4b69a6a31abfa06c39a8fe9d443259cf.ppt

- Количество слайдов: 68

Executive Master in International Postal Management Patrick Foley April, 2010

Executive Master in International Postal Management Patrick Foley April, 2010

Executive Master in International Postal Management Innovation Managing in Complex and Uncertain Times: Red and Blue Oceans Tuesday 13 th April, 2010 Patrick Foley

Executive Master in International Postal Management Innovation Managing in Complex and Uncertain Times: Red and Blue Oceans Tuesday 13 th April, 2010 Patrick Foley

Innovation has a range of meanings and applications Definitions of innovation · A successfully commercialised invention · A learning process where knowledge is enhanced and applied · The solution of problems through discovery and creation · The successful production, assimilation and exploitation of novelty · A new or different solution to a new or existing problem · Device + Marketing · Systematic entrepreneurship · The process of turning an idea into income - commercialising invention · The search for, discovery experimentation, development, imitation and adoption of new products, new processes and new organisational set-ups · The effort to create purposeful, focused change in an enterprise’s economic or social potential

Innovation has a range of meanings and applications Definitions of innovation · A successfully commercialised invention · A learning process where knowledge is enhanced and applied · The solution of problems through discovery and creation · The successful production, assimilation and exploitation of novelty · A new or different solution to a new or existing problem · Device + Marketing · Systematic entrepreneurship · The process of turning an idea into income - commercialising invention · The search for, discovery experimentation, development, imitation and adoption of new products, new processes and new organisational set-ups · The effort to create purposeful, focused change in an enterprise’s economic or social potential

Innovation = Invention + Commercial Exploitation Is inventing the light bulb enough? No : it must pass the five tests of a new innovation 1. Function Test (does it perform the function? ) 2. Mass Production Test (can it be mass produced? ) 3. Market test (will it sell/ is there a solid market channel? ) 4. Financial test (Can we do all the above at a profit? ) 5. Permission Test (can it be legally used in the context intended)

Innovation = Invention + Commercial Exploitation Is inventing the light bulb enough? No : it must pass the five tests of a new innovation 1. Function Test (does it perform the function? ) 2. Mass Production Test (can it be mass produced? ) 3. Market test (will it sell/ is there a solid market channel? ) 4. Financial test (Can we do all the above at a profit? ) 5. Permission Test (can it be legally used in the context intended)

Innovation and Value Creation The Marketing and Sales departments must understand the customer and translate this knowledge into product design parameters. CUSTOMER NEEDS Also, advances in product design can occur ahead of needs. PRODUCT DESIGNS & SERVICES The production process must be capable of meeting the design specifications. Also, the design should facilitate ease of production and take advantage of production systems, technologies etc. Delivery, installation, commissioning and after sales service and support must all meet or exceed the customers expectations. PRODUCTION

Innovation and Value Creation The Marketing and Sales departments must understand the customer and translate this knowledge into product design parameters. CUSTOMER NEEDS Also, advances in product design can occur ahead of needs. PRODUCT DESIGNS & SERVICES The production process must be capable of meeting the design specifications. Also, the design should facilitate ease of production and take advantage of production systems, technologies etc. Delivery, installation, commissioning and after sales service and support must all meet or exceed the customers expectations. PRODUCTION

Sources of innovation fall into two distinct categories Four sources of opportunity exist within a company or industry · Unexpected occurrences · Three exist outside a company’s social & intellectual environment Incongruities · Process needs · Industry & market changes · Demographic changes · Changes in perception · New knowledge Source: Professor Peter F. Drucker, Innovation and Entrepreneurship: Practice and Principles; Harvard Business Review: Innovation, 1991

Sources of innovation fall into two distinct categories Four sources of opportunity exist within a company or industry · Unexpected occurrences · Three exist outside a company’s social & intellectual environment Incongruities · Process needs · Industry & market changes · Demographic changes · Changes in perception · New knowledge Source: Professor Peter F. Drucker, Innovation and Entrepreneurship: Practice and Principles; Harvard Business Review: Innovation, 1991

7

7

In all cases, the outcome is the creation of something new and transformational Examples of innovative inventions External opportunities Internal opportunities · The unexpected Du Pont’s Nylon, G. D. Searle’s Nutra. Sweet, Alexander Fleming’s penicillin · The incongruity Alcon Industries’ cataract enzyme, Ro-Ro container ships · Process needs AT&T’s automatic switchboard, Mergenthaler’s Linotype, Ochs, Pulitzer and Randolph Hearst’s modern advertising · Changes in industry or market structure Nokia’s mobile phones, investment banking, the car · Demographics BUPA’s healthcare insurance, Japan’s robotics industry, Club Mediterranee’s travel & resort business · Changes in perception Pfizer’s Viagra, organic food · New knowledge J. P. Morgan’s commercial banking, Douglas & Boeing’s commercial aircraft, the computer

In all cases, the outcome is the creation of something new and transformational Examples of innovative inventions External opportunities Internal opportunities · The unexpected Du Pont’s Nylon, G. D. Searle’s Nutra. Sweet, Alexander Fleming’s penicillin · The incongruity Alcon Industries’ cataract enzyme, Ro-Ro container ships · Process needs AT&T’s automatic switchboard, Mergenthaler’s Linotype, Ochs, Pulitzer and Randolph Hearst’s modern advertising · Changes in industry or market structure Nokia’s mobile phones, investment banking, the car · Demographics BUPA’s healthcare insurance, Japan’s robotics industry, Club Mediterranee’s travel & resort business · Changes in perception Pfizer’s Viagra, organic food · New knowledge J. P. Morgan’s commercial banking, Douglas & Boeing’s commercial aircraft, the computer

What type of competitive advantage does/could the innovation contribute to?

What type of competitive advantage does/could the innovation contribute to?

What is the driver of Innovations Cost Advantage?

What is the driver of Innovations Cost Advantage?

How does the innovation help to differentiate?

How does the innovation help to differentiate?

Red Ocean versus Blue Ocean Strategy The imperative for red ocean and blue ocean strategies are starkly different Red Ocean Strategy § § § Compete in existing market space Beat the competition Exploit existing demand Make the value/cost trade off Align the whole system/activities with either differentiation or low cost Blue Ocean Strategy § § § Create uncontested market space Make the competition irrelevant Create and capture new demand Break the value/cost trade off Align the whole system/activities in pursuit of differentiation and low cost

Red Ocean versus Blue Ocean Strategy The imperative for red ocean and blue ocean strategies are starkly different Red Ocean Strategy § § § Compete in existing market space Beat the competition Exploit existing demand Make the value/cost trade off Align the whole system/activities with either differentiation or low cost Blue Ocean Strategy § § § Create uncontested market space Make the competition irrelevant Create and capture new demand Break the value/cost trade off Align the whole system/activities in pursuit of differentiation and low cost

Porter’s Five Forces Model POTENTIAL ENTRANTS Threat of new entrants Bargaining power of suppliers INDUSTRY COMPETITORS SUPPLIERS Bargaining power of buyers (customers) BUYERS Rivalry among existing firms Threat of substitute products or services SUBSTITUTES Source: M. E. Porter, Competitive Advantage (1985) (Competitive forces) determine the profit potential of the industry and therefore, its attractiveness

Porter’s Five Forces Model POTENTIAL ENTRANTS Threat of new entrants Bargaining power of suppliers INDUSTRY COMPETITORS SUPPLIERS Bargaining power of buyers (customers) BUYERS Rivalry among existing firms Threat of substitute products or services SUBSTITUTES Source: M. E. Porter, Competitive Advantage (1985) (Competitive forces) determine the profit potential of the industry and therefore, its attractiveness

Forces Determining Industry Attractiveness 1. Intensity of Direct Competition – – – Excess production capacity Standardised products Large number of competitors Low market growth Commitment to industry

Forces Determining Industry Attractiveness 1. Intensity of Direct Competition – – – Excess production capacity Standardised products Large number of competitors Low market growth Commitment to industry

Forces Determining Industry Attractiveness 2. Buyer Power – Price sensitivity of buyers • A function of buyer profitability/perceived benefits • Proportion of product’s cost in their total expenditures – Negotiating power • Few buyers • Many manufacturers • Little differentiation • Low switching costs • Opportunities for backward integration (for industrial buyers)

Forces Determining Industry Attractiveness 2. Buyer Power – Price sensitivity of buyers • A function of buyer profitability/perceived benefits • Proportion of product’s cost in their total expenditures – Negotiating power • Few buyers • Many manufacturers • Little differentiation • Low switching costs • Opportunities for backward integration (for industrial buyers)

Forces Determining Industry Attractiveness 3. Threat of new entry – Weak barriers to entry (and demonstrated profitability) encourage new firms to enter industries • Patents & the diffusion of proprietary knowledge (e. g. , pharmaceuticals) • Legislation (e. g. , airlines) • Economies of scale (i. e. , minimum efficient scale) • Capital requirements (e. g. , telecoms) • Strength & importance of brands • Threat of retaliation • Access to distribution channels

Forces Determining Industry Attractiveness 3. Threat of new entry – Weak barriers to entry (and demonstrated profitability) encourage new firms to enter industries • Patents & the diffusion of proprietary knowledge (e. g. , pharmaceuticals) • Legislation (e. g. , airlines) • Economies of scale (i. e. , minimum efficient scale) • Capital requirements (e. g. , telecoms) • Strength & importance of brands • Threat of retaliation • Access to distribution channels

Forces Determining Industry Attractiveness 4. Threat of substitutes – Indirect competitors that can undermine demand prices • Alternative products (e. g. , cotton / wool) • New products (e. g. , telex -> fax -> e-mail) • Elimination of need (e. g. , choice fuels eliminating fuel additives) • Generic substitution (e. g. , broad categories of ‘leisure’ products competing for discretionary spending) • Abstinence

Forces Determining Industry Attractiveness 4. Threat of substitutes – Indirect competitors that can undermine demand prices • Alternative products (e. g. , cotton / wool) • New products (e. g. , telex -> fax -> e-mail) • Elimination of need (e. g. , choice fuels eliminating fuel additives) • Generic substitution (e. g. , broad categories of ‘leisure’ products competing for discretionary spending) • Abstinence

Forces Determining Industry Attractiveness 5. Power of suppliers – Suppliers limit industry attractiveness and profitability if they can increase input costs faster than they can be passed on • Few suppliers available • Suppliers have unique products • Switching costs are high • Threat of forward integration • Large number of small customers

Forces Determining Industry Attractiveness 5. Power of suppliers – Suppliers limit industry attractiveness and profitability if they can increase input costs faster than they can be passed on • Few suppliers available • Suppliers have unique products • Switching costs are high • Threat of forward integration • Large number of small customers

Porter’s Five Forces Model § The model systematically captures the business logic that all managers are intuitively familiar with: – – An industry that has weak suppliers and buyers… High barriers to entry… No substitutes… POTENTIAL ENTRANTS and is a monopoly. . . High Will be very profitable! Weak INDUSTRY COMPETITORS SUPPLIERS Weak BUYERS Rivalry among existing firms No rivalry (monopoly) None SUBSTITUTES

Porter’s Five Forces Model § The model systematically captures the business logic that all managers are intuitively familiar with: – – An industry that has weak suppliers and buyers… High barriers to entry… No substitutes… POTENTIAL ENTRANTS and is a monopoly. . . High Will be very profitable! Weak INDUSTRY COMPETITORS SUPPLIERS Weak BUYERS Rivalry among existing firms No rivalry (monopoly) None SUBSTITUTES

Narrow Scope (Market Segment) Differentiation") Generic Strategies Source of Advantage Broad Scope (Industry wide) Narrow Scope (Market Segment) Differentiation Cost Leadership Focus Porter (1980)

Generic Strategies Source of Advantage Broad Scope (Industry wide) Narrow Scope (Market Segment) Differentiation Cost Leadership Focus Porter (1980)

Porter’s Competitive Advantage § Remember that a companies overall business strategy will drive all other strategies. § Porter defined these competitive advantages to represent various business strategies found in the marketplace. § Cost leadership strategy firms include Walmart, Suzuki, Overstock. com, etc. § Differentiation strategy firms include Coca Cola, Progressive Insurance, Publix, etc. § Focus strategy firms include the Ritz Carlton, Marriott, etc.

Porter’s Competitive Advantage § Remember that a companies overall business strategy will drive all other strategies. § Porter defined these competitive advantages to represent various business strategies found in the marketplace. § Cost leadership strategy firms include Walmart, Suzuki, Overstock. com, etc. § Differentiation strategy firms include Coca Cola, Progressive Insurance, Publix, etc. § Focus strategy firms include the Ritz Carlton, Marriott, etc.

STEP Framework STEP Analysis Factors Socio-cultural – Demographics – Social Trends Technological – Available infrastructure – Product / Process technology – E-commerce / routes to market Economic – Economic cycles – Unemployment / inflation – Tariffs Political-Legal – Stability of government – Regulations (e. g. , employment law) Potential Impact Type of Impact H – high M – Medium + Positive L – Low U - Undetermined - Negative ? Unknown Time Frame 0 -6 Months 6 -12 Months 12 -24 Months 24+ Months ∆ Impact > Increasing = Unchanging < Decreasing

STEP Framework STEP Analysis Factors Socio-cultural – Demographics – Social Trends Technological – Available infrastructure – Product / Process technology – E-commerce / routes to market Economic – Economic cycles – Unemployment / inflation – Tariffs Political-Legal – Stability of government – Regulations (e. g. , employment law) Potential Impact Type of Impact H – high M – Medium + Positive L – Low U - Undetermined - Negative ? Unknown Time Frame 0 -6 Months 6 -12 Months 12 -24 Months 24+ Months ∆ Impact > Increasing = Unchanging < Decreasing

Differentiation Strategy Variants § Shareholder value model: create advantage through the use of knowledge and timing (Fruhan) § Unlimited resources model: companies with a large resource can sustain losses more easily than ones with fewer resources (Chain Store vs Mom & Pop). § The problem with Porter and these variants are that the rate of change is no longer easily managed and sustained.

Differentiation Strategy Variants § Shareholder value model: create advantage through the use of knowledge and timing (Fruhan) § Unlimited resources model: companies with a large resource can sustain losses more easily than ones with fewer resources (Chain Store vs Mom & Pop). § The problem with Porter and these variants are that the rate of change is no longer easily managed and sustained.

Understanding Competitors

Understanding Competitors

Understanding Competitors 1. Size, Growth, and Profitability Position – Indicates level of resources (e. g. , to defend or advance a market position) – Commitment to segment or industry (e. g. , pursuing growth at the expense of profitability)

Understanding Competitors 1. Size, Growth, and Profitability Position – Indicates level of resources (e. g. , to defend or advance a market position) – Commitment to segment or industry (e. g. , pursuing growth at the expense of profitability)

Understanding Competitors 2. Strategic objectives of competitors – Differentiation via: • Product line breadth • Product quality • Service support • Distribution channel • Brand – Cost leadership via: • Scale • Experience • Sourcing novation roduct In P ntimacy Customer I cellence perating Ex O

Understanding Competitors 2. Strategic objectives of competitors – Differentiation via: • Product line breadth • Product quality • Service support • Distribution channel • Brand – Cost leadership via: • Scale • Experience • Sourcing novation roduct In P ntimacy Customer I cellence perating Ex O

Understanding Competitors 3. Competitors’ branding objectives – Intended brand positioning indicates likely strategic initiatives • ‘Innovative’ -> high R&D investment • ‘User friendly’ -> investment in service & support • ‘Value’ -> investment in efficient systems & manufacturing – Identifies unmet positions • Opportunities for building market share • Increasing profitability

Understanding Competitors 3. Competitors’ branding objectives – Intended brand positioning indicates likely strategic initiatives • ‘Innovative’ -> high R&D investment • ‘User friendly’ -> investment in service & support • ‘Value’ -> investment in efficient systems & manufacturing – Identifies unmet positions • Opportunities for building market share • Increasing profitability

Hypercompetition Often a characteristic of new markets and industries, hypercompetition occurs when technologies or offerings are so new that standards and rules are in flux, resulting in competitive advantages that cannot be sustained. In response, companies must constantly compete in price or quality, or innovate in , supply chain management , new value creation, or have enough financial capital to outlast other competitors.

Hypercompetition Often a characteristic of new markets and industries, hypercompetition occurs when technologies or offerings are so new that standards and rules are in flux, resulting in competitive advantages that cannot be sustained. In response, companies must constantly compete in price or quality, or innovate in , supply chain management , new value creation, or have enough financial capital to outlast other competitors.

§ Assumptions of D’Avenis Hypercompetition and the New 7 Ss Framework model: – Every advantage is eroded. – Sustaining an advantage can be a deadly distraction. – Goal of advantage should be disruption, not sustainability – Initiatives are achieved through series of small steps.

§ Assumptions of D’Avenis Hypercompetition and the New 7 Ss Framework model: – Every advantage is eroded. – Sustaining an advantage can be a deadly distraction. – Goal of advantage should be disruption, not sustainability – Initiatives are achieved through series of small steps.

D’Aveni’s new 7 Ss § § The 7 Ss are useful for determining different aspects of a business strategy and aligning them to make the organization competitive in the hypercompetitive arena. The 7 Ss are: 1. Superior stakeholder satisfaction: maximize customer satisfaction by adding value strategically 2. Strategic soothsaying: use new knowledge to predict new windows of opportunity 3. Positioning for speed: prepare the org. to react as fast as possible 4. Positioning for surprise: surprise competitors 5. Shifting the rules of competition: serve customers in novel ways 6. Signaling strategic intent: communicate intensions in order to stall competitors 7. Simultaneous and sequential strategic thrusts: take steps to stun and confuse competitors in order to disrupt or block their efforts

D’Aveni’s new 7 Ss § § The 7 Ss are useful for determining different aspects of a business strategy and aligning them to make the organization competitive in the hypercompetitive arena. The 7 Ss are: 1. Superior stakeholder satisfaction: maximize customer satisfaction by adding value strategically 2. Strategic soothsaying: use new knowledge to predict new windows of opportunity 3. Positioning for speed: prepare the org. to react as fast as possible 4. Positioning for surprise: surprise competitors 5. Shifting the rules of competition: serve customers in novel ways 6. Signaling strategic intent: communicate intensions in order to stall competitors 7. Simultaneous and sequential strategic thrusts: take steps to stun and confuse competitors in order to disrupt or block their efforts

Vision for Disruption Identifying and creating opportunities for temporary advantage via understanding • Stakeholder satisfaction • Strategic soothsaying to ID new ways to serve current customers better or serve those not being served Capability for Disruption Sustaining the momentum by developing abilities for: • Speed • Surprise that can be applied across many actions to build a series of temporary advantages Market Disruption Tactics for Disruption Seizing the initiative to gain advantage by • Shifting the rules • Signaling • Strategic thrusts with actions that shape, mould or influence the direction or nature of competitors’ responses

Vision for Disruption Identifying and creating opportunities for temporary advantage via understanding • Stakeholder satisfaction • Strategic soothsaying to ID new ways to serve current customers better or serve those not being served Capability for Disruption Sustaining the momentum by developing abilities for: • Speed • Surprise that can be applied across many actions to build a series of temporary advantages Market Disruption Tactics for Disruption Seizing the initiative to gain advantage by • Shifting the rules • Signaling • Strategic thrusts with actions that shape, mould or influence the direction or nature of competitors’ responses

Limitations of Traditional View § A key limitation of all the above strategies is that it ignores the dynamics of competition in the marketplace. § While the issue of foremost importance for the company is the customer, D’Aveni notes that competitive interaction among firms typically goes through six stages

Limitations of Traditional View § A key limitation of all the above strategies is that it ignores the dynamics of competition in the marketplace. § While the issue of foremost importance for the company is the customer, D’Aveni notes that competitive interaction among firms typically goes through six stages

Hypercompetition § D’Aveni developed a model that stated that sustainable competitive advantage could NOT be sustained. § Called the “Hypercompetition and the New 7 Ss Framework”. § Competitive advantage is rapidly erased by competition and the market.

Hypercompetition § D’Aveni developed a model that stated that sustainable competitive advantage could NOT be sustained. § Called the “Hypercompetition and the New 7 Ss Framework”. § Competitive advantage is rapidly erased by competition and the market.

Strategic Competitive Advantage Exploitation Profits from a sustained competitive advantage Launch Counterattack Traditional View Time Firm has already moved to advantage 2 Profits from a series of actions Exploitation Counterattack Hypercompetition Launch Time

Strategic Competitive Advantage Exploitation Profits from a sustained competitive advantage Launch Counterattack Traditional View Time Firm has already moved to advantage 2 Profits from a series of actions Exploitation Counterattack Hypercompetition Launch Time

• Timing and know-how") Hypercompetition Four arenas of competition • Cost & Quality (C-Q) • Timing and know-how (T-K) • Strongholds (S) • Deep pockets (D)

Hypercompetition Four arenas of competition • Cost & Quality (C-Q) • Timing and know-how (T-K) • Strongholds (S) • Deep pockets (D)

Coke vs. Pepsi Price / Ounce § Coke: 1886; Pepsi: 1893 1933: Pepsi struggling to stave off bankruptcy. Dropped price of its 10 c, 12 oz. bottle to 5 c, making it a better value Ad jingle “twice as much for a nickel” better known in the US than the Star Spangled Banner Pepsi Coke Perceived Quality Price / Ounce § § Coke Pepsi Perceived Quality

Coke vs. Pepsi Price / Ounce § Coke: 1886; Pepsi: 1893 1933: Pepsi struggling to stave off bankruptcy. Dropped price of its 10 c, 12 oz. bottle to 5 c, making it a better value Ad jingle “twice as much for a nickel” better known in the US than the Star Spangled Banner Pepsi Coke Perceived Quality Price / Ounce § § Coke Pepsi Perceived Quality

Coke vs. Pepsi, Contd. . u u Pepsi Coke Youth & Middle Class Segments Perceived Quality Price / Ounce u Pepsi keeps price advantage through 60 s and 70 s, when Pepsi charged its bottlers 20% less for its concentrate With rising ingredient costs, Pepsi could no longer offer twice as much for the same price. So it raised price to Coke’s level giving it a war chest to fuel an aggressive ad campaign Battle shifted from Price to Quality, with Pepsi targeting the youth What followed was the Pepsi Challenge & “Real Thing” Coke ads Price / Ounce u First move: Pepsi Challenge 2 nd move: Coke’s Ad war Perceived Quality

Coke vs. Pepsi, Contd. . u u Pepsi Coke Youth & Middle Class Segments Perceived Quality Price / Ounce u Pepsi keeps price advantage through 60 s and 70 s, when Pepsi charged its bottlers 20% less for its concentrate With rising ingredient costs, Pepsi could no longer offer twice as much for the same price. So it raised price to Coke’s level giving it a war chest to fuel an aggressive ad campaign Battle shifted from Price to Quality, with Pepsi targeting the youth What followed was the Pepsi Challenge & “Real Thing” Coke ads Price / Ounce u First move: Pepsi Challenge 2 nd move: Coke’s Ad war Perceived Quality

Coke vs. Pepsi, Contd. . u u Generics RC Cola Coke & Pepsi Price Spiral Perceived Quality Price / Ounce u Perceived quality caught up. Deeper pocketed and lower cost Coke initiated a price war in selective markets where Pepsi was weak in the 70 s. Pepsi responded with its discounts and by the end of the 80 s, 50% of food store sales were on discount Other companies moved into the lower left quadrant of the market. But the two major players forced price down to “ultimate value. ” To break price spiral, Coke launched New Coke to keep Coke loyals and induce switching among Pepsi buyers. Rejected by market. Attempts to move to next arena via niches in caffeine and sugar substitutes Price / Ounce u New. Coke Classic Coke & Pepsi Actual New. Coke Intended Perceived Quality

Coke vs. Pepsi, Contd. . u u Generics RC Cola Coke & Pepsi Price Spiral Perceived Quality Price / Ounce u Perceived quality caught up. Deeper pocketed and lower cost Coke initiated a price war in selective markets where Pepsi was weak in the 70 s. Pepsi responded with its discounts and by the end of the 80 s, 50% of food store sales were on discount Other companies moved into the lower left quadrant of the market. But the two major players forced price down to “ultimate value. ” To break price spiral, Coke launched New Coke to keep Coke loyals and induce switching among Pepsi buyers. Rejected by market. Attempts to move to next arena via niches in caffeine and sugar substitutes Price / Ounce u New. Coke Classic Coke & Pepsi Actual New. Coke Intended Perceived Quality

The Cycle of Price-Quality Competition - Moving Up the Escalation Ladder Move to the next Arena Return to Price Wars Commodity like Market Attempt to redefine Quality Move to Ultimate Value Niching & Outflanking Full line Producers Price-Quality Maneuvers Price War

The Cycle of Price-Quality Competition - Moving Up the Escalation Ladder Move to the next Arena Return to Price Wars Commodity like Market Attempt to redefine Quality Move to Ultimate Value Niching & Outflanking Full line Producers Price-Quality Maneuvers Price War

Firm builds a Tech. Resource Base to create advantage Escalating costs & risks each cycle Then moves into a new market first: Pioneer Followers imitate products & overcome switching costs and brand loyalties Pioneer throws up impediments to imitation Followers overcome impediments and replicate pioneer’s resource base First mover uses a Transformation Strategy & abandons product design/ technology based approach Builds resources to match followers manufacturing skills Price War First mover moves downstream into higher value added products First mover uses a Leapfrog Strategy to a new resource base Cycle of Timing / Know-How Competition

Firm builds a Tech. Resource Base to create advantage Escalating costs & risks each cycle Then moves into a new market first: Pioneer Followers imitate products & overcome switching costs and brand loyalties Pioneer throws up impediments to imitation Followers overcome impediments and replicate pioneer’s resource base First mover uses a Transformation Strategy & abandons product design/ technology based approach Builds resources to match followers manufacturing skills Price War First mover moves downstream into higher value added products First mover uses a Leapfrog Strategy to a new resource base Cycle of Timing / Know-How Competition

Build entry barrier around market A to exclude competition Build entry barrier around market B to exclude competition Circumvent barriers and attack niche in market B Short Run: Withdraw from niche or fail to respond Entrant breaches barriers or triggers price war in B Cycle restarts with entry into a new market Incumbent’s stronghold in B weakens as it grows more competitive Entrant responds in market A or in market B One firm builds new stronghold Other firm divests Delayed Response: Barriers to contain entrant to a segment of B Standoff until one party gains the upper hand in market A or B If one firm dominates Long Run: Incumbent attacks entrant’s market A to punish Both strongholds erode or merge into one market Price War STRONGHOLDS ARENA

Build entry barrier around market A to exclude competition Build entry barrier around market B to exclude competition Circumvent barriers and attack niche in market B Short Run: Withdraw from niche or fail to respond Entrant breaches barriers or triggers price war in B Cycle restarts with entry into a new market Incumbent’s stronghold in B weakens as it grows more competitive Entrant responds in market A or in market B One firm builds new stronghold Other firm divests Delayed Response: Barriers to contain entrant to a segment of B Standoff until one party gains the upper hand in market A or B If one firm dominates Long Run: Incumbent attacks entrant’s market A to punish Both strongholds erode or merge into one market Price War STRONGHOLDS ARENA

Deep pocket develops Antitrust laws invoked - work occasionally Small firms forced to outmaneuver deep pocket Cycle of Deep Pockets Competition Buyers or suppliers develop a countervailing force Hostile takeover of large firm Small firm escalates own resource base Cooperative strategy develops Avoidance strategy niching, etc. Large scale alliances form with equally deep pockets Deep pocket advantage is eliminated or neutralized Launches attack to drive out small firms New attempt to escalate resources

Deep pocket develops Antitrust laws invoked - work occasionally Small firms forced to outmaneuver deep pocket Cycle of Deep Pockets Competition Buyers or suppliers develop a countervailing force Hostile takeover of large firm Small firm escalates own resource base Cooperative strategy develops Avoidance strategy niching, etc. Large scale alliances form with equally deep pockets Deep pocket advantage is eliminated or neutralized Launches attack to drive out small firms New attempt to escalate resources

Framework Key Idea Application to Information Systems Porter’s generic strategies framework Firms achieve competitive advantage through cost leadership, differentiation, or focus. Understanding which strategy is chosen by a firm is critical D’Aveni’s hypercompetition model Speed and aggressive The 7 Ss give the manager suggestions on what moves and countermoves to make. countermoves by a firm create competitive advantage .

Framework Key Idea Application to Information Systems Porter’s generic strategies framework Firms achieve competitive advantage through cost leadership, differentiation, or focus. Understanding which strategy is chosen by a firm is critical D’Aveni’s hypercompetition model Speed and aggressive The 7 Ss give the manager suggestions on what moves and countermoves to make. countermoves by a firm create competitive advantage .

Ansoff’s Growth Vector Matrix PRODUCTS / SERVICES MARKET Present New Market penetration Product / Service development New Present Market development Diversification Source: D. T. Brownlie & C. K. Bart, Products and Strategies, MCB University Press, Vol. 11, No. 1, 1985, p. 29

Ansoff’s Growth Vector Matrix PRODUCTS / SERVICES MARKET Present New Market penetration Product / Service development New Present Market development Diversification Source: D. T. Brownlie & C. K. Bart, Products and Strategies, MCB University Press, Vol. 11, No. 1, 1985, p. 29

Using the Ansoff Matrix in the Objective-setting Process PRODUCTS / SERVICES Established New MARKET Established Market penetration (1) New Product / Service development (2) High Risk Market development (3) Diversification (4)

Using the Ansoff Matrix in the Objective-setting Process PRODUCTS / SERVICES Established New MARKET Established Market penetration (1) New Product / Service development (2) High Risk Market development (3) Diversification (4)

The Myth of the Linear Model of Innovation Basic Research Applied Research Development Commercialization Myth: Innovation is a Linear Process § Reality: Innovation is a Complex Process – Major overlap between Basic and Applied Research, as well as between Development and Commercialization – Principal Investigators and/or Patents and Processes are Mobile, i. e. , not firm-dependent – Many Unexpected Outcomes – Technological breakthroughs may precede, as well as stem from, basic research

The Myth of the Linear Model of Innovation Basic Research Applied Research Development Commercialization Myth: Innovation is a Linear Process § Reality: Innovation is a Complex Process – Major overlap between Basic and Applied Research, as well as between Development and Commercialization – Principal Investigators and/or Patents and Processes are Mobile, i. e. , not firm-dependent – Many Unexpected Outcomes – Technological breakthroughs may precede, as well as stem from, basic research

Non-Linear Model of Innovation Basic Research Quest for Basic Understanding • New Knowledge • Fundamental Ideas Potential Use • Application of Knowledge to a Specific Subject • “Prototypicalization” Feedback: • Basic Research needed for discovery • Search for new ideas and solutions to solve longer-term Feedback: Applied Research issues needed to design new product characteristics Applied Research Development Feedback: Market Signals/ Technical Challenge • Desired Product Alterations or New Characteristics • Cost/design trade-off New Unanticipated Applications Development of Products • Goods and Services Commercialization

Non-Linear Model of Innovation Basic Research Quest for Basic Understanding • New Knowledge • Fundamental Ideas Potential Use • Application of Knowledge to a Specific Subject • “Prototypicalization” Feedback: • Basic Research needed for discovery • Search for new ideas and solutions to solve longer-term Feedback: Applied Research issues needed to design new product characteristics Applied Research Development Feedback: Market Signals/ Technical Challenge • Desired Product Alterations or New Characteristics • Cost/design trade-off New Unanticipated Applications Development of Products • Goods and Services Commercialization

Principles of successful innovation § Analyse the sources of all new opportunities – These will have different importance at different times depending on the context – new knowledge may be of little relevance to someone innovating a social instrument to satisfy a need that changing demographics or tax laws have created. Think laterally and with vision. § Be aware of everything and everyone around you – Innovation is both conceptual and perceptual – go out and look, ask and listen. Successful innovators use both the right and left sides of the brain. They look at figures and people. They work out analytically what the innovation has to be to satisfy an opportunity. They look at potential users to study their expectations, their values and their needs.

Principles of successful innovation § Analyse the sources of all new opportunities – These will have different importance at different times depending on the context – new knowledge may be of little relevance to someone innovating a social instrument to satisfy a need that changing demographics or tax laws have created. Think laterally and with vision. § Be aware of everything and everyone around you – Innovation is both conceptual and perceptual – go out and look, ask and listen. Successful innovators use both the right and left sides of the brain. They look at figures and people. They work out analytically what the innovation has to be to satisfy an opportunity. They look at potential users to study their expectations, their values and their needs.

Principles of successful innovation § Focus on simple and specific areas § § – To be effective, an innovation has to be simple and focused. It should do only one thing otherwise it confuses people. Even the innovation that creates new users and new markets should be directed toward a specific clear and carefully designed application. Effective innovations start small. They try to do one specific thing and are based around a simple notion. They are not grandiose. By contrast, grandiose ideas for things that will ‘revolutionise an industry’ are unlikely to work. Aim for transformational innovations – The successful innovation aims from the beginning to become the standard setter, to determine the direction of a new technology or a new industry, to create the business that is – and remains – ahead of the pack. If an innovation does not aim at leadership from the beginning, it is unlikely to be innovative enough. Be systematic and persistent – Innovation is work rather than genius. It requires knowledge. It often requires ingenuity. And it requires focus. Innovators rarely work in more than one area – an innovator in financial areas is unlikely to embark on innovations in health care. Most of all, innovation requires hard, focused, purposeful work - if diligence, persistence and commitment are lacking, talent, ingenuity and knowledge are to no avail.

Principles of successful innovation § Focus on simple and specific areas § § – To be effective, an innovation has to be simple and focused. It should do only one thing otherwise it confuses people. Even the innovation that creates new users and new markets should be directed toward a specific clear and carefully designed application. Effective innovations start small. They try to do one specific thing and are based around a simple notion. They are not grandiose. By contrast, grandiose ideas for things that will ‘revolutionise an industry’ are unlikely to work. Aim for transformational innovations – The successful innovation aims from the beginning to become the standard setter, to determine the direction of a new technology or a new industry, to create the business that is – and remains – ahead of the pack. If an innovation does not aim at leadership from the beginning, it is unlikely to be innovative enough. Be systematic and persistent – Innovation is work rather than genius. It requires knowledge. It often requires ingenuity. And it requires focus. Innovators rarely work in more than one area – an innovator in financial areas is unlikely to embark on innovations in health care. Most of all, innovation requires hard, focused, purposeful work - if diligence, persistence and commitment are lacking, talent, ingenuity and knowledge are to no avail.

Continuum of Innovations

Continuum of Innovations

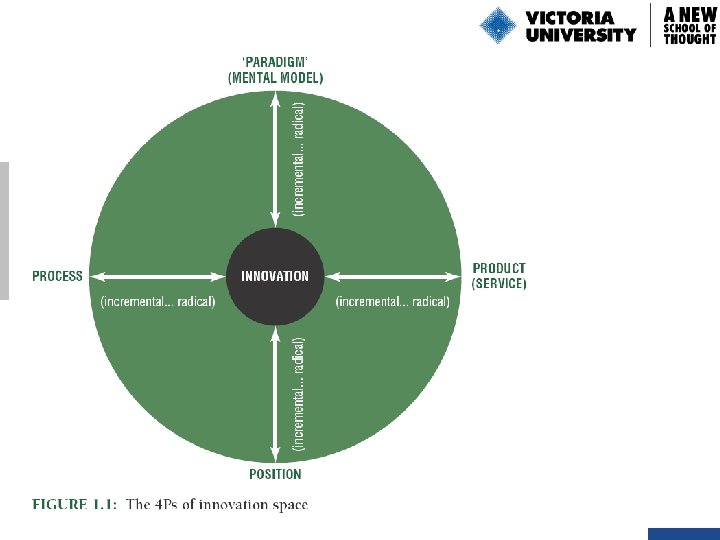

Dimensions of innovative space high low

Dimensions of innovative space high low

A range of options: innovativeness as it applies to products and services New to the world products/services New to the market products/services New product/service line in a country Additions to product service lines Product improvements/revisions New applications for existing products/services Repositioning of existing products/services Cost reductions for existing products/services

A range of options: innovativeness as it applies to products and services New to the world products/services New to the market products/services New product/service line in a country Additions to product service lines Product improvements/revisions New applications for existing products/services Repositioning of existing products/services Cost reductions for existing products/services

The Strategy Focused Organization Treacy and Wiersema propose that a business should follow four rules for success: 1. Become best at one of the three value disciplines. 2. Achieve an adequate performance level in the other two disciplines. 3. Keep improving one’s superior position in the chosen discipline so as not to lose out to a competitor. 4. Keep becoming more adequate in the other two disciplines, because competitors keep raising customers’ expectations.

The Strategy Focused Organization Treacy and Wiersema propose that a business should follow four rules for success: 1. Become best at one of the three value disciplines. 2. Achieve an adequate performance level in the other two disciplines. 3. Keep improving one’s superior position in the chosen discipline so as not to lose out to a competitor. 4. Keep becoming more adequate in the other two disciplines, because competitors keep raising customers’ expectations.

Operational Excellence • Companies that pursue this are not primarily product or service innovators, nor do they cultivate deep, one-to-one relationships with customers. • Operationally excellent companies provide middle-ofthe-market products at the best price with the least inconvenience.

Operational Excellence • Companies that pursue this are not primarily product or service innovators, nor do they cultivate deep, one-to-one relationships with customers. • Operationally excellent companies provide middle-ofthe-market products at the best price with the least inconvenience.

Product Leadership • Its practitioners concentrate on offering products that push performance boundaries. • Their proposition to customers is an offer of the best product, period.

Product Leadership • Its practitioners concentrate on offering products that push performance boundaries. • Their proposition to customers is an offer of the best product, period.

Customer Intimacy • Firms following this value discipline focus on delivering not what the market wants but what specific customers want. • Customer-intimate companies do not pursue one-time transactions; they cultivate relationships.

Customer Intimacy • Firms following this value discipline focus on delivering not what the market wants but what specific customers want. • Customer-intimate companies do not pursue one-time transactions; they cultivate relationships.

Pursuing Value Innovation: The Six Paths Framework 1. Across substitute industries Reduce What factors should be reduced well below the industry standard? 6. Across time/trends Eliminate What factors should be that eliminated the industry has taken for granted? 5. Across functional or emotional appeal Create New Value Curve Raise What factors should be raised well beyond the industry standard? 4. Across complementary offerings 2. Across strategic groups What factors should be created that the industry has never offered? 3. Across the chain of buyers

Pursuing Value Innovation: The Six Paths Framework 1. Across substitute industries Reduce What factors should be reduced well below the industry standard? 6. Across time/trends Eliminate What factors should be that eliminated the industry has taken for granted? 5. Across functional or emotional appeal Create New Value Curve Raise What factors should be raised well beyond the industry standard? 4. Across complementary offerings 2. Across strategic groups What factors should be created that the industry has never offered? 3. Across the chain of buyers

Challenges in New-Product Development – Incremental innovation – Disruptive technologies § Why do new products fail? – A high-level executive pushes a favorite idea through in spite of negative research findings. – The idea is good, but the market size is overestimated. – The product is not well designed.

Challenges in New-Product Development – Incremental innovation – Disruptive technologies § Why do new products fail? – A high-level executive pushes a favorite idea through in spite of negative research findings. – The idea is good, but the market size is overestimated. – The product is not well designed.

Challenges in New-Product Development – The product is incorrectly positioned in the market, not advertised effectively, or overpriced. – The product fails to gain sufficient distribution coverage or support. – Development costs are higher than expected. – Competitors fight back harder than expected.

Challenges in New-Product Development – The product is incorrectly positioned in the market, not advertised effectively, or overpriced. – The product fails to gain sufficient distribution coverage or support. – Development costs are higher than expected. – Competitors fight back harder than expected.

Market Definition, Size, Growth and Profitability § What is the market? How can it be defined? § How big is it/what’s the size of the opportunity? § What will affect its future growth? § What will affect its future profitability? § How much can you expect to capture? § How long will it be before others solutions erode your market share?

Market Definition, Size, Growth and Profitability § What is the market? How can it be defined? § How big is it/what’s the size of the opportunity? § What will affect its future growth? § What will affect its future profitability? § How much can you expect to capture? § How long will it be before others solutions erode your market share?

Factors affecting Growth and Profitability of Markets § All our assumptions so far have not considered factors that could impact on the growth and profitability of our selected markets § A number of models exist to systematically work through key factors to identify the most important ones – Environmental Audit – Industry Analysis

Factors affecting Growth and Profitability of Markets § All our assumptions so far have not considered factors that could impact on the growth and profitability of our selected markets § A number of models exist to systematically work through key factors to identify the most important ones – Environmental Audit – Industry Analysis

“Value innovation is about making the competition irrelevant by creating uncontested marketspace. We argue that beating the competition within the confines of the existing industry is not the way to create profitable growth. ” —Chan Kim & René Mauborgne from Blue Ocean Strategy

“Value innovation is about making the competition irrelevant by creating uncontested marketspace. We argue that beating the competition within the confines of the existing industry is not the way to create profitable growth. ” —Chan Kim & René Mauborgne from Blue Ocean Strategy

Value Innovation v. Conventional Strategic Thinking Dimension Conventional Value Innovation Logic Strategic Thinking Industry Conditions are given Conditions can be cha Strategy Build competitive Competition is not benchmar focus advantage to Pursue quantum leap i beat competition Customer Existing customers Mass markets focus Segment, customise Key commonalities Capabilities, Leverage existing What would we be doing if w assets ones started anew? Products, Determined by What is the total soluti services industry boundaries the customer?

Value Innovation v. Conventional Strategic Thinking Dimension Conventional Value Innovation Logic Strategic Thinking Industry Conditions are given Conditions can be cha Strategy Build competitive Competition is not benchmar focus advantage to Pursue quantum leap i beat competition Customer Existing customers Mass markets focus Segment, customise Key commonalities Capabilities, Leverage existing What would we be doing if w assets ones started anew? Products, Determined by What is the total soluti services industry boundaries the customer?

The Value Innovation Concept What factors should be eliminated that our industry takes for granted? What factors should be reduced well below the industry standard? Costs Cost savings from eliminating & reducing Value Innovation Cost advantages from high volume What factors should be raised well above the industry standard? What factors should be created that the industry has never offered? Buyer value Superior value by raising & creating

The Value Innovation Concept What factors should be eliminated that our industry takes for granted? What factors should be reduced well below the industry standard? Costs Cost savings from eliminating & reducing Value Innovation Cost advantages from high volume What factors should be raised well above the industry standard? What factors should be created that the industry has never offered? Buyer value Superior value by raising & creating

Factors of Competition

Factors of Competition

Value Curve of Formule 1 in the French Low Budget Hotel Industry using“Value Curves” to plot relative strategic positioning High F 1 2 Star Relative Level 1 Star Key elements of product, service, and delivery ice Pr ce en Sil e ien Hy g B Qu ed ali ty 2 Re 4 -H ce ou pt ion r ist Fu Roo Am rnit m en ure/ iti es e siz m Ro o Lo Ap ung pe e al E Fa atin cil g itie s Ar c Ae hitec sth tu eti ral cs Low

Value Curve of Formule 1 in the French Low Budget Hotel Industry using“Value Curves” to plot relative strategic positioning High F 1 2 Star Relative Level 1 Star Key elements of product, service, and delivery ice Pr ce en Sil e ien Hy g B Qu ed ali ty 2 Re 4 -H ce ou pt ion r ist Fu Roo Am rnit m en ure/ iti es e siz m Ro o Lo Ap ung pe e al E Fa atin cil g itie s Ar c Ae hitec sth tu eti ral cs Low

Results of Formula 1’s Strategy From Formula 1’s perspective: Cost per room Cost of staff Profit Margins Occupancy rates 100, 000 FF 270, 000 FF 20 -23% of sales vs. 23 -25% > 2 x industry average > 3 x industry average From customers’ perspective: Hygiene Bed quality Silence Price > average 2* hotel 100 FF 200 FF of industry

Results of Formula 1’s Strategy From Formula 1’s perspective: Cost per room Cost of staff Profit Margins Occupancy rates 100, 000 FF 270, 000 FF 20 -23% of sales vs. 23 -25% > 2 x industry average > 3 x industry average From customers’ perspective: Hygiene Bed quality Silence Price > average 2* hotel 100 FF 200 FF of industry