072688e02dc0274e37f239376f902641.ppt

- Количество слайдов: 58

Discounted Cash Flow Analysis (Time Value of Money(

Discounted Cash Flow Analysis (Time Value of Money(

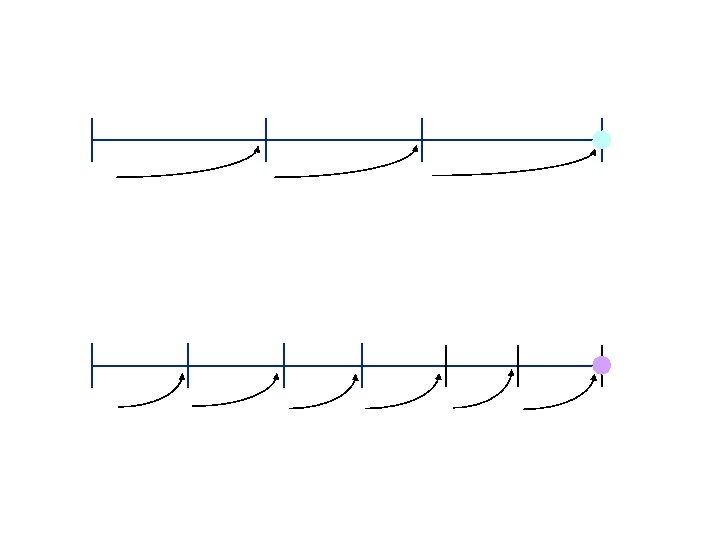

Time lines show timing of cash flows. 0 i% 1 2 3 Tick marks at ends of periods, so Time 0 is today; Time 1 is the end of Period 1, or the beginning of Period 2; and so on.

Time lines show timing of cash flows. 0 i% 1 2 3 Tick marks at ends of periods, so Time 0 is today; Time 1 is the end of Period 1, or the beginning of Period 2; and so on.

Time line for a $100 lump sum due at the end of Year 2. 0 1 2 Years i% 100

Time line for a $100 lump sum due at the end of Year 2. 0 1 2 Years i% 100

Time line for an ordinary annuity of $100 for 3 years. 0 i% 1 2 3 100 100

Time line for an ordinary annuity of $100 for 3 years. 0 i% 1 2 3 100 100

Time line for uneven CFs -$50 at t = 0 and $100, $75, and $50 at the end of Years 1 through 3. 0 50 - i% 1 2 3 100 75 50

Time line for uneven CFs -$50 at t = 0 and $100, $75, and $50 at the end of Years 1 through 3. 0 50 - i% 1 2 3 100 75 50

What’s the FV of an initial $100 after 3 years if i = 10%? 0 10% 1 2 3 FV? = Finding FVs is compounding.

What’s the FV of an initial $100 after 3 years if i = 10%? 0 10% 1 2 3 FV? = Finding FVs is compounding.

After 1 year After 2 years

After 1 year After 2 years

After 3 years In general,

After 3 years In general,

What’s the PV of $100 due in 3 years if i = 10%? Finding PVs is discounting, and it’s the reverse of compounding. 0 PV? = 10% 1 2 3 100

What’s the PV of $100 due in 3 years if i = 10%? Finding PVs is discounting, and it’s the reverse of compounding. 0 PV? = 10% 1 2 3 100

1 + 1 i 1 1. 10

1 + 1 i 1 1. 10

If sales grow at 20% per year, how long before sales double? Solve for n:

If sales grow at 20% per year, how long before sales double? Solve for n:

Graphical Illustration:

Graphical Illustration:

ordinary annuity and annuity due

ordinary annuity and annuity due

What’s the difference between an ordinary annuity and an annuity due?

What’s the difference between an ordinary annuity and an annuity due?

What’s the FV of a 3 -year ordinary annuity of $100 at 10%? 0 10% 1 2 3 100 100 110 121 FV = 331

What’s the FV of a 3 -year ordinary annuity of $100 at 10%? 0 10% 1 2 3 100 100 110 121 FV = 331

What’s the PV of this ordinary annuity? 0 90. 91 82. 64 75. 13 = 248. 69 PV 2 3 100 10% 1 100

What’s the PV of this ordinary annuity? 0 90. 91 82. 64 75. 13 = 248. 69 PV 2 3 100 10% 1 100

Ordinary Annuity and Annuity Due Ordinary Annuity Due

Ordinary Annuity and Annuity Due Ordinary Annuity Due

Find the FV and PV if the annuity were an annuity due. 0 10% 1 2 100 3

Find the FV and PV if the annuity were an annuity due. 0 10% 1 2 100 3

What is the PV of this uneven cash flow stream? 0 2 3 4 100 10% 1 300 50 - 90. 91 247. 93 225. 39 34. 15= 530. 08 PV

What is the PV of this uneven cash flow stream? 0 2 3 4 100 10% 1 300 50 - 90. 91 247. 93 225. 39 34. 15= 530. 08 PV

What interest rate would cause $100 to grow to $125. 97 in 3 years?

What interest rate would cause $100 to grow to $125. 97 in 3 years?

Will the FV of a lump sum be larger or smaller if we compound more often, holding the stated i% constant? Why? LARGER! If compounding is more frequent than once a year--for example, semiannually, quarterly, or daily--interest is earned on interest more often.

Will the FV of a lump sum be larger or smaller if we compound more often, holding the stated i% constant? Why? LARGER! If compounding is more frequent than once a year--for example, semiannually, quarterly, or daily--interest is earned on interest more often.

