2e71b1c67b746cd8c776ab4727039b41.ppt

- Количество слайдов: 42

CPE Program on "Independence of Auditors" by CA. Ramachandran Mahadevan

MAHATMA GANDHI • • • Seven Social Sins in Today’s World Wealth without work Pleasure without conscience Knowledge without character Commerce without morality Science without humanity Religion without sacrifice Politics without principle

AUDITOR • The Chartered Accountant is a person on whom every section of society could rely upon, and rely strongly. His certificate would be one by way of a seal and a hallmark which would at once inspire confidence in the minds of all concerned as certification by a person fully competent and holding a charter from the supreme legislature of the country for the purpose… He must be above reproach; he must reflect the highest ethics of the

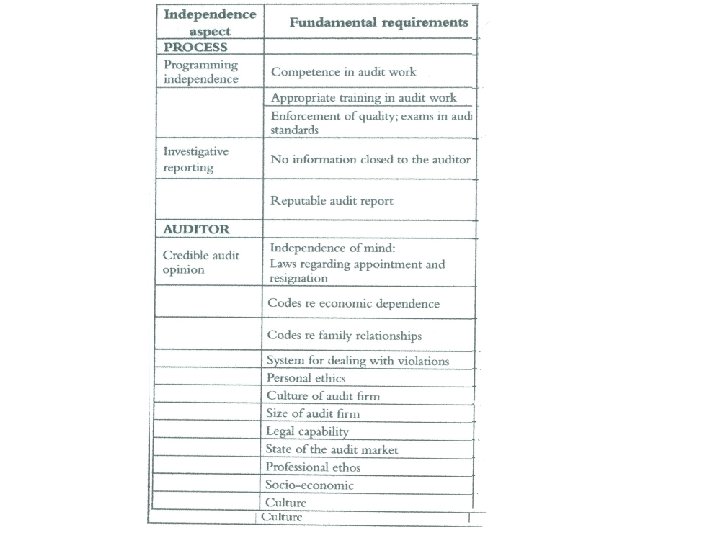

INDEPENDENCE • Independence of Mind – The state of mind that permits the expression of a conclusion without being affected by influences that compromise professional judgment, thereby allowing an individual to act with integrity and exercise objectivity and professional skepticism. • Independence in Appearance – The avoidance of facts and circumstances that are

INDEPENDENCE-CONTD • Independence Should be Exhibited in • Objectivity • Integrity • Professional Services

PUBLIC INTEREST • • • Public Consists of Clients Credit /LOAN GIVERS Government Employers

JUDGMENT • Judgment is the process • of reaching a decision or drawing a conclusion when there a number of possible alternative solutions.

EFFECTIVE JUDGMENT • An effective • judgment process will be logical, flexible, unbiased, • objective, and consistent. • It will utilize an appropriate • amount of relevant information, and it will properly • balance experience, knowledge, intuition, and

JUDGMENT TRAPS • One of the most common judgment traps that individuals and • groups fall into is the tendency to want to immediately solve • a problem, to appear decisive by making a quick judgment. • In a group setting, this rush to solve is often manifested • as a tendency to strive toward quick compromise and

JUDGMENT BIAS • Overconfidence is the tendency for decision makers to • overestimate their own abilities to perform tasks or to • make accurate assessments of risks or other judgments • and decisions. • Confirmation which is the tendency for

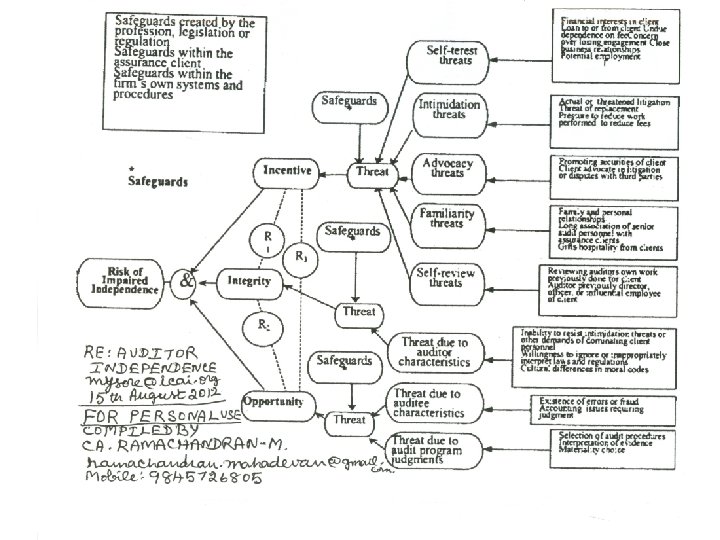

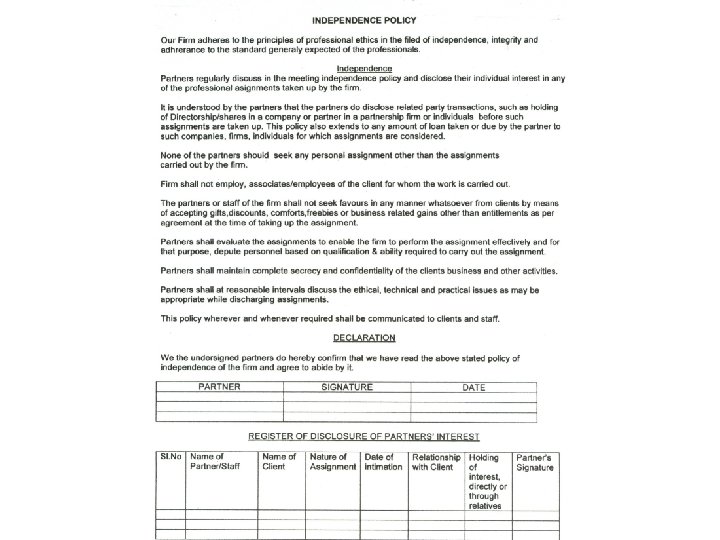

ICAI • CODE OF CONDUCT • GUIDANCE NOTE ON INDEPENDENCE • The conceptual framework approach shall be applied by professional accountants to: • Identify threats to independence; • Evaluate the significance of the threats identified; and • Apply safeguards, when necessary, to eliminate

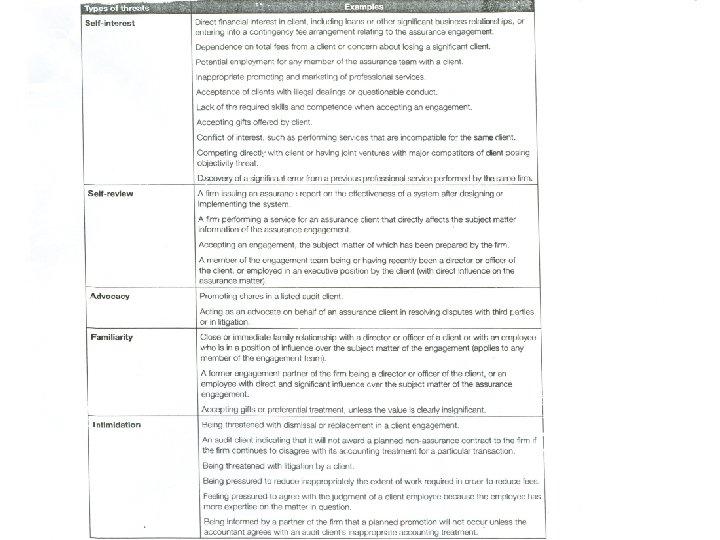

THREATS • Threats may be created by a broad range of relationships and circumstances. When a relationship or circumstance creates a threat, such a threat could compromise, or could be perceived to compromise, a professional accountant’s compliance with the fundamental principles. A circumstance or relationship may create more than one threat, and a threat may affect compliance with more than one fundamental principle.

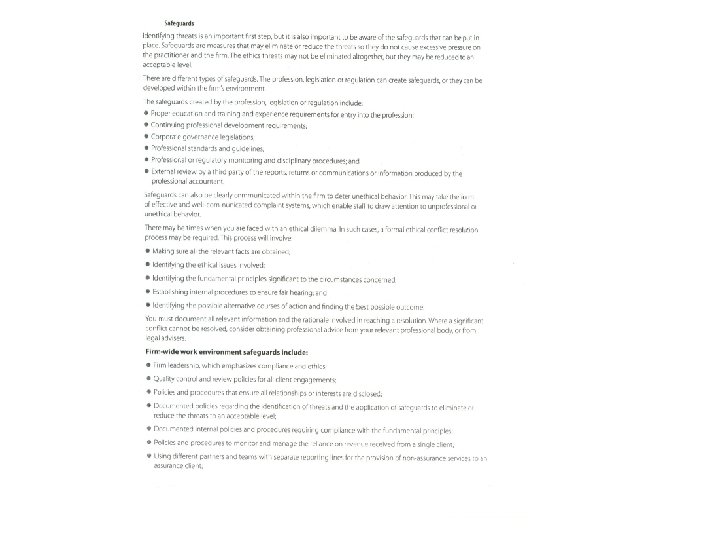

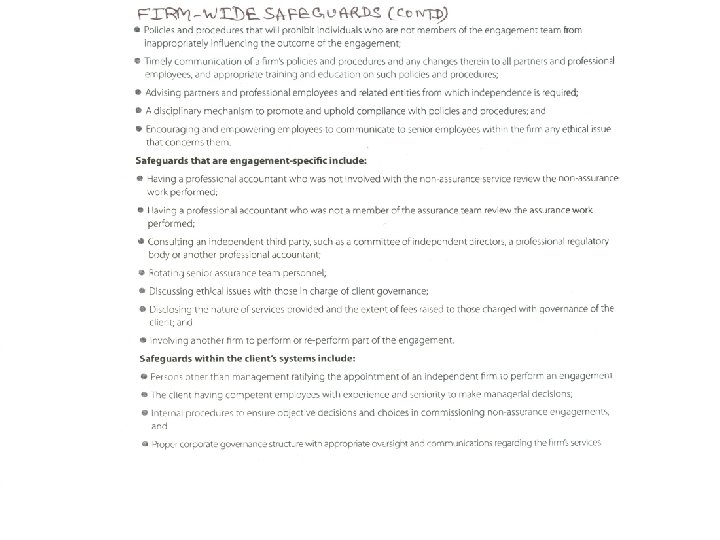

SAFEGUARDS • SAFEGUARDS ARE ACTIONS/MEASURES • TO ELIMINATE/REDUCE THREATS • TO AN ACCEPTABLE LEVEL • There are some situations where threat created is so significant no safeguards could eliminate threat or reduce it to an acceptable level. In such situations the circumstances or relationship creating the threat must be avoided.

SAFEGUARDS ICAI • Education, Training & Experience • Continuing Education Requirements • Professional Standards & Disciplinary Processes. • External Review of Firms Quality Control System. • CA ACT REGULATION NOTIFICATION

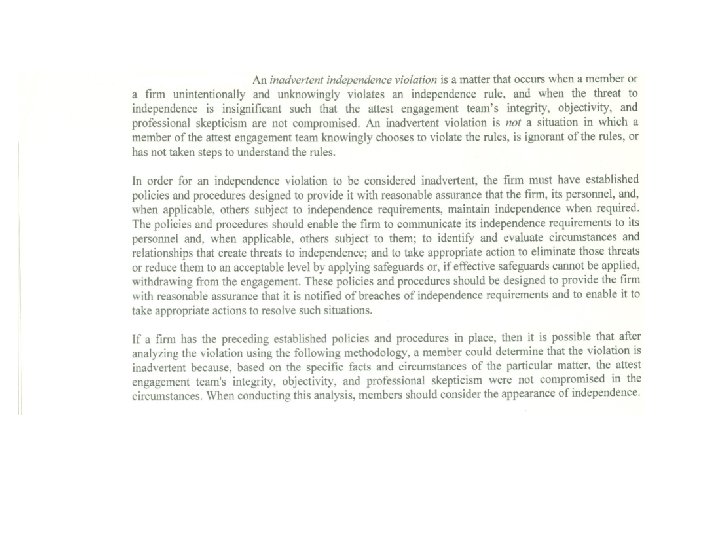

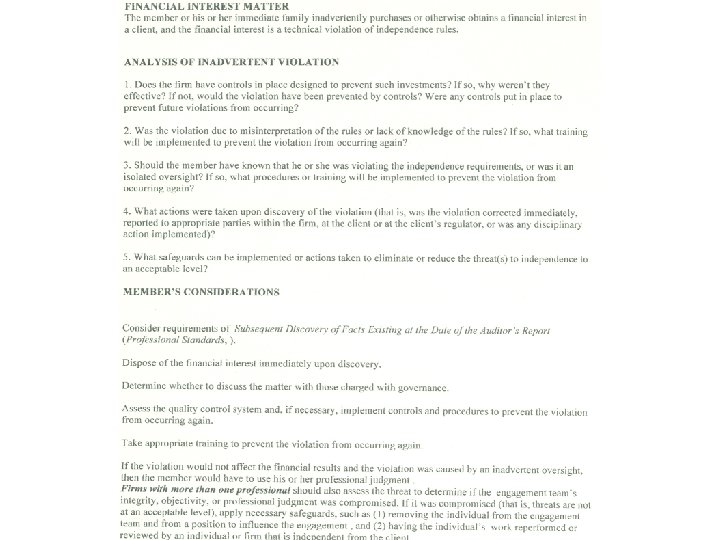

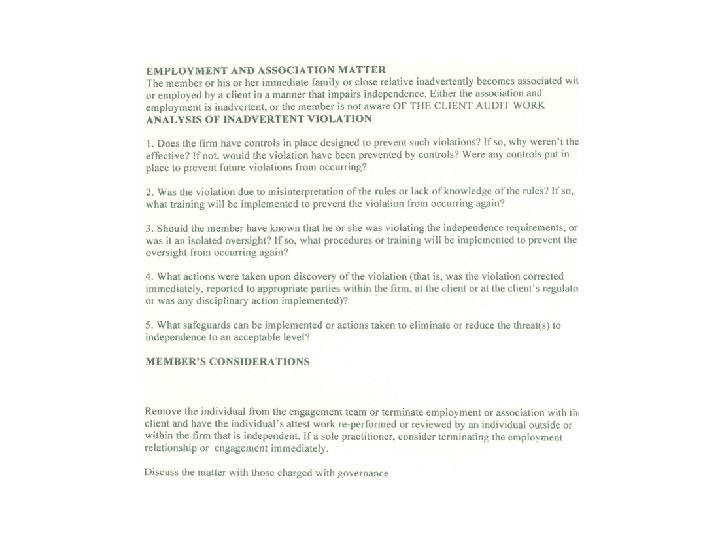

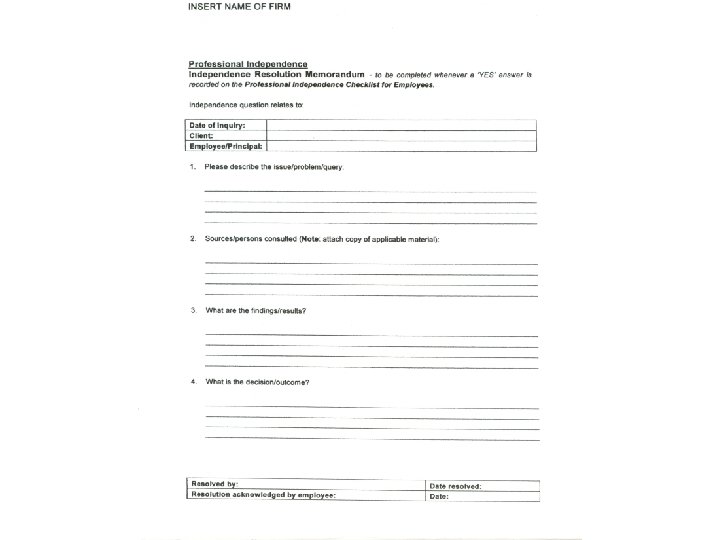

DOCUMENTATION • • The professional accountant shall document conclusions regarding compliance with independence requirements and the substance of relevant discussions supporting conclusions: – When safeguards are required, the nature of the threat and safeguards in place or applied to reduce threat to an acceptable level shall be

AUDITOR THREATS • Merriam. Webster's Dictionary defines integrity as firm adherence to a code of especially moral or artistic values; • incorruptibility. " That definition says a lot about integrity as a foundational value; but the Code describes integrity • specifically in terms of the member's responsibility. Integrity requires a member to be honest and candid, yet • respect the constraints of client confidentiality.

AUDITEE THREATS • • ERRORS FRAUDS ESTIMATE COMPLEXITY JUDGMENT

AUDITEE SAFEGUARDS • Safeguards within the Assurance Client • Competent Employees to make Managerial Decisions. • Policies and Procedures for fair Financial Reporting. • Internal Procedures • Corporate Governance Structure • •

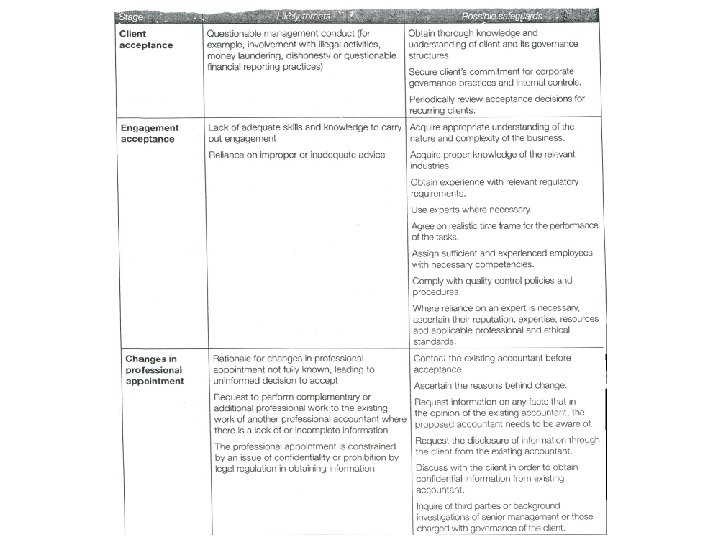

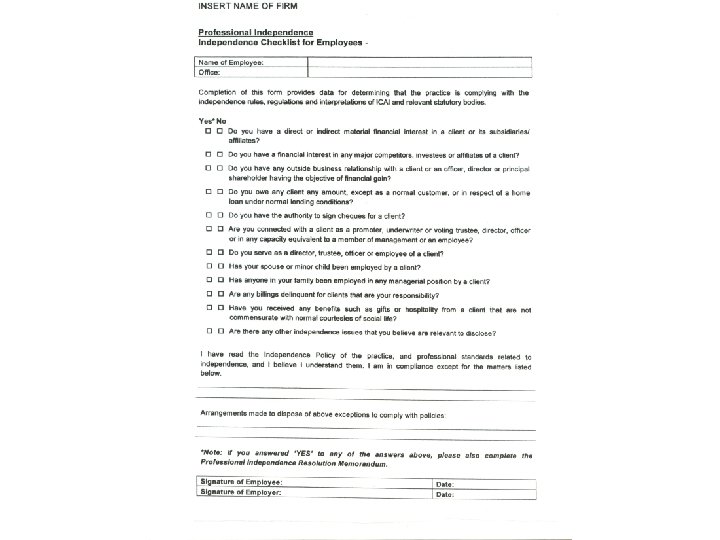

AUDITEE EVALUATION • When evaluating the client, the following factors to consider: • Identity and business reputation of the client's principal owners, key management, and those charged with • its governance. • Nature of operations and specific business practices of the client. • Attitude of the client's owners, key management, those charged with governance

![AUDITEE EVALUATION FORMAT • On [Insert date. ], I (we) [Names of Partners in](https://present5.com/presentation/2e71b1c67b746cd8c776ab4727039b41/image-21.jpg "AUDITEE EVALUATION FORMAT • On [Insert date. ], I (we) [Names of Partners in")

AUDITEE EVALUATION FORMAT • On [Insert date. ], I (we) [Names of Partners in Attendance] considered the acceptability of continuing to • provide all or certain professional services to each client on the firm's client list • . Among the factors • considered in evaluating each client were: • Timely payment of fees.

AUDIT PROGRAM THREATS • • SELECTION OF AUDIT PROCEDURES INTERPRETATION OF EVIDENCE MATERIALITY CHOICE ISSUES REQUIRING JUDGMENTS

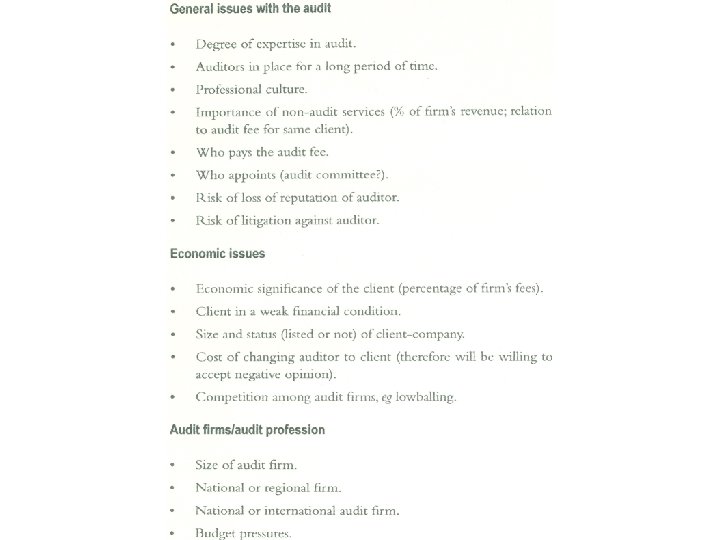

INDEPENDENCE RISK • • • What incentives create independence risk? Direct incentives Direct investments Indirect Incentives Interpersonal relationships Auditing work of self or firm Potential employment Financial dependence

PRACTICE AREA RISK • Maintaining independence in fact and • appearance can be challenging, especially in cases where the client relationship is cozy and the client has the • highest integrity, operates in an ideal industry, and the engagement fits perfectly within the firm profile. • Additionally, • the discovery of any potential conflicts of interest should cause the firm to seriously

BIG FOUR INDEPENDENCE • KPMG audits Citigroup, Wells Fargo – who now owns client Wachovia – GE, and GM. They used to audit two big mortgage originators before they blew up – Countrywide and New Century. They also used to audit Fannie Mae and Moody’s before they were fired and sued. They also audit the US Treasury. • Pricewaterhouse. Coopers audits JP Morgan Chase, Bank of America, Goldman Sachs, AIG,

AUDITOR SAFEGUARDS • Safeguards within the Firms own Systems & Procedures • Firm Leadership • Policies & Procedures for Quality Control • Documented Independence regarding Identification of threats and Application of Safeguards. • Disciplinary Mechanism

PROFESSIONAL MASTERY • Acting as a role model within the accounting profession by behaving in accordance with required professional values, ethics and attitude; • • Providing thought leadership in areas requiring experience and expertise; and • • Communicating with impact

’s audit firm, Price Waterhouse, was in the auditor for S")

Pricewaterhouse. Coopers (Pw. C)’s audit firm, Price Waterhouse, was in the auditor for S have been auditing their accounts since 2000 -01. The fraudulent role played by the Pricewaterhouse. Coopers (Pw. C) in the failure of Satyam matches the role played by Art Anderson in the collapse of Enron. S Goplakrishnan and S Talluri, partners of Pw. C acco SFIO findings, had admitted they did not come across any case or instance of fraud by t However, Ramalinga Raju admission of having fudged the accounts for several years pu these statutory auditors on the dock. The SFIO report stated that the statutory auditor using an independent testing mechanism used Satyam’s investigative tools and thereb compromised on reporting standards. The last straw of deficiencies in statutory standa despite having observed control deficiencies in the Information Systems and the risk o frauds, Pw. C chose to keep silent and did not report the matter to the shareholders. In before the SFIO, VSP Gupta, Global Head Internal audit had said that even though the c and resources of internal audit was not commensurate with the size of the business, P this fact and certified the company. Pw. C did not check even one per cent of the invoice they pay enough attention to verification of sundry debtors, which according to Ramal confession was overstated by 23 per cent (SFIO report says it was overstated by almos cent). 57 The Statutory auditors also failed in discharging their duty when it came to ind verifying cash and bank balances, both current account and fixed deposits. Ideally, if th claims it has cash on its hand, that should be enough signal for auditors to check wheth in hand is available or not; whether bank balance has been invested properly of not; w

In India, the auditor has to take care to protect independence. The corporate sector is dominated by family businesses. The accountant and the auditor is treated as the ‘friend, philosopher and guide’ to the promoter-manager of the company. Auditor is an economic man and also has emotions. Therefore, it is natural that auditor has temptation to protect income by strengthening the relationship with the head of the family. It is also difficult to avoid emotional bonding with the family developed over long years. Therefore, the onus of avoiding impairment of independence lies on each and every auditor.

FRAUD It is the primary responsibility of the management and those charged with governance to prevent and detect frauds. The auditor is only concerned with frauds that cause a material misstatement in the financial statements. Misstatements may arise from fraudulent financial reporting and/or misappropriation of assets. Fraudulent activities may take place within a CLIENT ENTITY by, or with the knowing involvement of, management or personnel. Alternatively, fraud may be perpetrated on a CLIENT without the knowledge complicity of the EMPLOYYES OF THE CLIENT.

2e71b1c67b746cd8c776ab4727039b41.ppt