating costs § Divide income equally § Not very common now

Contract Farming § Usually involves growing specialty crops l § § § high oil corn, seed corn, organic grains, etc May receive a fixed payment May receive a guaranteed price Must meet quality standards Management requirements are stricter May need separate storage Need a guaranteed market

Contract Farming § Usually involves growing specialty crops l § § § high oil corn, seed corn, organic grains, etc May receive a fixed payment May receive a guaranteed price Must meet quality standards Management requirements are stricter May need separate storage Need a guaranteed market

Contract Finishing § Operator provides buildings, labor, operating costs § Contractor provides animals, feed, health services, marketing § Operator receives a fixed payment per animal or space. May have a bonus. § Limited risk, limited returns

Contract Finishing § Operator provides buildings, labor, operating costs § Contractor provides animals, feed, health services, marketing § Operator receives a fixed payment per animal or space. May have a bonus. § Limited risk, limited returns

§ Operator supplies feedlot, labor, feed, and all operating expenses") Custom Feeding (mostly cattle) § Operator supplies feedlot, labor, feed, and all operating expenses § Owner of cattle pays a yardage fee ($ per head per day) plus health costs, feed costs, transportation

Custom Feeding (mostly cattle) § Operator supplies feedlot, labor, feed, and all operating expenses § Owner of cattle pays a yardage fee ($ per head per day) plus health costs, feed costs, transportation