How do we find EFF% for a nominal rate of 10%, compounded semiannually?

How do we find EFF% for a nominal rate of 10%, compounded semiannually?

EAR = EFF% of 10%

EAR = EFF% of 10%

Can the effective rate ever be equal to the nominal rate?

Can the effective rate ever be equal to the nominal rate?

When is each rate used? Written into contracts, quoted by banks and brokers. Not used in calculations or shown on time lines unless compounding is annual.

When is each rate used? Written into contracts, quoted by banks and brokers. Not used in calculations or shown on time lines unless compounding is annual.

Used in calculations, shown on time lines.

Used in calculations, shown on time lines.

EAR = EFF: % Used to compare returns on investments with different compounding patterns. Also used for calculations if dealing with annuities where payments don’t match interest compounding periods.

EAR = EFF: % Used to compare returns on investments with different compounding patterns. Also used for calculations if dealing with annuities where payments don’t match interest compounding periods.

FV of $100 after 3 years under 10% semiannual compounding? Quarterly? FV = PV. + FV i m 0. 10 = 100$ 1 + 2 1

FV of $100 after 3 years under 10% semiannual compounding? Quarterly? FV = PV. + FV i m 0. 10 = 100$ 1 + 2 1

What’s the value at the end of Year 3 of the following CF stream if the quoted interest rate is 10%, compounded semi -annually? 0 5% 1 2 100 3 4 100 5 100

What’s the value at the end of Year 3 of the following CF stream if the quoted interest rate is 10%, compounded semi -annually? 0 5% 1 2 100 3 4 100 5 100

Compound Each CF 0 5% 1 2 100 3 4 100 5 6 100. 00 110. 25 121. 55 331. 80

Compound Each CF 0 5% 1 2 100 3 4 100 5 6 100. 00 110. 25 121. 55 331. 80

b. The cash flow stream is an annual annuity whose EFF% = 10. 25%.

b. The cash flow stream is an annual annuity whose EFF% = 10. 25%.

What’s the PV of this stream? 0 90. 70 82. 27 74. 62 247. 59 2 3 100 5% 1 100

What’s the PV of this stream? 0 90. 70 82. 27 74. 62 247. 59 2 3 100 5% 1 100

Amortization Construct an amortization schedule for a $1, 000, 10% annual rate loan with 3 equal payments.

Amortization Construct an amortization schedule for a $1, 000, 10% annual rate loan with 3 equal payments.

Step 1: Find the required payments. 0 1000 - 10% 1 2 3 PMT PMT

Step 1: Find the required payments. 0 1000 - 10% 1 2 3 PMT PMT

Step 1: Find the required payments. 1000/2. 4869= 402. 107 =

Step 1: Find the required payments. 1000/2. 4869= 402. 107 =

Step 2: Find interest charge for Year 1. Step 3: Find repayment of principal in Year 1. Repmt = PMT - INT 100 - 402. 11 =. 302. 11$ =

Step 2: Find interest charge for Year 1. Step 3: Find repayment of principal in Year 1. Repmt = PMT - INT 100 - 402. 11 =. 302. 11$ =

Step 4: Find ending balance after Year 1. End bal = Beg bal - Repmt. 697. 89$ = 302. 11 - 1, 000 = Repeat these steps for Years 2 and 3 to complete the amortization table.

Step 4: Find ending balance after Year 1. End bal = Beg bal - Repmt. 697. 89$ = 302. 11 - 1, 000 = Repeat these steps for Years 2 and 3 to complete the amortization table.

Interest declines. Tax implications.

Interest declines. Tax implications.

On January 1 you deposit $100 in an account that pays a nominal interest rate of 10%, with daily compounding (365 days. ( How much will you have on October 1, or after 9 months (273 days)? (Days given(.

On January 1 you deposit $100 in an account that pays a nominal interest rate of 10%, with daily compounding (365 days. ( How much will you have on October 1, or after 9 months (273 days)? (Days given(.

FV = 100$ =. 107. 77$

FV = 100$ =. 107. 77$

You are offered a note which pays $1, 000 in 15 months (or 456 days) for $850. You have $850 in a bank which pays a 7. 0% nominal rate, with 365 daily compounding, which is a daily rate of 0. 019178% and an EAR of 7. 25%. You plan to leave the money in the bank if you don’t buy the note. The note is riskless. Should you buy it?

You are offered a note which pays $1, 000 in 15 months (or 456 days) for $850. You have $850 in a bank which pays a 7. 0% nominal rate, with 365 daily compounding, which is a daily rate of 0. 019178% and an EAR of 7. 25%. You plan to leave the money in the bank if you don’t buy the note. The note is riskless. Should you buy it?

2 Ways to Solve: . 1 Greatest future wealth: FV. 2 Greatest wealth today: PV

2 Ways to Solve: . 1 Greatest future wealth: FV. 2 Greatest wealth today: PV

. 1 Greatest Future Wealth Find FV of $850 left in bank for 15 months and compare with note’s FV = $1000. Buy the note: $1000 > $927. 67.

. 1 Greatest Future Wealth Find FV of $850 left in bank for 15 months and compare with note’s FV = $1000. Buy the note: $1000 > $927. 67.

. 2 Greatest Present Wealth Find PV of note, and compare with its $850 cost:

. 2 Greatest Present Wealth Find PV of note, and compare with its $850 cost: