4e3870dfa71847cc66a0b348273df60d.ppt

- Количество слайдов: 28

Chapter Seven Planning for Profit and Cost Control Mc. Graw-Hill/Irwin

Chapter Seven Planning for Profit and Cost Control Mc. Graw-Hill/Irwin

Three Levels of Planning • Strategic planning involves making long-term decisions such as defining the scope of the business, determining which products to develop, and identifying the most profitable markets. • Capital budgeting focuses on intermediate range planning and involves decisions such as whether to buy or lease equipment, whether to stimulate sales, or whether to increase investments in company assets • The Master Budget describes short-term objectives in terms of specific sales targets, production goals, and financing plans.

Three Levels of Planning • Strategic planning involves making long-term decisions such as defining the scope of the business, determining which products to develop, and identifying the most profitable markets. • Capital budgeting focuses on intermediate range planning and involves decisions such as whether to buy or lease equipment, whether to stimulate sales, or whether to increase investments in company assets • The Master Budget describes short-term objectives in terms of specific sales targets, production goals, and financing plans.

Advantages of Budgeting Promotes Planning Promotes Coordination Budgeting Enhances Performance Measurement Enhances Corrective Actions

Advantages of Budgeting Promotes Planning Promotes Coordination Budgeting Enhances Performance Measurement Enhances Corrective Actions

Budgeting and Human Behavior Upper management must be sensitive to the impact of the budgeting process on employees. Budgets are constraining. They limit individual freedom in favor of an established plan. Many people find evaluation based on budget expectations stressful. Think of students and exams. Upper management must demonstrate that budgets are sincere efforts to express realistic goals employees are expected to meet.

Budgeting and Human Behavior Upper management must be sensitive to the impact of the budgeting process on employees. Budgets are constraining. They limit individual freedom in favor of an established plan. Many people find evaluation based on budget expectations stressful. Think of students and exams. Upper management must demonstrate that budgets are sincere efforts to express realistic goals employees are expected to meet.

Cash Receipts and Payments Schedules Operating Budgets Start Pro forma Financial Statements Cash receipts Sales budget Income Statement Cash payments for inventory Inventory purchases budget Balance Sheet Cash payments for S & A expense budget Statement of Cash Flows Cash budget

Cash Receipts and Payments Schedules Operating Budgets Start Pro forma Financial Statements Cash receipts Sales budget Income Statement Cash payments for inventory Inventory purchases budget Balance Sheet Cash payments for S & A expense budget Statement of Cash Flows Cash budget

Sales Budget Detailed schedule prepared by the marketing department showing expected sales for the coming periods and expected collections on those sales. It is critical to the success of the entire budgeting process.

Sales Budget Detailed schedule prepared by the marketing department showing expected sales for the coming periods and expected collections on those sales. It is critical to the success of the entire budgeting process.

is preparing a sales budget for the last quarter") Sales Budget Hampton Hams (HH) is preparing a sales budget for the last quarter of the year. Ham sales are expected to peak in the months of October, November, and December (the holiday seasons). The store sales for October are expected to total $160, 000 ($40, 000 in cash sales, and $120, 000 in sales on account). Sales are expected to increase by 20% per month for November and December. Let’s prepare a sales budget.

Sales Budget Hampton Hams (HH) is preparing a sales budget for the last quarter of the year. Ham sales are expected to peak in the months of October, November, and December (the holiday seasons). The store sales for October are expected to total $160, 000 ($40, 000 in cash sales, and $120, 000 in sales on account). Sales are expected to increase by 20% per month for November and December. Let’s prepare a sales budget.

