bdb83e3e75dc427692fd0c1b1f765b73.ppt

- Количество слайдов: 57

CIFPs Annual National Conference Niagara Falls, Ontario David Wm. Brown CLU, Ch. FC, CFP, RHU Tuesday June 21 nd 2005

CIFPs Annual National Conference Niagara Falls, Ontario David Wm. Brown CLU, Ch. FC, CFP, RHU Tuesday June 21 nd 2005

AGENDA 1. Introduction 1. 2. The Case for Income Replacement/Critical Illness insurance 1. 2. 3. Income Replacement Insurance Critical Illness Insurance The Comparison 1. 5. Personal demonstration Statistics Definitions 1. 2. 4. Disclosure, qualifications, guarantees Income Replacement/Critical Illness Insurance in Canada 1. 2. Current status Challenges

AGENDA 1. Introduction 1. 2. The Case for Income Replacement/Critical Illness insurance 1. 2. 3. Income Replacement Insurance Critical Illness Insurance The Comparison 1. 5. Personal demonstration Statistics Definitions 1. 2. 4. Disclosure, qualifications, guarantees Income Replacement/Critical Illness Insurance in Canada 1. 2. Current status Challenges

AGENDA- Cont’d 6. Critical Illness Taxation Issues 1. 2. 7. 8. Structuring the C. I. Policy Prospecting 1. 2. 3. 9. C. R. A C. A. L. U Your doctors Your clients – individual/group Yourself Questions?

AGENDA- Cont’d 6. Critical Illness Taxation Issues 1. 2. 7. 8. Structuring the C. I. Policy Prospecting 1. 2. 3. 9. C. R. A C. A. L. U Your doctors Your clients – individual/group Yourself Questions?

SURVEY

SURVEY

STROKE

STROKE

HEART DISEASE

HEART DISEASE

HEART ATTACK

HEART ATTACK

CANCER

CANCER

Disabled as a result of an Accident or of a Sickness ?

Disabled as a result of an Accident or of a Sickness ?

CANCER 38% of Women 41% of Men Will Develop Cancer In their Lifetime.

CANCER 38% of Women 41% of Men Will Develop Cancer In their Lifetime.

Cancer n 1 in 3 Canadians will contract some form of lifethreatening cancer n 125, 000 newly diagnosed cases per year Heart Attack n 1 in 4 Canadians will contract heart disease n 75, 000 suffer heart attacks each year - 1 in 2 < 65 Stroke n 1 in 20 Canadians run the risk of stroke before the age of 65 n 50, 000 suffer a stroke each year - 1 in 3< 65 Accounts for almost 1% of the total Canadian population

Cancer n 1 in 3 Canadians will contract some form of lifethreatening cancer n 125, 000 newly diagnosed cases per year Heart Attack n 1 in 4 Canadians will contract heart disease n 75, 000 suffer heart attacks each year - 1 in 2 < 65 Stroke n 1 in 20 Canadians run the risk of stroke before the age of 65 n 50, 000 suffer a stroke each year - 1 in 3< 65 Accounts for almost 1% of the total Canadian population

Income Replacement Insurance Income Replacement or Disability Income Insurance is designed to replace a portion of an individuals income; in the event that the individual as a result of an accident or sickness cannot work in his/her/any/own occupation

Income Replacement Insurance Income Replacement or Disability Income Insurance is designed to replace a portion of an individuals income; in the event that the individual as a result of an accident or sickness cannot work in his/her/any/own occupation

Disability Insurance Variables 1. 2. 3. 4. 5. 6. Elimination period Monthly Indemnity Benefit period Definition of total disability Definitions of partial/residual disability Options; F. I. O; C. O. L. A

Disability Insurance Variables 1. 2. 3. 4. 5. 6. Elimination period Monthly Indemnity Benefit period Definition of total disability Definitions of partial/residual disability Options; F. I. O; C. O. L. A

Critical Illness Insurance The Critical Illness plan provides a lump sum tax-free benefit to be paid in the event that an individual contracts a critical illness. The Critical Illness policy is designed to provide the necessary financial assistance to permit the insured and his/her family to cope with a critical illness.

Critical Illness Insurance The Critical Illness plan provides a lump sum tax-free benefit to be paid in the event that an individual contracts a critical illness. The Critical Illness policy is designed to provide the necessary financial assistance to permit the insured and his/her family to cope with a critical illness.

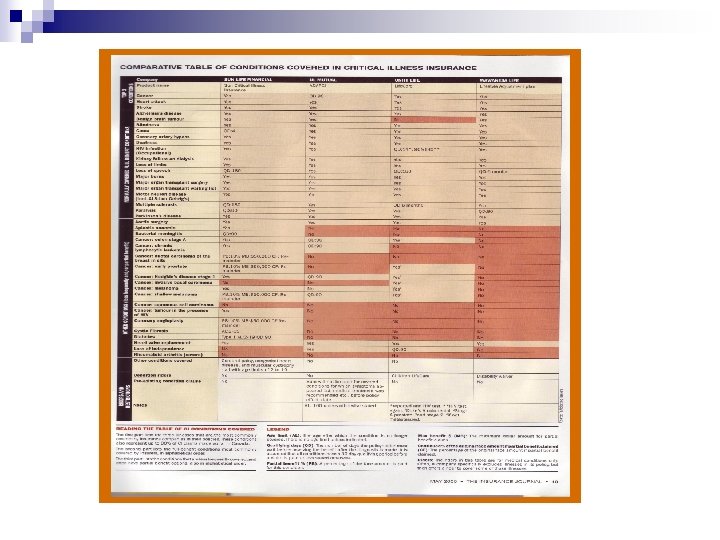

Critical Illness Insurance Covered Illnesses n n n Alzheimer’s Disease Aortic Surgery Blindness Benign Brain Tumor Cancer Coma Coronary Angioplasty Coronary Artery Bypass Surgery Cystic Fibrosis Diabetes Deafness Kidney Failure n n n n Heart Attack Heart Valve Replacement Loss of Independent Existence Loss of Limbs Loss of Speech Major Organ Transplant Motor Neuron Disease Multiple Sclerosis Occupational HIV Infection Paralysis Parkinson’s Disease Rheumatoid Arthritis Severe Burns Stroke

Critical Illness Insurance Covered Illnesses n n n Alzheimer’s Disease Aortic Surgery Blindness Benign Brain Tumor Cancer Coma Coronary Angioplasty Coronary Artery Bypass Surgery Cystic Fibrosis Diabetes Deafness Kidney Failure n n n n Heart Attack Heart Valve Replacement Loss of Independent Existence Loss of Limbs Loss of Speech Major Organ Transplant Motor Neuron Disease Multiple Sclerosis Occupational HIV Infection Paralysis Parkinson’s Disease Rheumatoid Arthritis Severe Burns Stroke

Critical Illness Insurance Plan Provisions n n n Lump Sum Non-Taxable Benefit Payout 30 Days After Diagnosis Guaranteed Renewable to Age 65 Limited Qualified Right to Change Premiums Guaranteed Issue (no medical requirements) Optional Individual Increase Offered (with medical requirements) Group - 15% Discount Return of Premium on Death Portable Coverage Pre-Existing Condition Exclusion 24 months Recharge Provision - 5 Years

Critical Illness Insurance Plan Provisions n n n Lump Sum Non-Taxable Benefit Payout 30 Days After Diagnosis Guaranteed Renewable to Age 65 Limited Qualified Right to Change Premiums Guaranteed Issue (no medical requirements) Optional Individual Increase Offered (with medical requirements) Group - 15% Discount Return of Premium on Death Portable Coverage Pre-Existing Condition Exclusion 24 months Recharge Provision - 5 Years

Extraordinary Costs of a Critical Illness $ $ Medical Costs Alternative treatment Experimental drugs Out of province treatment Nursing care Reduce Financial Obligations $ Debt/mortgage repayment $ $ Non-Medical Costs Leave of absence for insured or spouse Home and/or vehicle adaptation Childcare Work style changes

Extraordinary Costs of a Critical Illness $ $ Medical Costs Alternative treatment Experimental drugs Out of province treatment Nursing care Reduce Financial Obligations $ Debt/mortgage repayment $ $ Non-Medical Costs Leave of absence for insured or spouse Home and/or vehicle adaptation Childcare Work style changes

Critical Illness Insurance Benefits Effectively cover the most catastrophic events 4 Provide stable, predictable costs 4 Give a significant lump sum payout 4 Provide access to world renowned medical services 4 Fill the growing gap due to increased morbidity 4 Address real needs 4 Covers real risks 4

Critical Illness Insurance Benefits Effectively cover the most catastrophic events 4 Provide stable, predictable costs 4 Give a significant lump sum payout 4 Provide access to world renowned medical services 4 Fill the growing gap due to increased morbidity 4 Address real needs 4 Covers real risks 4

Critical Illness Insurance Assistance Services BEST DOCTORS/CERIDIAN/HEALING JOURNEY Inter. Consultation • Expert Medical Evaluation by World-Class Physicians Find. Best. Doc • Customized Search for Best Doctors Including Specialized Canadian Physicians Find. Best. Care • Comprehensive Services and Access to Treatment Centers Throughout the United States Ceridian/The Healing Journey • 24 Hour Access to Daily Living Assistance Professionals • Membership in a Self-Help Healing Program

Critical Illness Insurance Assistance Services BEST DOCTORS/CERIDIAN/HEALING JOURNEY Inter. Consultation • Expert Medical Evaluation by World-Class Physicians Find. Best. Doc • Customized Search for Best Doctors Including Specialized Canadian Physicians Find. Best. Care • Comprehensive Services and Access to Treatment Centers Throughout the United States Ceridian/The Healing Journey • 24 Hour Access to Daily Living Assistance Professionals • Membership in a Self-Help Healing Program

“EITHER” OR Income Replacement Insurance Critical Illnesses Insurance Triggering Event Sickness or Accident Critical Illness 27+ Diseases Definitions Inability to work n. Own occupation n. Any occupation n. Residual n. Partial Diagnoses of Critical Illness survival for 30 days(90 days in the case of Cancer following issue of contract) Premiums Guaranteed/Non Guaranteed Return Of Premium on Death Not usually applicable - 3 month survivorship benefit Usually included Return of Premium on expiry Not usually applicable (May be available as a rider) Can be included as rider

“EITHER” OR Income Replacement Insurance Critical Illnesses Insurance Triggering Event Sickness or Accident Critical Illness 27+ Diseases Definitions Inability to work n. Own occupation n. Any occupation n. Residual n. Partial Diagnoses of Critical Illness survival for 30 days(90 days in the case of Cancer following issue of contract) Premiums Guaranteed/Non Guaranteed Return Of Premium on Death Not usually applicable - 3 month survivorship benefit Usually included Return of Premium on expiry Not usually applicable (May be available as a rider) Can be included as rider

Income Replacement Insurance Critical Illnesses Insurance Other Options Future income option Cost of living benefits Early Intervention Benefits Medical Assistance Benefits Contract Terms To age 65 with possible extension Can be designated to continue for life Underwriting Based on medical history and family history Benefit Payment Paid out monthly Lump sum Adjudication Ongoing One time Maximum Payment In relation to income replacement tables $2, 000 Taxability If paid in after tax dollars benefit is tax free Considered tax free - No ruling yet - Eligibility Needs income to qualify No income requirement

Income Replacement Insurance Critical Illnesses Insurance Other Options Future income option Cost of living benefits Early Intervention Benefits Medical Assistance Benefits Contract Terms To age 65 with possible extension Can be designated to continue for life Underwriting Based on medical history and family history Benefit Payment Paid out monthly Lump sum Adjudication Ongoing One time Maximum Payment In relation to income replacement tables $2, 000 Taxability If paid in after tax dollars benefit is tax free Considered tax free - No ruling yet - Eligibility Needs income to qualify No income requirement

“Canadian Critical Illness sales are paltry by comparison to other countries in the English speaking universe” Advisor. ca May 17, 2005

“Canadian Critical Illness sales are paltry by comparison to other countries in the English speaking universe” Advisor. ca May 17, 2005

C. I. SALES STATS AND ANALYSYS 2004 n n n In 2004 sales increased by 11% More limited guarantees introduced Average size of policy dropped by 2% Permanent products increased over renewable products Return of premium at expiry benefit reduced by 6% Only 3% of new policies sold were for “Basic” coverage of five or fewer conditions Source: Limra CI Sales 2004

C. I. SALES STATS AND ANALYSYS 2004 n n n In 2004 sales increased by 11% More limited guarantees introduced Average size of policy dropped by 2% Permanent products increased over renewable products Return of premium at expiry benefit reduced by 6% Only 3% of new policies sold were for “Basic” coverage of five or fewer conditions Source: Limra CI Sales 2004

“If you don’t sell CI, have a huge financial indemnity policy because your client will sue you” Bhupinder Anand Associates London, England

“If you don’t sell CI, have a huge financial indemnity policy because your client will sue you” Bhupinder Anand Associates London, England

REASONS 1. 2. 3. 4. No standardized definitions Concern over high premiums Advisors not aggressive enough Tough underwriting concerns

REASONS 1. 2. 3. 4. No standardized definitions Concern over high premiums Advisors not aggressive enough Tough underwriting concerns

DON’T TRY TO BE A DOCTOR !

DON’T TRY TO BE A DOCTOR !

CRITICAL ILLNESS UNDERWRITING Family History n Smoking n Height-Weight Ratio n Elevated Cholesterol n Medical Impairments that affect more than one body system or organ n Seemingly Insignificant Condition n

CRITICAL ILLNESS UNDERWRITING Family History n Smoking n Height-Weight Ratio n Elevated Cholesterol n Medical Impairments that affect more than one body system or organ n Seemingly Insignificant Condition n

TAXATION “The Canadian Life and Health Insurance Association and The Conference of Advanced Life Underwriting Discussion Paper” March 2004 See Website: www. calu. com

TAXATION “The Canadian Life and Health Insurance Association and The Conference of Advanced Life Underwriting Discussion Paper” March 2004 See Website: www. calu. com

Question Accident or Sickness Insurance IS C. I. OR Life Insurance With/or Without Refund of Premium ON DEATH ON EXPIRY

Question Accident or Sickness Insurance IS C. I. OR Life Insurance With/or Without Refund of Premium ON DEATH ON EXPIRY

Critical Illness Insurance Taxation n n CRA has not yet clarified the Agency’s interpretation of the provisions of the Act with reference to the taxation of Critical Illness Contracts (especially with refund benefits) The Conference of Advanced Life Underwriters is continuing to work with the Department of Finance to ensure an appropriate framework for taxation of Living Benefits

Critical Illness Insurance Taxation n n CRA has not yet clarified the Agency’s interpretation of the provisions of the Act with reference to the taxation of Critical Illness Contracts (especially with refund benefits) The Conference of Advanced Life Underwriters is continuing to work with the Department of Finance to ensure an appropriate framework for taxation of Living Benefits

-Grouped") TAXATION Canada Revenue Agency Technical Interpretation Letter (2003 -0034505, December 9 , 2003) -Grouped C. I. Non taxable benefits and deductible premium – ~ Assumption no return or premiums

TAXATION Canada Revenue Agency Technical Interpretation Letter (2003 -0034505, December 9 , 2003) -Grouped C. I. Non taxable benefits and deductible premium – ~ Assumption no return or premiums

Understanding The Taxation Of Critical Illness Insurance Personally – Owing Policy Purpose Structure Provides cash benefit Insured owner for beneficiary and payor 1. Medical expenses 2. Pay down mortgage 3. Renovate home 4. Replace caregiver income Tax Treatment Premium non deductible living expense n Benefit non taxable n Return of premium on death and at expiry non taxable n CRA has confirmed that it views Critical Illness Insurance Policies without ROP benefits as accident and sickness Insurance.

Understanding The Taxation Of Critical Illness Insurance Personally – Owing Policy Purpose Structure Provides cash benefit Insured owner for beneficiary and payor 1. Medical expenses 2. Pay down mortgage 3. Renovate home 4. Replace caregiver income Tax Treatment Premium non deductible living expense n Benefit non taxable n Return of premium on death and at expiry non taxable n CRA has confirmed that it views Critical Illness Insurance Policies without ROP benefits as accident and sickness Insurance.

