e8461f2fda321e19df96eab415176731.ppt

- Количество слайдов: 27

Economics Honors UNIT II Microeconomics: Demand, Supply, Price Chapters 4, 5, & 6

Economics Honors UNIT II Microeconomics: Demand, Supply, Price Chapters 4, 5, & 6

PART 1 Chapter 4: Demand

PART 1 Chapter 4: Demand

What is DEMAND? What Is the Law of Demand? • The law of demand states that consumers buy more of a good when its price decreases and less when its price increases. The Substitution Effect and Income Effect • The substitution effect occurs when consumers react to an increase in a good’s price by consuming less of that good and more of other goods. • The income effect happens when a person changes his or her consumption of goods and services as a result of a change in real income.

What is DEMAND? What Is the Law of Demand? • The law of demand states that consumers buy more of a good when its price decreases and less when its price increases. The Substitution Effect and Income Effect • The substitution effect occurs when consumers react to an increase in a good’s price by consuming less of that good and more of other goods. • The income effect happens when a person changes his or her consumption of goods and services as a result of a change in real income.

• A demand") The Demand Curve Market Demand Curve Price per slice (in dollars) • A demand curve is a graphical representation of a demand schedule. • When reading a demand curve, assume all outside factors, such as income, are held constant. 3. 00 2. 50 2. 00 1. 50 1. 00. 50 0 0 50 100 150 200 250 300 350 Slices of pizza per day

The Demand Curve Market Demand Curve Price per slice (in dollars) • A demand curve is a graphical representation of a demand schedule. • When reading a demand curve, assume all outside factors, such as income, are held constant. 3. 00 2. 50 2. 00 1. 50 1. 00. 50 0 0 50 100 150 200 250 300 350 Slices of pizza per day

Shifts in Demand occur for reasons other than PRICE!

Shifts in Demand occur for reasons other than PRICE!

Prices of Related Goods • Complements are two goods that are bought and used together. Example: skis and ski boots • Substitutes are goods used in place of one another. Example: skis and snowboards

Prices of Related Goods • Complements are two goods that are bought and used together. Example: skis and ski boots • Substitutes are goods used in place of one another. Example: skis and snowboards

• Positive shifts in") Illustrating a Shift in Demand Price per slice (in dollars) • Positive shifts in demand are to the right • Negative shifts in demand are to the left. Market Demand Curve 3. 00 2. 50 2. 00 1. 50 1. 00. 50 0 0 50 100 150 200 250 300 350 Slices of pizza per day

Illustrating a Shift in Demand Price per slice (in dollars) • Positive shifts in demand are to the right • Negative shifts in demand are to the left. Market Demand Curve 3. 00 2. 50 2. 00 1. 50 1. 00. 50 0 0 50 100 150 200 250 300 350 Slices of pizza per day

Name a product you really, need:

Name a product you really, need:

What Is Elasticity of Demand? Elasticity of demand is a measure of how consumers react to a change in price. • Demand for a good that is very sensitive to changes in price is elastic. • Demand for a good that consumers will continue to buy despite a price increase is inelastic.

What Is Elasticity of Demand? Elasticity of demand is a measure of how consumers react to a change in price. • Demand for a good that is very sensitive to changes in price is elastic. • Demand for a good that consumers will continue to buy despite a price increase is inelastic.

Calculating Elasticity of Demand Elasticity is determined using the following formula: Elasticity = Percentage change in quantity demanded Percentage change in price To find the percentage change in quantity demanded or price, use the following formula: subtract the new number from the original number, and divide the result by the original number. Ignore any negative signs, and multiply by 100 to convert this number to a percentage: Percentage change = Original number – New number Original number x 100

Calculating Elasticity of Demand Elasticity is determined using the following formula: Elasticity = Percentage change in quantity demanded Percentage change in price To find the percentage change in quantity demanded or price, use the following formula: subtract the new number from the original number, and divide the result by the original number. Ignore any negative signs, and multiply by 100 to convert this number to a percentage: Percentage change = Original number – New number Original number x 100

Graphing Elasticity

Graphing Elasticity

Factors Affecting Elasticity

Factors Affecting Elasticity

WHY IS DEMAND IMPORTANT? ? ? ? ? ?

WHY IS DEMAND IMPORTANT? ? ? ? ? ?

UNIT 2: Chapter 5 SUPPLY

UNIT 2: Chapter 5 SUPPLY

To understand supply you must think like a _____________

To understand supply you must think like a _____________

Supply 1. Definition: 2. Law of Supply: 3. Profit:

Supply 1. Definition: 2. Law of Supply: 3. Profit:

The Supply Curve different prices. • Graphical representation of the law of supply Market Supply Curve 3. 00 2. 50 Price (in dollars) • A market supply curve is a graph of the quantity supplied of a good by all suppliers at 2. 00 1. 50 1. 00. 50 0 0 500 1000 1500 2000 2500 3000 3500 Output (slices per day)

The Supply Curve different prices. • Graphical representation of the law of supply Market Supply Curve 3. 00 2. 50 Price (in dollars) • A market supply curve is a graph of the quantity supplied of a good by all suppliers at 2. 00 1. 50 1. 00. 50 0 0 500 1000 1500 2000 2500 3000 3500 Output (slices per day)

Elasticity of Supply Elasticity of supply is a measure of the way quantity supplied reacts to a change in price. • An elastic supply is very sensitive to changes in price. • If supply is not very responsive to changes in price, it is considered inelastic.