Sales Budget Accounts receivable at December 31 st are $172, 800, the uncollected sales on account. $40, 000 × 120% = $48, 000 $120, 000 × 120% = $144, 000

Sales Budget Accounts receivable at December 31 st are $172, 800, the uncollected sales on account. $40, 000 × 120% = $48, 000 $120, 000 × 120% = $144, 000

will collect cash sales in the month") Schedule of Cash Receipts Hampton Hams (HH) will collect cash sales in the month of sale. Past experience shows that the company will collect cash from its credit sales in the month following the month of the sale (October credit sales will be collected in full in November). Let’s prepare the cash receipts budget.

Schedule of Cash Receipts Hampton Hams (HH) will collect cash sales in the month of sale. Past experience shows that the company will collect cash from its credit sales in the month following the month of the sale (October credit sales will be collected in full in November). Let’s prepare the cash receipts budget.

Schedule of Cash Receipts Sales revenue on the income statement will be the sum of the monthly sales ($582, 400).

Schedule of Cash Receipts Sales revenue on the income statement will be the sum of the monthly sales ($582, 400).

Inventory Purchases Budget The total amount of inventory needed for each month is equal to the amount of the cost of budgeted sales plus the desired ending inventory.

Inventory Purchases Budget The total amount of inventory needed for each month is equal to the amount of the cost of budgeted sales plus the desired ending inventory.

Inventory Purchases Budget HH maintains a policy that ending inventory should be equal to 25% of the next month’s projected cost of goods sold. At HH, cost of goods sold normally equal 70% of sales. Suppliers require HH to pay 60% of inventory purchases in the month goods are purchased and the remaining 40% in the month after the purchase. Let’s prepare the inventory purchases budget and the schedule of cash payments for inventory purchases.

Inventory Purchases Budget HH maintains a policy that ending inventory should be equal to 25% of the next month’s projected cost of goods sold. At HH, cost of goods sold normally equal 70% of sales. Suppliers require HH to pay 60% of inventory purchases in the month goods are purchased and the remaining 40% in the month after the purchase. Let’s prepare the inventory purchases budget and the schedule of cash payments for inventory purchases.

Inventory Purchases Budget $134, 400 × 25% = $33, 600 $155, 960 × 40% = $62, 384 Accounts Payable

Inventory Purchases Budget $134, 400 × 25% = $33, 600 $155, 960 × 40% = $62, 384 Accounts Payable