Understanding The Taxation Of Critical Illness Insurance Corporate Protection Purpose Provide cash benefit to corporation for 1. Immediate cash needs (key employee) 2. Repay business debts 3. Fund buy - sell Structure Tax Treatment Insured: n Premium non deductible to employee or corporation shareholder. n. Benefits non taxable to Owner, payor and corporation beneficiary is n Return of premium on corporation death or at expiry may be non taxable

Understanding The Taxation Of Critical Illness Insurance Corporate Protection Purpose Provide cash benefit to corporation for 1. Immediate cash needs (key employee) 2. Repay business debts 3. Fund buy - sell Structure Tax Treatment Insured: n Premium non deductible to employee or corporation shareholder. n. Benefits non taxable to Owner, payor and corporation beneficiary is n Return of premium on corporation death or at expiry may be non taxable

Understanding The Taxation Of Critical Illness Insurance Individual Policy as an Employee Benefit Purpose Structure Tax Treatment Provides cash to the employee for 1. Medical expenses 2. Pay down mortgage 3. Renovate home 4. Replace caregiver income The Employee is the insured. Owner is employee or corporation. Payor is corporation. Benefits payable to employee or corporation (Employee not as shareholder) 1. If employee owned and corporate paid. Premium included in employee’s income, deductible to employer, benefit non taxable to employee 2. If corporate owned and corporate paid. Premium not included in employees income deductible to corporation as business expense. Cash benefit not taxable to corporation if paid to employee taxable in income

Understanding The Taxation Of Critical Illness Insurance Individual Policy as an Employee Benefit Purpose Structure Tax Treatment Provides cash to the employee for 1. Medical expenses 2. Pay down mortgage 3. Renovate home 4. Replace caregiver income The Employee is the insured. Owner is employee or corporation. Payor is corporation. Benefits payable to employee or corporation (Employee not as shareholder) 1. If employee owned and corporate paid. Premium included in employee’s income, deductible to employer, benefit non taxable to employee 2. If corporate owned and corporate paid. Premium not included in employees income deductible to corporation as business expense. Cash benefit not taxable to corporation if paid to employee taxable in income

Understanding The Taxation Of Critical Illness Insurance Grouped Individual policies providing Employee benefit Purpose Structure Tax Treatment Provides cash to an employee for 1. Medical costs 2. Pay down mortgage 3. Renovate home 4. Replace caregiver income The employee is the insured. Owner and payor is corporation. Benefits payable to corporation or owner. (Employee not as Shareholder) n If corporation pays on a number of corporate owned policies, premiums not included in employees income. n Premiums are a deductible expense to corporation. n Cash benefit paid to employee non - taxable to employee (Health and Welfare Trust)

Understanding The Taxation Of Critical Illness Insurance Grouped Individual policies providing Employee benefit Purpose Structure Tax Treatment Provides cash to an employee for 1. Medical costs 2. Pay down mortgage 3. Renovate home 4. Replace caregiver income The employee is the insured. Owner and payor is corporation. Benefits payable to corporation or owner. (Employee not as Shareholder) n If corporation pays on a number of corporate owned policies, premiums not included in employees income. n Premiums are a deductible expense to corporation. n Cash benefit paid to employee non - taxable to employee (Health and Welfare Trust)

Standard Group Benefit Coverages • Life Insurance • Accidental Death and Dismemberment • Dependant Life • Extended Health Care • Dental Care • Short Term Disability • Long Term Disability

Standard Group Benefit Coverages • Life Insurance • Accidental Death and Dismemberment • Dependant Life • Extended Health Care • Dental Care • Short Term Disability • Long Term Disability

WHAT’S MISSING?

WHAT’S MISSING?

Critical Illness Insurance, A Living Benefit Without Critical Illness Insurance, will your employees be forced to… Ü Ü Ü Deplete their RRSP’s? Increase their debt load? Rely on relatives? Pass the hat around the office? Forgo access to timely medical treatment?

Critical Illness Insurance, A Living Benefit Without Critical Illness Insurance, will your employees be forced to… Ü Ü Ü Deplete their RRSP’s? Increase their debt load? Rely on relatives? Pass the hat around the office? Forgo access to timely medical treatment?

Perspective Critical Illness helps refocus benefits back to providing for the most catastrophic events 3 Provides the opportunity to create a more “caring parent” environment and reduces the need to “pass the hat” around the office to help an employee dealing with a critical illness 3 Average person starting out in the workforce has a: 2. 1% chance of dying prior to age 65 20. 1% chance of having a critical illness diagnosis prior to age 65 It is not a question of “if”, but rather “when” 3

Perspective Critical Illness helps refocus benefits back to providing for the most catastrophic events 3 Provides the opportunity to create a more “caring parent” environment and reduces the need to “pass the hat” around the office to help an employee dealing with a critical illness 3 Average person starting out in the workforce has a: 2. 1% chance of dying prior to age 65 20. 1% chance of having a critical illness diagnosis prior to age 65 It is not a question of “if”, but rather “when” 3

