00908006511c446ff7b0cd2bc4f2563e.ppt

- Количество слайдов: 24

Chapter 5: The Open Economy

Chapter 5: The Open Economy

International Trade A country’s participation is measured by the value of its – export as a percentage of GDP – Import as a percentage of GDP Data indicate that while international trade is important in the U. S. , it is even more vital for other countries such as Canada and France.

International Trade A country’s participation is measured by the value of its – export as a percentage of GDP – Import as a percentage of GDP Data indicate that while international trade is important in the U. S. , it is even more vital for other countries such as Canada and France.

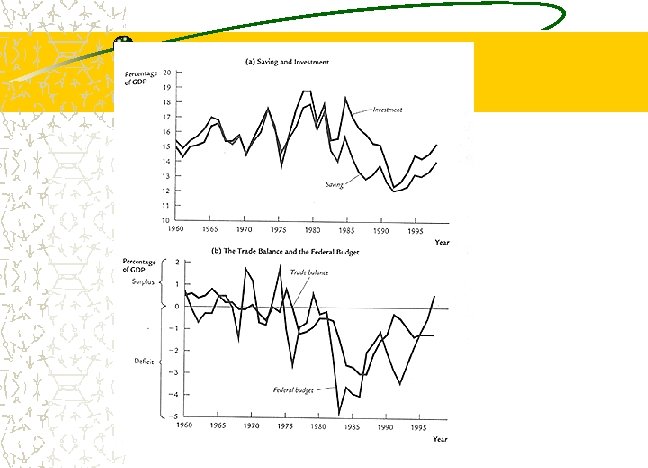

International Trade

International Trade

National Income Accounting The GDP for an open economy: Y = C + I + G + NX Consumption = C Investment = I Government purchases = G Net Exports = NX (Exports less Imports)

National Income Accounting The GDP for an open economy: Y = C + I + G + NX Consumption = C Investment = I Government purchases = G Net Exports = NX (Exports less Imports)

National Income Identity Y = C + I + G + NX Y – C – G = I + NX S = I + NX Where S = Y - C - G is National Savings

National Income Identity Y = C + I + G + NX Y – C – G = I + NX S = I + NX Where S = Y - C - G is National Savings

= NX Net") Saving Investment Identity Equilibrium in the product market: S – I(r) = NX Net Foreign Investment = Trade Balance If S>I: foreign capital outflow; hence NX>0: trade surplus If S

Saving Investment Identity Equilibrium in the product market: S – I(r) = NX Net Foreign Investment = Trade Balance If S>I: foreign capital outflow; hence NX>0: trade surplus If S

, reduces national savings (S = Y –") Twin Deficits The federal budget deficit (G>T), reduces national savings (S = Y – C – G) Reduced national savings foreign capital inflow, hence causing a trade deficit (NX<0) So, budget deficit causes trade deficit

Twin Deficits The federal budget deficit (G>T), reduces national savings (S = Y – C – G) Reduced national savings foreign capital inflow, hence causing a trade deficit (NX<0) So, budget deficit causes trade deficit

Saving Investment: Small Open Economy For a small open economy, r = r*, where r = domestic real interest rate r* = world real interest rate So, S – I(r*) = NX

Saving Investment: Small Open Economy For a small open economy, r = r*, where r = domestic real interest rate r* = world real interest rate So, S – I(r*) = NX

Determination of Real Interest Rate r NX>0 r* r S If r

Determination of Real Interest Rate r NX>0 r* r S If r

Fiscal Policy at Home Real interest rate S 2 r* S 1 An increase in G or a decrease in T results in a lower S. Now S

Fiscal Policy at Home Real interest rate S 2 r* S 1 An increase in G or a decrease in T results in a lower S. Now S

Fiscal Policy Abroad Real interest rate S r 2* NX<0 An increase in G or a decrease in T in the U. S. results in a higher r* causing S>I and a trade surplus. r 1* I(r*) Investment, Saving

Fiscal Policy Abroad Real interest rate S r 2* NX<0 An increase in G or a decrease in T in the U. S. results in a higher r* causing S>I and a trade surplus. r 1* I(r*) Investment, Saving

results in") Increase in Investment Demand Real interest rate S An increase in I(r*) results in S

Increase in Investment Demand Real interest rate S An increase in I(r*) results in S

Exchange Rate Nominal exchange rate = e: the relative price of the currency of two countries; e. g. , $1 = 120 yen or 1 yen = $0. 00834 Real exchange rate = ε: nominal exchange rate adjusted for the foreign price difference ε = e (P/P*) where P = domestic price level P* = foreign price level

Exchange Rate Nominal exchange rate = e: the relative price of the currency of two countries; e. g. , $1 = 120 yen or 1 yen = $0. 00834 Real exchange rate = ε: nominal exchange rate adjusted for the foreign price difference ε = e (P/P*) where P = domestic price level P* = foreign price level

Real Exchange Rate and Trade Balance ε NX<0 The lower the real exchange rate, the less expensive are domestic goods relative to foreign goods, thus the greater is the net export. NX>0 NX(ε) - 0 + NX

Real Exchange Rate and Trade Balance ε NX<0 The lower the real exchange rate, the less expensive are domestic goods relative to foreign goods, thus the greater is the net export. NX>0 NX(ε) - 0 + NX

Determinants of Real Exchange Rate Equilibrium value of ε is determined by: Net Foreign Investment = Trade Balance S – I = NX Here, the quantity of dollars supplied for net foreign investment equals the quantity of dollars demanded for the net export of goods and services.

Determinants of Real Exchange Rate Equilibrium value of ε is determined by: Net Foreign Investment = Trade Balance S – I = NX Here, the quantity of dollars supplied for net foreign investment equals the quantity of dollars demanded for the net export of goods and services.

I") Determinants of Real Exchange Rate ε S-I ε Equilibrium real exchange rate NX(ε) I

Determinants of Real Exchange Rate ε S-I ε Equilibrium real exchange rate NX(ε) I

Fiscal Policy at Home Real exchange rate S 2 - I S 1 - I ε 2 An increase in G or a decrease in T reduces S, shifting S-I line to the left. This shift causes ε to increase, but NX to decrease. ε 1 NX(ε) NX 2 NX 1 Net export

Fiscal Policy at Home Real exchange rate S 2 - I S 1 - I ε 2 An increase in G or a decrease in T reduces S, shifting S-I line to the left. This shift causes ε to increase, but NX to decrease. ε 1 NX(ε) NX 2 NX 1 Net export

Fiscal Policy Abroad Real exchange rate S 1 - I S 2 - I ε An increase in G or a decrease in T in the U. S. results in a higher r* causing I to decrease. This shift causes ε to decrease, but NX to increase 1 ε 2 NX(ε) NX 1 NX 2 Net export

Fiscal Policy Abroad Real exchange rate S 1 - I S 2 - I ε An increase in G or a decrease in T in the U. S. results in a higher r* causing I to decrease. This shift causes ε to decrease, but NX to increase 1 ε 2 NX(ε) NX 1 NX 2 Net export

Increase in Investment Demand Real exchange rate S – I 2 S – I 1 ε An increase in I shifts S-I line to the left. This shift causes ε to increase, but NX to decrease. 2 ε 1 NX(ε) NX 2 NX 1 Net export

Increase in Investment Demand Real exchange rate S – I 2 S – I 1 ε An increase in I shifts S-I line to the left. This shift causes ε to increase, but NX to decrease. 2 ε 1 NX(ε) NX 2 NX 1 Net export

Effect of Trade Protectionism Real exchange rate S-I ε Protectionism reduces the demand for imports, increasing net export. A higher NX line causes ε to increase, with no net change in net export. 2 ε 1 Here the value of foreign trade is unchanged because the rise in the real exchange rate discourages exports, which offsets the decline in imports. NX 1 = NX 2 NX(ε)1 Net export

Effect of Trade Protectionism Real exchange rate S-I ε Protectionism reduces the demand for imports, increasing net export. A higher NX line causes ε to increase, with no net change in net export. 2 ε 1 Here the value of foreign trade is unchanged because the rise in the real exchange rate discourages exports, which offsets the decline in imports. NX 1 = NX 2 NX(ε)1 Net export

, write e =") Determinants of Real Exchange Rate From ε = e * (P/P*), write e = ε (P*/P) Take percentage rate: %Δe = %Δε + %ΔP* - %ΔP %Δe = %Δε + ( * - ) Where ( * - ) is the difference in inflation rates of the two countries

Determinants of Real Exchange Rate From ε = e * (P/P*), write e = ε (P*/P) Take percentage rate: %Δe = %Δε + %ΔP* - %ΔP %Δe = %Δε + ( * - ) Where ( * - ) is the difference in inflation rates of the two countries

Inflation and Nominal Exchange Rate Countries with relatively high inflation tend to have depreciating currencies. Countries with relatively low inflation tend to have appreciating currencies.

Inflation and Nominal Exchange Rate Countries with relatively high inflation tend to have depreciating currencies. Countries with relatively low inflation tend to have appreciating currencies.

Inflation and Nominal Exchange Rate

Inflation and Nominal Exchange Rate