$145, 600 × 60% = $87, 360 $145, 600 × 40% = $58, 240

$145, 600 × 60% = $87, 360 $145, 600 × 40% = $58, 240

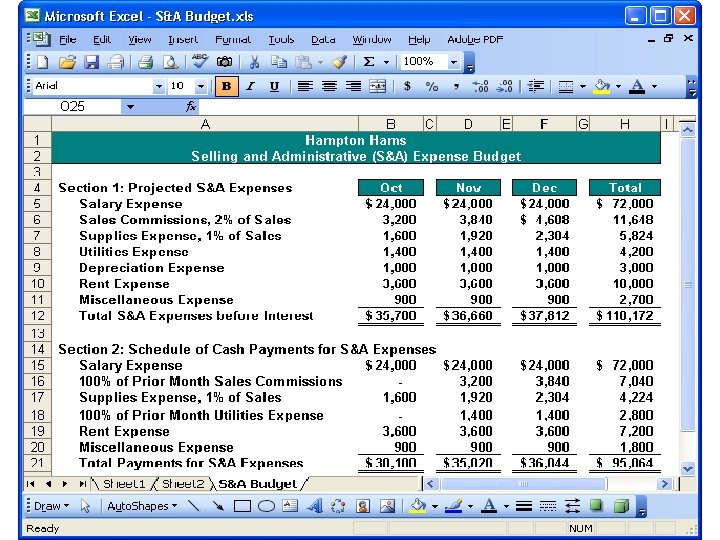

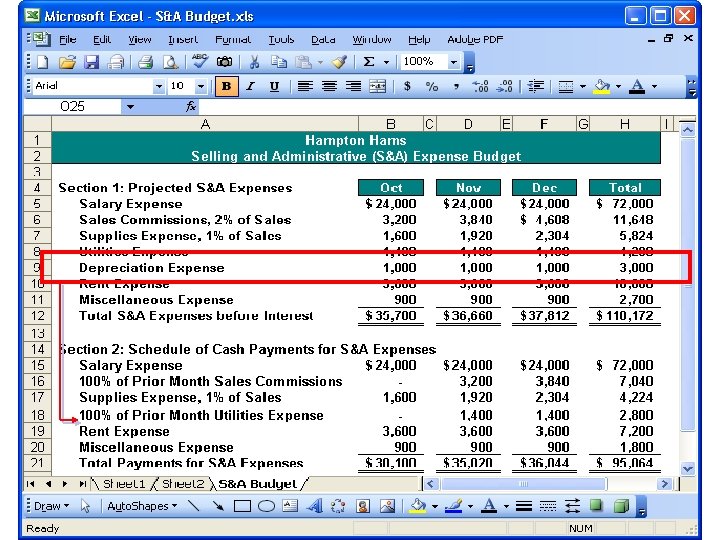

Budget") Selling and Administrative Expense Budget The details of the Selling and Administrative (S&A) Budget are shown on the next two screens. It is important to note that sales commissions (based on 2% of sales) are paid in the month following the sale, while supplies expense (based on 1% of sales) are paid in the month of the sale. The utility expense is paid in the month following the usage of the electricity, gas, and water.

Selling and Administrative Expense Budget The details of the Selling and Administrative (S&A) Budget are shown on the next two screens. It is important to note that sales commissions (based on 2% of sales) are paid in the month following the sale, while supplies expense (based on 1% of sales) are paid in the month of the sale. The utility expense is paid in the month following the usage of the electricity, gas, and water.

Selling and Administrative Expense Budget

Selling and Administrative Expense Budget

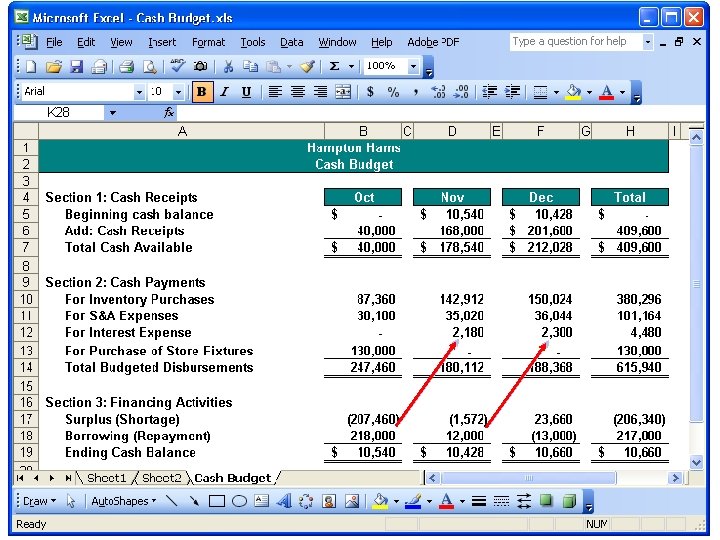

Cash Budget HH plans to purchase, for cash, store fixtures with a cost of $130, 000 in October. HH borrows or repays principal and interest on the last day of each month. Any monies borrowed from the bank bear interest at an annual rate of 12% (1% per month). The management at HH wants to maintain an end of month cash balance of at least $10, 000.

Cash Budget HH plans to purchase, for cash, store fixtures with a cost of $130, 000 in October. HH borrows or repays principal and interest on the last day of each month. Any monies borrowed from the bank bear interest at an annual rate of 12% (1% per month). The management at HH wants to maintain an end of month cash balance of at least $10, 000.