Keeping Things in Perspective How Significant are the Following Events Your Clients Car is Stolen n Your Clients TV is Stolen n Your Clients Computer is Stolen n You Client is Diagnosed with Cancer n Your Client Dies n Rank the Significance of the Event on your clients family from 1 to 4, 4 being the greatest

Keeping Things in Perspective How Significant are the Following Events Your Clients Car is Stolen n Your Clients TV is Stolen n Your Clients Computer is Stolen n You Client is Diagnosed with Cancer n Your Client Dies n Rank the Significance of the Event on your clients family from 1 to 4, 4 being the greatest

What Does Your Client Currently Have Insured? Your Clients car n Your Clients TV n Your Clients Computer n Your Clients Life n The Diagnosis of Clients Critical Illness n

What Does Your Client Currently Have Insured? Your Clients car n Your Clients TV n Your Clients Computer n Your Clients Life n The Diagnosis of Clients Critical Illness n

How many of you have either a personal income replacement policy or Critical Illness Policy Please Stand Up

How many of you have either a personal income replacement policy or Critical Illness Policy Please Stand Up

Anyone who has applied for or has a Critical Illness Contract PLEASE SIT DOWN!

Anyone who has applied for or has a Critical Illness Contract PLEASE SIT DOWN!

Critical Illness Insurance Sample Costs for $100, 000 Benefit Female Age 55 $235. 79 monthly Female Age 40 $103. 22 monthly Female Age 50 $178. 37 monthly Female Age 35 $79. 19 monthly Female Age 45 $134. 72 monthly Female Age 30 $63. 89 monthly Calculations based on female non-smoker status, 12 months of non tobacco use

Critical Illness Insurance Sample Costs for $100, 000 Benefit Female Age 55 $235. 79 monthly Female Age 40 $103. 22 monthly Female Age 50 $178. 37 monthly Female Age 35 $79. 19 monthly Female Age 45 $134. 72 monthly Female Age 30 $63. 89 monthly Calculations based on female non-smoker status, 12 months of non tobacco use

CRITICAL ILLNESS RECOVERY PLAN Return of Premium on Death Included Male Age 42 Non-Smoker $100, 000 A 10 Year Renewable to age 75 B Level to Age 75 C Level for Life $683. 88 $1, 233. 96 $ 340. 92 $1, 574. 88 $1, 451. 88 $ 448. 92 $1, 900. 80 *(Optional Return of Premium) Age 52 $1, 672. 92 Age 62 $3, 566. 88 Age 72 $8, 004. 96

CRITICAL ILLNESS RECOVERY PLAN Return of Premium on Death Included Male Age 42 Non-Smoker $100, 000 A 10 Year Renewable to age 75 B Level to Age 75 C Level for Life $683. 88 $1, 233. 96 $ 340. 92 $1, 574. 88 $1, 451. 88 $ 448. 92 $1, 900. 80 *(Optional Return of Premium) Age 52 $1, 672. 92 Age 62 $3, 566. 88 Age 72 $8, 004. 96

CRITICAL ILLNESS RECOVERY PLAN Return of Premium on Death Included Female Age 42 Non-Smoker $100, 000 A 10 Year Renewable to age 75 *(Optional Return of Premium) Age 52 B Level to Age 75 C Level for Life $651. 96 $1, 049. 88 $ 399. 96 $1, 449. 84 $1, 274. 88 $ 423. 96 $1, 698. 84 $1, 344. 96 Age 62 $2, 427. 96 Age 72 $5, 797. 88

CRITICAL ILLNESS RECOVERY PLAN Return of Premium on Death Included Female Age 42 Non-Smoker $100, 000 A 10 Year Renewable to age 75 *(Optional Return of Premium) Age 52 B Level to Age 75 C Level for Life $651. 96 $1, 049. 88 $ 399. 96 $1, 449. 84 $1, 274. 88 $ 423. 96 $1, 698. 84 $1, 344. 96 Age 62 $2, 427. 96 Age 72 $5, 797. 88

IT’S ALL ABOUT…….

IT’S ALL ABOUT…….

CHOICE!

CHOICE!

Thank You! Al G. Brown & Associates Over 60 years of dedicated service

Thank You! Al G. Brown & Associates Over 60 years of dedicated service