Elasticity of Supply Elasticity of supply is a measure of the way quantity supplied reacts to a change in price. • An elastic supply is very sensitive to changes in price. • If supply is not very responsive to changes in price, it is considered inelastic.

would not make") ? ? ? What is the only reasons you (as a producer)would not make more of a product if you knew the price was going up? ? ? • TIME • COST

? ? ? What is the only reasons you (as a producer)would not make more of a product if you knew the price was going up? ? ? • TIME • COST

TIME The Short RUN The Long RUN • In the short run, a firm cannot easily change its output level, so supply is inelastic. • In the long run, firms are more flexible, so supply can become more elastic.

TIME The Short RUN The Long RUN • In the short run, a firm cannot easily change its output level, so supply is inelastic. • In the long run, firms are more flexible, so supply can become more elastic.

COSTS! !!!! AH!!

COSTS! !!!! AH!!

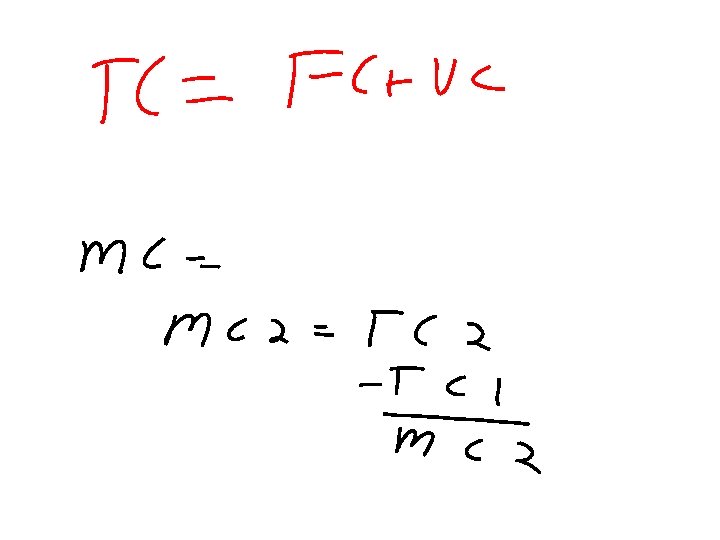

The Costs of Production • A fixed cost is a cost that does not change, regardless of how much of a good is produced. Examples: rent and salaries • Variable costs are costs that rise or fall depending on how much is produced. Examples: costs of raw materials, some labor costs. • The total cost equals fixed costs plus variable costs. • The marginal cost is the cost of producing one more unit of a good.

The Costs of Production • A fixed cost is a cost that does not change, regardless of how much of a good is produced. Examples: rent and salaries • Variable costs are costs that rise or fall depending on how much is produced. Examples: costs of raw materials, some labor costs. • The total cost equals fixed costs plus variable costs. • The marginal cost is the cost of producing one more unit of a good.

COST QUESTIONS 1. Using 5. 6 and 5. 7: How many workers should you hire in your beanbag factory. 2. Using figure 5. 9: How many bean bags per hour should you make? Why? 3. All of #7 on page 114 4. #15 on page 123

COST QUESTIONS 1. Using 5. 6 and 5. 7: How many workers should you hire in your beanbag factory. 2. Using figure 5. 9: How many bean bags per hour should you make? Why? 3. All of #7 on page 114 4. #15 on page 123

Hey Kyle Cunningham! What would happen to your supply curve if the costs for your CAR WASH business suddenly decreased? ? ? ?

Hey Kyle Cunningham! What would happen to your supply curve if the costs for your CAR WASH business suddenly decreased? ? ? ?

Shifts in Supply 1. REASONS: Market Supply Curve a. rising/decreasing 3. 00 2. 50 Price (in dollars) costsb. technologyc. government- taxes, subsidies, regulation, deregulation d. future pricese. number of suppliers - 2. 00 1. 50 1. 00. 50 0 0 500 150 200 250 0 0 Output (slices 0 day) per 0 300 350 0 0

Shifts in Supply 1. REASONS: Market Supply Curve a. rising/decreasing 3. 00 2. 50 Price (in dollars) costsb. technologyc. government- taxes, subsidies, regulation, deregulation d. future pricese. number of suppliers - 2. 00 1. 50 1. 00. 50 0 0 500 150 200 250 0 0 Output (slices 0 day) per 0 300 350 0 0

What is the importance of understanding SUPPLY? ? ?

What is the importance of understanding SUPPLY? ? ?