Cash Budget

Cash Budget

Cash Budget

Cash Budget

Check Yourself Astor Company expects to incur the following operating expenses during September: Salary Expense, $25, 000; Utility Expense, $1, 200; Depreciation Expense, $5, 400; and Selling Expense, $14, 000. It pays operating expenses in cash in the month in which it incurs them. Based on this information, the total amount of cash outflow reported in the Operating Activities section of the pro format Statement of Cash Flows would be: a. $45, 600. b. $31, 600. c. $40, 200. d. $44, 400 Depreciation Expense is a non-cash charge to income and will not appear on the Statement of Cash Flows.

Check Yourself Astor Company expects to incur the following operating expenses during September: Salary Expense, $25, 000; Utility Expense, $1, 200; Depreciation Expense, $5, 400; and Selling Expense, $14, 000. It pays operating expenses in cash in the month in which it incurs them. Based on this information, the total amount of cash outflow reported in the Operating Activities section of the pro format Statement of Cash Flows would be: a. $45, 600. b. $31, 600. c. $40, 200. d. $44, 400 Depreciation Expense is a non-cash charge to income and will not appear on the Statement of Cash Flows.

Pro Forma Income Statement The pro forma income statement gives management an estimate of the expected profitability of HH. If the project appears to be unprofitable, management can make the decision to abandon it. Although managers remain responsible for data analysis and decision making, computer technology offers powerful tools to asset in those tasks.

Pro Forma Income Statement The pro forma income statement gives management an estimate of the expected profitability of HH. If the project appears to be unprofitable, management can make the decision to abandon it. Although managers remain responsible for data analysis and decision making, computer technology offers powerful tools to asset in those tasks.

Pro Forma Income Statement Cost of Goods Sold: Beg. Inv. $0 Purchases $442, 680 CGAS $442, 680 End. Inv. $35, 000 COGS $407, 680

Pro Forma Income Statement Cost of Goods Sold: Beg. Inv. $0 Purchases $442, 680 CGAS $442, 680 End. Inv. $35, 000 COGS $407, 680

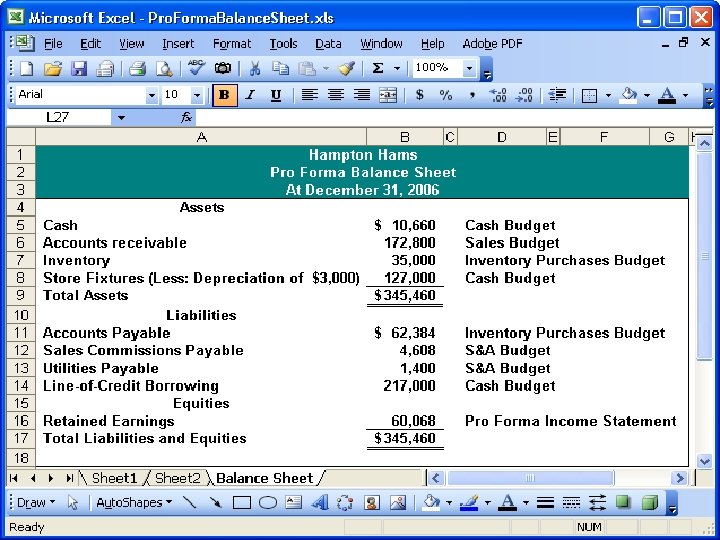

Pro Forma Balance Sheet This new store has no contributed capital because its operations will be financed through debt (line-ofcredit) and earnings. The amount of retained earnings will be equal to the net income because there are not prior periods. The fixtures purchased in October will be depreciated for a full three months. Total accumulated depreciation will be $3, 000.

Pro Forma Balance Sheet This new store has no contributed capital because its operations will be financed through debt (line-ofcredit) and earnings. The amount of retained earnings will be equal to the net income because there are not prior periods. The fixtures purchased in October will be depreciated for a full three months. Total accumulated depreciation will be $3, 000.

Questions? Mc. Graw-Hill/Irwin

Questions? Mc. Graw-Hill/Irwin